Ruiyun Lianchuang's Haste for Hong Kong Stock Listing: Balancing Large Dividends with R&D Fundraising

07/08 2026

07/08 2026

416

416

Recently, Xiamen Ruiyun Lianchuang Innovation Technology Co., Ltd. (hereinafter referred to as 'Ruiyun Lianchuang'), which has earned the reputation of being the 'leading provider of smart intercom solutions in North America and Europe,' is pressing ahead with its plans for a Hong Kong stock listing. However, its journey towards listing has quickly drawn regulatory scrutiny. The China Securities Regulatory Commission (CSRC) has requested additional materials concerning the company's overseas issuance and listing filing, directly highlighting several compliance issues. These include equity nominee arrangements, potential benefit transfers through employee stock ownership plans, whether the shareholder count has hit the 200-person threshold, and the implementation of rectifications for customs administrative penalties.

Beyond these compliance concerns, the company's operational fundamentals also present risks that warrant close attention. A review of the prospectus by Securities Star reveals that while this technology company, with a strong focus on overseas markets, has achieved growth in both revenue and profit, there are underlying concerns. These include the fact that overseas income accounts for over 90% of total revenue, a persistent decline in R&D spending as a percentage of revenue, and simultaneous increases in inventory and accounts receivable.

01. Single Product Line Fuels Performance, Overseas Income Dominates at 90%

According to the prospectus, Ruiyun Lianchuang, established in 2016, specializes in providing smart intercom solutions. Its offerings encompass AI-powered smart intercoms, access control systems, smart home devices, and cloud services tailored to various scenarios.

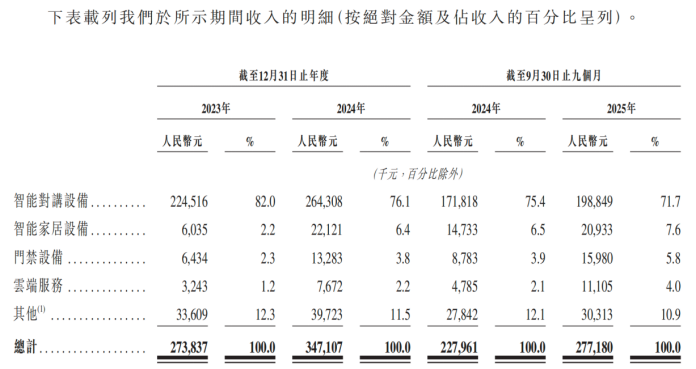

From a financial standpoint, the company reported revenues of RMB 274 million, RMB 347 million, and RMB 277 million for the years 2023, 2024, and the first three quarters of 2025, respectively. Net profits for the same periods were RMB 38 million, RMB 53 million, and RMB 45 million, respectively, indicating an overall trend of fluctuating growth.

In terms of revenue composition, although the contribution from smart intercom devices decreased from 82.0% at the start of the reporting period to 71.7%, it remains the primary revenue source for the company. Meanwhile, emerging businesses such as smart homes, access control equipment, and cloud services have seen increased revenue contributions. Nevertheless, the company's overall performance still heavily relies on this single product line.

From a market perspective, the company's revenue is highly concentrated in overseas markets. During the reporting periods, income from markets outside mainland China accounted for 97.1%, 95.2%, and 91.8% of total revenue, respectively, underscoring a significant overseas presence.

Ruiyun Lianchuang asserts that its business spans over 110 countries and regions globally, with long-standing cooperative relationships established with more than 180 distributors across 66 countries and regions. However, in terms of revenue contribution, the company's overseas operations are predominantly concentrated in the European and North American markets. During the reporting period, revenue from North America accounted for 23.7%, 22.3%, and 26.3%, respectively, while Europe contributed 32.3%, 31.0%, and 23.9% during the same periods. Although the combined revenue share from these two regions declined from 56% to 50.2%, they still constitute half of the company's total revenue, highlighting regional concentration risks that are not to be overlooked.

More notably, in these two highly dependent markets, the company's competitive edge is not particularly strong. According to data released by Frost & Sullivan, based on shipment volume in 2024, Ruiyun Lianchuang has emerged as the largest provider of smart intercom solutions in North America and Europe. However, in terms of market share and revenue scale, the company still trails behind regional leaders.

Specifically, in 2024, the company generated USD 9.2 million in revenue in the North American market, capturing a 9.3% market share and ranking second. In contrast, the leading enterprise, Company B, reported USD 13.7 million in revenue during the same period, with a 13.8% market share, maintaining a substantial lead. In the European market, the company's revenue was USD 11.3 million, with a 12.5% market share, ranking third. The top two players, Company C and Company D, recorded revenues of USD 28.6 million and USD 12.9 million, respectively, with market shares of 31.4% and 14.1%.

