Embodied Intelligence: A Quest to Revitalize Intelligent Driving Manufacturers

06/03 2025

06/03 2025

540

540

After the capital markets' recent excitement over large models, investors are keen to capitalize on the burgeoning trend of embodied intelligence.

In the first quarter of 2025 alone, several companies including Zhipingfang, Vital Power, Fourier Intelligence, and Xinghaitu announced financing news, with individual amounts typically exceeding 100 million yuan. Notably, a Shanghai-based embodied intelligence startup, established just two months prior, completed a $120 million angel round of financing, setting a new record for the largest angel round in China's embodied intelligence industry.

The pursuit of embodied intelligence extends beyond internet giants and auto and home appliance industry leaders; intelligent driving manufacturers are increasingly venturing into this space. Recently, Zhixing Technology, the "first autonomous driving stock" on the Hong Kong Stock Exchange, plans to acquire a majority stake in Suzhou Xiaogongjiang Robotics through its wholly-owned subsidiary Aimoxing Robotics, becoming a controlling shareholder. Similarly, Youjia Innovation, another Hong Kong-listed company, has established a wholly-owned robotics subsidiary, Shenzhen Xiaozhu Robotics Technology Co., Ltd.

Theoretically, autonomous driving and embodied intelligence share a high degree of reusability in core technologies, allowing for the sharing of technological accumulations. This is the primary reason why intelligent driving manufacturers are branching into embodied intelligence. However, behind this collective shift lies a deeper industry dilemma, and embodied intelligence may not necessarily be the "salvation" for intelligent driving manufacturers.

Intelligent driving faces challenges, and prominent enterprises struggle to "stage a comeback."

On October 25, 2024, WeRide.ai listed on Nasdaq at an issue price of $15.5 per share, with a first-day increase of 6.8% and a market value of approximately $4.49 billion. However, just four days later, WeRide.ai's share price fell below the IPO issue price. As of April 30, WeRide.ai's share price plummeted to $6.70 per share, losing more than half of its value.

This is not an isolated case. Robotaxi operator Ruqi Chuxing broke its issue price on its first day of listing on the Hong Kong stock market, and Aurora's share price has fallen by 60% from its peak.

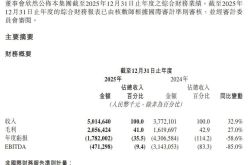

The high investment costs and the current lack of a clear path to profitability are direct reasons why autonomous driving enterprises like WeRide.ai are losing trust in the capital market. For instance, Horizon Robotics, known as "China's first autonomous driving stock," has accumulated losses of over 22 billion yuan in the past three and a half years. Leading enterprise Pony.ai has maintained revenue growth for three consecutive years, but behind this growth lies continuously expanding losses. In 2024, the net loss attributable to shareholders reached $274 million, an increase of 119.63% year-on-year.

According to an incomplete count by China Business News, nine out of ten major domestic intelligent driving enterprises are in a state of loss, with only one not disclosing financial statements, and its profitability remains unknown.

As competition in the autonomous driving industry shifts from technology validation to commercialization, the focus of the capital market has shifted from "story valuation" to "profit verification." This year, the wave of universal intelligent driving presents an excellent opportunity for these prominent enterprises.

Looking back at this year's auto shows and press conferences, a notable change is that autonomous driving companies, which were once behind the scenes, are now making a strong debut as "technical solution providers." Automakers are no longer shy about enhancing their intelligent driving capabilities through suppliers. For example, Chery has partnered with Lightboat Robotics, Great Wall has invested in Yuanrong Qixing, and among the partners of new forces such as NIO, XPeng, and Li Auto, external suppliers frequently appear. Even BYD, which emphasizes a "high self-sufficiency rate," has its Tianshen Eye A and B versions of intelligent driving solutions provided by Momenta.

Additionally, Japanese automakers represented by Toyota and Nissan, American automakers represented by General Motors, and German automakers represented by Audi and Mercedes-Benz have all fully embraced Chinese intelligent driving companies.

This change means that after attempting self-research, many automakers have adjusted their strategic positioning and restarted cooperation with leading intelligent driving suppliers, creating conditions for the latter's large-scale commercialization. However, a safety incident triggered a public opinion storm, abruptly halting universal intelligent driving. Multiple parties, from enterprises to the industry and regulatory authorities, have stepped on the "brake" for intelligent driving of new energy vehicles in China.

