Telecom Giants Launch AI Data Packages: A Game-Changer or Just Another Service?

05/22 2026

05/22 2026

655

655

Token Economics: A New Tripartite Contest

The platforms of the three major telecom operators are now directly vying with cloud service providers and large model vendors in the token market.

Recently, China Telecom, China Mobile, and China Unicom have rolled out token packages for both individual consumers and businesses, offering AI large model computing power at set prices, akin to traditional "data packages."

Shanghai Mobile is offering "1 yuan for 400,000 tokens," China Telecom has introduced personal packages starting at 9.9 yuan/month, and China Unicom is providing 30 million tokens for free testing to OPC clients in Shanghai.

(Note: Operator packages adhere to a "monthly cap" system, where unused tokens expire and excess usage necessitates additional purchases. The calculated unit prices are theoretical, with actual costs contingent on monthly consumption ratios.)

Suddenly, AI computing power has stepped into the era of "phone bills," becoming a new benchmark for operators, following SMS and data services.

Following the announcement by the three major operators, they garnered positive feedback in the capital market, with stock prices rising steadily. However, in the consumer market, few developers and enterprise users seem enthusiastic.

"The operator's token package costs 9.9 yuan in the first month, but it takes five minutes to generate the first word, resulting in very low overall efficiency. Moreover, some of the large models it utilizes are not particularly intelligent," a product manager from a cloud provider told Guangzhui Intelligence.

He drew a vivid analogy to illustrate the experience gap between using cloud provider tokens and operator tokens: "It's like you're accustomed to staying in luxury hotels and suddenly switch to a regular guesthouse—you always feel something is amiss."

Additionally, some users bluntly stated: "None of the models in the operator's token package are competitive. I want GPT 5.5 or Claude 4.7 tokens. Can other tokens really compare?"

The three major operators' foray into token sales is not met with optimism in the overall consumer market. Even the operators themselves seem unprepared, with many employees unaware of their own token package services.

In the current token economy market, cloud providers are the undisputed frontrunners, dominating most large model API channels. The three major operators' entry now undoubtedly aims to capture a share of this burgeoning market.

An expert in the telecommunications industry also noted that this is the first time domestic operators have explicitly marketed tokens as standardized telecom-grade products, bundling "tokens + connectivity + security" into an integrated pricing model. If China Telecom, China Mobile, and China Unicom follow suit, the large model API channel market may partially shift from cloud providers to the operator ecosystem.

So, why are the three major operators so keen on selling token packages? Can they compete head-to-head with cloud providers and large model vendors?

As AI computing power is billed like utilities, the three major operators are pivoting en masse, attempting to redefine their business narratives with token packages. But behind this transformation lies anxiety over dwindling traffic dividends or a genuine bid to enter the intelligent era?

Forced Transformation: The three major operators' launch of token packages may appear to sell computing power, but it is essentially a survival-driven strategy.

To understand this, one must first grasp their urgent operational conditions. According to their 2025 financial reports, revenue growth for all three operators fell below 1% (Mobile: 0.9%, Telecom: 0.1%, Unicom: 0.7%).

Additionally, MIIT data reveals that in 2025, China's data traffic volume increased while revenue declined, with traffic growing by 17.3% but revenue dropping by 3.1%. ARPU (Average Revenue Per User) continued to decline (Mobile: 46.8 yuan, Telecom: 45.1 yuan). User growth has plateaued, with mobile users exceeding 1 billion and penetration surpassing 70%, leaving little room for new growth.

Meanwhile, in 2025, the three major operators' combined capital expenditures reached 289.8 billion yuan, down 9.1% year-on-year. While overall investment is shrinking, spending on computing infrastructure is surging, with this trend intensifying in 2026.

China Telecom plans to invest 25.5 billion yuan in computing infrastructure, up 26% year-on-year, accounting for 35% of total investment. China Unicom's capital expenditures are around 50 billion yuan, with computing investment exceeding 35%. China Mobile is accelerating its computing network expansion.

This indicates that the three major operators are "suppressing traditional investments and prioritizing computing power," reducing spending on 5G networks and other traditional areas to allocate resources to AI computing power. The question remains: how to monetize these investments?

Against this backdrop, the "traffic economics" model that sustained them for two decades is no longer viable. When gigabytes of traffic can no longer drive revenue growth, and computing power dominates the market, operators must find new "pricing units."

