Unitree's IPO Approaches, but the Final Battle for Humanoid Robots is Far from Over

04/03 2026

04/03 2026

530

530

Unitree's Key to Success or Failure

As Unitree Technology's IPO approaches, the drumbeats of war have officially sounded in China's—and indeed the global—robotics industry. The focus of the race has abruptly shifted from the 'positioning battle' for traditional industrial robots to the 'final showdown' in the vast expanse of humanoid robots. The years 2025-2026 are widely seen as the critical inflection point from 'torso awakening' to mass production, and Unitree's listing is undoubtedly the most significant footnote to this technological battle.

More critically, the capital market's support for tech-innovation enterprises is unprecedented. This is evidenced by two waves of IPOs from late 2025 to early 2026. By late 2025, after 'China's first domestic GPU stock' Moore Threads went public on the A-share market, four domestic GPU companies—Moore Threads, MetaX, Biren Technology, and Illuvatar CoreX—went public in rapid succession within just 35 days, with their shares surging over sevenfold on the first trading day. In January 2026, large language model companies Zhipu and MiniMax successively listed on the Hong Kong Stock Exchange, each briefly exceeding a market capitalization of HK$300 billion, even surpassing established internet giant JD.com.

Image Source: Internet

So, how much should Unitree Technology—long regarded as the 'pacesetter' in humanoid robots—be valued, and how many will profit from this feast? Many investors believe the first wave of embodied AI companies can be compared to previous domestic chip and large language model listings, with 'market capitalizations quickly inflated.'

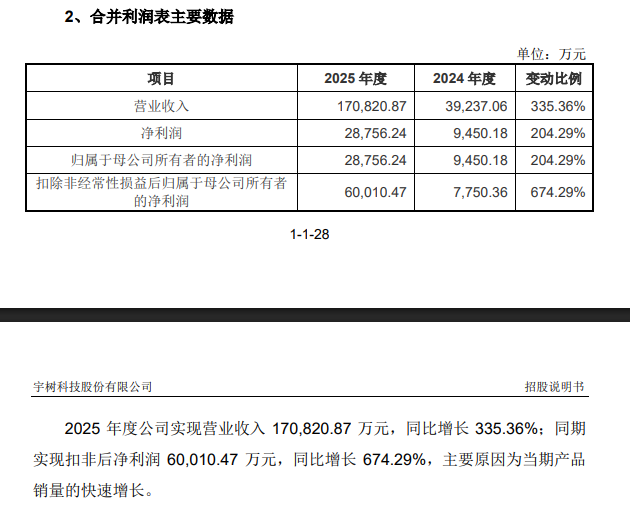

Objectively, Unitree's prospectus is highly impressive. In terms of performance, Unitree achieved profitability in 2024 and became the global leader in humanoid robot shipments in 2025, with annual revenue reaching RMB 1.708 billion, a year-on-year surge of 335.36%, and non-GAAP net profit exceeding RMB 600 million. The gross margin for humanoid robots remained stable above 60%. In hardware manufacturing, Apple's 46% gross margin was once considered an insurmountable 'ceiling.'

Image Source: Unitree Technology's Prospectus

Does this mean Unitree has completed the final answer to commercialization? The answer may not be so simple. While Unitree is indeed a first-tier leader, it still falls short of the expected scale of commercialization and closed-loop mass production.

