SpaceX: Space Computing Power - Musk's New Vision or Real Future?

07/09 2026

07/09 2026

394

394

In the article 'SpaceX: As AI Burns Money Endlessly, Is 'Space Computing Power Hegemony' the Ultimate Killer Move?' by Dolphin Research, it is mentioned that space data centers are not only the most crucial part of SpaceX's grand narrative but also the largest 'option value' in its future valuation.

To realize this vision, SpaceX has formulated a seemingly insane 'space computing power deployment timeline':

1. 2028: First batch of computing satellites enters orbit: The first batch of orbital AI satellites, 'AI1,' is expected to commence large-scale commercial networking in 2028. These satellites will have a wingspan of up to 70 meters and an average power consumption of 120kW (peak 150kW), resembling floating power stations in space.

'Starship + Self-Built Chip Factory' Dual Engines: Between 2028 and 2031, SpaceX will launch two groundbreaking infrastructure projects: one is the ultra-high-frequency heavy-lift launches of Starship (V3 can launch 100 tons into orbit per launch, with a long-term goal of producing and launching 10,000 ships annually); the other is its Texas-based Terafab chip factory (using a 2nm process, with a long-term goal of producing 1TW of computing power annually, about 800GW dedicated to space).

2. After 2030: Transporting 1 million tons of computing power to space annually: With the combined support of transport capacity and computing power, SpaceX plans to achieve the annual transport of 1 million tons of computing hardware into orbit within 4-5 years (i.e., 2030-2031). Calculated at 100kW per ton of hardware, this corresponds to an annual Add (xīn zēng, 'newly added') capacity of 100GW of space computing power deployment, with an ultimate goal of reaching 1TW (1,000GW).

For comparison, the current total AI computing power accumulated by major global cloud service providers (CSPs) on Earth is only in the range of 30-50GW. This means that SpaceX's annual 'increment in space computing power' alone is equivalent to recreating two to three 'global cloud computing totals' in space. If this plan materializes, it will completely break through the energy and land growth ceilings faced by ground-based computing power.

Faced with such a disruptive industrial landscape, this research by Dolphin Research will focus on the following two core questions:

1) Is the transition from ground exercises to 'space computing power hegemony' a splendid interstellar sci-fi or a 'dimensional reduction strike' against traditional tech giants?

2) Faced with such a vast and unprecedented commercial closed loop (bì huán, 'closed loop'), how should we value SpaceX, this super unicorn?

Below is the main text

I. The Soul-Searching Question: Can Vacuum Heat Dissipation Work? Almost There

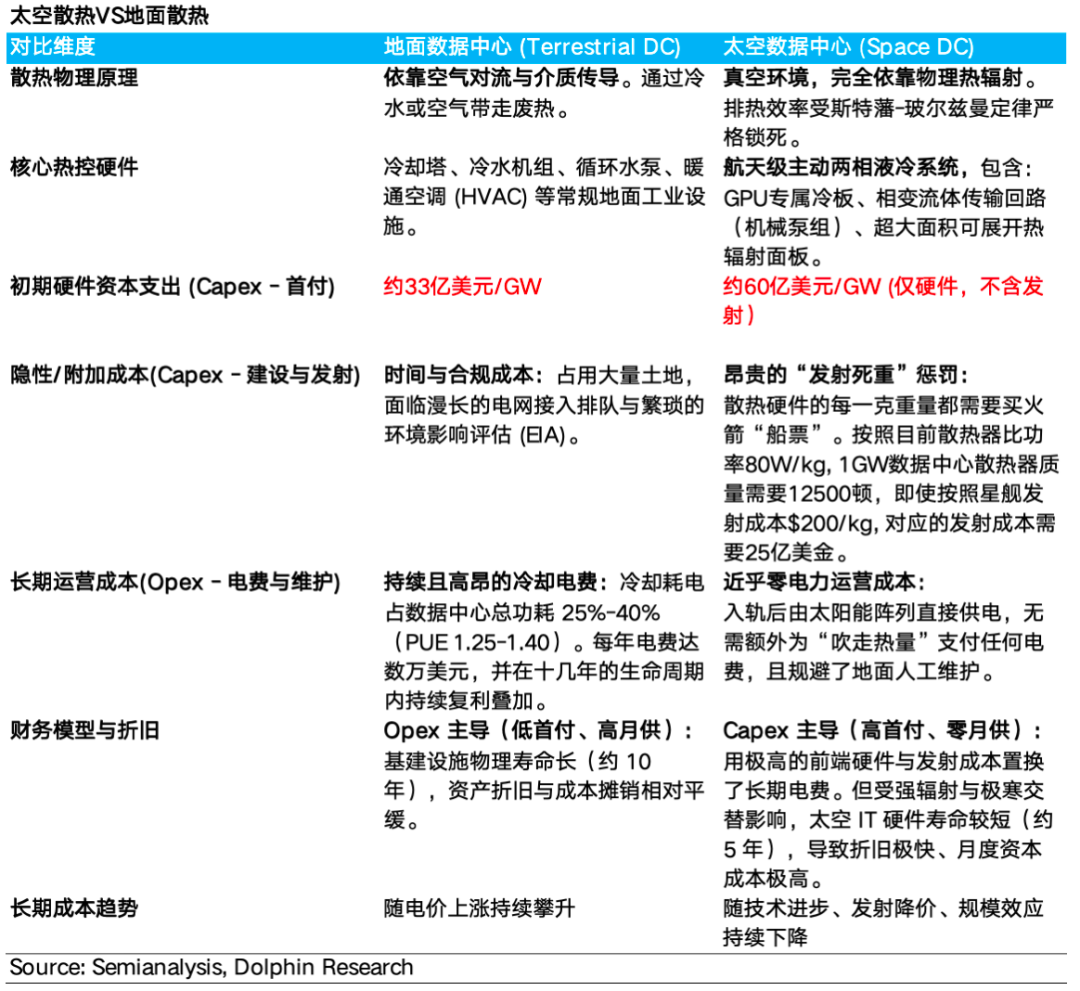

Ground-based AI data centers are already challenging, but space presents even greater difficulties due to the vacuum environment, which lacks convection and relies solely on thermal radiation to emit heat into deep space in the form of infrared radiation. However, under the same temperature difference, the heat dissipation efficiency is only 1% of that of ground-based air convection.