At the Shanghai Auto Show, which should have been a grand display of intelligent driving solutions and achievements, automakers without "intelligent driving" were overshadowed by robots.

For the intelligent driving or autonomous driving industry, although constraints on marketing and promotion will not hinder the penetration of intelligent driving in the field of new energy vehicles, this sudden brake has made safety a top priority. This may change the focus of competition among automakers and technology suppliers. At least for now, to meet safety requirements, they will inevitably need to incur more costs. For enterprises already in continuous losses, the cost pressure has increased.

While the narrative is promising, embodied intelligence may also "empty" intelligent driving.

Besides leading manufacturers like Zhixing Technology, other players across the entire intelligent driving industry chain are also entering this field. For instance, Black Sesame Technology's annual report shows that it is verifying and expanding its product mass production to commercial vehicles, special vehicles, vehicle-road-cloud integration, and humanoid robots. Livox Technology, a leading lidar manufacturer, has signaled its entry into the humanoid robot race since last year and has begun to clearly position itself as a robot technology platform supplier.

Auto giants have long been deploying forces in the robotics field, with some showing more enthusiasm than others.

The surge in the embodied intelligence boom, coupled with the entry of internet giants, has made this track unprecedentedly popular. Intelligent driving enterprises, as cross-border players, have received particular attention. The high degree of reusability of underlying AI technology between autonomous driving and embodied intelligence has filled the outside world with expectations for the application of leading intelligent driving manufacturers' technology in the field of humanoid robots. The capital market is more willing to see new stories.

However, risks coexist. When more and more intelligent driving manufacturers try to find new growth from the embodied intelligence track and blindly increase investment, they may not only fail to gain growth but may also continue to plunge the enterprise into a quagmire where input and output are difficult to be proportional.

Embodied intelligence is also a money-burning track. Taking "the first humanoid robot stock" UBTECH as an example, it has been in a state of "living beyond its means," losing a cumulative total of 4.96 billion yuan in five years, with R&D investment accounting for a high proportion for consecutive years.

For intelligent driving-related enterprises that have also been in long-term losses, funds have already become a problem. For example, WeRide.ai's total R&D and operating expenses in 2024 reached 2.284 billion yuan, with a net loss of 2.517 billion yuan for the year. At this rate, its cash reserves of 4.888 billion yuan can only support less than two years. If funds are dispersed into new tracks or debt is increased for new tracks, long-term high investment will inevitably exacerbate the enterprise's capital chain crisis. Moreover, once there are large fluctuations in the company's revenue, it is likely to reach a dead end.

Zongmu Technology is the most direct example. In 2022, Zongmu Technology established Cancong Robotics in Shanghai, planning to implement L4 technology in the field of energy storage. In 2024, Cancong Robotics launched the autonomous driving charging robot FlashBot, but things did not go as planned. The market response to Cancong Robotics' products was lukewarm, occupying the cash flow required for its main business.

In 2021, 2022, and 2023, Zongmu Technology's net operating cash outflows were 476 million yuan, 588 million yuan, and 411 million yuan, respectively. As of January 31, 2024, Zongmu Technology had 462 million yuan in borrowings but only 199 million yuan in cash and cash equivalents. What made the company's situation worse was that Thalys' orders were "intercepted," and after Changan began self-research, it also kicked Zongmu out of the core supply chain, severely impacting its main business. Under this heavy blow, this prominent enterprise collapsed suddenly.

Intelligent driving manufacturers entering the embodied intelligence track not only need to disperse funds but also human resources. However, the fierce talent competition among the intelligent driving, embodied intelligence, and new energy vehicle industries seems to make intelligent driving manufacturers become "tools" for delivering talent. When talent flowing from intelligent driving to embodied intelligence becomes a "hotcake" in the eyes of other enterprises, intelligent driving manufacturers may face a more serious brain drain.

A former employee of TuSimple Future said that autonomous driving companies do not offer much, basically requiring a salary reduction or flat salary upon entry, while robot companies, the internet, and even automakers doing L2 levels offer more attractive packages.

"After cooperating on a project with an intelligent driving enterprise, both sides become familiar, and the automaker can directly hire people at high salaries and use them immediately," revealed an intelligent driving R&D personnel from another leading automaker.

