Tencent: Boldly Investing in AI, the 'King of Stocks' Embarks on a New Growth Trajectory

05/15 2025

05/15 2025

642

642

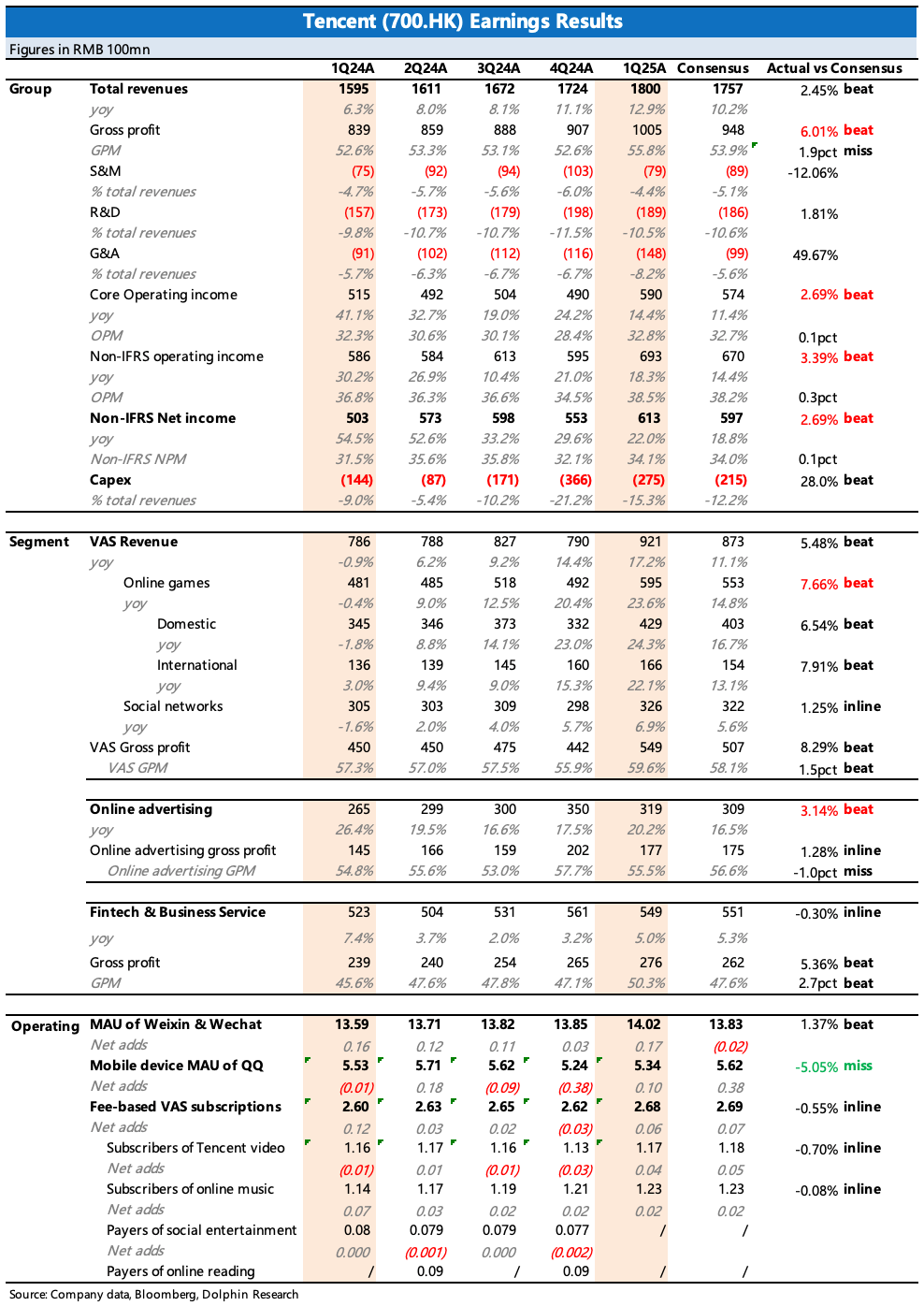

After a two-month hiatus, Tencent unveiled its first-quarter 2025 financial results following the close of the Hong Kong stock market today (May 14, Beijing time). The results, fueled by robust growth in gaming, advertising, and a recovery in the payment environment, surpassed expectations and impressed investors.

While gaming significantly contributed to Tencent's stellar Q1 performance, the high base effect of the DNF mobile game is anticipated to start exerting pressure from Q2 onwards. This implies that, from a broader trend perspective, the overall profit growth rate will slow down to a new range. Hence, the market eagerly anticipates whether AI can reignite Tencent's growth momentum.

Last month, Dolphin Insights initially delved into Tencent's potential AI strategic roadmap, focusing on its capital allocation (Review: "Tencent: From Stingy Buybacks to a Clear Super AI Plan?"). This time, combining the financial report, let's explore further.

First, let's recap the performance:

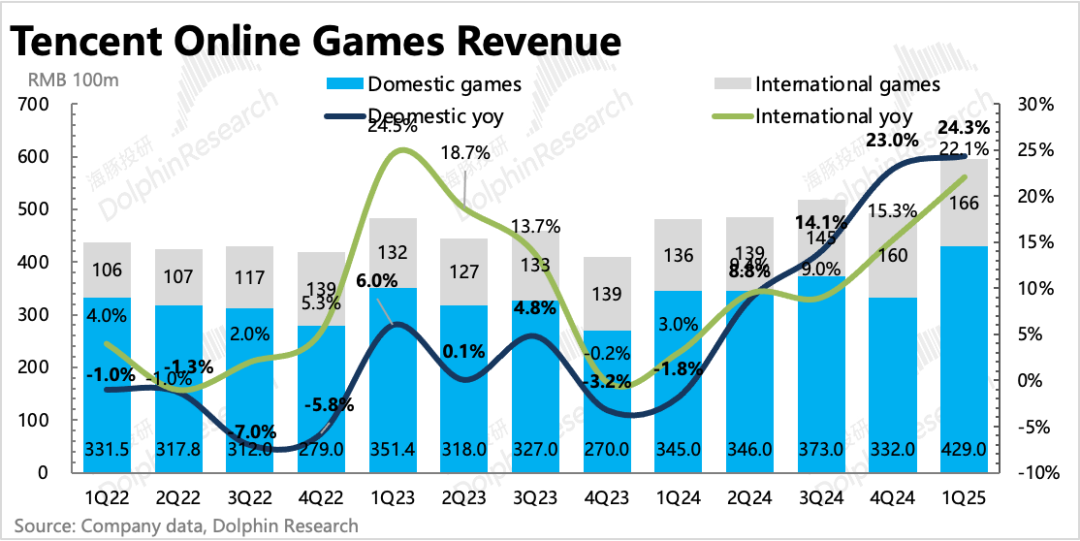

1. Evergreen games continue to drive growth, with the gaming business exceeding expectations: Q1 gaming revenue surged by 24%, representing a robust growth rate regardless of expectations. In addition to contributions from the "DNF mobile game" and "Delta Force," the two enduring hits "Honor of Kings" and "Game for Peace" also performed exceptionally well during the Spring Festival period due to content updates and operational activities. Overseas revenue was also bolstered by high growth from "PUBG Mobile" and Supercell's classic games.

