a16z's Latest AI Top 100: Leading VC Firm Unveils the Global Generative AI Race's Cutting-Edge Trends

08/29 2025

08/29 2025

632

632

Following last year's explosive growth, the generative AI consumer application market is stealthily transitioning into a new era.

Recently, Andreessen Horowitz (a16z), a preeminent global venture capital firm, unveiled the fifth edition of its "Top 100 Gen AI Consumer Apps" report, offering us a "high-definition telescope" to scrutinize the global AI consumer application landscape.

As one of Silicon Valley's most influential venture capital firms, a16z's insights into the AI sector have consistently been regarded as an industry barometer.

For research institutions and investors, this report serves as a pivotal reference for grasping industry trends and identifying investment opportunities. To this end, SV Entrepreneur specifically connected with a top VC from its expert team in Silicon Valley to offer investors an in-depth examination of the report's underlying core trends.

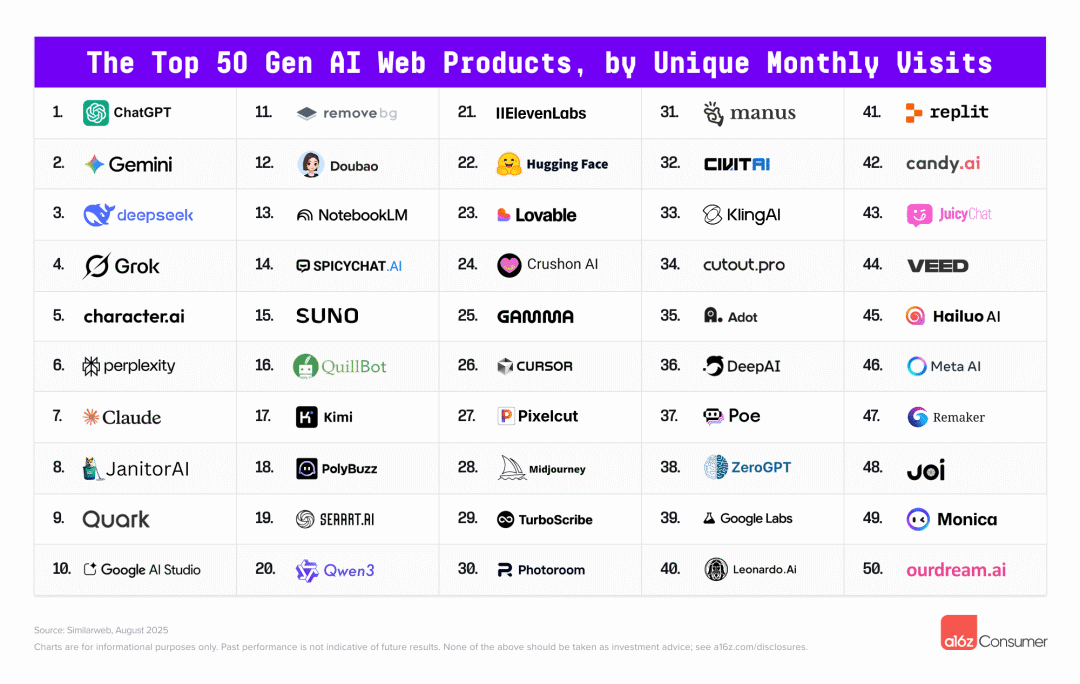

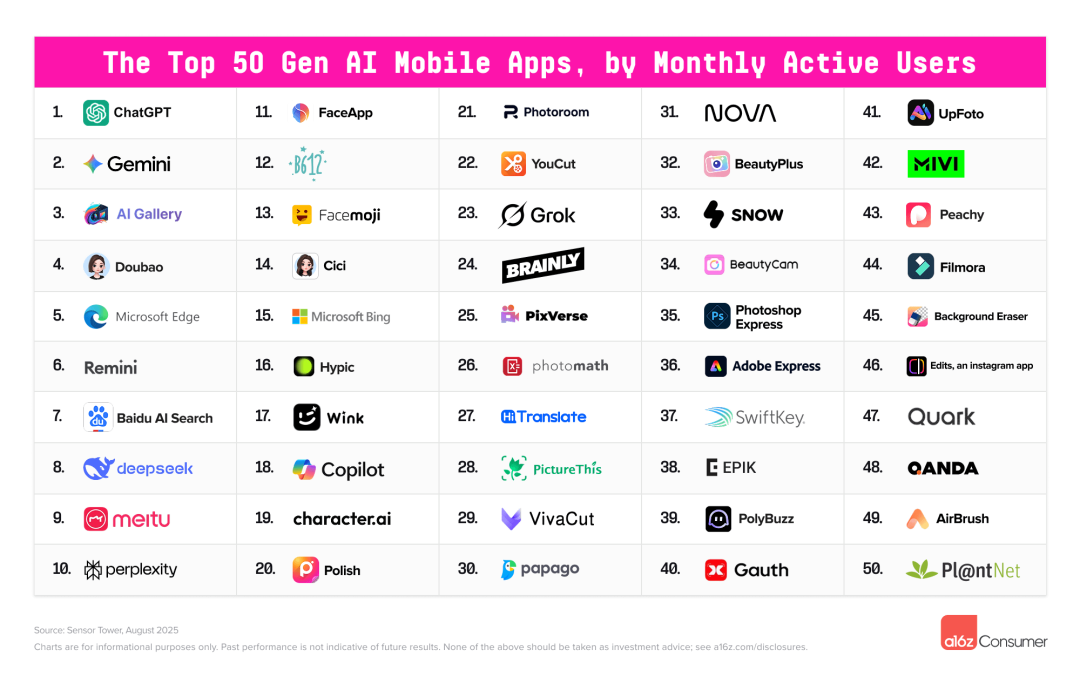

Before diving into the report's core content, it's essential to understand the criteria for selecting these applications. Methodology note: These lists are ranked based on monthly unique visitors (from Similarweb) for the top 50 AI-driven web products and monthly active users (from Sensor Tower) for the top 50 AI-driven mobile applications.

Notably, the list focuses solely on "AI-native" applications. Products like Canva or Notion, which have incorporated AI functions but did not originate from AI, are excluded. The rationale behind this criterion is thought-provoking: True AI applications must be products conceived for the AI era.

