Research on the Underlying Industrial Logic of the Booming Sales of Chinese Action Camera Brands in Japan and the Decline of GoPro: The UGC+AIGC Creation Wave Reshapes the Market Landscape

07/14 2026

07/14 2026

519

519

In early July 2026, Chinese action camera brands DJI Osmo Pocket 4 and Insta360 Luna Ultra were launched in Tokyo's Akihabara, with offline consumers queuing overnight to purchase them. Related content on social platforms surpassed tens of millions of views in a single day, creating a phenomenon-level spread.

Back in May, GoPro, once the dominant player in action cameras, announced the initiation of a strategic review, which may lead to the sale of the company or a merger.

RUNTO conducted a joint analysis of these two landmark industry events: ① The shift in market share is essentially an industry reshuffle driven by creative demand. The global scale of content creators has entered a period of rapid expansion. The combination of the democratization of UGC and the implementation of AIGC editing technology is completely rewriting the demand logic for portable imaging devices. The scalable expansion of UGC creators is the underlying growth factor, while the integrated AIGC hardware and software capabilities are the core determinants of success. ② Chinese brands are transitioning from hardware production to establishing rules for the creative ecosystem, with the competition's core shifting to a complete ecosystem where on-device AIGC adapts to UGC scenarios. Manufacturers that can match everyday recording for the general public and lower the barriers to creation will continue to capture the market and form technological barriers. Established companies that cling to niche scenarios and lag in AI creative ecosystems will see their market shares shrink.

Therefore, these two events are not isolated surface phenomena but the inevitable result of the resonance (resonance) of three factors: the transformation of the creative ecosystem, the differentiation of AI capabilities in integrated hardware and software, and the iteration of product segments.

RUNTO will deeply analyze the medium- to long-term development trends behind the industry reshuffle by combining retail market monitoring data, quantitative data on the global creator economy, market competition transformations, and the core logic of the two sides of the same coin.

I. Global Market Data Performance: After Significant Shifts, Chinese Brands Have Almost Monopolized the Market

According to RUNTO data, from January to April 2026, in the Japanese retail market for action cameras, DJI and Insta360 together accounted for approximately 85% of the market share, with GoPro and other affordable niche brands sharing less than 15% of the market. Traditional Japanese digital camera brands hardly compete in this segment.

In fact, in the Chinese action camera market, these two brands also hold a very high share. From January to May, DJI's sales market share reached 60.5%, and Insta360's was 26.1%, with the combined sales share of the two brands reaching as high as 86.6%.

In the global market, GoPro once held a 75% share. Now, according to RUNTO data, in the global pan-action camera field in the first quarter of 2026, its share has plummeted to the edge of 10%. In terms of capital market performance, GoPro reached a peak market value of $13 billion upon its IPO in 2014, but its current market value in 2026 is only $130 million, having evaporated 99% from its high, becoming a micro-cap junk stock. Additionally, it has consistently reported losses in its quarterly financial reports over the past three years.

II. Underlying Drivers: Explosive Growth in the Global UGC Creator Economy

According to RUNTO research, it is estimated that by 2026, the total number of global content creators will exceed 250 million, with a three-year compound annual growth rate of 86% from 2023 to 2026. On this basis, the scale of the global content creator economy is expected to exceed $300 billion, with annual growth rates in viewership for four major vertical content categories—short-form video Vlogs, outdoor cycling, travel documentaries, and extreme sports—all exceeding 30%. This will directly drive sustained upward demand for hardware such as action cameras and pocket gimbal cameras.

Under this wave, the action camera industry is completing a positioning shift from a 'niche tool for professional extreme enthusiasts' to a universal daily UGC recording medium.

According to RUNTO's survey of Chinese consumers, over 70% of ordinary content creators abandon secondary distribution of their material due to the high barriers of traditional editing. Therefore, lightweight and simple AIGC automatic video generation has become an important decision-making factor for users when purchasing products.

III. UGC+AIGC Dual-Wheel Drive Reconstructs Competition Standards for Action Camera Devices

RUNTO qualitatively predicts that the current competition in the action camera industry has moved beyond mere hardware parameter competition and has entered a dual-core track (track) of hardware shooting capabilities and on-device AIGC creative ecosystems.

