YU7 Launch: Xiaomi's Market Value Soars to 1.6 Trillion, Where Lies the Future Ceiling?

06/27 2025

06/27 2025

832

832

This article is based on publicly available information and is intended solely for informational purposes, not constituting investment advice.

Produced by|Company Research Room

On the evening of June 26, Xiaomi Group held a highly anticipated new product launch event. At the event, the pricing for Xiaomi's latest model, the YU7, was officially unveiled: starting at RMB 253,500.

Immediately following the announcement, Xiaomi YU7's large order data (a non-refundable RMB 5,000 deposit automatically locked after 7 days) surpassed 200,000 units within three minutes and reached over 289,000 units within an hour.

"I'm thrilled to see such an overwhelming response, far exceeding my initial expectations," Lei Jun, CEO of Xiaomi, enthused in a post-event interview.

That night, Xiaomi Group's American Depositary Receipts (ADR) witnessed a peak increase of nearly 12%.

However, the following day, when A/H shares opened, both Xiaomi Group's Hong Kong shares (01810.HK) and A-share Xiaomi concept stocks opened higher but closed lower, recording negative lines. This indicated that some investors took advantage of the positive news of Xiaomi's new car launch to lock in profits.

An industry insider acknowledged that Xiaomi Group's stock price has surged over 70% since the beginning of the year, with short positions amounting to 349 million shares and intense competition between foreign and domestic capital. Many investors are concerned that Xiaomi's stock price may have peaked following the YU7 launch.

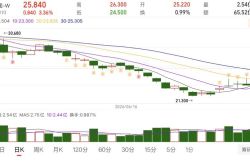

Since its listing in July 2018, Xiaomi Group's valuation has been a subject of significant controversy in the capital market, leading to significant fluctuations in its stock price.

This is evident from Xiaomi Group's monthly K-line chart.

Looking back, Xiaomi Group's positioning in the capital market has undergone three distinct transitions.

1.0 Era (2018-2020): Hardware Manufacturer Label.

During this period, Xiaomi Group was primarily perceived as a "cost-effective smartphone manufacturer," with internet services accounting for less than 10% of its revenue. Its average selling price (ASP) was only RMB 997, earning it criticism as an "assembly plant" with low technical barriers. This perception posed a "bottleneck" in its valuation, with the market pegging its PE ratio at 15-20 times. Consequently, Xiaomi's stock price fell from an initial listing high of HK$22.2 per share to below HK$10, reaching a low of HK$8.28. It is said that a female shareholder even "scolded" Lei Jun for about an hour after the stock price fell below the issue price.

2.0 Era (2021-2024): Transition to Technology-Driven Smart Manufacturing.

During this phase, Xiaomi's ASP for high-end smartphones surpassed RMB 3,500 (with the Xiaomi 15 starting at RMB 4,499), and it captured a 22.6% market share in the RMB 4,000-5,000 price range. The company boasted over 40,000 technical patents, including self-developed Xuanjie O1 chips and super motors V8s (27,200 rpm). This breakthrough led to a reevaluation of Xiaomi's valuation anchor: the PE ratio increased to 25-30 times, benchmarking technology hardware companies. As a result, Xiaomi's stock price rose from around HK$10 to around HK$35.

3.0 Era (2025 onwards): Full-Scene Ecological Platform.

In March 2024, Xiaomi released its first car model, the SU7, bringing its smartphone expertise into the electric vehicle realm. As Xiaomi SU7 shipments increase in 2025, the Pengpai OS integrates smartphones, cars (SU7/YU7), and smart homes (900 million devices), creating a closed loop between people, cars, and homes. Simultaneously, the behavior data of 674 million MIUI users trains the HyperMind system, enabling precise service push notifications. This upgrade of the human-car ecosystem has also ushered in a new qualitative shift in Xiaomi's valuation logic: transitioning from a hardware PE model to a SaaS model based on "terminal entry × ecological services × data value" (similar to internet businesses enjoying a 30-times PE).

Riding on the wave of revaluation of Chinese assets since the beginning of the year, Xiaomi Group has emerged as a key target for overseas capital and southbound funds, with its stock price surging over 70%.

As Xiaomi's stock price climbs, some investors are starting to worry about a potential peak. The launch of the YU7 new car presents them with an opportunity to sell at a high price.

Currently, investors' concerns about Xiaomi's stock price stem primarily from short-term technical adjustments and future business risks. Besides the lingering shadow of previous vehicle safety incidents, the market is most concerned about Xiaomi's car delivery capacity: the backlog of SU7 orders exceeds 100,000 units, and the planned second-phase production of the factory did not commence in the middle of the year. If YU7 shares the production line, it may exacerbate delivery delays and trigger cancellation risks (current cancellation rate is about 40%).

However, many observers have noted that "the launch of YU7 is merely a phased stress test for Xiaomi's automotive business." Such investor concerns have not undermined Xiaomi Group's long-term growth trajectory: YU7, as an SUV model targeting family users, forms a "sedan + SUV" dual matrix with SU7, potentially replicating Tesla's Model 3/Y incremental logic (Tesla's dual-car strategy drove a 38% sales increase in 2023).

These observers believe that Xiaomi's ultimate battlefield is not in the sales volume of a single product but in reshaping users' living scenarios with ecological stickiness. When cars become mobile smart home control towers, smartphones transform into health managers, and home appliances automatically respond to travel plans, the scarcity of this "seamless interconnection" experience is Xiaomi's true competitive advantage in challenging Apple and Tesla.

They contend that after transitioning from a "hardware traffic entry" to a "scenario definer," Xiaomi's next ambition is to become a "standard setter" (such as unifying charging protocols and open-sourcing OS). If this is achieved, Xiaomi Group's valuation still holds considerable upside potential.

Some insiders estimate that Xiaomi Group's current market value is HK$1.54 trillion (approximately RMB 1.41 trillion), significantly lower than its divisional aggregate valuation of RMB 2.13 trillion (smartphones: RMB 500 billion + cars: RMB 287.5 billion + IoT: RMB 240 billion + internet: RMB 1.1 trillion). Therefore, its reasonable value range is estimated to be between RMB 2.1 and 2.5 trillion.

Of course, this valuation is static and needs to dynamically incorporate production capacity risk discounts (-15%) and technology breakthrough premiums (+30%). In other words, the potential valuation ceiling for Xiaomi Group in the future could be around a total market value of RMB 3 trillion.

-

![]()

Weekly Stock Review | Who Dominates the Market: Hedge Funds, Quant Traders, Institutions, or Hot Money?

-

![]()

Sales Slump Again: Why Are Affluent Buyers No Longer Exclusively Opting for Porsche?

-

![]()

Xiaomi’s New Auto Brand Launch Sparks Stock Rebound: Is a Trend Reversal on the Horizon?

-

![]()

Seres Mid-Year Report Catastrophe: Projected Losses Surpass 1.5 Billion Yuan!

-

![]()

"Fruit Chain Brother No.1" Plummets Below Issue Price on Debut Trading Day! Chaoshan's Wealthiest Woman Stakes HK$24 Billion on AI

-

![]()

Auto Market Undergoes Major Shake-Up: Winners and Losers Revealed

-

![]()

The Successful Recovery of the First Stage of the Long March 10B: What Does It Mean for China's Commercial Space Industry?

-

![]()

Xiaomi Pengcheng: Crafting the Future of Mobility