Weekly Stock Review | Who Dominates the Market: Hedge Funds, Quant Traders, Institutions, or Hot Money?

07/13 2026

07/13 2026

328

328

Reviewing a Week of Automotive Stocks and Exploring the Dynamic Automotive Market.

The past week has witnessed notable volatility in A-shares.

On Monday, the Shanghai Composite Index opened at 4,041 points, the Shenzhen Component Index at 15,417 points, the ChiNext Index at 3,949 points, and the STAR 50 Index surpassed the 2,000-point threshold, reaching 1,996 points.

On Tuesday, the Shanghai Composite Index dipped below the psychological 4,000-point mark, closing at 3,990 points. The Shenzhen Component Index finished at 15,225 points, and the ChiNext Index at 3,912 points. Although the STAR 50 Index rose marginally by 0.27% to 2,002 points, it showed signs of weakness during the trading session. From Wednesday to Thursday, the market entered a period of indecision, characterized by the absence of clear trends, trading volume, and direction. The entire market oscillated within a narrow band, with trading volumes consistently shrinking and investor confidence gradually diminishing.

Particularly noteworthy was Thursday's market performance, which witnessed the strongest single-day rebound of the year, with the STAR 50 Index surging by 8.41%. SMIC's stock price jumped by 13.74% to RMB 173, with its market capitalization exceeding RMB 1.48 trillion, thereby surpassing Kweichow Moutai to claim the top spot in A-share market capitalization. Fifteen semiconductor ETFs collectively reached their daily limits.

However, by Friday afternoon, the situation took a dramatic turn. The relentless selling pressure finally took its toll, ending the market's chaos.

The STAR 50 Index initially soared to 2,233 points in early trading but encountered panic selling in the afternoon, ultimately plummeting by 5.53% to close at 2,065 points. From its intraday peak to the closing price, it dropped by 168 points, marking a significant amplitude. The ChiNext Index fell by 4.37% to 3,843 points, the Shenzhen Component Index declined by 2.29% to 15,047 points, and the Shanghai Composite Index dipped slightly by 1.00% to 3,996 points, barely maintaining its position above the psychological 4,000-point threshold.

From a capital flow perspective, overall market liquidity remained robust this week, but hot money rotated rapidly. Capital continued to flow out of high-valuation sectors such as new energy and photovoltaics, shifting towards low-valuation, stable high-end manufacturing sectors. The automotive supply chain, bolstered by solid fundamentals and policy support, emerged as a core safe haven amid this week's market turbulence, exhibiting an independent structural trend.

Industry-level differentiation was pronounced, with sectors like photovoltaics experiencing sustained net capital outflows, while physical manufacturing sectors such as defense, automotive, and machinery equipment bucked the trend by attracting capital. Notably, the automotive sector witnessed significant net inflows of main funds on Friday, ranking among the top in the market.

It is worth mentioning that the automotive sector had been in a prolonged downtrend for over a month prior, with many stocks reaching their lowest levels in nearly a year.

The underlying logic for this trend lies in two key factors: firstly, the automotive industry's fundamentals continue to strengthen, with steady recovery in domestic terminal consumption, sustained high export figures, and ongoing implementation of new energy vehicle promotion policies in rural areas, leading to resilient industry production and sales data that exceeded expectations. Secondly, the sector had undergone sufficient correction earlier, with overall valuations at historical lows and ample safety margins. Against the backdrop of valuation corrections in high-flying sectors, low-valuation, high-certainty automotive manufacturing assets now offer compelling value.

Meanwhile, this week's automotive sector trend shifted from broad-based gains or losses to precise structural differentiation. Only leading enterprises with technological barriers, global layouts, and core advantages in intelligence attracted capital inflows.

In contrast, small and medium-sized automakers and component suppliers lacking core technologies, relying on low-end mass production, and engaged in homogeneous competition continued to weaken, with their valuations contracting further.

This differentiated trend reflects the accelerating 'knockout phase' in the current automotive industry, where market capital is shifting from speculative themes and expectations towards tangible performance delivery, technological implementation, and global revenue generation. The industry's investment logic has fully returned to fundamentals.

As the undisputed leader in complete vehicles, BYD demonstrated strong resilience throughout the cycle this week, being one of the few stocks in the sector to sustain continuous capital inflows.

Amid the overall correction in the automotive sector and declining stock prices of most automakers midweek, BYD bucked the trend with a slight gain, showcasing its strong resilience. It closed at RMB 90.0 per share on Friday, up 2.28% for the week.

Just last week, BYD's stock hit a historical low, with its market capitalization shrinking to RMB 665 billion, down approximately RMB 330 billion in a few months. Three months prior, the stock was trading near RMB 108, with a market cap nearing RMB 1 trillion.

BYD's trailing price-to-earnings (P/E) ratio, which approached 250x in 2021, fell to around 28x by the end of 2025 and about 26x in early July 2026, now above the automotive sector's average. The market's valuation of BYD already includes a confidence premium for its global expansion and technological prowess.

Beyond this point, capital becomes hesitant. This is not bearishness toward BYD but skepticism about 'continuing to sell high-growth logic for a giant producing 5 million vehicles annually.' Currently, BYD's valuation sits at a reasonable low, with strong earnings certainty, making it a core holding for institutional funds in volatile markets. Its future trajectory will closely follow sales volumes and overseas business expansion.