As revenue continues to concentrate in overseas markets, the company's accounts receivable have also increased, reflecting its relatively weak bargaining power in overseas channels. During the reporting period, trade receivables rose from RMB 28.5 million at the end of 2023 to RMB 61.6 million by the end of September 2025, while the days sales outstanding (DSO) extended from 30 days to 46 days. Meanwhile, overseas distributors typically demand credit terms ranging from 30 to 180 days, and the longer settlement cycles further exacerbate the company's capital occupation pressure.

Additionally, the company's inventory levels have also shown an upward trend, rising from RMB 49.496 million at the end of 2023 to RMB 73.271 million by the end of September 2025, with inventory turnover days increasing slightly from 129 days to 134 days.

02. Declining R&D Spending Ratio, Smart Home R&D Projects Put on Hold

As a technology company that positions 'AI-driven' as its core selling point, Ruiyun Lianchuang's stance on R&D investment has gradually become nuanced and somewhat contradictory.

According to the prospectus, the company's R&D expenditures were RMB 61.546 million and RMB 68.911 million in 2023 and 2024, respectively. Although there was a slight absolute increase in 2024, the proportion of R&D spending relative to revenue declined from 22.5% to 19.9%. In the first nine months of 2025, R&D expenditures shrank to RMB 45.578 million, representing a 6.6% year-on-year decrease. The company attributed this change primarily to the discontinuation of R&D projects for smart home devices.

It is worth noting that the smart home device business experienced revenue growth during the reporting period. The business generated revenues of RMB 6,035 and RMB 22,121 in 2023 and 2024, respectively, and further climbed to RMB 20,933 in the first nine months of 2025 from RMB 14,733 in the same period of the previous year.

Notably, the revenue contribution from smart intercom devices, the company's main revenue pillar, declined slightly. However, from an industry perspective, the global smart intercom market is projected to reach USD 1.13 billion by 2029, with a compound annual growth rate (CAGR) of 22.4% from 2025 to 2029, indicating a relatively robust growth trajectory. Against the backdrop of deep penetration by AI, IoT, cloud computing, and other technologies, smart intercom devices are evolving from single communication tools into integrated security and smart home control centers. To maintain or expand market share in this technological upgrade cycle, sustained and robust R&D investment is essential. However, given the company's actual R&D spending, whether it can keep pace with industry advancements remains a genuine concern.

Ruiyun Lianchuang is clearly cognizant of this industry trend. From its fundraising plans, the company explicitly intends to allocate a portion of the raised funds towards hiring and retaining R&D personnel, developing new smart community solutions, and constructing and upgrading R&D centers, in an attempt to 'catch up' on R&D.

However, in stark contrast to the sense of urgency for R&D reflected in the fundraising plan, the company has opted to distribute large dividends for three consecutive years on the profit distribution front. The prospectus reveals that the company paid dividends of RMB 39.6 million, RMB 52.7 million, and RMB 52.8 million in 2023, 2024, and the first nine months of 2025, respectively, with cumulative dividends exceeding RMB 145 million, effectively distributing nearly all profits to shareholders during these periods. Compared to its operating cash flow performance, net operating cash flow was RMB 69.627 million, RMB 56.199 million, and RMB 52.108 million in 2023, 2024, and the first nine months of 2025, respectively, with dividend scales continuously approaching operating cash inflows during these periods.

Securities Star notes that the direct beneficiaries of these substantial dividends are likely controlled by the controlling shareholder, Yuan Tao, through Chuangzhi Shidai. Based on shareholding ratios, over half of the dividend funds ultimately flow into the pockets of the actual controller. (This article is first published by Securities Star, Author | Xia Fenglin)

- End -

-

![]()

OFILM Reports Colossal 460 Million Yuan Loss: Founder Quietly Shifts Focus to Optical Modules!

-

![]()

Yutong Optics and Zeiss Forge Partnership to Develop Quality Measurement System and Launch "Optical Communication Joint Measurement Class"

-

![]()

AutoNavi Revises Splash Screen Ads with Precision Amid Controversy

-

![]()

Unlicensed Vehicle Disputes: AutoNavi Ensnared in the Aggregation Model

-

![]()

Agent: The 'Hard Requirement' for Entering Core Enterprise Systems for the First Time

-

![]()

Global Auto Market Outlook: Sales Decline in China, US, and Europe, Chinese Exports Approach 10 Million

-

![]()

AI Pioneer Breaks Free from the 'Doldrums'

-

![]()

Valuation Exceeds $26 Billion! Three Chinese "Gold Medalists" Shake Up the AI Industry