Heat dissipation is the first major technical obstacle for space computing power, with a priority even higher than deployment costs and space radiation. In a vacuum, 'how to expel heat' is the physical prerequisite for all computing activities.

Currently, SpaceX faces several major dilemmas:

a. Area Limitation: Based on physical laws, the radiation power increases with higher temperatures, larger heat dissipation areas, and higher surface emissivity, leading to faster heat dissipation. However, at a high cabinet temperature of, say, 70°C, the radiation heat dissipation limit is only 880 W/m² . A 1.5MW data center requires 2,100 m² of heat dissipation plates (about 1/3 of a football field), far exceeding the volume of a rocket fairing.

b. Heat Dissipation Arrays as Targets for Space Microparticles? Due to their large area, 1mm micro-debris in space can puncture the thin heat dissipation walls when impacting at orbital speeds.

In addition, low-Earth orbit satellites experience drastic light-dark cycles with temperature differences exceeding 250°C (+120°C to -160°C) every 90 minutes. Such violent thermal shocks can easily cause chip packaging to crack or pipeline fatigue leaks. Since space cannot be manually repaired, a single puncture and leak will result in complete heat dissipation failure and the entire satellite becoming scrap.

c. High Costs: Currently, the International Space Station adopts a customized aerospace model, with heat dissipation costs as high as $4.5-6.6 million/kW. Even with commercial cost reduction and mass production, the pure heat dissipation hardware cost is still $6 billion/GW, nearly twice that of ground-based data centers ($3.3 billion/GW).

d. Freight Cost Disparity: Based on the current status of the Falcon 9, transporting this 'heat dissipation dead weight' into orbit costs as high as $23 billion/GW (nearly four times the cost of heat dissipation hardware). Even if Starship freight costs drop to $200/kg in the future, the total launch cost in 2026 (with a specific power of 80W/kg) will still be $2.5 billion/GW; it is not expected to drop to $1 billion/GW until 2032 after thermal control iterations (specific power of 195W/kg).

Faced with the above contradictions, space data centers must find a balanced solution among 'efficiency, weight, and reliability':

a. Trade Lifespan for Area (Increase Temperature Threshold): Utilizing the physical characteristic that radiation efficiency is proportional to the fourth power of temperature, allowing chips to operate at full capacity at 85-100°C. For every 20°C increase in temperature, the heat dissipation area can be compressed by 15%-25%. The trade-off is sacrificing reliability and accelerating chip depreciation (GPU and HBM operating above 85°C for extended periods will accelerate failure modes).

b. Trade Power Consumption for Space (Active Liquid Cooling Decoupling): Adopting a 'cold plate → active pump → coolant → external radiation plate' transport path. Although this adds an additional 2%-4% power consumption and the risk of pump failure, it removes the geometric restriction that chips and heat sinks must be 'tightly attached.'

c. Trade Weight for Cost (Material Downgrading and Folding Deployment): Abandoning expensive aerospace materials and using ordinary 6061-T6 aluminum alloy with good thermal conductivity but relatively high weight, following the logic of 'cheap dead weight for low manufacturing costs.' During launch, it can be folded like an 'accordion' and then massively deployed after entering orbit.

d. Trade Redundancy for Risk Resistance (Independent Modular Honeycomb Piping): Reusing the engineering experience from Starlink, adopting an integrated chassis with radiation fins and designing the liquid cooling piping as an independent modular honeycomb network. In the event of an impact, a leak in a single piping section can be instantly physically isolated, effectively preventing systemic total loss caused by a single point of failure.

From a technical perspective, the active liquid cooling + deployable heat sink approach is theoretically feasible but still in the engineering verification stage and has not undergone large-scale deployment testing.

II. Space Radiation: Will It Fry the Chips? Not a Big Problem

In semiconductor physics, the core indicator determining whether a transistor will be affected by radiation is the 'critical charge'—the minimum energy required to trigger a transistor state flip (0→1).

As chip processes evolve from 28nm to 3nm and even smaller, transistor volumes shrink dramatically, and operating voltages decrease significantly, causing the critical charge to decline exponentially.

High-energy particles in space can easily cause single-event upsets (SEUs, data errors) and single-event latch-ups (SELs, short-circuit burnouts); however, traditional radiation-hardened large-process chips lack sufficient computing power for AI tasks.

SpaceX's solution is to accept localized errors while ensuring system stability:

a. Orbital Advantage: Deploying in 500–1000km LEO/SSO, utilizing the Earth's magnetic field to deflect most high-energy particles and reduce radiation flux at the source.

b. Heterogeneous Architecture Separation: Using 3nm GPUs for computing (the 'brain') and 65/28nm radiation-hardened FPGAs/MCUs for monitoring (the 'cerebellum'), detecting abnormal currents in real-time and cutting off/restarting the GPU within milliseconds to prevent burnout risks.

c. Spot Gradient Shielding: Abandoning the full-cabinet heavy metal wrapping scheme and only covering extremely thin coatings of 'low Z polymer + high Z tantalum/tungsten' above the GPU and power management chip cores to suppress secondary radiation while balancing thermal conductivity and lightweight design.

d. AI's Natural Tolerance + Hierarchical Fault Tolerance: LLMs are probabilistic models, and single-point SEUs are acceptable in most inference scenarios; HBM is equipped with ECC automatic error correction, and core control nodes deploy triple modular redundancy (TMR) majority voting to completely filter out single-point hard errors.

