Discussing the Financial Reports of MiniMax and Zhipu AI: Who Will Achieve Profitability First?

04/05 2026

04/05 2026

517

517

As members of the "AI Six Tigers," MiniMax and Zhipu AI recently released their 2025 financial reports, showcasing two distinct financial profiles to the outside world.

The former delivered a C-end (consumer-side) performance heavily reliant on overseas pan-entertainment traffic, concentrating its resources and the majority of its funds on multimodal applications and front-end user interaction. The latter resembles a traditional To B cloud computing and large enterprise software supplier, focusing on the underlying infrastructure for government and enterprise digitalization and MaaS (Model as a Service).

These two financial reports demonstrate the execution capabilities of China's top AI companies in commercializing their technologies while also exposing the reality that "large models are still far from true profitability."

Despite high revenue growth, one fact remains: both companies are grappling with significant operational burdens within their respective business models.

Whether they can achieve healthy gross profit margins and positive operating cash flow will be the core criteria for determining whether these AI companies can truly navigate through the current cycle. In the deep waters of large model commercialization, there are no shortcuts for them to take.

1. Divergence in Revenue Profiles: "Quick Money" vs. "Slow Grind"

Examining the core revenue sources of the two companies reveals a fundamental divergence in the commercial nature of C-end traffic monetization and B-end cloud service delivery. This determines the pace, predictability, and ceiling of their revenue generation.

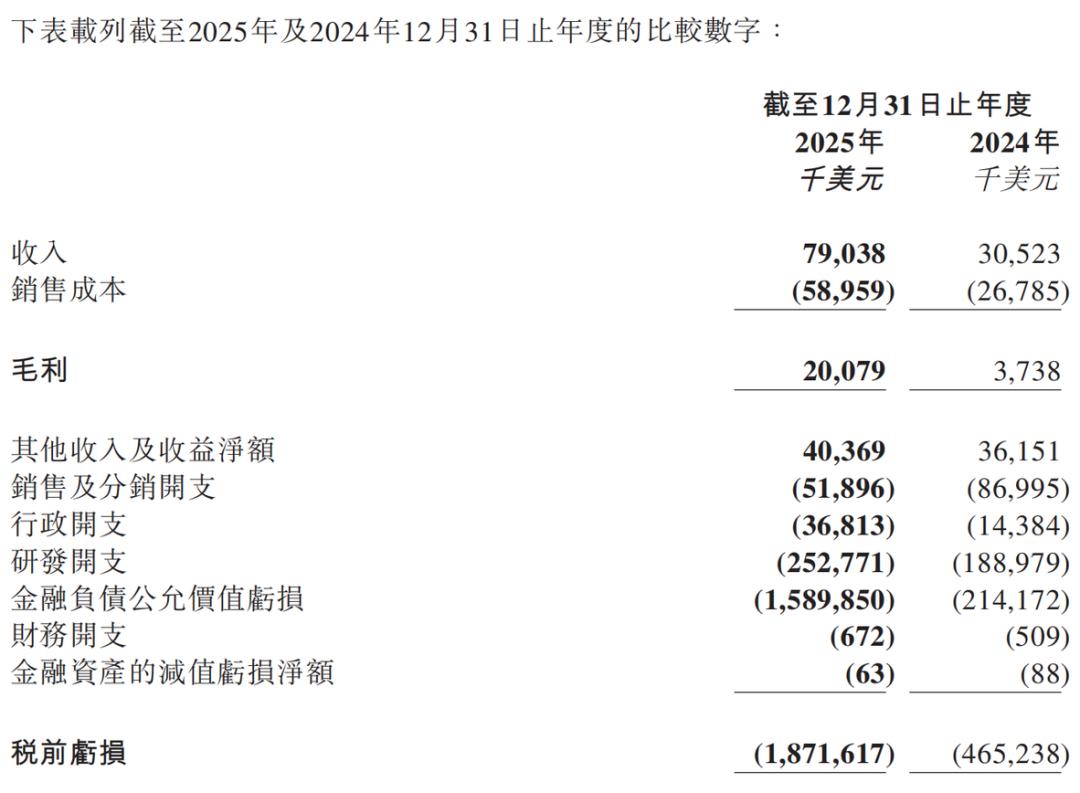

MiniMax's financial report carries a strong "Mobile Internet 2.0" vibe. In 2025, MiniMax's total revenue reached approximately $79.03 million (about RMB 560 million). Within this seemingly modest revenue pool, overseas income accounted for a staggering 73%.