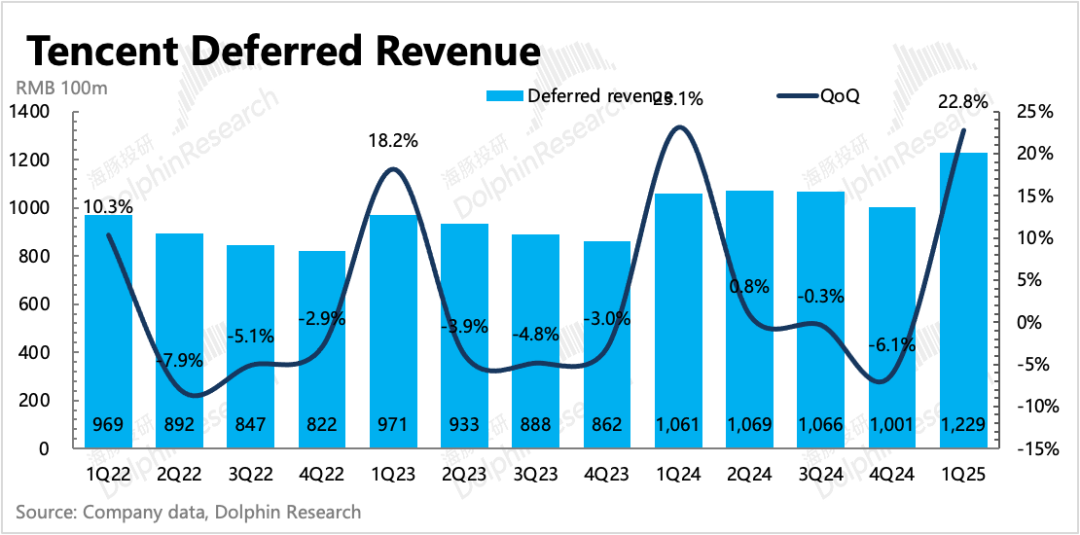

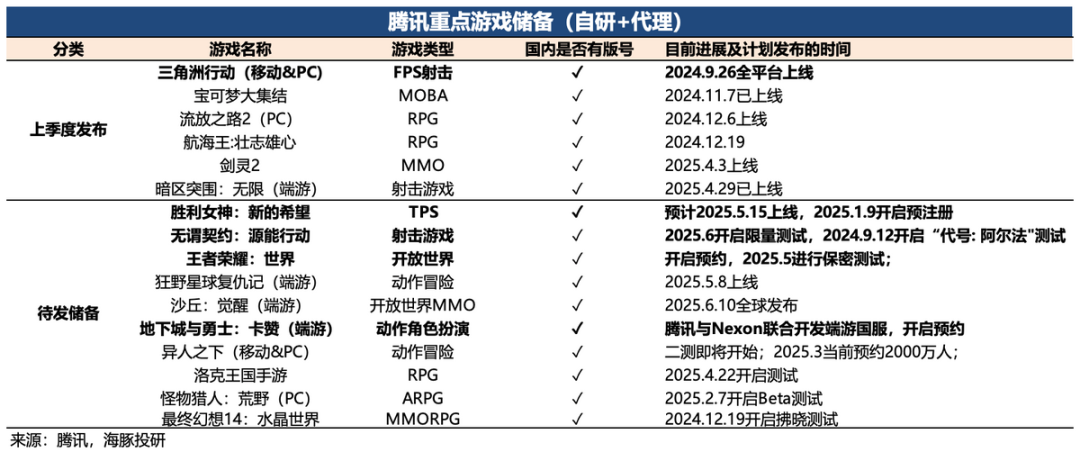

From the perspective of deferred revenue, the quarter-on-quarter growth rate was higher than previous years, expected to continue supporting Q2. However, starting from Q2, the "DNF mobile game" will inevitably pose a high base effect. Judging from the current pipeline, numerous heavyweight titles led by "Honor of Kings: World" are in the wings, although most have already secured game licenses. There may still be a time lag before their scheduled launches, and it remains uncertain whether they will release this year.

Therefore, under such growth pressure, there will be a heavier reliance on evergreen games. Since entering the second quarter, "Honor of Kings" has continued to strengthen its collaboration with renowned IPs such as Nezha. Additionally, "Game for Peace" will undergo a significant update this summer, enhancing content experiences through AI.

2. Advertising thrives, with acceleration driven by e-commerce: Q1 advertising revenue grew by 20%, further accelerating despite the high base and exceeding market expectations. During the last conference call, the company mentioned that increasing the loading rate of video ads is the core driver supporting advertising growth in an uncertain macroeconomic environment this year. Currently, video ads are the second-largest advertising revenue type within WeChat, with a loading rate of only 4%, trailing behind short video peers.

However, a smooth increase in the loading rate also necessitates the support of advertisers with substantial budgets. E-commerce merchants are known to be the biggest spenders on advertising. Recently, an e-commerce product department was added under the WeChat Business Group, signaling clear intentions.

3. Financial Technology and Business Services (FinTech & Business Services) exhibit an expected recovery: Primarily driven by the implementation of certain policies. However, given the high uncertainty in the consumer environment, we anticipate that the growth rate may remain subdued throughout the year. Nonetheless, if e-commerce takes off, it will also propel payments, compensating for Tencent's relatively weaker position in online physical e-commerce payments.