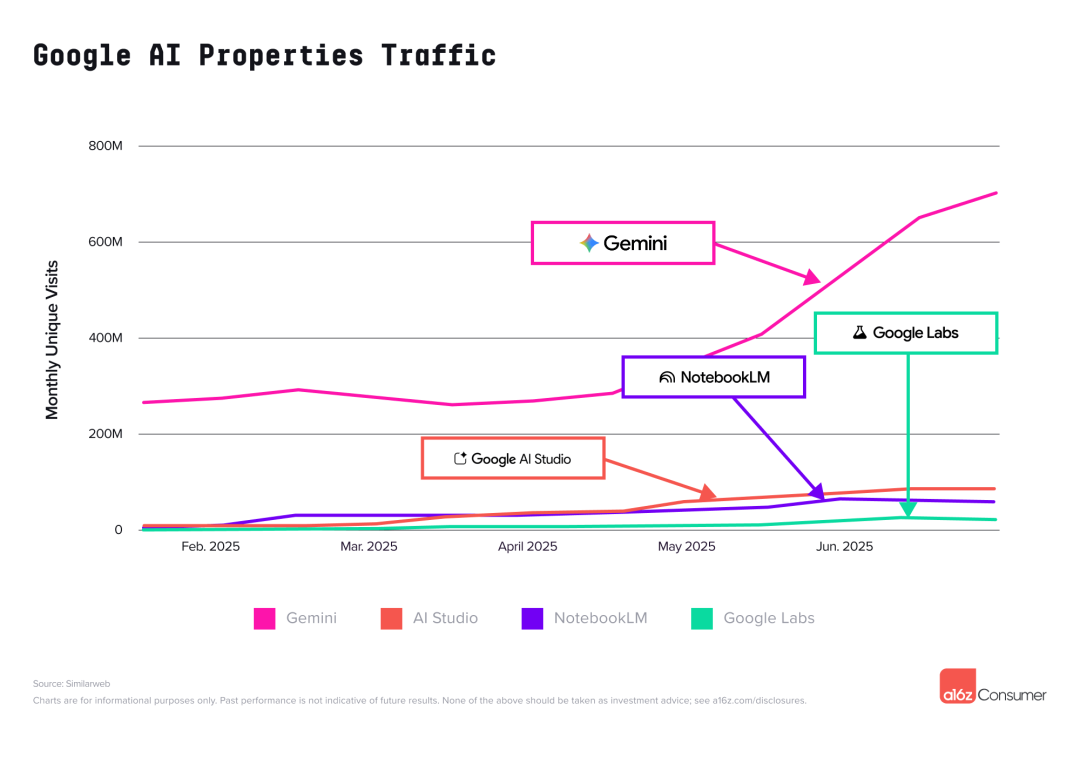

One of the most striking developments in this list is the collective debut of Google's AI offerings.

Google's general large model assistant, Gemini, ranks second on both web and mobile platforms, trailing only ChatGPT. Particularly on Android devices, Gemini shines brightly, with nearly half the monthly active users of ChatGPT.

In addition to Gemini, AI Studio for developers, the note-taking tool NotebookLM, and the AI experimentation platform Google Labs have also made the list. The strategic intent is clear: Google is leveraging its ecosystem advantages and distribution capabilities to comprehensively encircle and suppress ChatGPT.