Google's paper, through 67MeV proton beam experiments simulating extreme LEO radiation, has shattered the traditional belief that 'space must use expensive dedicated chips':

HBM Memory (3x tolerance, imperceptible error correction): It absorbed 2 krad (nearly three times the expected dose for ultra-low-orbit satellites over five years) before individual errors occurred, all of which were automatically repaired by ECC with no business impact.

Core Computing Chips (20x tolerance, zero physical damage): They withstood 15 krad (20 times the expected dose) without any permanent damage, with AI training and inference tasks remaining stable throughout.

This test empirically proves that the technical route of 'advanced process (COTS chips) + software fault tolerance (ECC/watchdog reset)' can withstand extreme tests.

III. Latency: A Problem!

Internally, the space data center remains a standard 'NVIDIA machine room,' but its external interconnectivity becomes a vast wireless network woven from 'space lasers (inter-satellite high-speed)' and 'microwave/hybrid space-ground lasers (space-to-ground backhaul)':

a. Internal Interconnect (Within Satellite vs. Ground Cabinet): Identical

GPUs on the same motherboard still use NVLink/NVSwitch interconnects, and different computing nodes are still connected via traditional Ethernet or InfiniBand to form a local area network.

b. Node Interconnect (Between Satellites vs. Between Ground Data Centers): From 'Tangible' to 'Intangible'

On the ground: Data centers or cabinets must be connected by physical fiber optic cables buried underground or suspended in the air.

In space: Completely wireless. Different satellites use optical inter-satellite links (ISLs), which means ultra-high-speed data transmission is achieved with invisible laser beams.

c. Backbone Backhaul (Between Space and Earth vs. Ground Backbone Network): The Dilemma of Stability vs. Speed

This is the biggest difference between space and ground networks. Ground data centers directly access extremely stable and ultra-high-bandwidth ground fiber optic backbones; however, space computing power must transmit data to Earth users across the thick atmosphere, facing physical-level compromises:

Stability First (Ka-band Microwave): The current mainstream solution. Using electromagnetic waves to transmit data is slower (about 17Gbps) but 'rugged and reliable,' ignoring cloudy or rainy weather for 24/7 uninterrupted connectivity.

Speed First (Optical Laser Ground Links): A future upgrade solution. Bandwidth is hundreds of times higher, suitable for transmitting massive AI data; however, it is extremely 'delicate,' easily disrupted by cloudy or rainy weather, requiring the construction of a vast number of backup ground stations worldwide to 'rely on the weather.'

Currently, space data centers face several issues:

a. Data Latency: A low-Earth orbit (LEO) computing satellite orbits the Earth 15 times a day, spending only 5-7 minutes over a specific ground station each time. Connection quality is only good when the satellite is directly above the user's nearest ground station, but this situation lasts only 5-7 minutes per day.

Once it flies away, data must be relayed multiple times ('Chinese whispers') among multiple satellites, causing one-way latency to surge to 30-80 ms (ground fiber optics only take <1 ms).

b. Space-to-Ground Backhaul: The problem worsens when switching to optical ground links instead of RF links. Space-to-ground laser links are highly susceptible to interference from cloudy or rainy weather, leading to disconnections. Building ground stations globally is prohibitively expensive, and communication between dispersed ground stations and end-users becomes another source of increased latency.

For SpaceX, feasible solutions include:

b. Promoting 'Sensing-Computing Integration' Edge Computing: Allowing satellites to process images and then directly hand them over to nearby computing satellites, where AI interprets the results in orbit within 1 second, compressing a 10GB raw image into a few KB of conclusion 'text messages' (e.g., 'Abnormal target detected at longitude X latitude Y') for transmission back to Earth. This reduces downstream data volume by over 90%.

With significantly reduced data volume, even if lasers are obstructed, switching to weather-independent microwave backup links (Ka/V bands) can achieve all-weather second-level responses. However, this affects AI's multi-round, multi-modal interaction scenarios.

Communication latency stems from physical limitations of light speed and orbital mechanics and cannot be eliminated through technical means. Therefore, space data centers must abandon millisecond-level real-time scenarios (autonomous driving, high-frequency trading) and precisely position space computing power for high-latency-tolerant asynchronous computing: AI training (day/week cycles), meteorological and climate simulations (tolerant of a few seconds' delay), and on-site space computing (debris collision warnings, astrophysical modeling, etc.).

Operations and Maintenance: The inability to conveniently intervene manually in orbit is the core operational challenge for space data centers. At present, redundancy design (e.g., preset (yù shè, 'preset') 20% GPU overconfiguration to cope with irreparable permanent hardware failures and Reserve (yù liú, 'reserve') radiation-induced computing availability degradation—such as 95% computing availability) and software-level fault tolerance mechanisms (ECC error correction, watchdog resets, etc.) are used to replace on-site repairs, driving up overall deployment and operational costs.

Space robot maintenance is still in the experimental stage. It is expected that after 2032, as in-orbit robot technology matures, a certain degree of in-orbit repairs and component replacements will become possible, improving the lifespan of space data centers.

IV. Cost-Effectiveness: Is It Reliable?

The above analysis primarily focuses on technical feasibility. Now, let's examine economic viability. Compared to ground-based computing centers, space computing centers emphasize the seemingly inexhaustible energy supply.