The strategy of Chinese powerhouses DJI and Insta360 involves deeply integrating AIGC capabilities with hardware and software, incorporating features such as AI highlight recognition, automatic camera movement cropping, panoramic intelligent correction, and one-click matching of music and subtitles, thereby achieving full-link automation from 'shooting, material selection, to finished video export.' Additionally, they customize exclusive AI models for high-frequency UGC scenarios such as cycling, skiing, travel, and home Vlogs, significantly reducing post-production costs for ordinary creators and perfectly matching the needs of a vast number of long-tail UGC users.

In contrast, the shortcomings of GoPro's product line lie in the relatively lag (lagging) iteration of AI capabilities. The basic video generation functions of its Quik editing tool require a paid subscription to unlock, and its on-device local AI computing power is insufficient, only able to recognize simple motion shots and unable to adapt to everyday Vlog creation for the general public.

IV. Core Logic Behind the Booming Sales of Chinese Brands and the Decline of the Industry Pioneer

Regarding the booming sales of Chinese brands in the Japanese market, RUNTO believes that: ① There is an insufficient supply of local Japanese portable gimbal/panoramic camera products. ② DJI and Insta360's products break the stereotype that action cameras are only suitable for outdoor extremes, adapting to all scenarios for universal UGC. ③ Their native built-in localized AI video generation functions and other on-device AIGC differentiated advantages directly address the core pain points of Japanese short-form video creators. ④ Additionally, Chinese brands offer significant cost-effectiveness and ecological advantages, with pricing around 30% lower than GoPro for equivalent imaging specifications, coupled with a well-established ecosystem of third-party accessories, perfectly meeting the affordable creation needs of Japanese mass creators.

It is these four points that have led to a narrative reversal in the industry: More than a decade ago, Chinese consumers flocked to Japan to purchase Japanese imaging equipment, but now domestically produced smart imaging devices are reversely occupying the local market in the birthplace of cameras, superposition ( superposition ) with AIGC creation experience advantages, forming extremely strong brand momentum.

Regarding GoPro's global decline, RUNTO analyzes the deep-seated internal causes as follows: ① In terms of product iteration rhythm, it only updates one generation of its HERO flagship per year, with slow functional iterations and long-term stagnation in capabilities. ② In terms of product positioning, it has long adhered to a single scenario of hardcore extreme sports such as skydiving, surfing, and skiing, missing out on the universal UGC dividend; while DJI and Insta360 simultaneously cover both professional players and ordinary UGC users, opening up a billion-dollar incremental market. ③ The construction of the AIGC ecosystem is seriously lag (lagging), with a strategic mismatch to the AIGC creation cycle. GoPro's paid subscription model for creative functions goes against the needs of UGC users, and its insufficient investment in on-device local AI computing power creates a stark technological gap with domestic devices that offer zero-barrier one-click video generation. ④ The pricing of flagship models and accessory premiums weaken its competitiveness in the mass market, with customer segments being diverted. ⑤ In addition to the dimensionality reduction strike from the two domestic powerhouses, the imaging capabilities of smartphones continue to upgrade. High-end phones come with built-in wide-angle and basic electronic image stabilization, creating downward pressure on the market for low-end entry-level devices.

