70.06 Million Yuan in Subsidies Lead to First-Quarter Profitability, Moore Threads Continues to Await Commercialization Turning Point

04/29 2026

04/29 2026

654

654

Text/Xu Wenwen

Edited by/Zhang Xiao

Revenue maintains high growth, losses narrow year-on-year—On April 26, Moore Threads released its financial results for the first quarter of 2026 and the full year of 2025, revealing these two key performance indicators.

For the full year of 2025, revenue reached 1.505 billion yuan, a year-on-year increase of 243.37%. Net profit attributable to shareholders of the parent company and net profit attributable to shareholders of the parent company excluding non-recurring items narrowed by 38.16% and 33.38%, respectively. After excluding the impact of share-based compensation, the net loss for 2025 was 648 million yuan, a year-on-year narrowing of 56.65%.

In the first quarter of this year, revenue was 738 million yuan, a year-on-year increase of 155.35%. In terms of profitability, Moore Threads achieved single-quarter profitability in this period, with net profit attributable to shareholders of the parent company at 29 million yuan. Net profit attributable to shareholders of the parent company excluding non-recurring items was a loss of 54 million yuan, compared to a loss of 136 million yuan in the same period last year.

On April 27, influenced by first-quarter performance, Moore Threads' stock price rose by 7.99%, with its market capitalization increasing by 24 billion yuan in a single day to reach 324.084 billion yuan.

Beyond the single-quarter profitability on paper, a more worthy discussion is how Moore Threads achieved profitability and whether it has truly reached a profitability turning point.

01

Behind Single-Quarter Profitability: 70 Million Yuan in Subsidies and Major Customer Dependency

Among the first annual and quarterly reports released by Moore Threads after its listing, the most eye-catching information is undoubtedly the single-quarter profitability in the first quarter of this year.

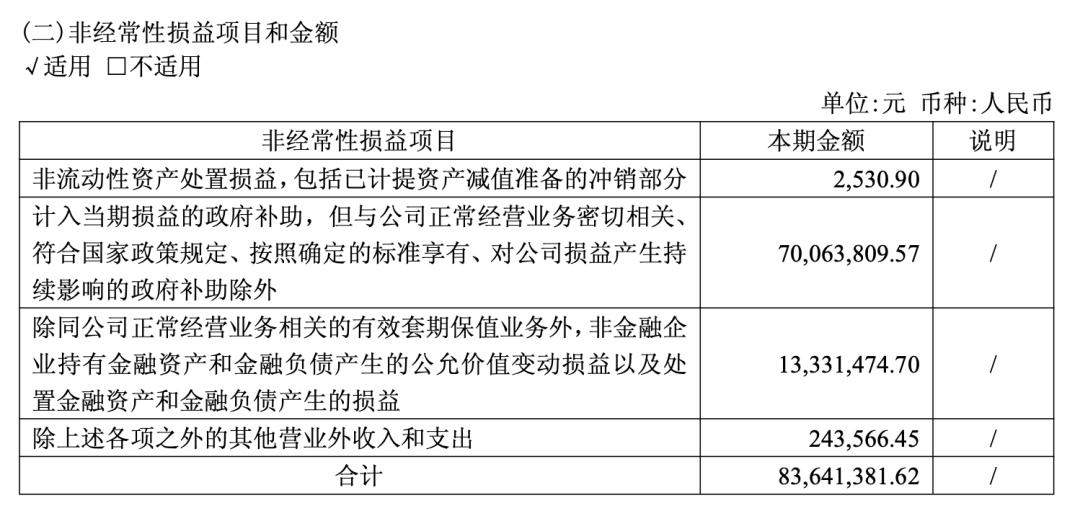

Behind the figures, Moore Threads' net profit attributable to shareholders of the parent company of 29 million yuan in the first quarter was mainly driven by 83.64 million yuan in non-recurring gains and losses. Among them, 70.06 million yuan was government subsidies recognized in current profits and losses. Excluding the impact of non-recurring gains and losses, Moore Threads still incurred losses in the first quarter, albeit with a significant narrowing of the loss margin.

Figure/Moore Threads' first-quarter financial report

Specifically, the company's total operating costs continued to grow rapidly in the first quarter, increasing by 82.10% year-on-year to 770 million yuan.

Among them, operating costs increased by 271.78% year-on-year to 241 million yuan; selling expenses increased by 141.33% year-on-year to 76 million yuan; and research and development expenses increased by 49.95% year-on-year to 369 million yuan.