However, this energy is not entirely free. Sunlight duration varies significantly across different orbits, directly affecting power supply capabilities and energy storage costs:

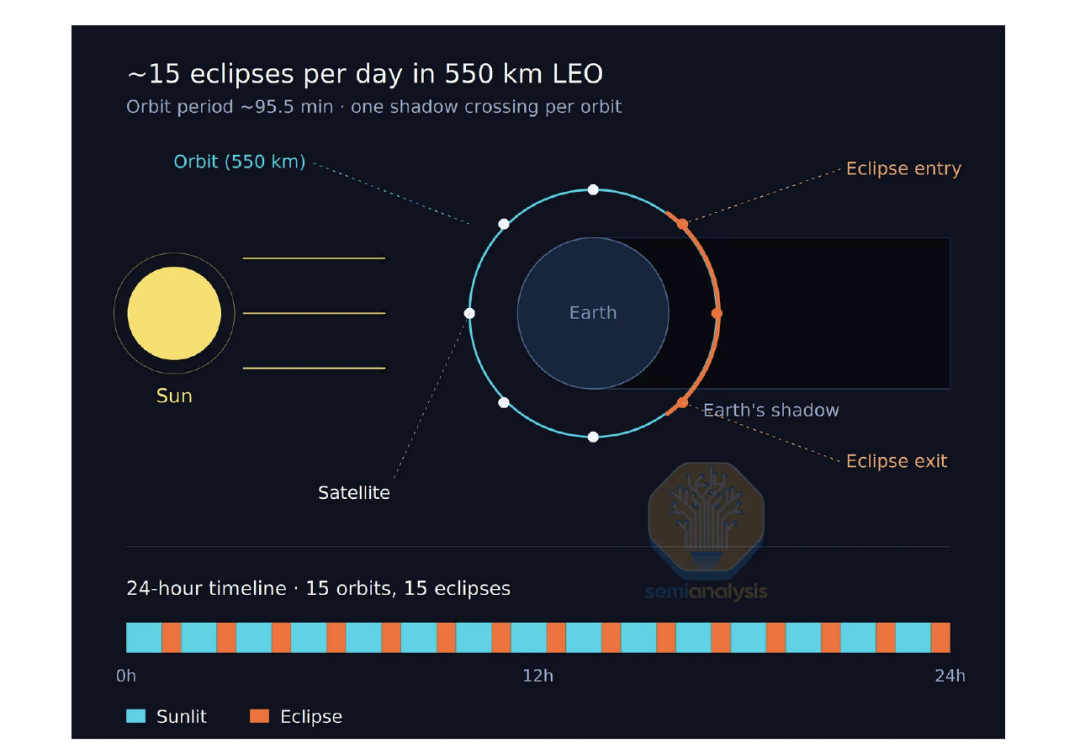

Low Earth Orbit (LEO): Orbiting the Earth about 15 times a day, LEO satellites receive sunlight only 60% of the time, resulting in low average effective solar irradiance levels. Frequent entry into the Earth's shadow zone requires large-capacity energy storage batteries, significantly increasing system complexity and hardware costs.

Sun-synchronous dawn-dusk orbit (SSO): The preferred orbit for space data centers. This orbit runs retrograde along Earth's terminator, maintaining continuous solar exposure for most of the year with a maximum daily shadow period of just 35 minutes. The required battery energy storage capacity is significantly lower than that of LEO. However, SSO represents a scarce orbital resource with available capacity far smaller than that of conventional low-Earth orbits.

The energy model for space data centers follows a CAPEX-substituting-OPEX pattern: there are no ongoing electricity bills, as all energy costs are capitalized in the upfront construction of solar arrays and energy storage systems.

The essence of space-based computing power lies not in simple arbitrage of 'scarce total electricity' but in using high fixed costs—launch, on-orbit system manufacturing, and reliability costs—to hedge against the multi-dimensional expansion bottlenecks faced by terrestrial data centers. These include not only direct electricity supply cost increases but also non-energy constraints such as grid interconnection queues, land and environmental permits, industrial material production capacity, and construction labor.

From a supply hierarchy perspective, terrestrial computing power faces four progressive layers of electricity supply buffering, each corresponding to different costs and expansion difficulties:

Space data centers only begin to demonstrate economic value when these four supply layers are progressively exhausted and the comprehensive costs of terrestrial computing power continue to rise. Prior to this point, significant untapped cost reduction potential remains on the ground.

To a certain extent, the core question of viability hinges on whether the electricity-related costs in operating terrestrial computing centers can outperform the additional (non-energy-related) costs required for space-based computing over the operational lifecycle.

Based on this framework, will space-based computing power remain a 'nice-to-have backup' or become an 'essential necessity'? Two distinct evolutionary paths are expected to emerge:

1) Stabilizing power supply-demand balance

Cost dynamics: From 'prohibitively expensive' to 'long-term parity'

