Net Profit Slumps 23%, Yet Musk Remains Optimistic: Big Moves Ahead for Robots and Robotaxi

07/25 2025

07/25 2025

677

677

Suspense Lingers Until Next Year

Author|Wang Lei

Editor|Qin Zhangyong

Tesla's second-quarter financial report has been released, revealing a challenging performance. Profits plummeted, marking the largest single-quarter decline in a decade.

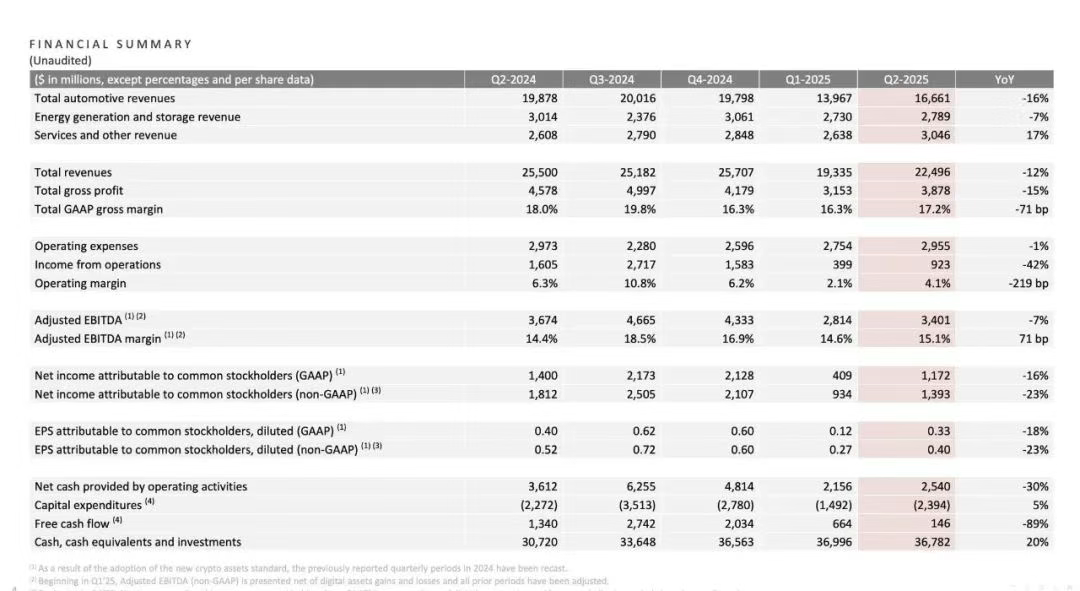

Revenue stood at $22.496 billion, a 12% year-on-year decrease, while net profit amounted to $1.172 billion, a 20.7% drop from the previous year. Free cash flow nosedived by nearly 90% to just $146 million.

Despite these figures, Musk remains unfazed. He commented that the second quarter of 2025 marks a significant milestone for Tesla, transitioning from a leader in electric vehicles and renewable energy to a frontrunner in AI, robotics, and related services.

Musk boldly declared that Tesla is moving from a phase where robots are rare to one where they are so ubiquitous that no one takes notice. In just 20 minutes, he painted a grand vision for investors, affirming that Tesla is undoubtedly poised to become the "most valuable company in the world."

Although performance fell short, Musk's confidence remains unshaken.

01 Notable Decline in Performance

Let's examine two key data points.

Tesla's second-quarter revenue was $22.496 billion, a 12% decrease from the same period last year. This decline set a record for the largest single-quarter revenue drop since 2012 and fell short of Wall Street's expectation of $22.6 billion.

Net profit stood at $1.172 billion, a 16% year-on-year decrease, while adjusted net profit was $1.393 billion, down 23% from the previous year. Adjusted earnings per share were only $0.40, not only lower than Wall Street's expectation of $0.42 but also a significant 23% year-on-year decline.

Even when considering the entire first half of the year, Tesla's overall performance continued to show declines in both revenue and profit. Total revenue for the first half was $41.8 billion (approximately RMB 299.5 billion), an 11% year-on-year decrease from $46.8 billion (approximately RMB 335.1 billion) in the same period last year.

Furthermore, net profit declined by 30% in the first half of the year. It amounted to $2.327 billion (approximately RMB 16.7 billion), compared to $3.348 billion (approximately RMB 24 billion) in the same period last year.

The poor performance of these core data points underscores the serious challenges Tesla is facing.

Specifically, looking at individual business segments, the core automotive business fell from $19.9 billion (approximately RMB 142.5 billion) in the second quarter of 2024 to $16.6 billion (approximately RMB 118.9 billion), a 16.6% decline.

For the other two segments, revenue from the energy business was $2.79 billion, down 7% year-on-year, and revenue from services and other segments was $3.05 billion, up 17% year-on-year.

The core automotive business has become a drag on performance.

The downturn in the automotive business is primarily due to weak sales. In the second quarter of 2025, new vehicle deliveries totaled 384,100, a decrease of approximately 60,000 from the second quarter of last year, representing a 13.48% year-on-year drop. While this figure exceeds the market's pessimistic expectation of 350,000, it is still the largest single-quarter decline in Tesla's history.

Many anticipated the downturn in Tesla's automotive business. After all, in recent months, Tesla has reported varying degrees of sales declines or halving in various major sales markets.

Looking at a longer timeframe, Tesla's cumulative deliveries in the first half of 2025 were also about 110,000 fewer than the same period last year. If Tesla fails to make up for this gap in the second half of the year, it is highly likely that the company will experience its first annual sales decline since 2016.