The same logic applies to Seres. It closed at RMB 59.9 per share on Friday, up 1.32% for the week.

Since its Hong Kong listing, Seres has not only seen its A-share price plummet from a high of RMB 173.55 to nearly RMB 59 but also its Hong Kong-listed stock fall below the HKD 100 billion market cap threshold, affecting all IPO participants, both institutional and retail. Over the past six months, its stock price has followed a steady 45-degree downward trajectory.

If Seres can achieve breakthroughs in core technologies (e.g., high-voltage platforms, three-electric systems, software-defined vehicles), long-term brand operations, and overseas expansion in the coming years, it still has a chance to be revalued under a new valuation framework. However, if technological self-reliance progresses limitedly and product advantages are continuously matched by latecomers, the market premium it once enjoyed will struggle to sustain its previous market capitalization.

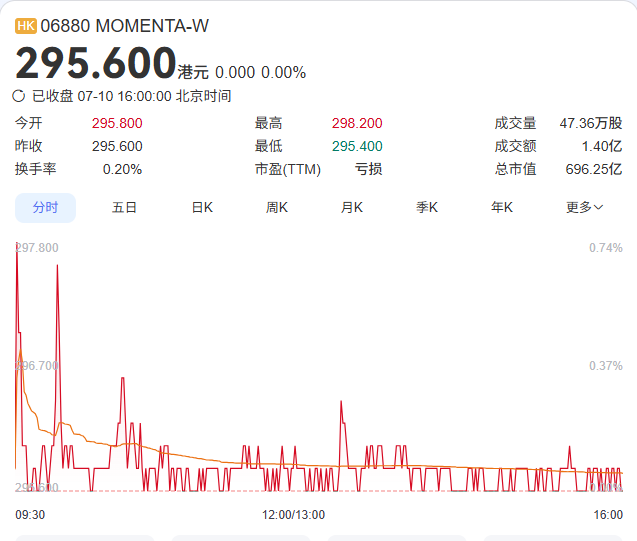

This week's most significant revaluation in the automotive sector came from Momenta, which reached a historic milestone with its Hong Kong listing. Coupled with the simultaneous launch of Mercedes-Benz's all-electric GLC, the company achieved dual highlights of 'new vehicle launch + capital market debut,' sparking a revaluation of the automotive intelligence sector.

As a leading local intelligent driving player deeply integrated with Mercedes-Benz for a decade, Momenta's partnership goes beyond simple supply chain collaboration. It represents a deep synergy model of long-term technological co-construction and capital binding, with Mercedes-Benz continuously endorsing its technical prowess through angel investments and now as a cornerstone investor.

In the short term, the listing will drive valuation repair, while in the long term, leveraging Mercedes-Benz's global mass production capabilities, the company's revenue and technological iteration will enter a virtuous cycle, positioning it as a core growth stock in the automotive intelligence sector.

From its opening price of HKD 300 per share, Momenta held firm amid a broader market downturn. Institutional support played a crucial role in this.

Moreover, Momenta's liquidity remains low, with an overall turnover rate of just 0.2%. This means only a minimal amount of capital is needed through the greenshoe option to stabilize the stock price. True valuation and capital sentiment may only become clear by the end of this month.

Considering this week's overall market and automotive sector trends, the current market has entered a phase of high divergence, emphasis on performance, and focus on delivery. Significant unilateral rallies in indices are unlikely, but structural opportunities continue to emerge. The automotive sector, combining low valuations, high earnings certainty, continuous technological iteration, and sustained policy support, remains a key allocation direction for the market.

The sector's internal differentiation will intensify, with future capital flows concentrating on three types of stocks: firstly, complete vehicle leaders like BYD, characterized by stable performance and global expansion; secondly, autonomous automakers like Geely, known for racing technology feedback and strong manufacturing capabilities; and thirdly, intelligent driving core technology firms like Momenta.

Overall, the automotive sector in mid-July has moved beyond mere speculative hype, entering a new phase driven by fundamentals, technological realization, and value repair.

In the short term, market volatility will not alter the automotive industry's core upward recovery trend. With mid-year earnings reports, continuous new vehicle iterations, and ongoing breakthroughs in intelligent driving technologies, structural opportunities in the automotive sector will further broaden, with valuation repair trends for high-quality leading stocks likely to continue.

Note: Images sourced from the internet. In case of infringement, please contact for removal.

-END-

-

![]()

Anthropic Engages with Samsung for Self-Developed AI Chips, Trend of Large Model Companies Collectively 'Building Chips' Emerges

-

![]()

Why Has Continental Evolved into a Pure Tire Company Post-'Downsizing'?

-

![]()

Zhipu’s Valuation Soars, MiniMax Faces Challenges

-

![]()

Weekly Stock Review | Who Dominates the Market: Hedge Funds, Quant Traders, Institutions, or Hot Money?

-

![]()

Sales Slump Again: Why Are Affluent Buyers No Longer Exclusively Opting for Porsche?

-

![]()

Xiaomi’s New Auto Brand Launch Sparks Stock Rebound: Is a Trend Reversal on the Horizon?

-

![]()

Seres Mid-Year Report Catastrophe: Projected Losses Surpass 1.5 Billion Yuan!

-

![]()

"Fruit Chain Brother No.1" Plummets Below Issue Price on Debut Trading Day! Chaoshan's Wealthiest Woman Stakes HK$24 Billion on AI