However, benefiting from the high year-on-year revenue growth of 155.35%, the impact of increased investment by Moore Threads in the first quarter was partially offset to some extent.

Moore Threads stated that the significant revenue growth in the first quarter was mainly due to the company's focus on the research and development and innovation of full-function GPUs during the reporting period, continuous advancement of rapid product architecture iteration, and further expansion of product competitive advantages, thereby promoting rapid revenue growth. The company also mentioned that the narrowing of net profit losses in this quarter was also due to the significant year-on-year revenue growth.

Behind this, nearly 200 million yuan of Moore Threads' 738 million yuan in revenue in the first quarter may have been obtained just at the end of March—

On March 31, it signed a contract with a customer for a total amount of 660 million yuan, with the contract subject matter (subject matter) being Moore Threads' KUAE intelligent computing cluster. According to the announcement, the customer will pay the funds in three installments, with 30% of the contract price paid within two days after the contract takes effect, 60% of the contract price paid within 180 days after goods receipt and acceptance, and 10% of the contract price paid before December 31 of this year.

Objectively, from a full-year perspective, this 660 million yuan order will have a particularly significant impact on boosting Moore Threads' performance for the entire year of 2026:

This single contract amount is equivalent to more than 40% of the company's revenue in 2025. In 2025, Moore Threads' revenue was 1.506 billion yuan.

However, for Moore Threads, while super-large orders drive performance soaring on one hand, the inevitable major customer dependency is on the other. The company also mentioned the risk of high customer concentration in its 2025 financial report.

Financial report data shows that the top five customers contributed as much as 91.36% to Moore Threads' revenue in 2025. Looking further back, from 2022 to 2024, the contribution ratio of the top five customers to the company's main business revenue was 89.86%, 97.54%, and 98.16%, respectively.

For comparison, among the other two domestic GPU companies that listed on the Hong Kong Stock Exchange in January this year, Biren Technology's revenue in 2025 had a contribution ratio of about 71.3% from the top five customers, a significant narrowing from 90.3% in 2024; Iluvatar CoreX's revenue contribution ratio from the top five customers in 2025 was also relatively healthier at 43%.

The ability to continuously secure large orders demonstrates market recognition of Moore Threads' capabilities from technology to products to engineering, and this recognition objectively also has potential demonstration (demonstration) effects.

However, the risk lies in the fact that when a company's revenue growth and profit performance are strongly correlated with major customers and large orders, such growth is inherently abnormal and unstable.

In other words, the single-quarter profitability on Moore Threads' books in the first quarter does not necessarily mean that the company has entered a profitability turning point to a certain extent.

Especially under the certainty of "high investment" as an influencing factor, Moore Threads' path to commercial breakthrough remains long and arduous.

02

New Challenges for Moore Threads to Sustain Operations

Since its listing on the STAR Market on December 5 last year as the "first domestic GPU stock," Moore Threads has consistently been the most closely watched and favored domestic GPU manufacturer by the capital market, perhaps without exception.

This is largely due to Moore Threads' technical path similar to NVIDIA's—under the grand narrative of domestic computing power autonomy and controllability, the market hopes Moore Threads will become a "NVIDIA alternative."

In fact, "becoming a NVIDIA alternative" is itself part of Moore Threads' capitalization narrative.

In terms of facts, among domestic AI chip manufacturers, only Moore Threads bets on the full-function GPU technology path, while other players focus more on the AI computing layer, targeting large model training and inference scenarios.

Full-function GPU, i.e., a GPU with complete functionality and precision integrity, offers significant advantages in work efficiency, ecological completeness and diversity, and compatibility.

Functional completeness: Integrates multiple capabilities such as AI computing acceleration, graphics rendering, physical simulation and scientific computing, and ultra-high-definition video codec in a single GPU chip to meet diverse computing needs;

Precision integrity: A single chip supports different computing precisions such as FP64 Vector, FP32 Vector, TF32 Tensor, FP16/BF16 Tensor, FP8 Tensor, and INT8 Tensor to meet the computing needs of GPU acceleration in different scenarios.

Under the full-function GPU technology path, Moore Threads' potential product system and landing scenarios will be more diverse, and its technological and ecological barriers will be higher from a long-term perspective.

From another perspective, this is Moore Threads' core differentiated advantage, yet it is also a burden.

Moore Threads' full-function GPU route offers greater technological imagination and potential commercialization space, but the technology ramp-up cycle is longer, and investment is heavier.

