Visual China’s Hong Kong IPO: Can the Capital Story Sustained by Tens of Thousands of Lawsuits Endure?

06/17 2026

06/17 2026

355

355

On June 14, 2026, Visual China (000681.SZ) filed its listing application with the Hong Kong Stock Exchange, with Huatai International as the sole sponsor.

This marks its second foray into the capital market. After achieving a backdoor listing on the Shenzhen Stock Exchange in 2014, its market value once soared beyond 35 billion yuan, reaching remarkable heights.

Eleven years later, its A-share price has plummeted by over 70% from its peak, with its market value shrinking to approximately 15 billion yuan. Meanwhile, the actual controllers and president cashed out nearly 300 million yuan just before submitting the listing application.

With a Hong Kong IPO, a retreating founding team, and a valuation narrative bolstered by tens of thousands of lawsuits, will this be Visual China’s redemption or its finale?

I. An Idealistic Beginning: Charging Forward Amid Controversy

The story begins with a touch of idealism.

In 2000, photojournalist Chai Jijun and writer Li Xueying conceived an idea during a casual conversation: photographers had images but no buyers, while media outlets searched daily for images but couldn’t find photographers. Could they create an 'Alibaba for images'? Thus, Photocome was born, becoming one of China’s earliest online image trading platforms.

In 2014, Chai Jijun led a backdoor listing via Yuan Dong Corporation (000681), injecting Huaxia Visual and Hanhua Yimei into the listed entity and securing exclusive licenses for Getty Images and Corbis libraries in China. At a time when internet copyright awareness was just emerging, the company’s stock price surged from around 10 yuan to nearly 53 yuan, with its market value exceeding 35 billion yuan.

But all booms lead to busts. In April 2019, Visual China added humanity’s first black hole photo to its library and demanded licensing fees, followed by watermarking and selling national symbols like the national flag and emblem. Official media outlets, including the Communist Youth League Central Committee and People’s Daily, took turns criticizing the company. Regulators intervened, the website was shut down for rectification, and its market value evaporated by nearly 10 billion yuan.

However, what truly outraged the public was the incident involving astrophotographer Dai Jianfeng in 2023. He discovered that his works were included in Visual China’s collection for sale, only to be counter-sued by Visual China for 80,000 yuan. In simple terms: images you took were sold by others, who then sued you for compensation.

In November 2025, the court ruled in favor of Dai Jianfeng in the first instance. The Tianjin Heping District People’s Court determined that Visual China illegally sold Dai’s photo 'Village Under the Milky Way,' infringing on his information network transmission rights and attribution rights. The court ordered Visual China and two other companies to jointly pay 15,000 yuan in compensation and publish an apology on their official website’s homepage for 48 consecutive hours.

Neither party appealed after the judgment.

Dai Jianfeng said in an interview, 'The court organized many pre-trial mediations, which I did not accept. I learned that many others had similar experiences, and they all supported me.' He also recalled receiving death threats against himself and his family in 2023, adding, 'Now that the first-instance ruling is out, what comforts me most is that the court recognized it was inappropriate for my own photo to be used by them to demand compensation from me.'

'Village Under the Milky Way' is not an isolated case. The official account of China National Astronomy also revealed receiving similar calls, with NASA-released public domain images being claimed as Visual China’s copyright. Public domain materials had become a 'private asset' of a commercial company. This farce only lingered on trending searches for a few days.

II. Financial Reality: Core Business Bleeding, Investments Propping Up the Scene

A glance at the prospectus reveals unoptimistic data.

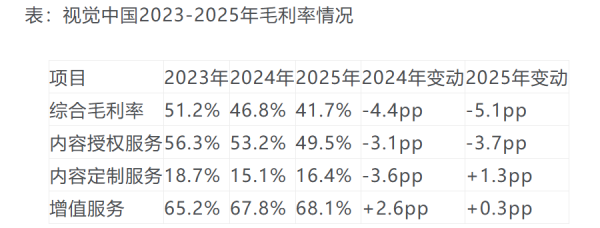

From 2023 to 2025, Visual China’s revenue stood at 781 million, 811 million, and 778 million yuan, respectively, showing an initial increase followed by a decline. Net profit slid from 154 million to 130 million and then to 93 million yuan, shrinking by nearly 40% over two years. Gross profit margin dropped from 51.2% to 41.7%, falling nearly 10 percentage points in three years.