4. AI and e-commerce propel enterprise services: Primarily fueled by the combined pull of AI cloud demand and e-commerce commissions. In the previous quarter, the company noted insufficient supply of AI cloud services. With the acceleration of chip deployment, revenue is expected to accelerate to growth of over 10%. However, the company's overall policy prioritizes internal computing power, so at least this year, there's no need to be overly optimistic about the growth rate of cloud services.

The aforementioned e-commerce layout can also bring incremental technology commission revenue to Tencent. Yet, this is not the primary focus. It's conceivable that Tencent may substantially reduce or waive this fee to attract merchants, expecting to generate more medium- and long-term value through e-commerce advertising.

5. Operating efficiency consistently supports profit margin growth: In Q1, alongside a favorable revenue growth trend, profit margins also increased. On one hand, changes in the business structure holistically improved business monetization efficiency (increase in comprehensive gross profit margin). On the other hand, operating expenses remained stable and grew at a low rate. For instance, although there were fewer new game launches in Q1, operational activities for existing games were intensive, yet sales expenses did not significantly increase. This underscores that evergreen games come with brand marketing and exceptional monetization efficiency. As a leading company with the most evergreen games, Tencent naturally has an edge over its peers.

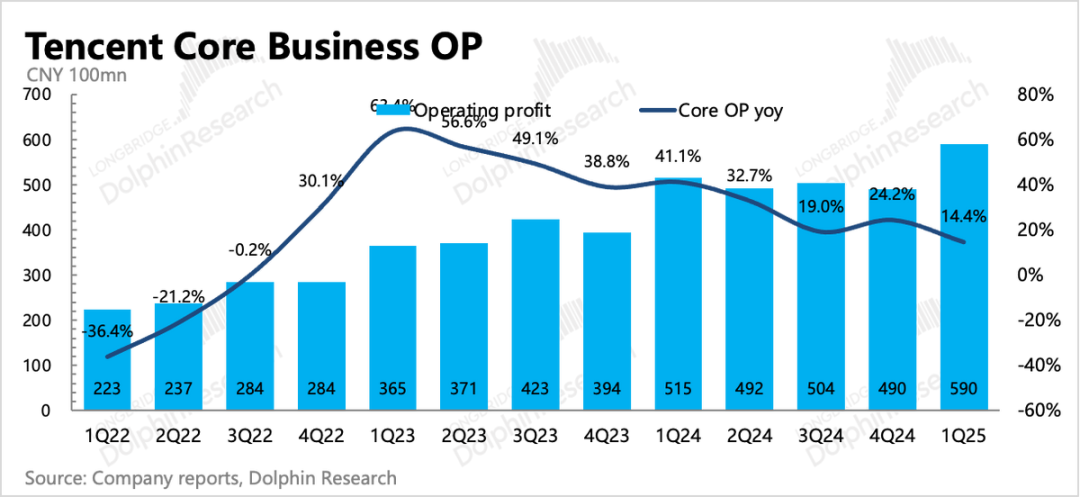

Ultimately, Non-IFRS net profit attributable to shareholders increased by 22% year-on-year, with a profit margin of 24%. Excluding the one-time equity compensation of 4 billion yuan due to the Ubisoft reorganization, the actual profit exceeded expectations even further. According to Dolphin Insights' consistent tracking of the main business operating profit indicator, excluding the impact of the Ubisoft merger, the actual year-on-year growth was 22%, maintaining high growth despite the high base.

6. AI investment remains relentless: Regarding cash flow and capital allocation, the focus is on capital investment and buybacks. In Q1, primarily due to the robust growth of the two cash-generative businesses—gaming and advertising—net operating cash inflow surged to 76.9 billion yuan, a record high.

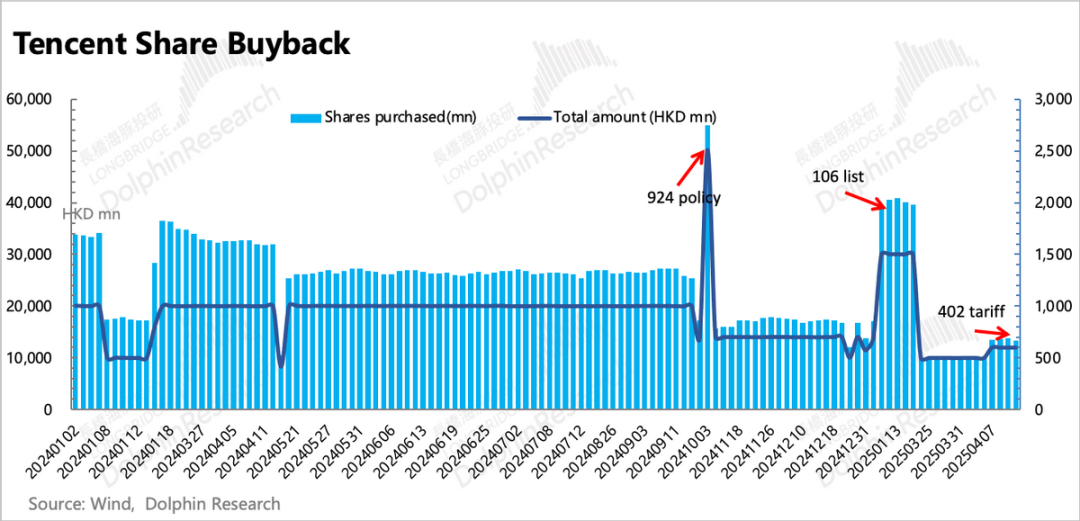

Q1 capital expenditures of 27.5 billion yuan exceeded market expectations and the normal deployment pace (referencing overseas giants, investment at the beginning of the year lags behind the full-year plan). While it's possible that there may be continued preemptive purchases before chip purchase restrictions escalate, according to the company, investments will dynamically change based on internal demand, indicating strong demand. Simultaneously, it also showcases Tencent's ambition for super AI. In terms of buybacks, Q1 is generally the lowest throughout the year, primarily due to the short time difference between the release of the two most recent financial reports, and buybacks are prohibited during the silent period.

Ultimately, with more inflows than outflows, a substantial amount of cash was retained in Q1, with net cash of 90.2 billion yuan at the end of the quarter, an increase of over 13 billion yuan from the previous quarter.

