Dream Weaver in the Eye of the Storm: Elon Musk's Business Empire and SpaceX's IPO Moment

06/18 2026

06/18 2026

341

341

Author|Yang Licheng

Editor|Chen Xiaoran

On June 12, 2026, at the Starship base in Boca Chica, Texas, there was no traditional Wall Street crystal bell to ring. Elon Musk, wearing a faded black baseball cap, stood with a dozen engineers in work uniforms in front of a large screen.

When the NASDAQ trading interface displayed the ticker SPCX and the stock price surged from its $135 IPO price, there were no cheers—only a few quiet clinks of energy drinks. For this group accustomed to explosions, failures, and late-night debugging, going public was just another milestone on a long journey.

By market close, SpaceX's valuation settled at $2.11 trillion, surpassing Meta and Tesla to become the world's seventh-largest publicly traded company. Market enthusiasm carried into Monday, June 15, opening at $171.81.

The $75 billion raised shattered Saudi Aramco's seven-year global IPO record. Musk's personal net worth soared past $1 trillion, making him history's first trillionaire.

Twenty-four years earlier, the South African entrepreneur who cashed out $100 million from PayPal to dive into the space industry had been ridiculed by the entire sector. Over two decades, he built a business empire spanning automotive, aerospace, energy, neuroscience, and social media.

Musk's business empire has always been built on what 'everyone said was impossible.'

In 2002, after cashing out his PayPal stake from eBay at age 29, Musk didn't settle into Silicon Valley's comfort zone. Instead, he made two seemingly insane decisions: build reusable rockets and electric vehicles.

At the time, aerospace was dominated by Boeing, Lockheed Martin, and NASA, with no successful precedents for private companies. The electric vehicle sector was dismissed as a fringe market—even General Motors had abandoned its EV1 program.

Against this backdrop, Musk bet most of his fortune on SpaceX while taking an investor role at Tesla, eventually seizing control.

2008 marked Musk's nadir. SpaceX's Falcon 1 failed in three consecutive launches, with funds barely covering a fourth attempt. Meanwhile, Tesla Roadster production stalled amid supply chain collapses and cash flow crises, leaving bankruptcy weeks away.

The fourth launch, scheduled for Christmas Eve 2008, succeeded. Falcon 1 became the first privately developed liquid-fueled rocket to reach orbit.

That success saved both SpaceX and, indirectly, Tesla. NASA awarded a $1.6 billion resupply contract shortly after, providing financial breathing room to pull Tesla back from the brink.

This dual crisis became etched into his business philosophy: always reserve capacity for trial and error, always believe in the last attempt. This obsessive conviction later became the foundation of all his ventures.

The 2010s were Musk's 'decade of deification.' SpaceX secured NASA's crewed spaceflight contract, with Falcon 9 achieving vertical first-stage recovery—slashing launch costs by an order of magnitude and rewriting global aerospace rules. Tesla's Model S redefined electric vehicles with intelligence and range, growing from its 2010 NASDAQ debut into a trillion-dollar automotive giant.

The 'Iron Man' label stuck. In 2016, Musk unveiled three new projects: Neuralink for brain-computer interfaces to address human-AI symbiosis; The Boring Company for underground tunnels to solve urban congestion; and the integration of SolarCity to connect photovoltaic energy storage with Tesla's power business.

Critics questioned his multi-track strategy, labeling him a 'PPT entrepreneur.' Few grasped his underlying logic: Tesla for ground transportation electrification, SolarCity for clean energy supply, Boring Company for urban spatial efficiency, Neuralink for AI-era human-machine interaction, and SpaceX for Mars transport—all orbiting 'multi-planetary human survival.'

Musk once admitted in interviews to working 120-hour weeks, often sleeping on factory conference room floors. He has virtually no material desires—no real estate holdings—with all wealth reinvested into the next project, the next gamble.

By 2021, Tesla's valuation exceeded $1 trillion, making Musk the world's richest person. In 2022, he forcibly acquired Twitter for $44 billion, renaming it X and launching a disruptive overhaul.

After firing 80% of staff, disbanding content moderation teams, and introducing paid Blue Verified badges, advertisers fled en masse, halving the company's valuation. Musk's frequent comments on COVID-19 and policies drew media and investor backlash.

Meanwhile, SpaceX quietly achieved critical technological milestones.

Starlink satellites launched at two batches per month, expanding from an initial thousand to nearly ten thousand, with users surging from millions to tens of millions—transforming from a cash drain into the company's cash cow. Starship prototypes iterated through explosions, breaking the atmosphere, validating hot-separation techniques, and testing controlled re-entry, each step solidifying progress.

Wall Street had speculated about SpaceX's IPO for a decade.

Musk repeatedly vowed to delay going public until Mars colonization became routine and Starship achieved regular flights. The 2026 IPO surprise lay hidden in the prospectus numbers.