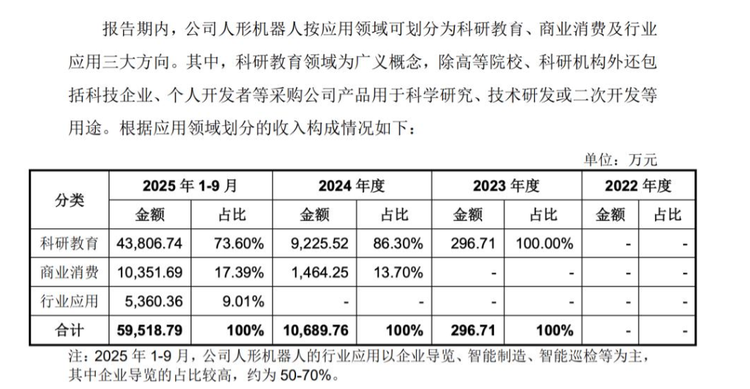

According to the Shanghai Stock Exchange's disclosure of Unitree's inquiry response, research and education remain the core application scenarios for Unitree's humanoid robots. In the first three quarters of 2025, revenue from research and education accounted for 73.6% of total humanoid robot revenue, with commercial consumption at 17.39% and industrial applications just 9.01%.

Image Source: Unitree Technology's Response to Inquiry

Within this less-than-10% industrial application revenue, over half comes from demonstration scenarios like exhibition hall guides. Actual sales revenue in core industrial scenarios such as smart manufacturing, industrial inspections, and logistics delivery amounted to just RMB 15.702 million, accounting for only 2.6% of total humanoid robot sales.

Nearly all well-known brands have vied for exposure on the CCTV Spring Festival Gala in recent years, but what goes unsaid is the difficulty in converting that exposure into lasting engagement. The H1 robot's performance at the 2025 CCTV Spring Festival Gala achieved phenomenal viral spread, but follow-up tracking revealed that this exposure primarily translated into brand awareness rather than commercial orders. The high development costs and low replicability of customized performance projects limited their contribution to profitability; while technical inquiries from potential clients increased, the conversion rate to actual purchases was less than 10%.

Image Source: Internet

An industry insider told us that a deeper issue lies in the ambiguity of the product's value proposition. For enterprise clients, procuring humanoid robots requires clear ROI calculations: how much labor will be replaced, how much efficiency improved, how much risk reduced, and the payback period. Currently, Unitree's products are less efficient than skilled workers in most scenarios, lack the reliability for continuous operation, and have higher comprehensive costs than the benefits of labor replacement.

However, the industry generally recognizes Unitree's leading position, as having a large order book and partnerships with high-quality supply chain enterprises is crucial for commercialization hopes. Competition in humanoid robots exhibits clear 'winner-takes-most' characteristics. According to the Humanoid Robot Scene Application Alliance, China's humanoid robot market will exceed RMB 9 billion in 2025, with the top five firms accounting for nearly 60% of the market (CR5) and the top eight accounting for 76% (CR8). This highly concentrated market structure means leading firms have established significant barriers in R&D, supply chain integration, and customer resources, while smaller players face dual bottlenecks in cost control and mass production.

The 'Hundred Schools of Thought' Contend in the Robot Industry

Wang Xingxing recently stated publicly that the true 'GPT moment' for embodied AI is still some time away, requiring 'at least two to three years.' This means that, in the foreseeable future, Unitree's delivered robots will be more akin to high-performance 'hardware platforms' or 'development platforms' rather than intelligent agents capable of autonomous understanding, decision-making, and execution. For the industry as a whole, the final outcome remains uncertain.

Unitree's prospectus specifically names Tesla, citing its 'mass production capabilities and AI technology resources' as factors that could rapidly reduce the cost of Optimus, 'directly intensifying price competition in the industry.' With Tesla planning to produce one million units annually, Figure AI aiming for 10,000 units per year, and Zhiyuan Robotics targeting 10,000 units in 2026, both domestic and international players are accelerating capacity ramps. While Unitree currently leads in shipments, as production scales up, 'latecomers' may quickly surpass it.

Figure Robot Image Source: Internet

The industry has shifted from early-stage financial investors like Shunwei, Sequoia, Hillhouse, and Qingcheng to late-stage industrial capital (BYD, Meituan) and state-backed funds joining in, indicating that robotics is now seen as a strategic national industry with certainty. BYD's entry suggests potential in automotive manufacturing scenarios, while Meituan's involvement points to opportunities in logistics and delivery.