7. Overview of detailed financial report data

Dolphin Insights' Viewpoint

The first-quarter performance was commendable, and the market had certain expectations for both gaming and advertising. Specifically for the gaming business, according to Sensor Tower data, the revenue growth rate can be roughly estimated at 25% year-on-year. However, the market remained conservative, possibly due to revenue recognition measurements and caution regarding overseas games.

Furthermore, the continued weak macroeconomic environment and subsequent high base pressure on gaming in Q2 may have also prompted some funds to avoid the financial report release, mainly to steer clear of Q2 guidance. This is understandable. After all, based on the original 2025 growth expectations, Tencent's current valuation implies a Non-GAAP P/E of 17-18 times, lower than the historical average. However, with increased investment in AI, operating expenses are also expanding, and the 5% fixed income supported by buybacks has halved to only 2.5%. Therefore, before AI investment yields positive cyclical returns, conservative funds may hesitate in the short term. Dolphin Insights already mentioned this in the previous quarter's financial report review.

But this financial report also reveals Tencent's 'resilience' beyond imagination, and we believe this resilience is likely due to AI already generating positive returns for internal operations:

(1) Advertising exhibits remarkable resilience under pressure. The overall environment in Q1 was barely satisfactory, and Tencent's advertising revenue also faced pressure from a high base. However, actual advertising revenue accelerated to grow by 20%, with the increase in the loading rate of video ads undoubtedly being the primary driver. But merchants generally focus on ROI. When consumption is weak, video ads increase inventory, and merchants are still willing to accept orders, further indicating that the ROI of video ads has improved. Combined with the company's statement in the financial report: "AI has made a substantial contribution to performance advertising," this is likely where the improvement lies.

From daily observation, the accuracy of WeChat advertising has not been high, at least significantly lower than Douyin and Kuaishou. The underlying reason could be minimal user data infringement or that WeChat itself does not prioritize advertising commercialization. Regardless of the reason, the assistance (marginal improvement) of AI to WeChat advertising should be significantly better than that of Douyin and Kuaishou (which are already at their peaks), akin to the ROI improvement brought by AI to Meta and Google.

(2) Evergreen games maintain high user engagement. Continuous development of evergreen games has been one of Tencent's core strategies since last year's gaming rectification. However, the user engagement of evergreen games is easily affected by migration from new games released during the same period, especially for MOBA games. As large DAU games, a decline in popularity further worsens the experience of existing users. In the past, there were heavy traces of bot players, but with the new generation of AI technology, users may find it difficult to distinguish between bots and real players, ensuring a high-quality gaming experience for an extended period.

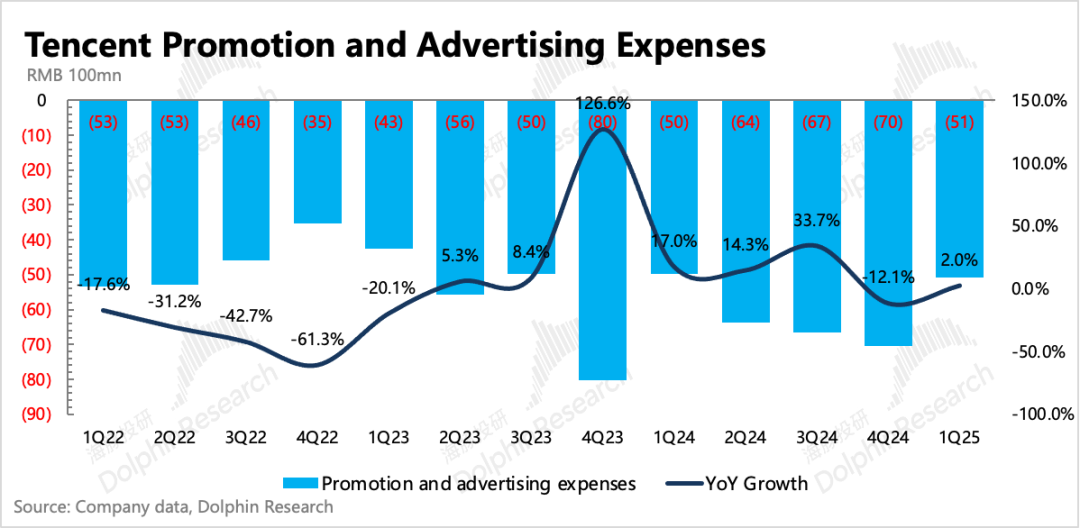

(3) Operating expenses are controlled against the trend. In Q1, the total expenditure of the three core expenses of the main business was 37.5 billion yuan (excluding the impact of the Ubisoft reorganization), with the primary optimization in sales expenses. Despite intensive gaming activities and the epic promotion of Yuanbao (with some external promotion expenses), sales expenses remained flat year-on-year.

Drawing from Meta and Google's experiences, AI can replace multiple aspects of comprehensive operational work and basic code writing. Therefore, on Tencent's vast organizational structure, more optimization may be anticipated.

And based on Tencent's always astute investment level, it has conveyed its attitude towards AI and the smooth progress of its current AI business through exceeding expectations in Capex. Therefore, aligning with our previous viewpoint, we believe that although it's challenging to quantify the revenue expansion and internal efficiency improvement space that AI can bring to Tencent, some positive adjustments can be made to the valuation, such as increasing it from the current 17x P/E to a relatively optimistic 20x P/E. And from a longer-term perspective, in terms of gaining a first-mover advantage in the value of the new generation of industries, whether it's traffic, talent, or the strategic vision and reliability of management, Tencent is currently a top contender within our field of vision.