Tokens offer this possibility, as operators control the computing power, networks, and orchestration capabilities needed to produce tokens.

Liu Liehong, Director of the National Data Administration, disclosed that China's daily token calls surged from 100 billion in early 2024 to 100 trillion by the end of 2025, exceeding 140 trillion by March 2026—a thousandfold increase in two years.

Consequently, the token economy is booming globally, with every computing power seller betting on tokens.

The three major operators are no exception. China Telecom's Chairman, Ke Ruiwen, proposed at the 2026 earnings briefing: "Focus on token services as the main business, fully transitioning from traffic operations to token operations."

China Unicom's Chairman, Dong Xin, proposed a new computing power operation model combining "Agent + Token + AI Cloud."

In summary, the three major operators' launch of token packages is a strategic choice driven by industry decline, asset idleness, and transformative changes in the era.

Their core goal is to escape "pipelineization," activate computing assets, seize AI infrastructure influence, and transform from "traffic operators" to "computing power operators" in the token economy era.

But can this succeed? Meanwhile, as they shift from partners to competitors with cloud providers and large model vendors, will they collaborate or clash?

The New Tripartite Contest in the Token Economy

With the three major operators entering the token market, players now form three factions:

First, cloud providers, including Alibaba Cloud, Tencent Cloud, and Volcano Engine, have launched Token Plan initiatives.

Comparatively, cloud providers' core logic for token packages is platform lock-in—selling not just tokens but a "model supermarket + development tools + enterprise services."

For example, Alibaba Cloud's Token Plan Team Edition charges per seat (198 yuan/seat/month), offering multi-model orchestration, Agent development frameworks, and enterprise-grade security.

(Alibaba Cloud Token Plan Team Edition pricing)

Tencent Cloud offers standard and Hy (Hunyuan) series Token Plans, bundling proprietary and third-party models. Volcano Engine introduces Coding Plan (40 yuan/month for 18,000 requests), tied to ByteDance's Doubao model ecosystem.

"Our Token Plan Team Edition aims to guide enterprise users to efficiently utilize model capabilities within controlled limits through reasonable usage caps and product linkages, avoiding disorderly consumption," an Alibaba Cloud marketing executive explained.

In their view, Alibaba Cloud's Token Plan Team Edition also helps align supply and demand, integrating its AI product ecosystem (e.g., Tongyi Qianwen, DQ) deeply with enterprise workflows, forming a closed-loop service from interaction to computation and results.

Thus, cloud providers' core logic for selling tokens remains platform capabilities.

Their advantage lies in the high migration costs for developers once integrated into their platforms, as cloud providers offer not just tokens but enterprise-grade features like log monitoring, permission management, and multi-model A/B testing.

Regarding the three major operators' token packages, Alibaba Cloud's Qianwen Cloud product leader candidly said: "Their services do pose competitive pressure, especially among price-sensitive customers who may opt for cheaper options."

However, she emphasized that Alibaba Cloud's competitiveness lies not just in pricing but in infrastructure stability, brand trust, and enterprise-grade service reliability.

Comparatively, large model vendors' core logic for selling tokens is model binding—assuming their superior models will attract developers.