Fourier Intelligence initially focused on rehabilitation medical robots before expanding into general-purpose humanoid robots. Its GRx series, validated for tasks like installing high-voltage components and high-precision operations at a Shanghai automotive factory, demonstrates its ability to migrate technology from medical to industrial scenarios.

Leju Robotics adopts a 'dual-wheel drive' model of 'education + industry,' achieving leadership in small-sized educational robots and serving 5,000 schools. In March 2026, Leju and Dongfang Precision launched China's first 10,000-unit-scale production line (in Foshan), producing one robot every 30 minutes with a 50% efficiency improvement and precision controlled within 0.02 millimeters.

Zhiyuan Robotics, Unitree's biggest competitor, employs a 'full-stack layout, ecosystem expansion' strategy. In 2025, Zhiyuan and Unitree were tied for global leadership in shipments, each selling over 5,000 units annually. By March 2026, Zhiyuan became the first to surpass 10,000 cumulative units produced, setting a new global mass production speed record. IDC data shows that Zhiyuan and Unitree have established absolute leadership in scalable delivery and application coverage.

Wang Chuang, President of Zhiyuan's General Business Division, stated that Zhiyuan is not engaged in a mere production race, as existing capacity could far exceed current numbers if that were the goal. 'What manufacturers should truly focus on is whether robots can meet customers' sustainable needs in real-world scenarios. Only when customers are willing to replicate and scale deployments does production volume become meaningful; otherwise, producing inventory is worthless.'

Image Source: Internet

While the robotics industry is indeed flourishing, no company dares claim to have achieved universal commercialization. The industry generally believes that when a company's annual shipments exceed 50,000 units, it signifies not only cost reductions but also a major shift in industry recognition of its solutions. Currently, only logistics robots are close to this threshold, while general-purpose robots remain far from a turning point. Perhaps in niche industrial scenarios, highly efficient and low-cost robotics companies will emerge.

For example, Wei Ming, Editor-in-Chief of Chief Business Review, visited Hinton AI Technology Co., Ltd. with Darden School of Business alumni last Friday. CEO Li Kepin introduced the company's mobile composite robot solutions for smart laboratories, smart manufacturing, and intelligent inspections. He emphasized that Hinton AI does not pursue single-hardware stacking but achieves high-precision, high-flexibility, and low-cost deployment through modular iteration, unified underlying control, multi-modal perception, and reinforcement learning. During the demonstration, Hinton AI's robots showcased millimeter-level end-effector positioning and navigation accuracy, as well as capabilities for unmanned operations, multi-well plate handling, equipment operation, and sample transfer in biological, chemical, and materials laboratories.

Unitree's 'Brain' Upgrade Won't Be Easy

In March 2025, Goldman Sachs released a field research report on Unitree Technology, concluding that the company's technical architecture suffers from structural imbalances: 'Unitree's robots excel in gait control, not intelligence.' This directly poured cold water on Unitree, denying its claimed AI leadership.

The report pointed out that, from a technical architecture perspective, Unitree's current AI system exhibits 'layered fragmentation.' The perception layer uses a multi-sensor fusion scheme of 3D LiDAR, depth cameras, and wide-angle cameras, surpassing Tesla's pure vision approach in hardware redundancy. The decision-making layer's UnifoLM large model integrates reinforcement learning and simulation training, supporting 'learn any action from any demonstration' dynamic motion generation. The execution layer achieves millisecond-level joint response based on model predictive control (MPC). However, these three layers have not achieved true end-to-end fusion—semantic understanding from perception is shallow, the decision-making layer's generalization for open-domain tasks is weak, and the execution layer's precision in following high-level intentions is limited.

This is not a temporary issue for Unitree but a persistent weakness over several years. Unitree's robots currently can reliably execute only tasks highly dependent on preset environments and human supervision. The Spring Festival Gala H1 robot's stunning performance relied on remote operators' real-time takeover readiness, with dance moves repeatedly debugged rather than autonomously generated. Path planning in industrial inspection scenarios requires pre-built maps, with limited strategies for unexpected obstacles; research and education clients primarily use the products as algorithm verification platforms, not plug-and-play productivity tools. This 'demonstration-viable but practically limited' technical state prevents the company from entering manufacturing core links and open service scenarios with higher autonomy requirements.

