Zeekr and Lynk & Co. Merge: The Era of Automotive Industry "Integration" Dawns

02/20 2025

02/20 2025

546

546

Author / Chen Buqi

Produced by / Jieche Technology

"The strategic importance of the merger between Zeekr and Lynk & Co. for the holding group lies in elevating the brand beyond mere price wars. We must rely on our technology, products, and quality competitiveness to forge a strong brand and compete in the market." An Conghui, President of Geely Holding Group and CEO of Zeekr Technology Group, stated in an interview on February 14.

After a three-month process, the merger between Zeekr and Lynk & Co. has been finalized.

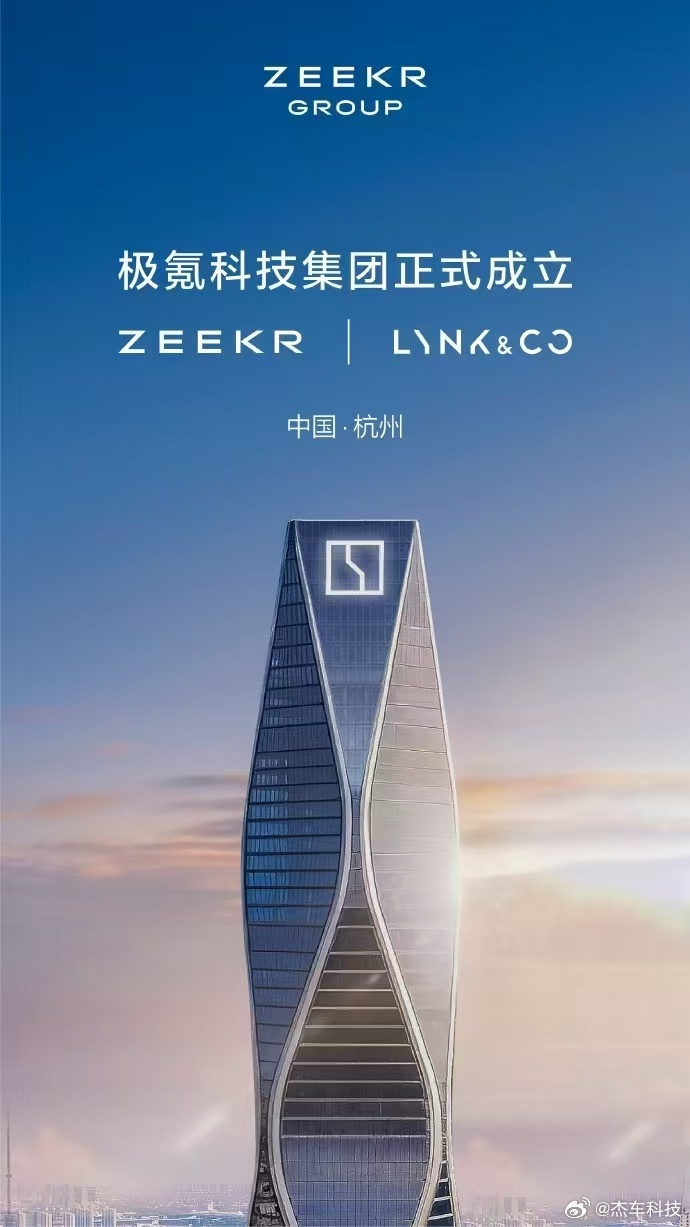

On February 14, Zeekr and Geely Automobile announced the completion of Zeekr's acquisition and capital injection into Lynk & Co. Post-transaction, Zeekr holds a 51% stake in Lynk & Co., with the remaining 49% continuing to be held by a wholly-owned subsidiary of Geely Automobile, making Lynk & Co. an official non-wholly-owned subsidiary of Zeekr. Simultaneously, the Zeekr Technology Group was announced, encompassing two major brands: Zeekr and Lynk & Co.