Embodied Intelligence: Half Prosperity, Half Empty Heat

Conceptually, embodied intelligence integrates artificial intelligence into physical entities such as robots, endowing them with the ability to perceive, learn, and interact dynamically with the environment. Intelligent driving, with automobiles as the carrier, can be said to be the earliest and currently the most mature form born within this conceptual category. Therefore, crossing over from autonomous driving to embodied intelligence seems to be a straightforward choice for intelligent driving manufacturers.

But ultimately, without the boom in embodied intelligence, there would not have been the scene of intelligent driving manufacturers entering the field one after another.

According to CVSource, as of March 29, the number of financing events in the robotics track this year has reached 102, far exceeding the 75 in the same period last year. Among them, there have been more than 20 financing events involving humanoid robots/embodied intelligent robots, compared to less than 10 in the same period last year.

Amid the surge of enthusiasm, the highly sought-after robotics company Unitree Robotics' old share transfer has seen premium snatching in the market, with some investors competing for its equity at a valuation of 10 billion yuan. Moreover, a certain humanoid robotics company in the Greater Bay Area is rumored to have seen its valuation increase by 1 billion yuan within two weeks, with investment institutions still enthusiastic. However, the pursuit of capital has infinitely amplified the market imagination of embodied intelligence, especially humanoid robots, resulting in bubbles.

A set of data shows that the market size of humanoid robots in China was only 2.76 billion yuan in 2024, but the financing amount reached 5 billion yuan, with a valuation bubble far exceeding actual demand.

While intelligent driving manufacturers crossing into embodied intelligence are not competing directly with the already somewhat crowded robotics companies on this track, as technology suppliers, the authenticity of market demand is crucial for the robotics business to truly support business growth. The applicability in new scenarios is even more related to the implementation of technology. However, from the current perspective, the market demand for humanoid robots has not been successfully and truly verified.

On the one hand, there is a continuous announcement of news, setting off a wave of orders; on the other hand, there are almost no return customers after the novelty wears off in the rental market.

Behind this lies the fact that the commercialization path for humanoid robots is not yet clear. In industrial scenarios, automakers prefer to use robotic arms or AGVs (Automated Guided Vehicles) due to their low cost and high stability. Household scenarios face ethical and safety controversies – Japan's SoftBank Pepper robot was resisted by many countries due to privacy leakage issues. Even in the field of education, the practicality of humanoid robots is highly questioned.

Robots do not lack applicable scenarios, but under the current technological maturity, scenario demand does not equal real demand. Moreover, many business stories are born to cater to capital.

For the track of humanoid robots or embodied intelligence, whether it revolves around true or false demands, it may bring growth momentum. However, for enterprises, once they bet on false demands, long-term high investment without returns is likely to drag them down, especially for cross-border intelligent driving manufacturers. Under the premise that their own main business is struggling to solve the commercialization dilemma, betting on embodied intelligence is also a huge gamble.

Whether the outcome is "life extension" or "life taking" remains to be seen.

Dao Zong You Li, previously known as Waidaodao, stands as a pioneering new media platform within the realm of internet and technology. This article is authored exclusively for Dao Zong You Li, and any form of republication without proper attribution to the author is strictly prohibited.

-

From 'CiYuan' to 'FuYuan': The Debate on AI's Fundamental Cognition Behind the Chinese Name for 'Token'", "Token, CiYuan, FuYuan, naming, symbol", "The National Committee for Terms in Sciences and Tec

-

![]()

New Energy Vehicle Market Transformation: The Early Onset of the 'Series 9' Showdown

-

![]()

What on earth is a 'World Model'? OpenWorldLib settles it once and for all: Perception + Interaction + Memory—that's what defines an AI capable of understanding the world!

-

![]()

Chinese EVs Make Waves in Europe! Q1 Market Share Tops 21%, BYD Breaks into Top 5, Leapmotor Soars | MIRROR Pro

-

Don't doubt it, it has the potential to become one of the largest, most unique, and most intelligent companies in the world

-

![]()

The Camera at Your Doorstep: From a ‘Dumb Recorder’ to a ‘Modern-Day Sherlock Holmes’

-

![]()

Cost Reduction Fails to Secure Real Profitability: The Hard Battle of SenseTime's Transformation Has Just Begun

-

![]()

OpenClaw Ecosystem Endgame: From 'Big Players Dominate' to 'Tropical Rainforest'