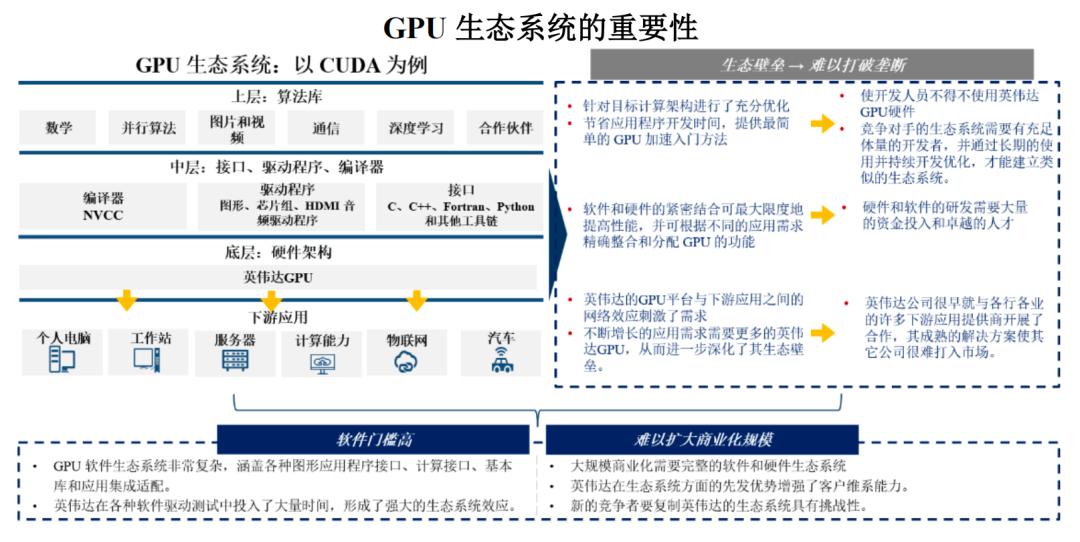

NVIDIA's moat is one side GPU and the other side the CUDA ecosystem. Under the grand narrative of domestic AI computing power autonomy and controllability, Moore Threads is objectively benchmarking against NVIDIA.

To some extent, NVIDIA's GPU ecosystem also hides shadows of Moore Threads.

Figure/Moore Threads' prospectus

At the underlying hardware architecture level, Moore Threads independently developed MUSA, a unified full-function GPU computing acceleration system architecture that integrates GPU hardware and software. Based on this architecture, it has iterated five proprietary chip architectures and launched four chips. Among them, the latest-generation chip architecture "Hua Gang," the "Hua Shan" chip for high-performance AI training and inference, and the "Lu Shan" chip focusing on high-performance graphics rendering are also in planning;

At the core IP and software stack level, Moore Threads is also accelerating the construction of the MUSA software stack, covering a complete toolchain from underlying drivers, compilers, and operator libraries to upper-layer development frameworks.

Moreover, the construction of Moore Threads' GPU software ecosystem is actually walking on two legs, compatible (compatible with) CUDA on one side while slowly building its own ecosystem on the other, i.e., the "full-stack ecosystem + high compatibility" mentioned in official statements.

Despite being largely aligned with NVIDIA strategically, it is not easy for Moore Threads to become a true "Chinese NVIDIA" in the short term, achieve a closed commercialization loop, and build commercialization barriers.

Betting on the full-function GPU technology path has objectively burdened Moore Threads with genes of high growth, high investment, and high losses.

Over the past few quarters, Moore Threads has indeed been reducing losses objectively—but as we mentioned above, at this stage, its loss reduction is largely abnormal and unstable, primarily reflected in its high dependency on major customers in terms of product shipment structure.

This means that in the medium to short term, whether Moore Threads can maintain high growth, continue to reduce losses, and even achieve true profitability adds another layer of uncertainty.

To break this uncertainty, the ideal solution is of course to continuously expand its customer base and optimize its shipment structure.

However, this points to another challenge for Moore Threads: It has not yet secured more orders from major internet companies, which are the core consumers of domestic GPU chips.

"Chinese internet companies account for more than 80% of the total demand for domestic GPU chips. For domestic GPUs to commercialize, they must enter the internet sector," a server manufacturer representative told Caixin in January this year. They also admitted that except for Cambrian and Kunlun Core, other domestic GPU startups are still in the "knocking on the door" stage with internet customers.

From this perspective, the practical challenges Moore Threads faces are even more severe.

IDC data released in April this year shows that total AI accelerator card shipments in the Chinese market in 2025 were approximately 4 million units, of which domestic chip companies shipped a combined total of about 1.65 million units, supplying 41% of the market share. Moore Threads failed to crack the top eight.