Core applications Talkie (overseas version) and Xingye (domestic version) drove MiniMax's commercial ecosystem.

Its revenue loop operated smoothly over the past year: relying on high-frequency advertising placements and user acquisition through global platforms like Facebook, Google, and TikTok, cultivating user companionship habits with virtual AI characters through free conversation quotas, and ultimately monetizing through monthly subscription fees (unlocking more memory length or conversation privileges) or virtual in-app purchases (drawing character cards, voice pack items).

This playbook perfectly replicated the classic path of Chinese gaming and social apps going overseas, enabling MiniMax to achieve a steep user growth curve in its early stages, serving over 236 million users globally. However, the flip side of the coin lies in the inherent fragility of this business model.

The core dilemma faced by companionship AI products is the extremely low physical ceiling for single-user ARPU (Average Revenue Per User).

The development trajectory of overseas counterpart Character.ai has already provided a cautionary tale: after experiencing explosive early growth, it fell into a quagmire of stagnant user growth and monetization difficulties. When the novelty of interacting with virtual characters fades, user churn rates can skyrocket exponentially due to the lack of genuine social network ties.

Virtual companionship apps remain tools and content platforms heavier than social platforms, unable to form highly fortified network effects. To maintain its RMB 560 million revenue base and prevent a collapse in daily active users, MiniMax must continuously purchase traffic like a gaming company.

Financial reports show that its 2025 sales and distribution expenses reached $51.9 million, a 40.3% decrease compared to 2024. However, given its relatively small revenue scale of $79.04 million, sales expenses for traffic acquisition still constitute a heavy burden for MiniMax—meaning it spends approximately $0.66 in sales expenses for every $1 of revenue earned.

Should overseas traffic acquisition costs rise or face regulatory pushback on data privacy in specific markets, its revenue base would suffer a fatal blow.

Unlike MiniMax's reliance on C-end traffic, Zhipu AI primarily targets B-end and G-end clients, with a revenue structure characterized by heaviness and dependence on major clients.

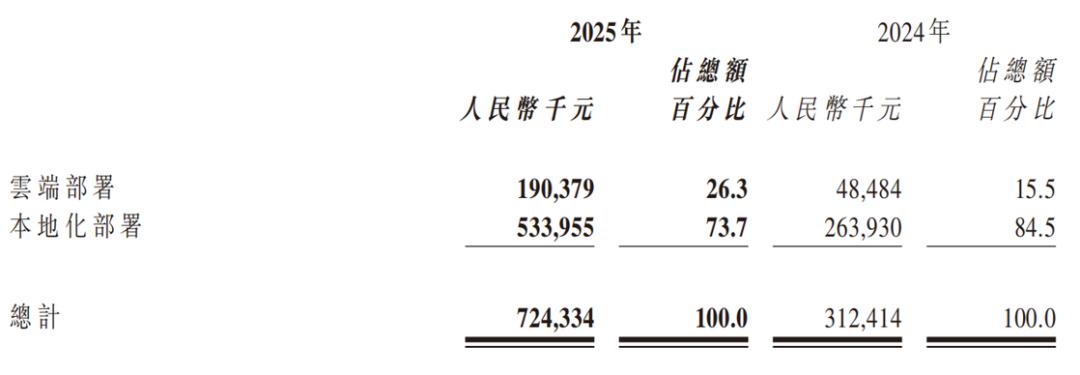

In 2025, Zhipu's overall revenue exceeded RMB 700 million, with its revenue matrix comprising four segments: open platform and API, enterprise-grade intelligent agents, enterprise-grade general-purpose large models, and technical services and others. Among these, the open platform and API represent cloud-based deployment, while the latter three are primarily localized deployments.