Image Source: Internet

On March 17, 2026, at NVIDIA's GTC conference, Wang Xingxing also discussed challenges facing embodied AI: 1) difficulty in generating and executing complex, diverse actions; 2) data scarcity, requiring improved utilization of video and simulation data; 3) lack of scalable reuse mechanisms for reinforcement learning, making training results hard to accumulate.

Thus, in this IPO, Unitree plans to allocate RMB 2.022 billion of the proceeds to intelligent robot model R&D projects. This means Unitree will heavily invest in strengthening its weak 'brain.' Wang Xingxing explicitly favors video-generation-based world models for the long term, allowing AI to first imagine and generate task videos in its 'brain' before aligning them into motion commands. However, the challenge lies in precisely aligning video-generated content with actual robot actions to avoid insufficient generalization.

As of March 2026, RMB 10.4 billion has been invested in the 'embodied brain' field, spawning at least 12 unicorn companies valued over RMB 10 billion. The industry widely expects the 'GPT 3.0 moment' for embodied AI to arrive between late 2026 and mid-2027, indicating that Unitree's 'brain' currently holds no industry premium or absolute monopoly.

Epilogue

Capital market fervor for robots is cooling. As of March 20, 2026, the CN Robot Industry Index has fallen 12.4%, while the CSI Robot Index dropped 6.8%. This reflects not just fund reallocation or avoidance of high valuations but a broader revaluation of tech giants as intelligent agents deeply intervene [jìn rù - integrate] workflows, with pure software-capable firms being hit hardest. For the highly uncertain, long-cycle manufacturing logic of robotics, what justifies high valuations is a question warranting deep reflection from all industry insiders and investors.

Image source: Internet

An investor believes that those engaging in robotics startups today need to be 'hexagon warriors,' referring to six key aspects: models, data, ontology, commercialization capabilities, financing capabilities, and team. If a startup only claims to excel in model capabilities, it can easily be surpassed by competitors. You need to have strong foundational capabilities across the board while also possessing your own core competitiveness.

Li Chao, Deputy Director of the Policy Research Office of the National Development and Reform Commission, explicitly pointed out at a press conference in November 2025 that balancing 'speed' and 'bubbles' is a core issue that needs to be addressed in the development of cutting-edge industries. Therefore, the author believes that industry reshuffling will accelerate in 2026, with companies lacking technical strength, slow in implementing scenarios, and facing tight funding at risk of being eliminated.

References:

Zhiyuan Produces 10,000th Unit Source: World Humanoid Robot Industry Cluster

Who is Driving Up the Hype for Embodied AI Financing Source: Caijing AI Pai

Half of the Investment Circle is Thanking Unitree Source: Rongzhong Finance

-

![]()

Model Giant Jieyue Xingchen Steps into Smartphone Arena: A Strategic Alliance with Huaqin Technology

-

![]()

Big Model Firm Dives into Phone Market: StepFun and Wingtech Forge a ‘Dynamic Duo’

-

![]()

Zhongrun Optics Makes a Bold Move with 1 Billion Yuan Investment: Is a Turning Point on the Horizon for the Precision Optics Industry?

-

![]()

Deploy CLBO Crystals and YIG Single Crystals! Erythritol Leader Invests 30 Million in Youwei Optoelectronics

-

CXMT’s July 16 Subscription: Leading Domestic Memory Manufacturer—What’s the Earning Potential per Lot?

-

![]()

Rhythm Discrepancy and Premium Value Erosion: Foreign Luxury Brands Must Re-evaluate Their China Strategy

-

![]()

Half-Year, 1 Billion Yuan Financing, 7 Billion Yuan Valuation: A New Dark Horse Emerges in the Embodied AI Sector

-

![]()

Strong Rebound for Tech Stocks in Hong Kong Stock Market: Is It Time to Bottom-Fish?