Of course, in the medium to long term, the Chinese AI computing acceleration chip market size will continue to maintain high growth. For domestic GPU manufacturers including Moore Threads, there is broad scope for breakthroughs.

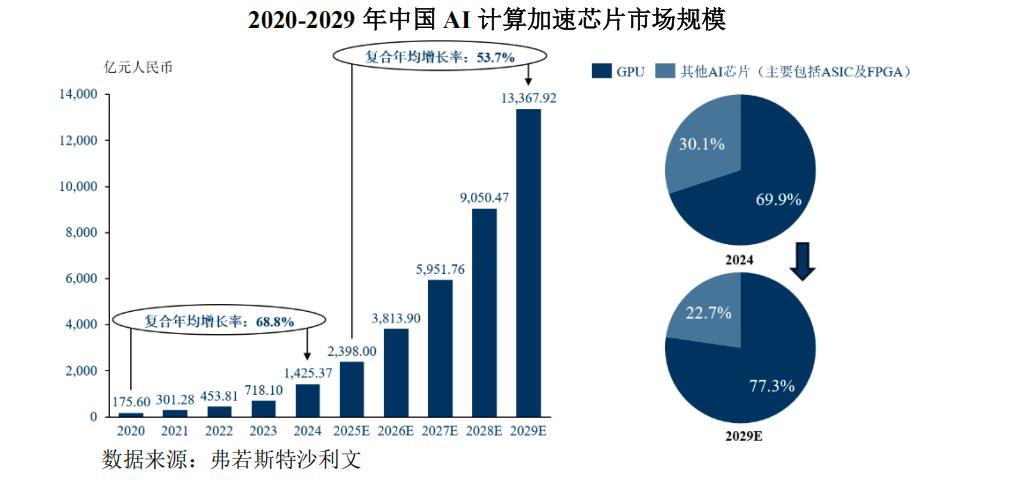

Frost & Sullivan predicts that by 2029, the Chinese AI chip market size will surge from 142.537 billion yuan in 2024 to 1.336792 trillion yuan, with a compound annual growth rate of 53.7% from 2025 to 2029. From a market segment perspective, GPU market growth will be the fastest, with its market share expected to rise from 69.9% in 2024 to 77.3% in 2029.

Figure/Moore Threads' prospectus

Focusing on Moore Threads, the advantages of the full-function GPU route are also expected to be gradually released.

However, how to cope with competition from rivals with relatively focused business structures, how to first narrow or even catch up with NVIDIA's hardware gap, and how to continuously lay a solid foundation in software ecosystem construction are all uncertainties facing Moore Threads.

At the earnings briefing after the financial report release, an investor asked, "How does the company balance short-term R&D investment with long-term profitability goals?"

Moore Threads' founder and CEO Zhang Jianzhong responded:

To balance the two, the company has adopted the following strategies: First, clarify R&D directions and focus on technological areas with high market potential and high barriers to ensure that R&D results can be quickly converted into commercial value and build long-term competitiveness; at the same time, continuously optimize resource allocation and improve R&D efficiency to ensure maximum benefit from each project's investment; the company has built a cloud-edge-end product line to fully leverage the capabilities of full-function GPUs and accelerate revenue growth through diversified product lines and services.

Header image/Moore Threads' official website

-

![]()

Model Giant Jieyue Xingchen Steps into Smartphone Arena: A Strategic Alliance with Huaqin Technology

-

![]()

Big Model Firm Dives into Phone Market: StepFun and Wingtech Forge a ‘Dynamic Duo’

-

![]()

Zhongrun Optics Makes a Bold Move with 1 Billion Yuan Investment: Is a Turning Point on the Horizon for the Precision Optics Industry?

-

![]()

Deploy CLBO Crystals and YIG Single Crystals! Erythritol Leader Invests 30 Million in Youwei Optoelectronics

-

CXMT’s July 16 Subscription: Leading Domestic Memory Manufacturer—What’s the Earning Potential per Lot?

-

![]()

Rhythm Discrepancy and Premium Value Erosion: Foreign Luxury Brands Must Re-evaluate Their China Strategy

-

![]()

Half-Year, 1 Billion Yuan Financing, 7 Billion Yuan Valuation: A New Dark Horse Emerges in the Embodied AI Sector

-

![]()

Strong Rebound for Tech Stocks in Hong Kong Stock Market: Is It Time to Bottom-Fish?