The MaaS business model for cloud-based deployment essentially competes with traditional giants like Alibaba Cloud, Huawei Cloud, and Tencent Cloud for large government and enterprise model service budgets.

For localized deployments, Zhipu has early established technical brand recognition in vertical sectors such as finance, manufacturing, and energy through its GLM series models.

The financial characteristics of To B businesses are evident: extremely high average contract values.

For instance, on January 16, 2026, the procurement results for the China Postal Savings Bank's large model platform engineering project (Package 1: Platform Application Software Development) (third round) were disclosed, with Zhipu winning the bid at RMB 4.0957 million.

More critically, localized private deployments often involve deep fine-tuning with enterprise private data and deep coupling with core IT systems. Models cease to be mere tools; replacement costs become prohibitively high. Switching suppliers would not only entail massive engineering costs for rewriting code and redoing security compliance audits but also risk disrupting core business operations.

Of course, the price of high certainty is the loss of explosive growth potential.

Procurement cycles for government and enterprise major clients are extremely lengthy, spanning initial requirements research (needs assessment), project approval, POC testing, strict bidding processes, to final delivery acceptance and payment collection.

This results in Zhipu's revenue growth relying on its sales team's rigid tackle key problems (project acquisition) efforts, potentially exhibiting significant volatility, especially during its growth phase. It also leads to high accounts receivable, such as exceeding RMB 300 million as of December 31, 2025, putting certain pressure on cash flow.

These characteristics mean Zhipu cannot replicate the viral growth miracles of the mobile internet era but must instead chart its growth curve through time and manpower.

2. Cost Dynamics: Escaping the Computing Power Burden and the Labor Quagmire

Both companies recorded substantial book losses in 2025, a common phenomenon among global foundational large model companies, but the causes of their losses differ.

MiniMax's losses highlight the ruthlessness of computing power economics.