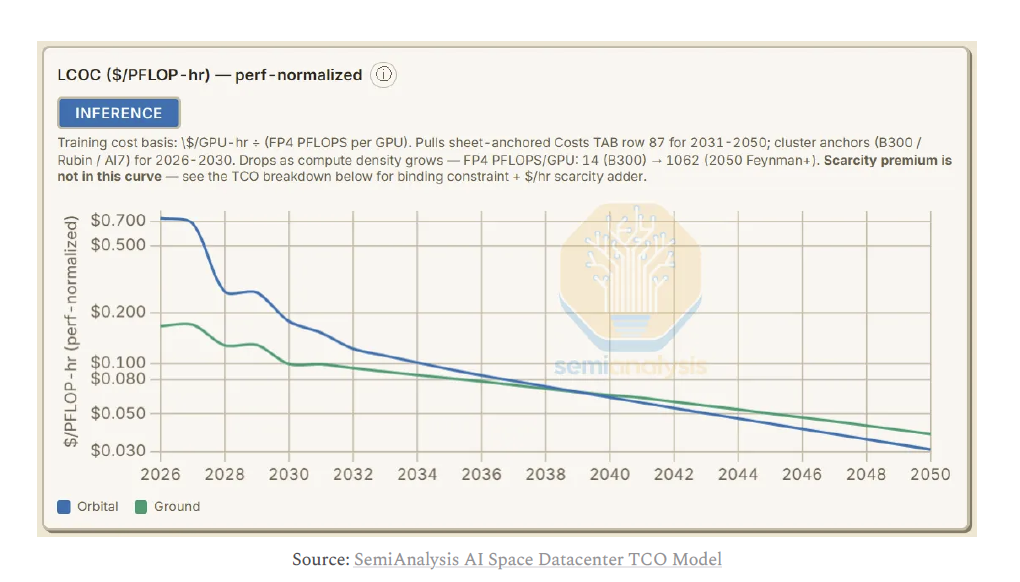

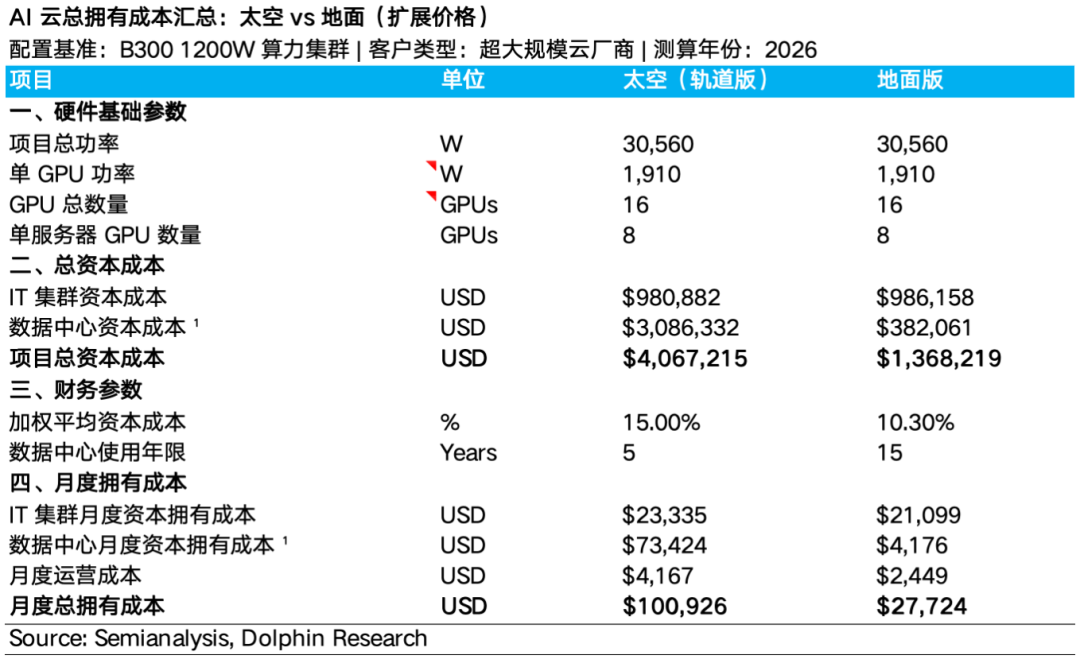

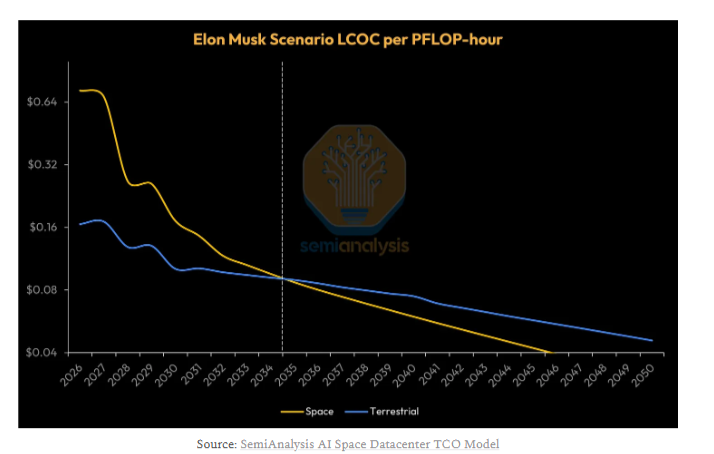

Initial disadvantage (2026): The total cost of ownership (TCO) for space data centers exceeds terrestrial counterparts by more than 4x. High costs stem from custom radiation-hardened/thermal control hardware, shortened chip lifespans due to radiation/thermal effects (5 years vs. 15 years), radiation-induced chip availability degradation (95%), and extremely high system redundancy costs due to non-repairability (requiring 20% GPU redundancy).

Long-term parity (2040): As engineering challenges in thermal management and space radiation are overcome, combined with Starship launch cost reductions, the levelized cost of computing (LCOC) for space and terrestrial systems will reach parity by ~2040 (in fact, by the early 2030s space costs will be only 30% higher than terrestrial, approaching scaling threshold).

b. Supply-demand evolution: Abundant terrestrial power makes space 'optional rather than essential'

Under baseline scenarios, terrestrial four-tier electricity supply releases steadily, with power capacity growing smoothly from 89 GW in 2026 to 338 GW in 2030.

2) Severe bottlenecks in terrestrial power expansion (electricity shortages)

a. Cost divergence: Parity arrives 6 years early

Surging terrestrial costs: Driven by grid approval delays and shortages in gas turbine/transformer production capacity, terrestrial data center CAPEX skyrockets from $34.6M/MW (baseline) to $53.4M/MW.

Plummeting space costs: Starship reduces launch costs to $80/kg with economies of scale, cutting space data center CAPEX to $11M/MW.