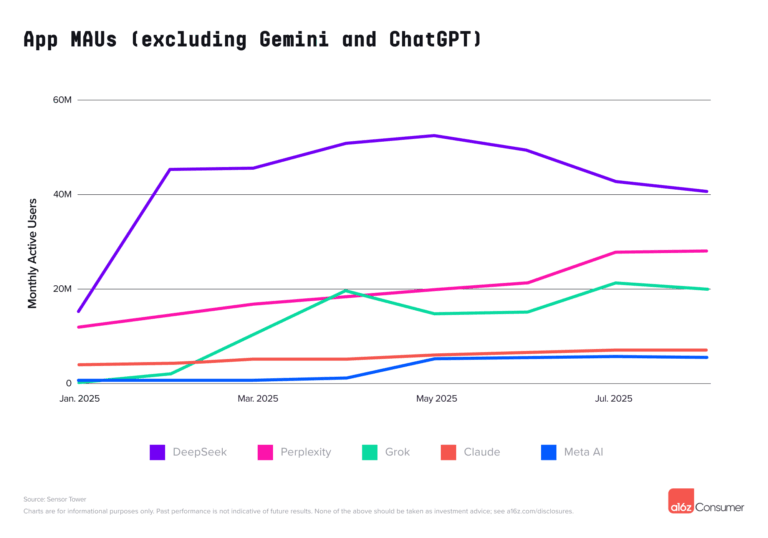

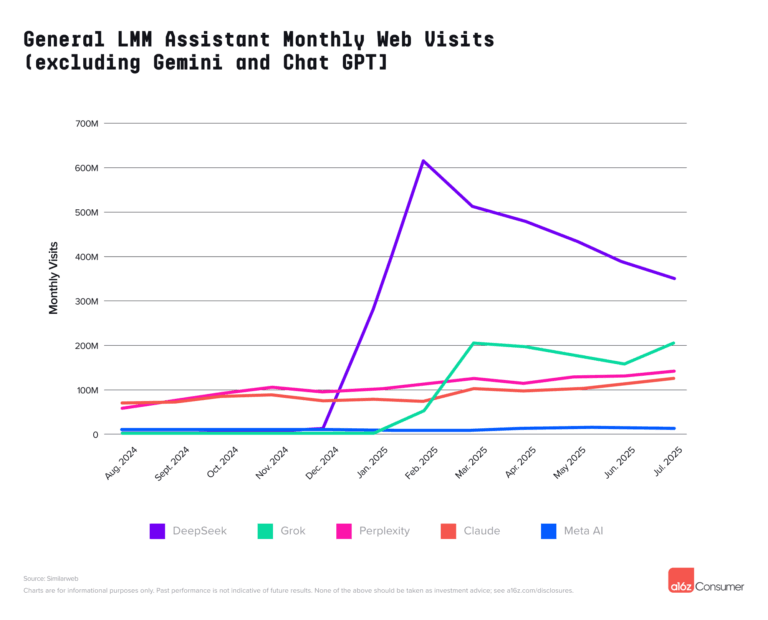

The competitive landscape for large model assistants is also undergoing nuanced shifts: ChatGPT maintains its lead, Google Gemini is surging ahead, and Musk's Grok (X platform) is growing rapidly, particularly on mobile. Meta AI is rapidly expanding, leveraging its social platform strengths.

In contrast, Claude and China's DeepSeek have witnessed slower growth on mobile.

What does this trend signify?

Many people's initial reaction is: Oh no, giants have entered the market, leaving no room for startups.

But pause for a moment. As investors, we need to look beyond the surface:

This precisely attests to the enormous user demand and commercial value of the AI assistant track, sufficient to accommodate multiple giants.

More importantly, the giants' approach is "big and comprehensive," inevitably leaving vast market gaps and innovation opportunities in numerous "small and beautiful" vertical niches. For investors, the key to decision-making lies in identifying which vertical tracks can construct moats that giants cannot easily breach.

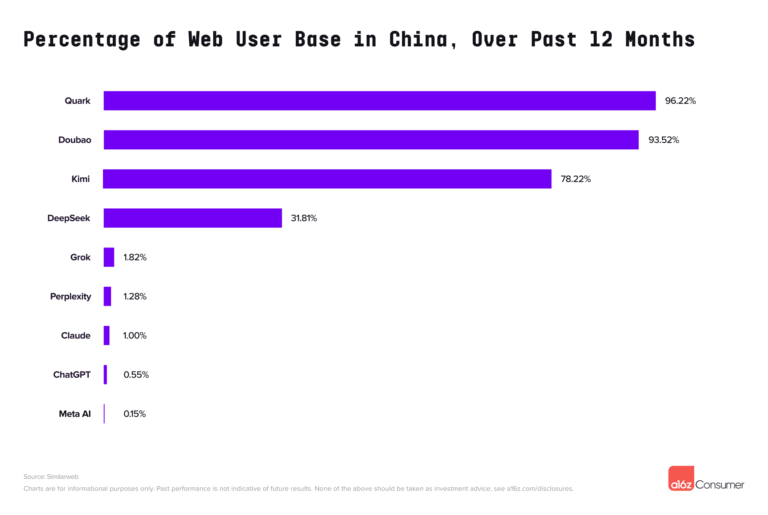

In this list, the presence of Chinese powerhouses is stronger than ever before.

But the nature of this strength is worth contemplating.

On one hand, it's the "king of the local market."

Due to regulatory constraints, foreign AI assistants struggle to directly serve the Chinese market.

This has instead spurred the development of powerful local products:

Alibaba's Quark

ByteDance's Doubao

Kimi from the Dark Side of the Moon

These products have all secured spots in the top 20 of the web list, establishing a firm foothold in the vast Chinese market.

What truly merits attention is the other aspect - "overseas warriors."

Can you believe it? Among the top 50 mobile apps, a16z estimates that 22 apps are developed by Chinese teams.

Especially in the realm of image and video editing, Meitu contributes five applications: Photo & Video Editor, BeautyPlus, BeautyCam, Wink, and Airbrush. ByteDance is also a significant player, launching apps like Doubao, Cici (general LLM assistant), Gauth (educational technology), and Hypic (photo/video editing).

What does this imply?