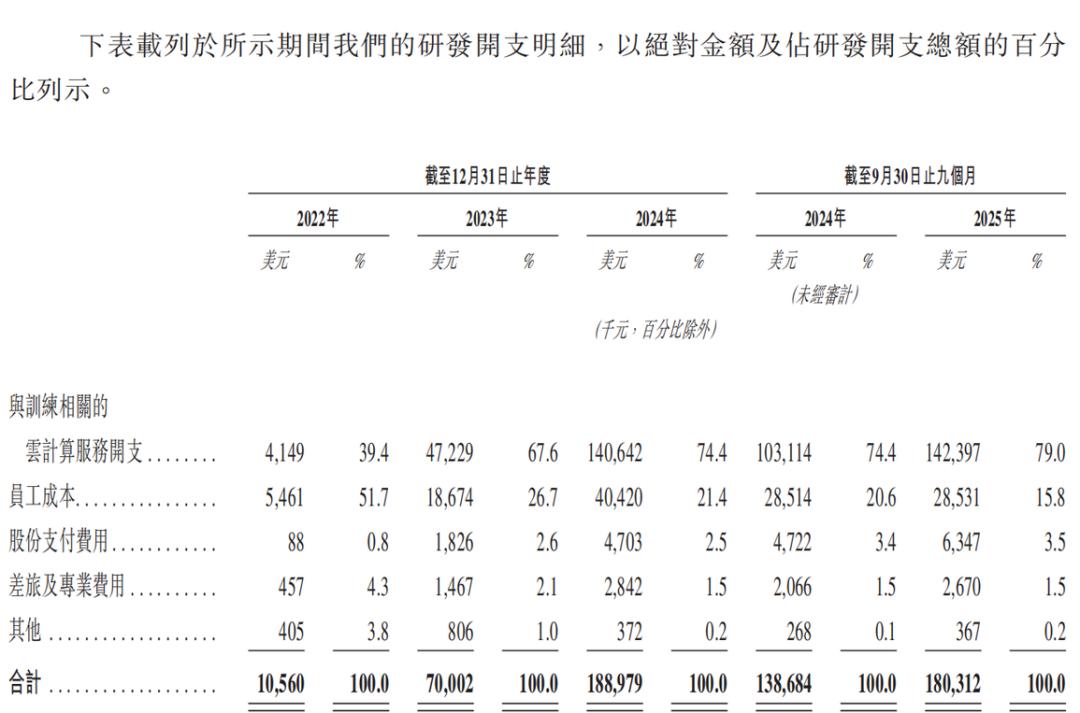

Within MiniMax's operating expenses, the most significant item is R&D, which reached $253 million in 2025, 3.2 times its revenue. Within R&D expenses, the bulk relates to cloud computing services for training, including large model training and architectural experimentation. The prospectus shows that in the first three quarters of 2025, these expenses accounted for nearly 80% of total R&D spending.

Each C-end user invocation also incurs cloud computing service fees related to inference, reflected in costs.

Calculated together, cloud computing service fees alone exceed revenue by more than threefold.

MiniMax's transformation direction is shifting from a "large model company" to an "AI-era platform company," with the core logic being to convert computing power costs from a "loss black hole" into a "scale lever" through technological innovation and business model upgrades.

On the technical front, MiniMax M2.5 adopts a Mixture of Experts (MoE) architecture, where the new-generation model activates only a subset of parameters during inference, significantly reducing single-call costs. Its API output price ranges from 1/10 to 1/20 of overseas leading models while maintaining leading model performance.

On March 18, MiniMax launched M2.7, continuing and deepening its core technological route in cost control.

On the business front, MiniMax's reliance on the C-end market is declining. In 2025, its B-end business (open platform and other AI-based enterprise services) revenue grew by 197.8%, with its revenue share increasing from 28.6% in 2024 to 32.8% in 2025.

The key observation now is whether the declining curve of computing power costs can outpace the consumption curve driven by expanding user scale.

Computing power is, of course, also a major loss point for Zhipu, but beyond that, its losses reflect the pitfalls of service economics.

Financial reports show that as of the end of 2025, Zhipu had 1,095 employees, with total compensation costs reaching RMB 1.36 billion (including share-based payments) in 2025. The reports also indicate share-based compensation expenses of RMB 558 million, meaning compensation costs excluding share-based payments were approximately RMB 800 million.

After a year of hard work, revenue was insufficient to cover salaries.

As mentioned earlier, when undertaking a project, Zhipu's engineering teams often need to be stationed at client sites for weeks or even months, assisting with internal data cleaning, model fine-tuning, knowledge graph construction, and code integration with existing legacy IT systems.

This hands-on, highly customized service model extremely strains enterprise management bandwidth and transforms what could be a high-margin standardized pure software business into a capital-intensive, low-margin IT integration project.

Thus, Zhipu aims to become "lighter."

Zhipu's lightening manifests in two ways: business structure and assets.

In terms of business structure, from the popularity of AI agents to Longxia's viral success and Token's overseas expansion, Zhipu's cloud-based deployment business has excelled.

In 2025, revenue from more scalable cloud-based deployment businesses increased from RMB 48.48 million to RMB 190 million, a 292.6% increase, accounting for 26.3% of revenue, up 10.8 percentage points, with gross margins rising from 3.3% in 2024 to 18.9% in 2025.

According to earnings call disclosures, Zhipu's cloud API business reached an ARR (annualized monthly revenue) of $250 million in March 2026.

In terms of assets, Zhipu adjusted its computing power procurement approach in 2025. While 2024 primarily involved leasing computing power equipment, 2025 shifted to a more flexible model prioritizing service procurement supplemented by equipment leasing.

3. Post-Crisis Transformations

Both companies show financial improvement, but they remain far from achieving profitability.

However, stepping outside the static 2025 financial reports and placing the two companies within the macro cycle of generative AI industry evolution, they each face market transformations capable of shaking their current business models.

Recently, leading cloud providers like Alibaba Cloud and Baidu Intelligent Cloud announced price hikes for large model-related services, marking the formal end of the fierce price war since late 2024.