This 'scissor effect' brings space LCOC to parity with terrestrial systems by ~2034 (6 years ahead of baseline), after which space cost advantages continue widening—by 2039 space LCOC will be nearly 20% lower, establishing significant cost competitiveness.

b. Supply-demand evolution: Historical inflection point—computing explosion triggers 'space spillover effect'

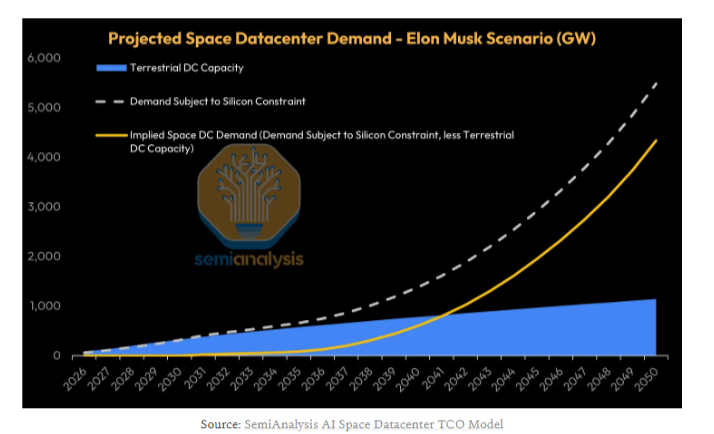

Chip capacity surges: Terafab adds ~1 million wafers/month capacity by 2040, significantly raising deployable computing power ceilings.

Terrestrial power capacity peaks in 2028 then stagnates, reaching only 576GW by 2035 (vs. 1,150GW in baseline) and ~2,400GW by 2050 (vs. ~7,500GW in baseline). Computing expansion constraints shift definitively from chip capacity to terrestrial power infrastructure.

Space spillover effect activates: Despite cost parity in 2034, true demand spillover occurs in 2037 when total chip capacity breaches terrestrial power ceilings, forcing massive computing deficits to migrate to space.

As demand sustained growth , space computing capacity expands rapidly: ~200GW in orbit by 2038, surging to ~4,800GW by 2050 (accounting for nearly 73% of annual chip capacity).

Space data centers then cease being supplementary options, becoming the core—and nearly exclusive—viable solution for large-scale AI computing deployment.

V. How to Value SpaceX's Colossus?

① Rocket launch business: In 'From Daydreams to Billions: Is SpaceX Really That Sci-Fi?', Dolphin Research argues rocket launch represents near-absolute monopoly, with some comparing it to the East India Company during the Age of Exploration.

For this unique monopoly asset, our valuation approach:

Assuming full utilization of 1 million tons annual payload capacity, commercialized at market parity of $200/kg, Starship's long-term annual revenue could reach $200 billion.

Profitability: After initial R&D/test flight investments, referencing Falcon 9's ~30% EBITDA margin at stable commercial operation, this business could generate ~$60 billion in annual EBITDA long-term. More detailed analysis is published in the Changqiao App [Dynamic-Depth] section under the same article title.

② Starlink business: In 'SpaceX: The Celestial Network Nears Invincibility?', we noted Starlink essentially leverages space transport monopoly to create a 'space-based telecom monopolist'.

The core challenge lies in spectrum 'spatial reuse'. While terrestrial operators can densify urban base stations for repeated spectrum use, a single satellite beam covers tens of thousands of square kilometers, forcing all users in that area to share limited bandwidth.

Thus, Starlink complements rather than replaces traditional terrestrial operators. Its core market will long remain suburban/remote areas and sea/air scenarios where terrestrial networks struggle or face prohibitive deployment costs, rather than penetrating dense urban centers.

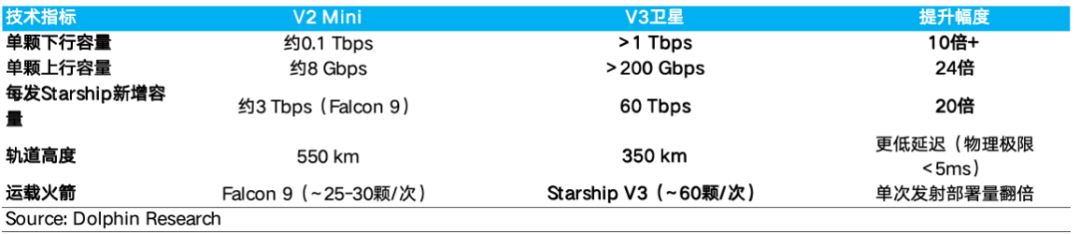

SpaceX plans to complete deployment of a 42,000-satellite mega-constellation by 2030 (currently ~9,600 in orbit), featuring systematic generational upgrades from V1/V2 to V3 and V-band satellites.

Among this 42,000-satellite target, next-gen V3 satellites represent the current strategic upgrade focus. Compared to incumbent V2 Mini, V3 satellites deliver comprehensive improvements in bandwidth, latency, and hardware architecture:

a. Broadband business: According to ARK Invest, global suburban/remote population totals 3.45 billion (800 million households). However, even a 42,000-V3-satellite constellation (1Tbps per satellite) faces physical capacity ceilings, capable of covering only 1.63 billion rural (380 million households) and 50 million urban (13 million households) populations at maximum.

We thus introduce an extreme assumption for Starlink's long-term expansion:

Assuming continuous capacity growth to eventually cover all 3.45 billion rural population globally, with continued 'localized pricing' (monthly broadband fees set at 2% of regional per capita GNI—industry affordability benchmark).

Under this ultimate scenario, Starlink's theoretical total addressable market (TAM) for global sink markets could surge to $249.6 billion annually (implying ~$26/month ASP per household).

However, during actual revenue conversion, factors including incomplete broadband demand in sink markets, ongoing terrestrial base station expansion into suburbs, and geopolitical barriers in markets like China/Russia prevent winner-takes-all outcomes.

Our revenue model thus assumes: Under neutral expectations, Starlink captures 30% of global rural market share ($74.9 billion revenue); under optimistic expectations, scale effects and first-mover advantages enable 50% market share ($124.8 billion revenue).

b. DTC business: For long-term valuation of direct-to-cell services, using SpaceX's disclosed 8 billion global mobile devices as baseline and referencing ~$8 global mobile ARPU, this market's long-term TAM reaches ~$740 billion.

