Model Giant Jieyue Xingchen Steps into Smartphone Arena: A Strategic Alliance with Huaqin Technology

07/09 2026

07/09 2026

540

540

On July 9th, Jieyue Xingchen, a prominent model unicorn enterprise, teased the imminent launch of the world's pioneering AI agent smartphone. Simultaneously, Ni Fei, Senior Vice President of ZTE, revealed on Weibo that Nubia, a subsidiary of ZTE, would unveil this smartphone at the forthcoming 2026 World Artificial Intelligence Conference next week.

This news comes as no surprise. Over the past six months, from ByteDance's Doubao partnering with ZTE to introduce an AI smartphone, to reports of OpenAI advancing AI agent smartphone development with anticipated mass production in 2027, it has become evident that leading model companies are venturing into the hardware realm.

However, it's noteworthy that, according to Cailian Press, "Jieyue Xingchen is set to launch an AI agent smartphone, manufactured by A-share listed company Huaqin Technology, with a deep-rooted cooperation between the two, rather than a mere OEM arrangement."

In fact, as per Tianyancha data, Jieyue Xingchen's latest funding round, amounting to approximately $2.5 billion, saw participation from several hardware supply chain giants, including Huaqin Technology, Longcheer Technology, OmniVision Group, and ZTE.

The Jieyue smartphone, produced by Nubia and manufactured by one of its investors, Huaqin, represents a unique trinity of 'investor + contract manufacturer + brand,' a rarity in the industry's history. In this new paradigm, major model companies lead in defining products and experiences, contract manufacturing behemoths provide manufacturing prowess and capital support, while traditional brand manufacturers offer distribution channels and user recognition. Each entity plays a distinct yet interconnected role.

While Jieyue Xingchen's foray into smartphone manufacturing will undoubtedly draw significant attention, it also hints at a new industrial division of labor—where hardware-software collaboration in the AI era necessitates an organizational approach distinct from the mobile internet era.

I. Why Major Model Companies Seek 'Manufacturing Allies'

The primary motivation for major model companies to delve into hardware manufacturing is to discover practical application scenarios.

Over the past two years, firms like Jieyue Xingchen, Yuezhi'anmian, and Zhipu AI have primarily competed on parameters, benchmarks, and developer ecosystems. Despite rapid advancements in model capabilities, commercialization has consistently faced challenges—the API call business model struggles to foster user loyalty or generate revenues commensurate with R&D investments.

Jieyue estimated a revenue target of 1 billion yuan for 2025 around this time last year, a figure that pales in comparison to the R&D and computing costs incurred during the same period.

As model capabilities cease to be a unique differentiator—with gaps in language, multimodality, and reasoning visibly narrowing—the question arises: How can model capabilities become an integral part of users' daily interactions?

The answer lies in terminals. Smartphones, cars, glasses, earphones, robots—any device with a screen, microphone, or sensor can serve as an entry point for models to reach users.

Unlike the mobile internet era, where the application layer reaped the rewards, AI-era model companies risk being sidelined by hardware manufacturers and operating systems if they do not actively penetrate the terminal market. Apple's closed ecosystem, with in-house major model development, is a case in point, as is Huawei's rapid iteration of HarmonyOS AI capabilities. For major model companies, the window of opportunity is narrowing.

However, it is impractical for a major model company to establish its own smartphone production line. Smartphone manufacturing is a capital-intensive, low-margin, high-turnover business, requiring years of accumulation in supply chain management, quality control, and delivery cycles.