A clear investment theme has emerged: China's productization and globalization capabilities in the AI application layer may have been severely underestimated by the market. While everyone is still fixated on the models themselves, these companies have quietly re-established the "Made in China, Used Globally" model in the AI era.

What is "Vibe Coding"?

In simple terms, it's a method of swiftly generating and iterating web pages or applications by describing "vibes" or "feelings" in natural language.

It sounds enigmatic? But the data speaks volumes.

In the previous report, this trend was in its nascent stages. Now, platforms like Lovable and Replit have officially made the list.

More importantly, these platforms have demonstrated robust commercial potential:

User retention rates significantly exceed average applications

Revenue retention rates surpass 100% within months of registration! Paid conversion rates continue to improve

What does this signify?

It indicates that users are not only staying but also consistently purchasing additional paid services. This underscores its formidable commercial value.

For investors seeking "non-consensus" opportunities, this is a signal demanding immediate attention. It represents a novel human-computer interaction paradigm, evolving from a geeky concept into a real track with high stickiness and a high willingness to pay.

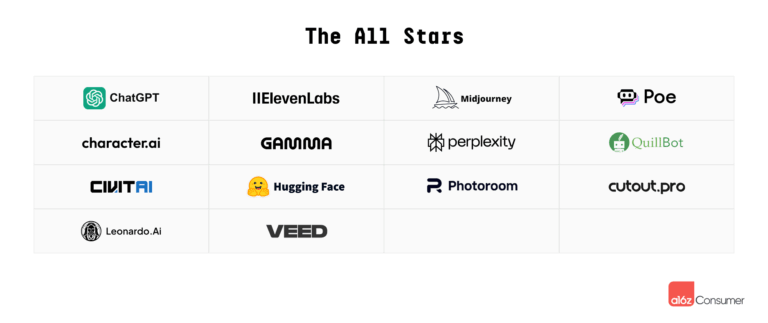

Finally, let's examine the companies that have weathered the cycles. Among the five editions of the web list, 14 companies have consistently made the cut, which a16z dubs "All Stars." These companies include: ChatGPT, Character.ai, Midjourney, Eleven Labs, etc.

But here's a groundbreaking revelation: Not all successful AI companies need to develop their own foundational models.

Among these 14 "All Star" companies:

5 have self-developed models

7 rely on APIs or open-source models

2 are model aggregation platforms

This data directly debunks the myth of the "big model theory." The core of competition in the AI era is swiftly shifting from a technical race of "who has the stronger model" to a comprehensive competition of "who has better product experiences and more successful commercialization."

This means that a plethora of investment opportunities are actually concealed within the application layer, tool layer, and middleware layer. Evaluating these companies' moats necessitates not only technical acumen but also profound insights into products, markets, and business models.

From Google's formidable entry into the market to the global output of Chinese powerhouses; from the commercialization of "Vibe Coding" to the successful path of the "All Stars"... This report by a16z paints a vivid picture of the latest battlefield in the realm of GenAI consumer-grade applications.

-

![]()

Why Hasn’t AI-Driven Payment Flourished Despite Tech Giants’ Push?

-

![]()

Intensify Efforts in the High-End Optoelectronic Semiconductor Sector! Aipu Dingchun and Jiangsu Meidong Forge a New Joint Venture

-

![]()

From Endoscopes to Optical Interconnects for AI Computing Power: A Veteran Optical Company's Strategic Shift

-

![]()

Behind the Scenes of Token Factories' Rise as a Capital Market Sensation

-

![]()

What Does MaaS Ultimately Bring to Chinese Cloud Providers? | In-Depth Industry Analysis

-

![]()

China’s Auto Resale Value Report Unveiled: AITO M9 Electric and Hybrid Variants Dominate Rankings

-

![]()

Dialogue with Huang Yangming: On the Eve of the Physical AI Boom, the Value of Data Infrastructure Begins to Materialize

-

![]()

The Experience is a Bit Unusual! Logitech G Cloud Review: Great Feel, but Not Ideal for Cloud Gaming