Lynk & Co.'s name will not vanish with its integration into the Zeekr Technology Group. The group will adhere to a dual-brand strategy, clearly distinguishing between the two brands. Zeekr targets the market above 300,000 yuan, focusing on medium and large vehicles, with medium-sized vehicles prioritizing pure electric and large vehicles focusing on super electric hybrids. Lynk & Co., meanwhile, aims at the market above 200,000 yuan, with small vehicles emphasizing pure electric and medium to large vehicles focusing on hybrids.

The "merger" of Zeekr and Lynk & Co. is not surprising. As the penetration rate of new energy vehicles rises, competition in the Chinese automotive market intensifies. The past strategy of "more children to fight better" is waning, with cost control, technological innovation, and integration becoming the core of industry competition. Both in-house brands within a group and independent automakers cannot escape the trend of unified collaboration.

The earliest mention of the Zeekr-Lynk & Co. merger can be traced back to the "Taizhou Declaration." In September 2024, Geely Holding Group released the "Taizhou Declaration" at the Taizhou International Auto Industry Expo, announcing a new stage of strategic transformation. The group would foster sustainable corporate development through five initiatives: "strategic focus, strategic integration, strategic synergy, strategic robustness, and strategic talent."

On November 14 of the same year, Geely Holding Group announced the optimization of Zeekr and Lynk & Co.'s shareholding structures, stating its commitment to promoting deep integration and efficient fusion of internal resources. As one of 2024's most notable automotive industry events, it signified the automotive market's entry into a fierce battlefield necessitating "huddling together for warmth."

Why did Zeekr and Lynk & Co., two established brands, choose to merge? In An Conghui's words, "Before the merger, there were product overlaps and duplicate investments in R&D resources. These issues prompted our decision to merge."

From a product perspective, Lynk & Co.'s initial foray into the pure electric market with the Z10 did not achieve the intended goal of competing with Xiaomi's SU7 alongside the Zeekr 001 and 007, as envisioned by Geely Holding Group. Instead, due to their similar appearances and positioning, the Z10 and 001 had internal conflicts. This issue also arose between the Lynk & Co. Z20 and Zeekr X. Overlapping product positioning and duplicate R&D costs became primary factors hindering brand harmony, making merger and integration inevitable.

"After the Lynk & Co.-Zeekr merger, a platform-based strategy will emerge. Both brands will utilize Zeekr's self-developed advanced intelligent driving system. For Lynk & Co., the Lynk & Co. 900 will be the first to adopt Zeekr's HaoHan intelligent driving system and the latest NVIDIA Thor chip," said An Conghui. With the Zeekr Technology Group's establishment, technological barriers between Zeekr and Lynk & Co. will dissolve, leveraging each brand's strengths. Besides reducing R&D costs through technology sharing, the merger's excellent cost control will also benefit procurement, marketing, services, and logistics.

Post-merger, the integrated Zeekr Technology Group will achieve full coverage of core technologies, possessing full-stack self-research and innovation capabilities combining software and hardware for industrial chain core technologies. Simultaneously, it will yield significant benefits in cost reduction and resource optimization, with anticipated savings of 10% to 20% in R&D investment, dropping the R&D expense ratio from 11% to 6%, 3% to 5% in production and manufacturing savings, and 10% to 20% in management expenses.

According to official announcements, the newly formed Zeekr Technology Group positions itself as a high-end luxury new energy automotive group, aiming to produce and sell one million vehicles within two years. The successful merger of Zeekr and Lynk & Co. sets a positive precedent for automotive industry "integration."

Since last year, domestic traditional automakers have successively embarked on brand integration.

In October 2024, Great Wall Motors' ORA announced that the ORA App would be removed from various app markets at the start of December, with all subsequent services migrating to the Great Wall Motors App. Then, on February 8 of this year, Zhao Yongpo, General Manager of Haval Automobile, announced on social media that he would manage both the Haval and ORA brands.