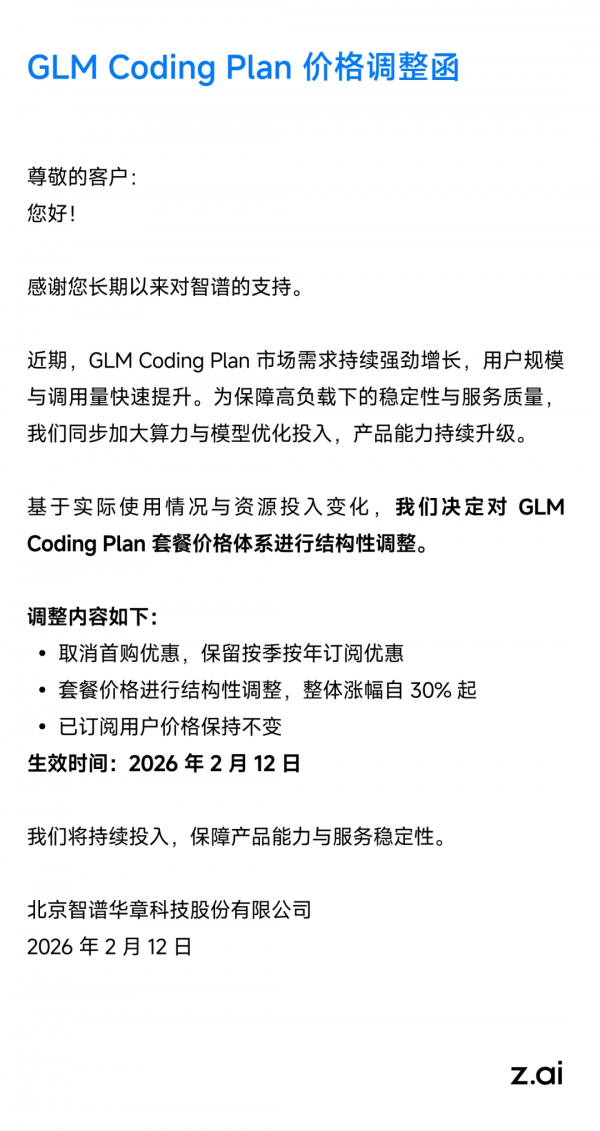

For instance, MiniMax is the world's first Token Plan supporting all modalities (text + voice + image + video + music), starting at 29 yuan/month. Xiaomi MiMo starts at 411.84 yuan/year, supporting eight models and emphasizing reasoning efficiency. Zhipu AI's Coding Plan raised prices by 30%, relying on model capabilities to sustain pricing power.

(Xiaomi MiMo Token Plan subscription pricing)

However, large model vendors face anxiety over lacking their own infrastructure, with computing costs constrained by cloud providers. When cloud providers raise prices, model vendors face pressure from both upstream costs and downstream pricing competition.

With operators joining the token fray, a battle for users, developers, and enterprise clients may ensue.

Yet, operators' token packages have not yet significantly impacted cloud providers and large model vendors, especially among enterprise users and developers.

Besides lacking competitive model pricing, operators lack a complete toolchain for AI development workflows. Developers, long accustomed to Alibaba Cloud, Tencent Cloud, and Volcano Engine APIs, face high migration costs.

Additionally, "Operators' current token packages don't integrate with our product ecosystems," the cloud provider product manager said. "For developers, their token allocations are far insufficient."

This means purchasing operators' token packages does not enable access to AI applications developed by major cloud providers.

Thus, users accustomed to mature AI applications from large vendors may face disjointed experiences if told, "Your operator tokens don't work here." Operators currently focus on building their own AI application gateways (e.g., Telecom's "Tianyi Zhinao," Mobile's "Jiutian") or integrating via APIs with specific third-party platforms.

In reality, mainstream AI applications, whether consumer- or enterprise-facing, are dominated by large model vendors and cloud providers. Each aims to monopolize users within their ecosystems, making short-term ecosystem barriers difficult to breach.

Moreover, operators lag behind leading cloud providers in model optimization, toolchain richness, and developer community operations. Their token packages often serve merely as "computing power conduits" lacking deep model optimization and application scenario closures.

Clearly, operators pose no immediate threat to cloud and model vendors. Operators' strengths lie in their 1.9 billion user base, nationwide retail outlets, phone bill payment systems, and government-enterprise relationships.

Ultimately, whoever controls developers' workflows may dominate the token economy. Cloud providers bet on "platform stickiness," model vendors on "model irreplaceability," and operators on "channel reach to 1.9 billion users."

AI Computing Power Becomes Accessible, but the Price War Subsides

Token prices will continue to decline—this is a consensus in the industry.

However, developers or tech leads at SMEs may perceive differently, as token usage costs are rising.

From late 2025 to early 2026, domestic vendors aggressively launched Coding Plans (programming subscription packages) for developers, with MiniMax at 9.9 yuan in the first month and Volcano Ark at 8.91 yuan—prices nearly "loss-leading."

The logic was simple: The Agent era is here, token consumption will surge, so acquire users cheaply first, then monetize later. But this logic collapsed in 2026.

Zhipu AI first raised Coding Plan prices by 30%. Tencent Cloud's proprietary model API prices surged by up to 463%. Alibaba Cloud and Baidu Intelligent Cloud also announced computing power price hikes.

The shift from Coding Plans to Token Plans reflects not just rising computing costs but a collective retreat from "subsidy-driven market capture" to "value-based pricing."

Why? Because token consumption growth is staggering.