The following is a detailed analysis

I. Benefiting from AI, the WeChat ecosystem expands steadily

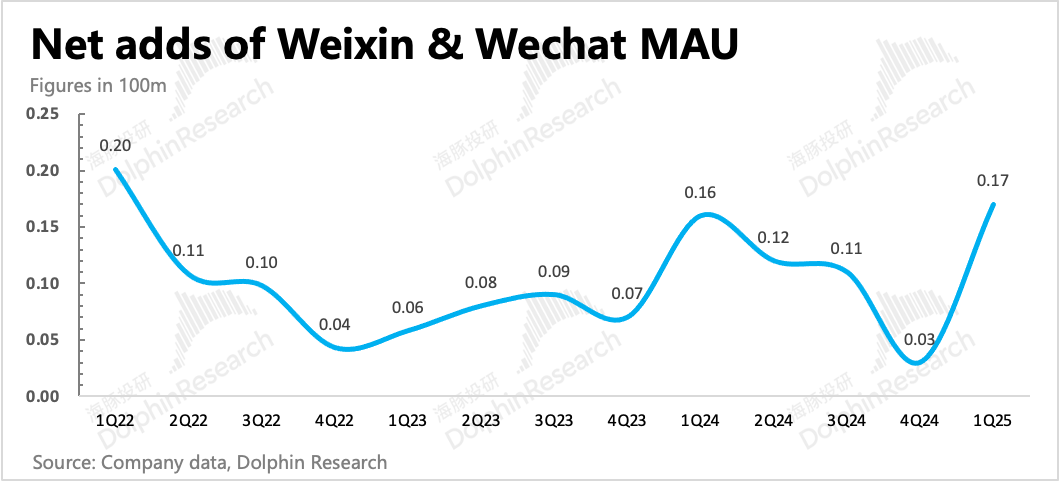

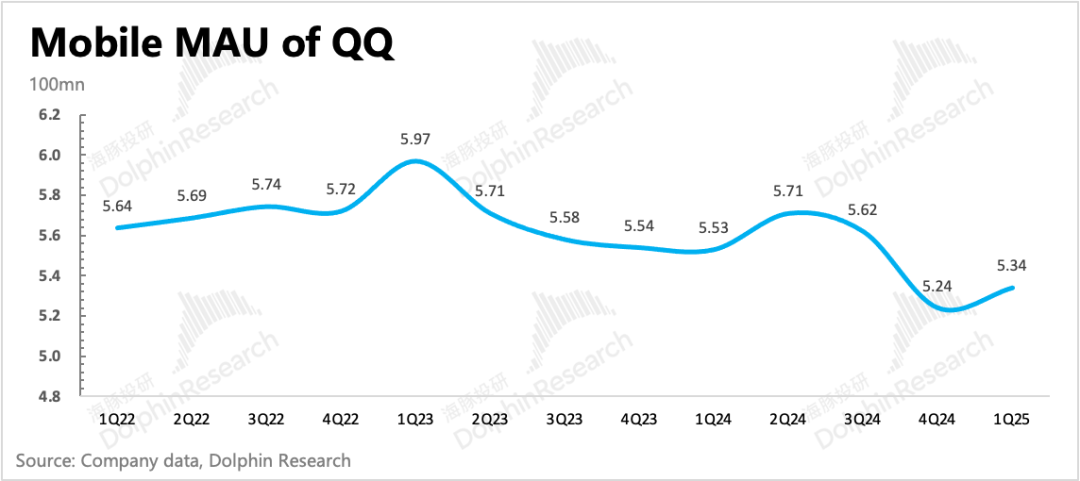

In Q1, WeChat had 1.402 billion users, with a net increase of 17 million compared to the previous quarter. Besides seasonal effects, this should also be driven by Yuanbao and WeChat stores within WeChat. QQ continued to decline year-on-year, with some reflow due to the Spring Festival. In the future, we will observe whether QQ can stabilize its traffic after AI integration.

After the initial aggressive promotion of the Yuanbao App at the beginning of the year, the monthly active users of the Yuanbao App have now surpassed 40 million but still lag behind the top two, Doubao with 107 million and DeepSeek with 97 million. In April, Yuanbao was officially integrated into WeChat (previously primarily for testing, directly attached to the original red envelope assistant), allowing users to more seamlessly invoke Yuanbao through chat windows, significantly enhancing penetration.

Regarding the super AI strategy, the AI Chatbot is merely one application direction. Judging from Tencent's current strategic direction, throughout the WeChat ecosystem, a more intelligent, task-result-oriented AI Agent will also be launched in conjunction with the invocation of mini-programs. The subsequent launch path is worth looking forward to and paying close attention to.

In March, the share of user time in the Tencent ecosystem increased quarter-on-quarter, possibly benefiting from the drive of the Yuanbao App. However, ByteDance still maintained a leading gap. This also indicates that Tencent and ByteDance will undoubtedly engage in a fierce battle for the next generation's largest traffic entrance.

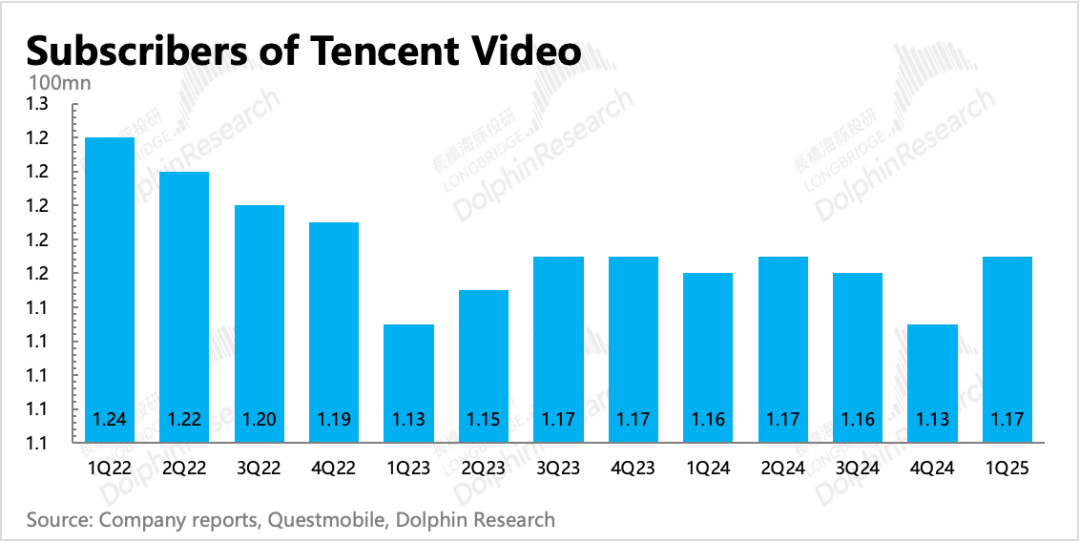

During the off-season, the number of paid users for value-added services witnessed a net increase of 6 million, primarily due to a surge of nearly 2 million for Tencent Music and a net gain of 4 million for Tencent Video, with the remainder attributed to Readwave and live streaming users.