However, constrained by satellite physical bandwidth limitations in dense urban areas, Starlink's DTC positioning isn't to replace traditional operators but to serve as a 'global coverage, blind spot elimination' value-added solution, forming B2B2C partnerships with global telecom giants.

Under the current 55:45 revenue-sharing model, Starlink cannot capture full mobile ARPU but instead earns 'wholesale-style' value-added shares (e.g., integrating as underlying network provider into T-Mobile USA's plans, with T-Mobile charging end-users and remitting proportional revenue to Starlink).

Leveraging its initial active device base and ongoing partnerships with leading global operators, we model penetration scenarios:

Neutral expectation: Assuming Starlink captures 10% of global mobile connections (~800 million devices) via value-added services and roaming partnerships, generating $40.7 billion in annual revenue at 55% revenue share.

Optimistic expectation: With deepening global demand for 'seamless connectivity', assuming 20% device penetration (~1.6 billion devices), DTC business could generate ~$81.4 billion in annual shared revenue, establishing itself as SpaceX's explosive second growth engine.

c. Aviation + maritime business

In high-value enterprise segments, aviation and maritime broadband represent Starlink's premium-priced, high-margin revenue streams:

Aviation market: With ~30,000 global commercial aircraft and extremely high ARPU (~$300,000 annualized), theoretical annual revenue reaches $9 billion.

Maritime market: With ~100,000 active merchant vessels and ~$34,000 annualized ARPU, theoretical annual revenue reaches $3.4 billion.

Combined, this niche segment's total addressable market (TAM) reaches $12.4 billion.

Leveraging LEO constellation advantages in 'low latency, high bandwidth, global seamless coverage', Starlink is rapidly dismantling traditional GEO satellite service barriers.

Assuming Starlink captures 80% of addressable aircraft/vessel market share long-term through hardware cost and experience advantages, this segment could stably contribute ~$10 billion in high-margin annual revenue.

Combining penetration projections across these three core businesses, we value Starlink's 2030 long-term valuation using EV/EBIT multiples and DCF methodology (discounted back to 2026 baseline). More detailed analysis is published in the Changqiao App [Dynamic-Depth] section under the same article title:

Neutral expectation: Starlink could achieve ~$128 billion in total revenue by 2030. Given satellite networks' extremely low marginal costs and scaling scale effects, we assume 45% operating profit margin (OPM), corresponding to $57.6 billion in EBIT.

Under optimistic expectations: With the global penetration rate climbing beyond expectations, Starlink's total revenue is projected to reach USD 218.6 billion by 2030. Under stronger economies of scale, assuming its OPM increases to 50%, the corresponding operating profit (EBIT) would reach as high as USD 109.3 billion.

③ AI Business: No Unique Value

In "SpaceX: AI's Relentless Cash Burn—Is 'Space Computing Hegemony' the Ultimate Game-Changer?", Dolphin Research noted that SpaceX's AI business consists of the X platform, the Grok model, Colossus ground computing power leasing, and space data center operations:

a. X Platform

Although the X platform is still undergoing restructuring, it is an undeniable fact that its advertising revenue has declined from a high of USD 2.3 billion in 2023 to USD 1.8 billion in 2025. The X platform is currently trapped in a dilemma akin to the "U.S. version of Weibo": While it remains a focal point for public opinion during major outbreak events (unexpected major events), its daily commercial traffic and user engagement are being systematically eroded by competitors, with its market share under continuous pressure.

b. Grok Model

Since SpaceX does not separately disclose revenue generated by the Grok model, Dolphin Research has conducted estimates based on publicly available data:

C-end Revenue Estimation:

1.9 million SuperGrok users: Based on a three-tier distribution (assuming Lite at $9/month accounts for 50%, Standard at $28/month accounts for 45%, and Heavy at $265/month accounts for 5%), the weighted monthly ARPU is approximately $30, resulting in an ARR of approximately USD 680 million.

4.4 million X Premium users: Their subscription fees are primarily for social features but also include access to Grok's functionalities. Assuming the incremental value of Grok's features is $8/month, the ARR is approximately USD 420 million.

Total C-end ARR is approximately USD 1.1 billion.

B-end Revenue Estimation:

Grok Business/Enterprise/API services are still in their infancy, and the model's capability gap limits its penetration in enterprise scenarios, resulting in minimal monetization volume. Assuming B-end revenue accounts for approximately 10%, the B-end ARR is about USD 100 million.

The current total ARR for the Grok model is approximately USD 1.2 billion.

c. Ground Computing Power Leasing Business:

Currently, SpaceX's computing power leasing adopts an ultra-large-scale single-tenant model focused on "a select few ultra-large clients." It has already signed contracts with three major clients, with these three contracts alone contributing an ARR of USD 27.8 billion to SpaceX's AI business.

As Dolphin Research has previously mentioned, SpaceX's computing power leasing is an extremely lucrative business—deploying computing power with a total investment lower than the industry average while leveraging the advantages of scarce assets and risk clauses to achieve pricing power 3-4 times higher than the industry average, locking in profit margins far exceeding those of peers.

However, the sustainability of these high profits faces constraints: (1) The 90-day termination clause means super contracts could disappear at any time; (2) After computing power supply and demand balance out around 2027/2028, pricing premiums will be compressed. Therefore, this represents more of a "very short-term windfall" during a scarce window of opportunity rather than a perpetual business that can be linearly extrapolated.

d. Space Data Center Business:

As mentioned earlier, SpaceX plans to achieve the ambitious goal of deploying 100 GW of computing power in orbit annually. Referencing the current pricing benchmark of approximately USD 10 billion/GW in the emerging cloud computing power leasing market, the total annualized revenue for this business under full-load operation would reach as high as USD 1 trillion.