Moreover, the "double decline" in sales and gross margin is creating a vicious cycle. Tesla's gross margin for the second quarter was 17.2%, which, although up from 15.8% in the first quarter, is still below the level of over 18% in the same period last year.

The compression in gross margin is mainly attributed to various incentives such as price reductions to boost sales, leading to a decline in revenue per vehicle. Revenue per vehicle fell to $42,231 in the second quarter, a decrease of $500 from the same period last year.

Additionally, Tesla disclosed a factor that directly impacts profits: the further decline in revenue from the sale of regulatory credits.

In the second quarter, with the phasing out of US electric vehicle subsidy policies and the tightening of carbon trading, Tesla's revenue from carbon emission credits was only $439 million, a decline of over 50%. Notably, this segment represents pure profit.

Despite the recent performance lows, Musk issued a warning, stating that Tesla is in an "unusual transition period." After losing electric vehicle sales incentives in the United States, the company may face "several challenging quarters."

02 Reluctance to Discuss Cheaper Cars

While Musk himself anticipates the next few quarters to be "tough," he doesn't seem overly concerned.

Instead, during the earnings call, he continued to paint an optimistic picture, asserting that the situation will significantly improve in the future, with breakthroughs focused on autonomous driving and robotics. He set the turning point for no later than the end of next year.

First, regarding Robotaxi, Musk said that by the end of this year, about half of the US population will have access to autonomous ride-hailing services.

Since the launch of the Robotaxi trial operation in June, it has logged over 7,000 miles, receiving positive customer feedback and "no significant safety-critical incidents so far." The Robotaxi service area in Austin is continuously expanding.

Musk plans to significantly increase the service area within two weeks, reaching a scale far exceeding that of competitors. Next, the Robotaxi service will be expanded to the Bay Area, Arizona, and Florida.

"I believe that by the end of this year, half of the US population will be able to enjoy Robotaxi services." Of course, Musk added that this depends on regulatory approval, and at that time, "the Tesla Robotaxi fleet is likely to grow from tiny to giant in a very short time."

In Musk's view, Tesla's technology already meets regulatory requirements, and the safety driver in the co-pilot seat is currently only to expedite regulatory approval and is not entirely necessary.

He also mentioned that he expects car owners to be able to add their vehicles to the Tesla fleet next year, "the specific timing is uncertain but definitely next year."

Moreover, costs will be further reduced, with the cost per mile dropping to $0.25-$0.30. He also highlighted the future Cybercab model, which has the potential to reduce costs to less than 30 cents. Musk said that the design of the Cybercab aims to optimize costs.

For instance, at reduced speeds, lower-cost tires or motors can be used, and even brake costs can be minimized. Musk anticipates that Robotaxi will have a significant impact on Tesla's financial situation by the end of next year.

However, before the Robotaxi scale becomes significant, Musk still wants more people to use FSD.

Since the launch of FSD V12, the adoption rate of FSD in North America has increased by 25%. The company's vehicle safety report shows that vehicles using FSD are 10 times safer than those without it.

Nonetheless, more than half of Tesla owners have never used FSD. To encourage these owners to adopt FSD, Tesla will proactively send FSD videos and demonstrate FSD functions to them.

Furthermore, in Tesla's view, FSD is the biggest driver of car sales. Currently, Tesla has not yet obtained approval for supervised FSD in Europe. This time, Musk revealed that they are close to obtaining approval from Dutch regulators for supervised full self-driving (FSD) functionality.

"We believe that once we can provide customers in Europe with the same experience as in the United States, our sales will improve significantly."

Additionally, Musk also stated that Tesla is making significant improvements to its FSD hardware, potentially increasing the number of model parameters by 10 times, i.e., HW5, which will achieve mass production by the end of 2026.

In contrast to his elaborate discussion on Robotaxi, Musk seems less enthusiastic about Tesla's upcoming cheaper car model and prefers not to disclose too much information about it.

During the conference call, an analyst inquired about the cheaper car model, to which Musk responded, "We'll talk about it after the car is released." Later, under persistent questioning from analysts, Musk confirmed that the model had started production in June as planned and would be released in the fourth quarter.

Then, Musk remained tight-lipped...

In stark contrast, Musk dedicated considerable time to discussing the robotics business. He revealed that the third-generation robot prototype will be unveiled this year and will enter mass production next year. He even boldly stated, "I would be very surprised if we can't produce 100,000 Optimus per month within 60 months (5 years)."

He also took a dig at Google, saying that while Google excels in AI, it lags in real-world AI applications. Years of experience in producing and designing cars prove invaluable.

Finally, Musk reiterated that if Tesla executes well, it can indeed become the most valuable company in the world.

-

![]()

Li Bin Claims, 'Denying the Pure EV Trend is Like Ostrichism.' What's Li Xiang's Take?

-

Lenovo: Liu Jun Turns Left, Yang Yuanqing Turns Right

-

Lenovo: Liu Jun Goes Left, Yang Yuanqing Goes Right

-

![]()

MiniMax Shares Unlock: Cornerstone Shareholders Show Long-Term Optimism, Yet Stock Plummets Nearly 30% in Two Days; Zhipu Also Sees Nearly 20% Drop Today

-

![]()

Single-Day Plunge of 40%: The 'First AGI Stock' Faces More Than Just Share Price Concerns

-

![]()

Ricoh and Fuji Hike Prices on Legacy Edge; Insta360 Poised to Disrupt Mirrorless Camera Market

-

![]()

Ricoh and Fujifilm Raise Prices in Tandem, Relying on Established Reputations; Insta360 Poised to Disrupt Mirrorless Camera Market

-

![]()

Strategic Shift in Photoelectric Sensing: Maxvision Secures Controlling Stake in CAS Optotech