II. Evergreen Games Propel Growth, Gaming Business Exceeds Expectations

In Q1, online game revenue amounted to 59.5 billion yuan, marking a 23.6% year-on-year increase. Besides contributions from the "DNF" mobile game and "Delta Force," evergreen games played a pivotal role in the quarter's unexpected growth—including local hits like "Honor of Kings" and "Game for Peace," as well as overseas favorites such as "Brawl Stars" and "Clash of Clans."

The domestic market expanded by 24.3%, maintaining robust growth. During the Spring Festival, "Honor of Kings" leveraged the snake year skin and a collaboration with the Sanrio IP, enhancing user experience through AI, maintaining user engagement, and achieving record-high monthly revenue. Following a significant content update, "Game for Peace" also witnessed a substantial revenue boost that continued into April.

Overseas game revenue grew by 22%, exceeding expectations. Initially, market expectations were modest, but Supercell revitalized old games with gameplay iterations.

The revenue indicator, combined with deferred revenue, better represents forward-looking indicators of real demand. In Q1, deferred revenue increased by 22% year-on-year, with a quarter-on-quarter growth rate higher than previous years' norms. Revenue increased by 16%, significantly accelerating compared to the prior quarter, expected to continue supporting Q2.

However, starting from Q2, it will inevitably face the high base effect of "DNF Mobile." Judging by the current pipeline, several high-impact reserves led by "Honor of Kings: World" are forthcoming, though most have obtained publishing licenses. Their launch schedules are uncertain, and it remains unclear if they will release this year.

Therefore, under growth pressure, there will be greater reliance on evergreen games. Since Q2, "Honor of Kings" has intensified collaborations with renowned IPs like Nezha. "Game for Peace" will also undergo a major update this summer, enriching content experiences through AI.

Driven by large-scale evergreen games, Tencent's high growth significantly supports the industry, enabling the market to continue recovering in the footsteps of Tencent's Q1 performance, both domestically and overseas.

III. Advertising Momentum Strong, Future Acceleration Hinges on E-commerce

Over the past two years, with the rise of video accounts and mini-program games, Tencent's advertising business has demonstrated resilience in adversity. However, as the low-base effect wanes, even with video accounts and mini-programs, it struggles to withstand intensifying environmental pressures.

In Q1, the overall environment was barely satisfactory, yet Tencent's advertising grew by 20%, further accelerating on a high base. The market had positive expectations, but Tencent's actual performance surpassed them.

In a previous conference call, the company mentioned that increasing video account loading rates is crucial for supporting advertising growth in an uncertain macroeconomic environment. Currently, video accounts are WeChat's second-largest advertising revenue source, with a loading rate of just 4%, significantly lower than short video peers.

However, smoothly increasing loading rates requires support from advertisers with real money. E-commerce merchants are the biggest advertisers. Today, an e-commerce product department has been established under the WeChat Business Group, with obvious intentions behind it.

According to estimates (for reference only), the scale of video account advertising revenue in Q1 (primarily external circulation + e-commerce, with mutual selection advertising accounting for a lower proportion due to net revenue recognition) may exceed 8 billion yuan, up over 50% year-on-year, accounting for 25% of total advertising revenue.

From daily observations, WeChat advertising's accuracy has always been lacking, notably lower than Douyin and Kuaishou. The underlying reason could be minimal user data infringement or WeChat's lack of emphasis on advertising commercialization. Regardless, AI's assistance to WeChat advertising (marginal improvement) should significantly outperform that of Douyin and Kuaishou (already at their peaks), akin to AI's ROI changes for Meta and Google.

IV. Fintech Hits Bottom, Enterprise Services' High Growth Not Urgent

In Q1, Fintech and enterprise services grew by 5% year-on-year, showing a warming trend within expectations.

Breaking it down, payment revenue, accounting for 2/3, has bottomed out and is warming up (referring to the change trend of total third-party reserve funds collected by the People's Bank of China, with the financial report disclosing roughly stable year-on-year performance). Meanwhile, enterprise services (cloud business and video account commissions, etc.) continue to accelerate growth.

In a previous conference call, management mentioned that the cloud business is currently limited by insufficient supply (primarily data centers), hence a low proportion of external leasing. With limited computing power, internal demand will be prioritized this year. This is the key difference between Tencent and Alibaba, Baidu in their AI strategies, stemming from their different revenue goals. Thus, the cloud business may continue to be supply-constrained this year but is expected to accelerate from next year.

Additionally, enterprise services include e-commerce commissions (only technical service fees). According to recent news, Tencent's WeChat Group has set up an e-commerce product department, with WeChat stores becoming a focus in the past two quarters' financial reports. This underscores Tencent's strategic intent towards e-commerce. However, technical service fees are secondary, with advertising being the real goal. Fees may be reduced or exempted in the future to attract more merchants and service providers.

In summary, despite a warming trend, for Fintech and enterprise services this year, cautious optimism is warranted.

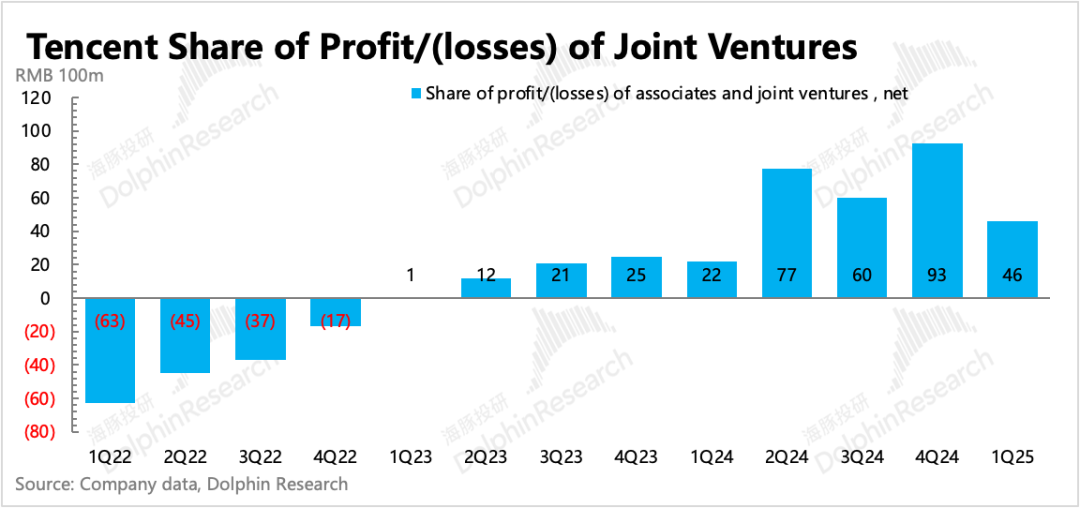

V. Investment Gains: Derived from Steady Reductions in Invested Companies + Financial Profit Sharing

Regarding investment gains, we focus on two parts based on the original indicator definition: net other income (including investment income) and share of profits of associated/joint ventures. In Q1, with minimal asset disposal, comprehensive investment income mainly came from profit sharing.