With 140 trillion tokens daily, the underlying computing costs are enormous. As large models evolve from "chat tools" to "Agent execution engines," single-task token consumption jumps from hundreds or thousands to tens or hundreds of thousands.

Continuing at 2024's "per-cent" pricing would bankrupt any vendor.

So, a fascinating split emerged in the Token market in 2026: package prices for C-end users were driven down to RMB 9.9/month by operators, while API prices for B-end developers were on the rise. The barrier to accessibility was lowered, but the cost of large-scale usage was increasing.

“This year’s budget for Tokens alone is around RMB 9 million, and monthly usage continues to climb, with some monthly quotas already insufficient,” Peng Chuang, head of the AI Innovation Division at Daojia, told Guangzhui Intelligence.

It is evident that in the short term, the prices of general-purpose AI Tokens are indeed trending downward, though some models have already seen price increases. In the long run, Tokens are likely to continue becoming cheaper, but “cheaper” does not equate to “lower total cost,” as soaring usage can actually drive up actual expenditures.

A reality that must be recognized is that for businesses and developers, the “price war” for Tokens has ended.

Token pricing is now reverting to a more rational level. The RMB 9.9 package offered by operators may appear inexpensive at first glance. However, when converted to the unit price per million Tokens, it is not significantly cheaper than the pay-as-you-go pricing model provided by cloud service providers.

The operators' competitive edge does not lie in offering lower prices, but rather in providing greater convenience. They bundle Tokens with phone bills, cloud storage, and broadband services, leveraging consumers' familiar payment habits and consumption scenarios to reduce the "psychological barrier" to purchase, rather than simply lowering the "absolute price."

True accessibility does not mean keeping Tokens perpetually cheap; instead, it means making the process of acquiring Tokens as straightforward as topping up your phone credit.

From this perspective, the entry of the three major operators has indeed opened the door to widespread accessibility of AI computing power. However, behind this door, there are no longer lavish subsidizers but cost-conscious operators.

Moreover, in the era of Token packages, there is a crucial factor that many tend to overlook: framework efficiency.

Luo Fuli from Xiaomi highlighted a stark reality: if framework efficiency does not improve, the increase in Token consumption will negate any price advantages. An inefficient Agent framework can turn a simple task into the consumption of hundreds of thousands of Tokens, whereas an efficient framework might accomplish the same task with just a few thousand.

This implies that future competition may no longer center on "whose Tokens are cheaper," but rather on "whose Tokens can achieve more." The true competitive advantage in Token economics lies not in pricing power, but in the "value output per Token." Whoever can complete more complex tasks with fewer Tokens may gain the upper hand in this new paradigm.

Overall, the collective launch of Token packages represents a watershed moment in the development history of China's AI industry.

It indicates that AI computing power has finally transitioned from laboratories and developer communities to the consumption lists of ordinary people. It also signifies that the three major operators are officially transforming into "intelligent service providers," striving to reclaim their foothold in the AI era.

Simultaneously, the overall development logic of the AI industry has shifted—from a focus on who possesses more flashy technology to who can sustain a more viable business model, and from burning money for growth to leveraging efficiency for profitability.

But this is just the beginning. How will Token prices evolve over time? Will operators and cloud providers form alliances or engage in fierce competition? Are Tokens the ultimate metric for pricing AI services? None of these questions have definitive answers yet.

The only certainty is that when the three major operators start selling Tokens alongside phone bills, AI will no longer be a distant concept confined to tech news but will become the next auto-renewing service in your phone.

The Token era has truly arrived.

-

![]()

OFILM Reports Colossal 460 Million Yuan Loss: Founder Quietly Shifts Focus to Optical Modules!

-

![]()

Yutong Optics and Zeiss Forge Partnership to Develop Quality Measurement System and Launch "Optical Communication Joint Measurement Class"

-

![]()

AutoNavi Revises Splash Screen Ads with Precision Amid Controversy

-

![]()

Unlicensed Vehicle Disputes: AutoNavi Ensnared in the Aggregation Model

-

![]()

Agent: The 'Hard Requirement' for Entering Core Enterprise Systems for the First Time

-

![]()

Global Auto Market Outlook: Sales Decline in China, US, and Europe, Chinese Exports Approach 10 Million

-

![]()

AI Pioneer Breaks Free from the 'Doldrums'

-

![]()

Valuation Exceeds $26 Billion! Three Chinese "Gold Medalists" Shake Up the AI Industry