The core 'content licensing services'—selling photos, videos, and music—generated 524 million yuan in 2025, accounting for 67.2% of revenue, a sharp 14.1% year-on-year decline. The prospectus attributed this to shrinking client budgets and AI disruption. While 'content customization services' grew 27.8% against the trend to 209 million yuan, their gross profit margin was only 16.4%, far lower than the 49.5% of licensing services.

More unsettling for investors were the Q1 2026 figures: revenue of 185 million yuan, down 2.15% year-on-year; net profit attributable to the parent company surging 1,240% to 239 million yuan—at first glance, stunning. But a closer look revealed that this was entirely propped up by 225 million yuan in fair value change gains from MiniMax’s listing. Excluding this non-recurring item, net profit after deducting non-recurring items was only 13.54 million yuan, a 17.32% year-on-year decline. The main business’s profitability had flashed a red warning light.

Additionally, the company’s book goodwill stood at 1.351 billion yuan, accounting for about one-third of total assets—a financial time bomb ready to detonate at any moment.

III. The Business of Tens of Thousands of Lawsuits: Rights Protection or 'Fishing'?

In Visual China’s business model, 'copyright litigation' plays an unspoken yet crucial role.

The so-called 'copyright fishing' process roughly unfolds as follows: disseminate images through free channels, wait for you to 'inadvertently' use them, detect this via the 'Eagle Eye' system, send demand letters, and ultimately convert you into a paying customer. Third-party platform data shows that Visual China and its subsidiaries, including Huagai Creative and Hanhua Yimei, have been involved in over 30,000 lawsuits and risk information entries, with the vast majority filed as plaintiffs, primarily for 'infringement of works’ information network transmission rights disputes.'

Based on an empirical study of 3,965 judgments, Chen Hangping, a professor at Tsinghua University Law School, identified core features of its litigation model: targeting only commercial entities as defendants, concentrating lawsuits in Guangdong, Tianjin, and Beijing courts, achieving only about 20% support for claimed amounts, and averaging around 2,000 yuan in compensation per image. Such behavior not only fails to benefit the copyright market but exacerbates the judicial contradiction of a high caseload with limited resources.

However, this 'copyright business' is now facing backlash. A design director at an advertising company told media, 'Our company used to budget over 300,000 yuan annually for legitimate images, but then we switched to AI-generated content and only faced one compliance issue in three months. Now our budget has been slashed by 60%.' He added, 'It’s not that I don’t support legitimate copies—it’s Visual China’s litigation model that intimidates our legal department. They’re not just selling images; they’re maintaining a legal team specifically to target clients.' This aligns with the grim 14.1% decline in the company’s content licensing revenue.

Beneath Dai Jianfeng’s rights protection Weibo post, a netizen commented, 'Visual China: As long as you use an image—whether taken by others or yourself—as long as you use it, I’ll come for you.' Both laughable and eerily precise.

IV. The AI Wave: Lifesaver or Mirage?

Visual China’s response strategy is to embrace AI—using copyrighted data to feed AI training.

According to the prospectus and public reports, the company has secured compliant data service orders from leading AI companies like Alibaba and Microsoft, possessing over 700 million high-quality, copyright-compliant content items for AI training. In 2025, Visual China’s outward investments reached 89.7 million yuan, up 266% from 24.49 million yuan the previous year, highly focused on AI and multimodal technology. It strategically invested in multiple AI companies, including MiniMax, Zhipu AI, and Shengshu Technology.

MiniMax listed on the Hong Kong Stock Exchange on January 9, 2026, surging over 50% in early trading and reaching a market value exceeding 76.3 billion Hong Kong dollars, setting a record for the fastest AI company IPO globally. This listing directly propelled Visual China’s Q1 2026 earnings—net profit attributable to the parent company surged 12.4 times. Visual China holds approximately 1.2% to 1.3% of MiniMax’s equity through a wholly-owned subsidiary, with a 6-month lock-up period expected to end in July 2026.

By the end of 2025, Visual China had contracted over 12,000 AI content providers, hosting over 9 million AI-generated images and videos, with cumulative sales exceeding 50 million yuan.

But this path is fraught with risks. Pricing logic for AI training data remains unclear, and whether using copyrighted library data for AI training requires additional authorization from original photographers remains an unsolved legal question. In Europe and the U.S., Getty Images has already sued AI companies over this issue, with domestic legal boundaries still to be clarified. Meanwhile, after MiniMax’s lock-up period ends, selling pressure could mount, causing sharper fluctuations in Visual China’s holding value.