As of Q1-end, the company's combined associated/joint venture asset scale totaled 312.6 billion yuan. Tencent's calculated investment return rate for Q1 was 1.5%, with a slight year-on-year increase. From 2022 to present, it has generally shown a positive trend.

VI. Operating Efficiency Improves Against the Trend

Adjusted net profit in Q1 was 61.3 billion yuan, exceeding market expectations of 59.7 billion yuan. From the perspective of operating profit from core businesses (= gross profit - three operating expenses), excluding the one-time equity compensation expense of 4 billion yuan from Ubisoft's reorganization and merger, actual core operating profit significantly surpassed market expectations, with a profit margin of 35%, up 3 percentage points year-on-year.

Let's delve into how this high profit margin was achieved:

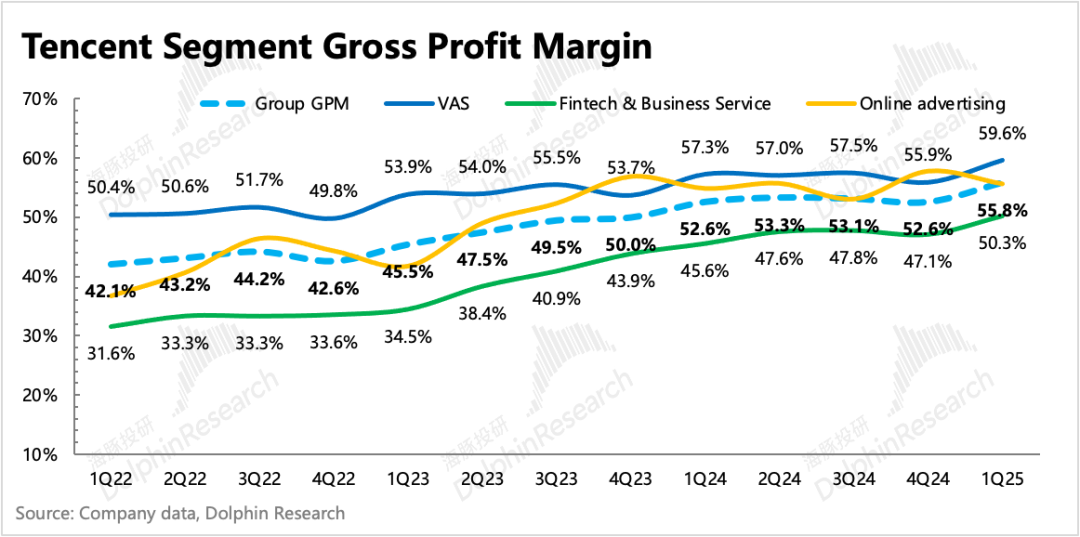

1. Structural Adjustment Boosts Overall Profitability

Games and advertising are high-margin businesses. Their sustained high growth has positively impacted both gross profit margin and cash flow. In Q1, the gross profit margin increased by 3 percentage points year-on-year to 55.8%, a record high.

2. Sustained R&D Investment Enhances Operating Efficiency

Due to AI, R&D expense growth is inevitable but not exaggerated. Compensation-related expenses increased by 14.4%, with a decelerating growth rate. Server bandwidth expenses surged by 52% year-on-year, continuing to accelerate, potentially related to the gradual expansion of AI-related R&D teams with current under-recognition.

However, there's a continuous drive to optimize management and sales expenses unrelated to AI investment. In Q1, the primary optimization was in sales expenses, which remained flat despite intense game activities and promotions. While management expenses increased by 17%, the combined total of both, excluding restructuring expenses, only grew by 11% year-on-year, lower than revenue growth.

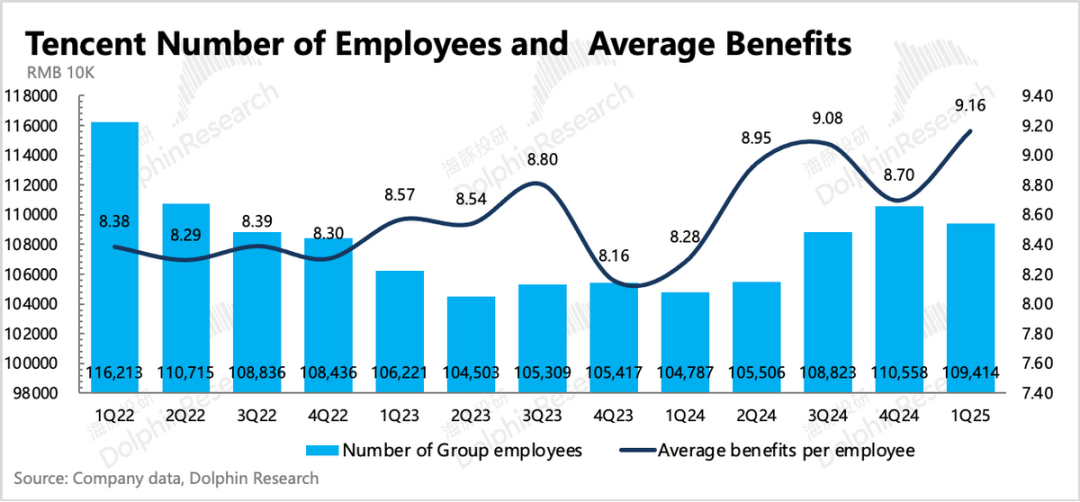

In terms of employee count, there was a decrease of 1,144 people quarter-on-quarter compared to Q4-end. This may exclude AI-driven personnel structure optimization. For instance, R&D personnel compensation grew by 14% year-on-year in Q1, with accelerated AI penetration, lower than the previous quarter's growth rate.

Drawing from Meta and Google's experiences, AI can replace multiple aspects of operational work and basic coding. Thus, in Tencent's vast organizational structure, more optimizations are anticipated.