Behind this personnel change lies Great Wall Motors' reevaluation of its brand architecture. Data shows that ORA's wholesale sales in 2024 were 63,300 units, a 41.69% year-on-year decline from 2023, making it Great Wall Motors' sub-brand with the steepest sales drop. In January 2025, ORA sold only 2,193 units, a 63.46% year-on-year decline. In the current new energy vehicle boom, such market performance is surprising. With no new models launched since 2023, ORA has become a "neglected child" of Great Wall Motors.

Merging with other Great Wall Motors sub-brands may help ORA reduce R&D and operating costs, redefine its market positioning, and accelerate new model launches leveraging other brands' mature channels and organizational structures.

Similarly, when Geely Holding Group announced the optimization of Zeekr and Lynk & Co.'s shareholding structures, SAIC Motor Passenger Vehicle Company officially announced the merger of the Roewe and Feifan brands. This marks Feifan Automobile's official return to SAIC Motor Passenger Vehicle Company after "repeatedly hitting a wall" post-independent operation.

Yu Jingmin, Executive Deputy General Manager of SAIC Motor Passenger Vehicle Company, revealed that integrating Feifan and Roewe's marketing and service organizations will be a future focus, with an expected 100 Roewe-Feifan dealer stores opening by 2024's end, achieving efficient resource allocation. Besides adjustments to Feifan, this merger also involves streamlining the Roewe brand's product line. Currently, Roewe sells fuel vehicles, plug-in hybrids, pure electrics, sedans, SUVs, MPVs, and other power forms across multiple market segments, comprising a complex matrix. Thus, Feifan and Roewe's integration will also involve repositioning the brands and product lines.

Entering 2025, news of Dongfeng and Changan's planned merger and reorganization caused significant buzz. On February 9, listed companies from the "Dongfeng Series" (Dongfeng Motor Corporation, Dongfeng Technology) and the "Arms Equipment Series" (Changan Automobile, Dongan Engine) nearly simultaneously announced that their indirect controlling shareholders were planning reorganization with other state-owned and central enterprises. This sparked speculation that Changan and Dongfeng, two major automotive groups, might restructure.

Looking back at 2024, Changan Deep Blue experienced a sales surge at year-end, with Changan Mazda and Changan Ford also achieving positive growth. Conversely, Dongfeng Group saw no improvement in Lantu sales, with the Eitra brand engaging in internal competition with other sub-brands, and both "cash cows" Dongfeng Honda and Dongfeng Nissan witnessing sales declines. A Changan-Dongfeng merger could directly reduce market competition and produce a 1+1>2 effect in R&D costs, procurement prices, and technological innovation.

Overall, traditional automakers' brand integration is not merely a passive response to market pressure but a strategic move to actively optimize resources and enhance competitiveness. With the new energy market's rapid development and consumer demand diversification, automakers' brand integration and resource allocation optimization will help them secure a more favorable position in future market competition. However, balancing brand positioning and avoiding internal competition during integration remains a critical challenge for automakers.

-

![]()

Li Bin Claims, 'Denying the Pure EV Trend is Like Ostrichism.' What's Li Xiang's Take?

-

Lenovo: Liu Jun Turns Left, Yang Yuanqing Turns Right

-

Lenovo: Liu Jun Goes Left, Yang Yuanqing Goes Right

-

![]()

MiniMax Shares Unlock: Cornerstone Shareholders Show Long-Term Optimism, Yet Stock Plummets Nearly 30% in Two Days; Zhipu Also Sees Nearly 20% Drop Today

-

![]()

Single-Day Plunge of 40%: The 'First AGI Stock' Faces More Than Just Share Price Concerns

-

![]()

Ricoh and Fuji Hike Prices on Legacy Edge; Insta360 Poised to Disrupt Mirrorless Camera Market

-

![]()

Ricoh and Fujifilm Raise Prices in Tandem, Relying on Established Reputations; Insta360 Poised to Disrupt Mirrorless Camera Market

-

![]()

Strategic Shift in Photoelectric Sensing: Maxvision Secures Controlling Stake in CAS Optotech