Considering that this business, once matured, will possess monopoly and capital-intensive attributes similar to those of a "space utility," we assign it a steady-state net profit margin of 20% (corresponding to a net profit of USD 200 billion) and apply a relatively conservative 10x PE valuation multiple. Under this benchmark, the terminal market cap anchor for the space data center is USD 2 trillion.

However, due to differing macro constraints, the timing for this "USD 2 trillion terminal asset" to actually materialize and deliver profits varies significantly. Combining this with an industry-weighted average cost of capital (WACC) of approximately 10%, we discount it to the current point in 2026:

Neutral Expectations (Baseline Scenario Extension): Space Computing as an "Option"

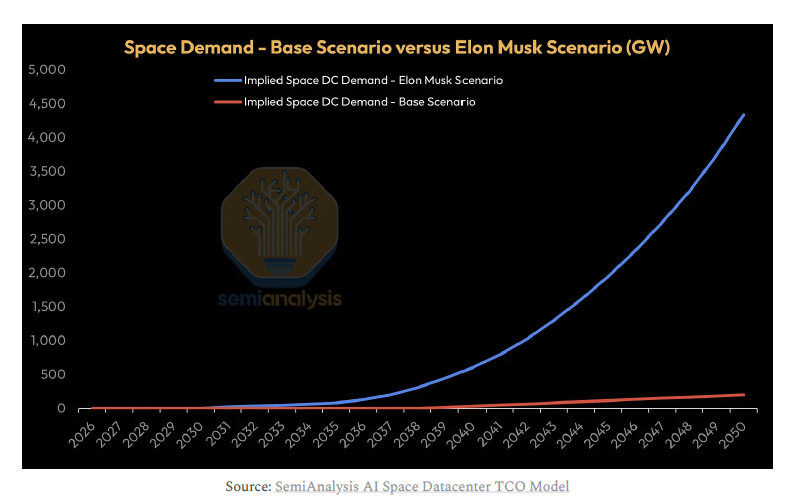

If ground-based power capacity expansion is sufficient to absorb chip production capacity, space data centers will lack short-term irreplaceable demand attributes and will serve more as a strategic reserve for ground computing power. In this scenario, we assume that the large-scale deployment node of 100 GW will be delayed to 2045.

Optimistic Expectations (Musk Scenario Realized): Space Computing as a "Necessity"

If ground-based power shortages intensify and wafer production capacity hits its ceiling, the "space spillover effect" will be forcibly activated. Space data centers will become the core foundation for accommodating the global AI computing power explosion.

In summary, the space data center is not only an engineering marvel but also a super bullish option catalyzed by "Earth's physical bottlenecks"—the lower the ceiling on the ground, the faster SpaceX will soar toward a trillion-dollar market cap.

- END -

// Reprint Authorization

This article is an original piece by Dolphin Research. Reprinting is prohibited without authorization.

// Disclaimer and General Disclosure

This report is intended solely for general comprehensive data purposes, designed for general reading and data reference by users of Dolphin Research and its affiliated institutions. It does not take into account the specific investment objectives, investment product preferences, risk tolerance, financial situation, or particular needs of any individual receiving this report. Investors must consult with independent professional advisors before making investment decisions based on this report. Any person making investment decisions using or referring to the content or information in this report does so at their own risk. Dolphin Research shall not be liable for any direct or indirect responsibilities or losses that may arise from the use of the data contained in this report. The information and data in this report are based on publicly available sources and are intended for reference purposes only. Dolphin Research strives to ensure but does not guarantee the reliability, accuracy, or completeness of the relevant information and data.

The information or viewpoints mentioned in this report shall not, under any jurisdiction, be construed or treated as an offer to sell securities or an invitation to buy or sell securities, nor shall they constitute advice, solicitations, or recommendations regarding relevant securities or related financial instruments. The information, tools, and data contained in this report are not intended for distribution to, nor are they intended to be used by, individuals or residents of jurisdictions where such distribution, publication, provision, or use would contravene applicable laws or regulations or would subject Dolphin Research and/or its subsidiaries or affiliated companies to any registration or licensing requirements in such jurisdictions.

This report merely reflects the personal viewpoints, insights, and analytical methods of the relevant contributors and does not represent the stance of Dolphin Research and/or its affiliated institutions.

This report is produced by Dolphin Research, and its copyright is solely owned by Dolphin Research. Without the prior written consent of Dolphin Research, no institution or individual may (i) reproduce, copy, duplicate, reprint, forward, or create any form of copies or replicas in any manner, and/or (ii) directly or indirectly redistribute or transfer them to any other unauthorized persons. Dolphin Research reserves all relevant rights.

-

![]()

Model Giant Jieyue Xingchen Steps into Smartphone Arena: A Strategic Alliance with Huaqin Technology

-

![]()

Big Model Firm Dives into Phone Market: StepFun and Wingtech Forge a ‘Dynamic Duo’

-

![]()

Zhongrun Optics Makes a Bold Move with 1 Billion Yuan Investment: Is a Turning Point on the Horizon for the Precision Optics Industry?

-

![]()

Deploy CLBO Crystals and YIG Single Crystals! Erythritol Leader Invests 30 Million in Youwei Optoelectronics

-

CXMT’s July 16 Subscription: Leading Domestic Memory Manufacturer—What’s the Earning Potential per Lot?

-

![]()

Rhythm Discrepancy and Premium Value Erosion: Foreign Luxury Brands Must Re-evaluate Their China Strategy

-

![]()

Half-Year, 1 Billion Yuan Financing, 7 Billion Yuan Valuation: A New Dark Horse Emerges in the Embodied AI Sector

-

![]()

Strong Rebound for Tech Stocks in Hong Kong Stock Market: Is It Time to Bottom-Fish?