3. Future Expenditure Expansion - Capex Front-loaded Investment Exceeds Expectations

While future AI investment will expand costs and operating expenses, Tencent's AI investment may yield higher returns in the long run. Currently, investing in AI is more of a defensive strategy to secure Tencent's leading position in the mobile internet.

Q1 capital expenditure was 27.5 billion yuan, exceeding market expectations and the normal deployment rhythm (referring to overseas giants, with initial investment lagging annual planning). While preemptive chip purchases before restrictions escalate cannot be ruled out, according to the company, investment will dynamically change based on internal demand, indicating strong demand.

VII. Prospects of Growth Revival Expected to Offset Major Shareholder Reduction Pressure

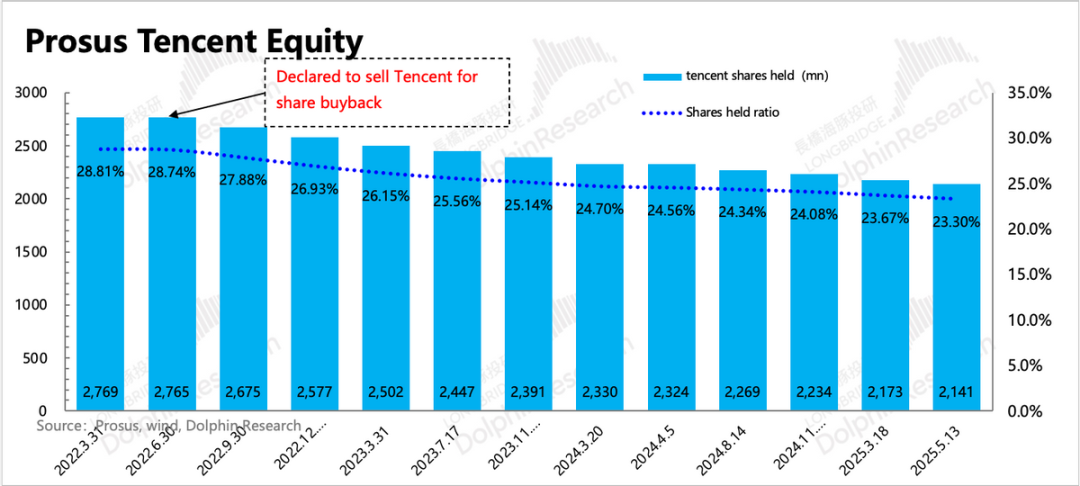

Lastly, let's examine the scenario of share repurchases and sales. Over the past two months since the last financial report was disclosed, Tencent's total share count has increased net due to factors such as employee option grants and a repurchase moratorium during a quiet period. Concurrently, major shareholders have not slackened their efforts to reduce their holdings, selling nearly 32 million shares in just two months, resulting in a reduction of their stake in Tencent to 23.3%, marking a decline of 0.37%.

In the article "Tencent: Shifting from Meager Repurchases to Super AI as a Clear Strategy?", Dolphin noted that the tariff war surpassed all expectations. Despite the share price falling by over 10% again, the company refrained from conducting large-scale repurchases to support the share price, unlike its actions during the previous two crises (new online game regulations at the end of 2023 and the Ministry of National Defense sanctions list at the beginning of 2025). This strategic shift reflects a transition from "defense" to "growth," emphasizing that the importance of AI deployment surpasses all other considerations.

- END -

// Reprint Authorization

This article is an original work by Dolphin Investment Research. For reprinting, please obtain authorization.

// Disclaimer and General Disclosure

This report is intended solely for general comprehensive data use and is meant for general browsing and data reference by users of Dolphin Investment Research and its affiliates. It does not take into account the specific investment objectives, investment product preferences, risk tolerance, financial status, or special needs of any individual receiving this report. Investors must consult independent professional advisors before making investment decisions based on this report. Any person who makes investment decisions using or referring to the content or information mentioned in this report does so at their own risk. Dolphin Investment Research shall not be held liable for any direct or indirect responsibility or loss arising from the use of the data contained in this report. The information and data presented in this report are based on publicly available sources and are provided for reference purposes only. Dolphin Investment Research strives for but does not guarantee the reliability, accuracy, and completeness of the relevant information and data.

The information mentioned or opinions expressed in this report should not be construed as or deemed to be an offer to sell securities or an invitation to buy or sell securities in any jurisdiction. It does not constitute advice, inquiry, or recommendation regarding relevant securities or related financial instruments. The information, tools, and materials contained in this report are not intended for distribution to citizens or residents of any jurisdiction where such distribution, publication, provision, or use would contravene applicable laws or regulations or result in Dolphin Investment Research and/or its subsidiaries or affiliates being subject to any registration or licensing requirements in that jurisdiction.

This report reflects solely the personal views, opinions, and analysis methods of the relevant creative personnel and does not represent the position of Dolphin Investment Research and/or its affiliates.

This report is produced by Dolphin Investment Research, and its copyright is exclusively owned by Dolphin Investment Research. Without the prior written consent of Dolphin Investment Research, no organization or individual may (i) produce, copy, reproduce, duplicate, forward, or otherwise create copies or reproductions in any form, and/or (ii) directly or indirectly redistribute or transfer to other unauthorized persons. Dolphin Investment Research reserves all relevant rights.

-

![]()

Model Giant Jieyue Xingchen Steps into Smartphone Arena: A Strategic Alliance with Huaqin Technology

-

![]()

Big Model Firm Dives into Phone Market: StepFun and Wingtech Forge a ‘Dynamic Duo’

-

![]()

Zhongrun Optics Makes a Bold Move with 1 Billion Yuan Investment: Is a Turning Point on the Horizon for the Precision Optics Industry?

-

![]()

Deploy CLBO Crystals and YIG Single Crystals! Erythritol Leader Invests 30 Million in Youwei Optoelectronics

-

CXMT’s July 16 Subscription: Leading Domestic Memory Manufacturer—What’s the Earning Potential per Lot?

-

![]()

Rhythm Discrepancy and Premium Value Erosion: Foreign Luxury Brands Must Re-evaluate Their China Strategy

-

![]()

Half-Year, 1 Billion Yuan Financing, 7 Billion Yuan Valuation: A New Dark Horse Emerges in the Embodied AI Sector

-

![]()

Strong Rebound for Tech Stocks in Hong Kong Stock Market: Is It Time to Bottom-Fish?