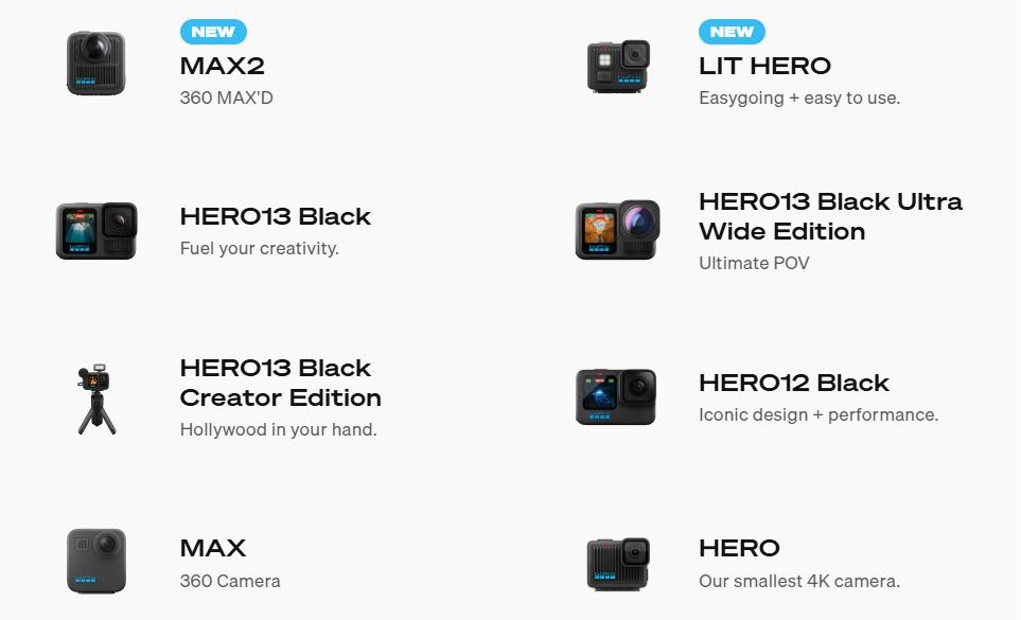

GoPro's Main Product Line for Sales in 2026

Information Source: Official Corporate Websites and the Internet

V. Three Major Trends for Medium- to Long-Term Industry Development

RUNTO concludes that the global action camera industry will primarily evolve in three directions going forward:

(1) Deep Integration of AIGC Hardware Becomes Normalized: The long-term growth space for future portable imaging devices will inevitably be tied to the continuous evolution of the universal UGC content creation ecosystem. All devices will come standard with local AI computing power, with automatic editing, intelligent camera movement, and material semantic recognition becoming basic functions. Business models that simply bundle essential AIGC functions like basic one-click editing and highlight recognition with paid subscriptions will gradually be eliminated by the mass market. A layered payment model featuring free basic AI video generation + value-added cloud services and advanced special effects will become the industry mainstream.

(2) Continuous Convergence of Category Boundaries: Traditional action cameras, panoramic cameras, and pocket gimbal cameras will mutually penetrate each other's forms, uniformly serving full-scenario UGC content production and continuously converging in form for the mass consumer market. However, professional extreme industrial-grade action cameras will remain in an independent niche segment.

(3) Intensification of the Matthew Effect in the Market: The market shares of the top two players with self-developed imaging algorithms + self-developed on-device large models + global channels will continue to solidify. For all industry participants, detach (detaching from) creator needs and underestimating the integrated layout of AIGC hardware and software will result in a continuous loss of market influence. Ultimately, the market space for small and medium-sized brands and overseas established manufacturers lacking AI creation capabilities will continue to be compressed. Additionally, beyond traditional action camera manufacturers, machine vision and smart home hardware manufacturers are also accelerating their cross-border layouts in creator shooting hardware (such as Shenmou V1 VlogCAM, Akiitu Pin by Aiketu, etc.).

-

![]()

The Voice in AI Hardware Industry is Quietly Shifting Amid Brain Drain

-

![]()

AI Enters Second Half: Buy the 'Cloud,' Not the 'Chip'?

-

![]()

Breaking the Monopoly! Trillion-Parameter Large Model Adopts Domestic Chips, Marking a Key Step Towards 'De-NVIDIA-ization' in AI Computing Power

-

![]()

Performance Drops Sharply, Seres Alerts 280,000 Shareholders

-

Behind the AI Boom: US Rakes in $314 Billion, South Korea $223 Billion, While China Lags at $26 Billion?

-

![]()

Volkswagen's 'Drastic Measures' to Cut Half of Its Models: Will China's Three Joint Ventures Be Affected?

-

![]()

It's already crowded in car manufacturing, yet Chunnan insists on joining in.

-

Confirmed: Fossil Fuel Vehicle Ban! Hainan Unveils New '15th Five-Year Plan', Weakening Passenger Vehicle Sector and Initiating Petroleum Asset Depreciation