On the surface, major players voluntarily halting the price war and raising API prices alleviates direct pricing pressure on Zhipu in the public cloud invocation market. However, the underlying logic of this transformation poses an even harsher test for Zhipu as an independent large model startup.

The cessation of price wars among major cloud ecosystems sends an extremely cold signal to the market: the physical costs of AI's underlying computing power (GPU inference computing) are extremely rigid, and loss-leading traffic acquisition no longer makes economic sense at the cloud computing level. Giants are beginning to retreat, shifting their core objectives from market expansion to commercial realization.

Zhipu lacks a foundational cloud computing presence at the IaaS (Infrastructure as a Service) level. The giants' price hikes mean the cost base for industry-wide computing power infrastructure is thickening.

Zhipu itself must also pay exorbitant GPU leasing and computing cluster fees to underlying computing power suppliers. With the end of the computing power Dividend period (bonus period), Zhipu, lacking self-sufficiency in computing power, will face even greater cost pressures at the underlying level.

After abandoning price wars, giants will fully pivot to leveraging PaaS and SaaS ecosystems to lock in high-value enterprise clients.

Alibaba Cloud, Tencent Cloud, and others will rely on their massive enterprise WeChat, DingTalk, and other collaborative office gateways, along with full-link cloud security services, to provide comprehensive AI solutions to government and enterprise major clients. Future B-end competition has upgraded from mere "API price comparison" to "holistic lock-in of cloud-based underlying ecosystems."

Zhipu must prove to the market that its GLM foundational models possess absolutely superior expertise in specific vertical industries compared to giants' general-purpose models and can deliver business value far exceeding deployment costs.

If it fails to win this high-value-added ecological battle, Zhipu still risks being squeezed out of core government and enterprise markets by the giants.

While giants adjust B-end strategies toward profitability, the open-source community poses a continuous threat to MiniMax at the underlying level.

Global open-source ecosystems, represented by Meta's Llama series, and domestic open-source model matrices are iterating at breakneck speed, rapidly closing the capability gap between open-source and closed-source leading models.

When underlying capabilities like long-text understanding and even multimodal generation of voice and video become freely downloadable and deployable public infrastructure, the logic of building commercial moats purely through technological gaps will no longer hold.

MiniMax's valuation system rests on its ability to continuously provide superior and exclusive multimodal experiences. When open-source models reach parity in multimodal generation, thousands of startups can leverage open-source foundations to develop low-cost alternatives to Talkie or Hailuo AI at minimal cost.

If MiniMax can swiftly solidify these "non-technical moats," the threat from open-source models will diminish. However, if application-layer operations lag, failing to rapidly accumulate massive UGC (user-generated content) digital assets and incubating highly sticky user community networks or exclusive IP, it risks becoming a mere demonstration shell for underlying technologies and facing user attrition.

MiniMax's market capitalization exceeding RMB 200 billion demands that it rapidly forge product operations and social precipitate (accumulation) into more formidable moats, creating truly super apps within a short timeframe.

-

![]()

Model Giant Jieyue Xingchen Steps into Smartphone Arena: A Strategic Alliance with Huaqin Technology

-

![]()

Big Model Firm Dives into Phone Market: StepFun and Wingtech Forge a ‘Dynamic Duo’

-

![]()

Zhongrun Optics Makes a Bold Move with 1 Billion Yuan Investment: Is a Turning Point on the Horizon for the Precision Optics Industry?

-

![]()

Deploy CLBO Crystals and YIG Single Crystals! Erythritol Leader Invests 30 Million in Youwei Optoelectronics

-

CXMT’s July 16 Subscription: Leading Domestic Memory Manufacturer—What’s the Earning Potential per Lot?

-

![]()

Rhythm Discrepancy and Premium Value Erosion: Foreign Luxury Brands Must Re-evaluate Their China Strategy

-

![]()

Half-Year, 1 Billion Yuan Financing, 7 Billion Yuan Valuation: A New Dark Horse Emerges in the Embodied AI Sector

-

![]()

Strong Rebound for Tech Stocks in Hong Kong Stock Market: Is It Time to Bottom-Fish?