V. Major Shareholders Cashing Out: A Divergence Between Confidence and Actions

Before news of the Hong Kong listing surfaced, major shareholders’ share reductions had already heightened market nerves.

On January 27, 2026, Visual China announced that its actual controllers, Liao Daoxun, Wu Yurui, and Chai Jijun, planned to jointly reduce their holdings by no more than 1.85% of the company’s total share capital via block trades and concentrated bidding from February 26 to May 25, 2026. Just before submitting the listing application, this reduction plan was fully executed. According to the reduction announcement, Wu Yurui sold 7.73 million shares, cashing out approximately 160 million yuan, reducing her stake from 10.7% to 9.89%; Chai Jijun sold 5.22 million shares, cashing out about 112 million yuan, lowering his stake from 3.9% to 3.46%. After the reductions, the trio held about 19.27% of the company.

For investors, the juxtaposition of ambitions to list on the Hong Kong Stock Exchange and the actual controllers and president quietly cashing out nearly 300 million yuan in the secondary market creates a dissonance that requires no commentary to interpret.

Liao Daoxun, Wu Yurui, and Chai Jijun are Visual China’s core controllers, founding members, and management representatives. As they cash out and exit, how will they convince new investors in the Hong Kong market that they are worth holding long-term? This itself is a highly tension-filled narrative trap.

An optimistic interpretation: a Hong Kong listing could open international financing channels, providing ammunition for AI transformation. A pessimistic view: with A-share liquidity drying up and valuations compressed, Hong Kong merely serves as another exit window for existing shareholders—both narratives may hold truth simultaneously.

VI. What Stories Can the Hong Kong IPO Still Tell?

The market environment Visual China faces is far from ideal. Global peer Getty Images saw its stock price break its issue price multiple times after listing via SPAC in 2022, with capital markets clearly pessimistic about traditional copyright libraries’ valuation logic.

Frost & Sullivan data shows that by 2025 revenue, Visual China ranked first in China’s visual content licensing services market, leading with an 8.2% market share—about 2.3 times the combined revenue of second to fifth-place companies—but holding only a 0.7% global share. The company boasts over 700 million content items, over 800,000 contracted contributors, around 300 copyright cooperation agencies, and over 400,000 cumulative paying clients, having paid a total of 3.1 billion yuan in royalties to content providers.

Put simply, Visual China’s Hong Kong story bets on a seed of 'AI data assets in the copyright realm.' With 550 million images, 800,000 contracted photographers, and over 700 million copyright-compliant data items, it does hold scarcity value amid surging AI training demand.

But 'asset scarcity' and 'sustained cash flow' are two different matters.

People view Visual China as a contradictory company. Supporters say it pioneered the digital copyright market, raising industry copyright awareness through legal means and providing monetization channels for photographers. Critics argue it turned mass rights protection into economies of scale, 'harvesting' under the guise of 'protecting copyright,' with photographer royalty splits laughably meager.

When AI can generate images for free, when users vote with their feet, and when creators sit as plaintiffs, how long can the revenue growth story propped up by rights protection last?

'We believe in the power of copyright.' This is Visual China’s frequent refrain. The question is: Do you believe in 'belief' or 'numbers'? (Produced by Zitai)

Risk Disclosure: All data herein comes from Visual China’s prospectus (submitted June 14, 2026), Q1 2026 report, A-share annual reports, China Judgments Online, Professor Chen Hangping of Tsinghua University’s research report, Frost & Sullivan, and public media reports. Analyses are for reference only and do not constitute investment advice. Investors should thoroughly read the prospectus and announcements to independently assess investment risks.

-

![]()

"One Million Kilometers": A Journey Without a Script, Where Car Owners and Honda Shine Together

-

![]()

The Supernatural Episodes of Claude Opus 4.8

-

![]()

"After Six Years of Selling A00-Class Cars, I Find Myself at a Crossroads"

-

![]()

Racing Against Time: Chinese Automakers Take Over European Factories

-

![]()

US$60 Billion Deal: Musk’s SpaceX Acquires Parent Company of ‘Cursor’!

-

![]()

Visual China’s Hong Kong IPO: Can the Capital Story Sustained by Tens of Thousands of Lawsuits Endure?

-

![]()

In-depth | Survival Transformation of 38 Million Freight Drivers: How Platformization Defines the Next Decade?

-

![]()

Why Have ‘Computing Power Rental’ Companies Emerged as the Biggest Winners in the AI Era Amid Soaring Chip Prices?