Financial disclosures revealed $18.674 billion in 2025 revenue but $4.937 billion in net losses, with cumulative losses since inception exceeding $41.3 billion.

Starship R&D remained a bottomless pit, with each test flight costing tens of millions. Next-gen Raptor engines, orbital refueling, and lunar lander projects demanded sustained billions. Starlink's spectrum acquisitions, V3 satellite deployments, and direct-to-phone expansions required trillion-yen-scale funding. The 2026 absorption of xAI for space-based AI computing added another narrative layer—making capital needs more urgent than ever.

What gave markets confidence was Starlink's proven business model. Its 2025 revenue hit $11.387 billion (60.98% of total), with $4.423 billion in operating profit. By Q1 2026, ~9,600 Starlink satellites orbited—75% of global active satellites—with over 10.3 million subscribers across 164 countries.

From 'space junk' accusations to becoming the world's largest satellite internet operator, Starlink validated its commercial worth in a decade, becoming SpaceX's IPO 'ballast.'

Starship represented the IPO's growth narrative.

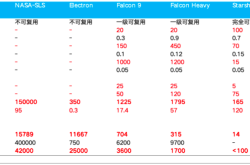

During its 12th test flight in May 2026, the third-gen Starship validated engine redundancy, satellite deployment, and controlled splashdowns—inching closer to full reusability. Once operational, launch costs could drop to 1% of Falcon 9's, enabling rapid V3 satellite deployment (60 per launch), point-to-point space travel, lunar base construction, Mars landings, and even low-Earth orbit AI computing centers—the core reason for Wall Street's 100x price-to-sales valuation.

This IPO shattered all Wall Street conventions. There was no pricing range—just a fixed $135 issue price. 30% of shares went to retail investors, far exceeding the typical 5–10% for large IPOs. Critically, a dual-class share structure gave public Class A shares one vote each, while Musk's Class B shares held 10 votes each—granting him >82% voting control with just 42% ownership.

In essence, public shareholders bought economic rights only, with Musk retaining sole decision-making power. Wall Street understood the risks but feared missing 'the next Tesla.' Pre-IPO subscriptions exceeded $350 billion—4x oversubscribed—as sovereign funds and retail investors alike rushed in.

Controversy never ceased. Notorious short-seller Jim Chanos called it a 'hope-and-dreams IPO,' arguing a company with <$20 billion in annual revenue couldn't justify a $2 trillion valuation—with a 110+x price-to-sales ratio dwarfing NVIDIA and Tesla—predicting inevitable collapse.

On IPO day, Musk avoided emotional speeches, posting only: 'This is just the beginning.'

The $75 billion raised will fuel Starship R&D, Starlink expansion, and AI initiatives. The empire's synergies will clarify as SpaceX matures: Starlink's global network can support X platform and Tesla Autopilot with universal data; Starship's low-cost launches can deploy space-based AI computing centers to train xAI's models; Tesla's battery and energy tech can power future lunar/Mars bases; Neuralink's brain-computer interfaces may solve consciousness challenges during interstellar travel.

Though seemingly dispersed, all companies revolve around 'multi-planetary human survival,' with SpaceX as the core engine.

To this day, Musk remains Earth's most controversial figure—obsessive, autocratic, and blunt, with a brutal management style perpetually at the storm's center.

Yet this very madness enabled what 'experts' deemed impossible. Twenty-four years ago, no one believed private rockets were feasible. Fifteen years ago, electric vehicles couldn't disrupt fuel-powered vehicle (internal combustion engines). Today, many still doubt Mars landings. But Musk never cared about belief—just leading teams through relentless trial and error, rebooting after failures until turning impossible into reality.

SpaceX's IPO isn't an endpoint but another ignition for this interstellar vessel—with one consistent captain at the helm.

-

![]()

Xiaomi and Others Boost Old Smartphone Battery Capacities, Power Banks Face Uncertain Future

-

![]()

Zhipu Soars to New Heights, MiniMax Faces Pressure: The Diverging Trajectories of the 'Dual Titans in Large Models'

-

AI Asset Spin-offs at Major Companies: Is Kling Paving the Way for ByteDance and Alibaba?

-

![]()

AI Agent Security Firm NewCore Raises $66 Million in Seed Funding, Achieves $300 Million Post-Money Valuation

-

From Pessimism to Optimism: China’s Hydrogen Fuel Cell Vehicles Set for Expansive Growth

-

The Race Against Time for Survival of Unitree and Its Peers

-

Dream Weaver in the Eye of the Storm: Elon Musk's Business Empire and SpaceX's IPO Moment

-

![]()

From 'Daydream' to 'Trillions in Wealth': Is SpaceX Really That 'Sci-Fi'?