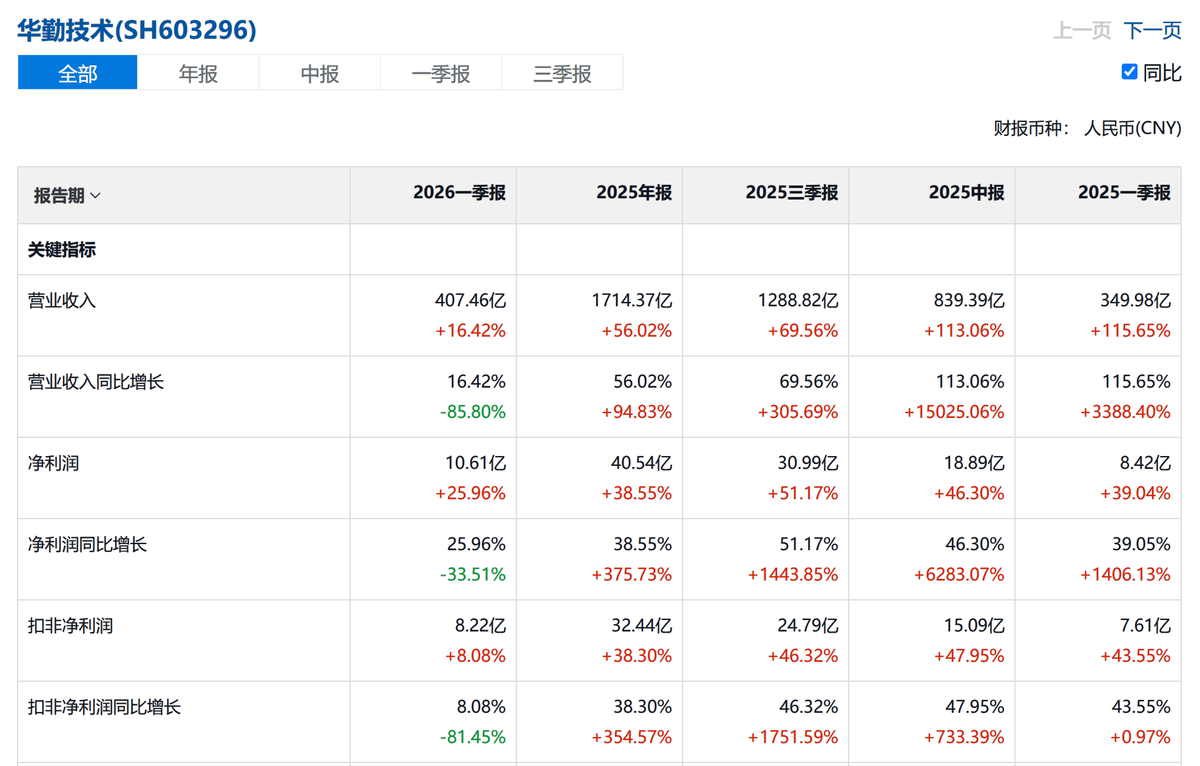

Even for Huaqin Technology, a giant with revenues exceeding 170 billion yuan in 2025, the overall gross margin is less than 8%, with even lower margins in the mobile terminal business. This business is fundamentally driven by scale, not technology. If a major model company were to dive in, it would not only strain its cash flow but also divert attention from model R&D.

This led to the cooperation model between Jieyue Xingchen and Huaqin Technology: Jieyue develops the AI brain, defining the interaction logic and user experience of the agent system; Huaqin handles manufacturing, providing full-chain contract manufacturing capabilities from design to delivery. The relationship between the two is not merely a principal-agent commission—Huaqin is itself an investor in Jieyue, aligning the interests of the manufacturing end and the model end through capital ties. This is a departure from traditional ODM models.

In the past, contract manufacturers and brands engaged in a delicate balance of power, with brands pressing for lower prices and contract manufacturers controlling costs. However, when a contract manufacturer holds equity in a model company, its focus shifts from maximizing contract manufacturing fees from a single order to ensuring the product's success, sustained shipment volumes, and driving subsequent collaborations on more products.

This is the most significant industrial signal behind the Jieyue smartphone: a deep binding beyond traditional supply chain relationships is forming between major model companies and manufacturing giants. Once this model proves viable, its scalable replication speed will far exceed in-house development.

II. The ODM Giant's Leap into the AI Era

From Huaqin Technology's perspective, betting on Jieyue Xingchen is not merely a financial investment decision.

Huaqin is the undisputed leader in China's consumer electronics ODM sector, ranking first globally in smartphone ODM shipments for five consecutive years, with a 22.5% market share in overall consumer electronics ODM in 2024. It also leads globally in ODM shares for tablets and smart wearables, with a client list that includes first-tier brands like Samsung, Xiaomi, OPPO, and Lenovo. In 2025, its annual revenue reached 171.4 billion yuan, up 56% year-on-year, with net profit attributable to shareholders of 4.05 billion yuan.

However, as mentioned earlier, the industry's overall gross margin is less than 8%, with mobile terminal business margins continuing to decline as smartphone contract manufacturing's proportion increases. Despite its scale, profitability relies on industry trends, with limited autonomy.

During the same period, although its AI server business grew rapidly, with annual revenue exceeding 40 billion yuan, core components like GPUs still needed to be procured externally, facing the same dilemma of 'high turnover, low margins.' Operating cash flow even turned negative in 2025. The company's asset-liability ratio reached 72.62% by the end of 2025, indicating the need for a business model breakthrough.

This is not unique to Huaqin but an inherent attribute of the entire ODM industry. With smartphones entering a mature market, replacement cycles lengthening, and hardware innovation margins diminishing, brand manufacturers' ability to press for lower prices has strengthened, while contract manufacturers' bargaining space has narrowed. To break free from the low-margin cycle of 'earning a few yuan per smartphone,' Huaqin needs to find new value growth points.

AI provides this opportunity. If major models can truly integrate into smartphones, PCs, cars, and IoT devices, the value of terminal products will shift from standardized hardware to personalized, continuously evolving intelligent services. For contract manufacturers, this means upgrading from 'helping brands build devices' to 'helping brands build intelligent devices.' The former's value-add lies in manufacturing capabilities and supply chain efficiency; the latter's lies in hardware-software collaboration and AI capability integration.

Huaqin's investment in Jieyue is essentially a preemptive move for this transformation. It is not simply aiming to sell more AI smartphones but attempting to redefine its industrial role—from a pure hardware contract manufacturer to an infrastructure provider for AI terminal ecosystems. If this role is established, its profit structure has the opportunity to extend upstream from contract manufacturing fees.

From this perspective, Huaqin's布局 (layout) in the AI industry chain is not scattered financial investments but a systematic strategy.

Investing in Jieyue Xingchen secures access to major model capabilities. Investing in OmniVision Semiconductor, GigaDevice, and Montage Technology secures core components like image sensors, memory chips, and memory interfaces. Investing in Victory Giant Technology secures AI server PCBs. It has even ventured into humanoid robots and embodied intelligence.

The logic behind this portfolio is that when the AI terminal wave arrives, Huaqin will not just be a contract manufacturing executor but a key node deeply embedded in every link of the industry chain.

III. A New Industrial Division of Labor Paradigm Emerges

From a broader industrial perspective, the emergence of the Jieyue smartphone may mark the beginning of an era where AI terminals are entering manufacturing implementation, albeit with differences from previous contract manufacturing models.

The division of labor in the mobile internet era's smartphone industry was clear: chip manufacturers provided underlying computing power, operating system vendors provided software platforms, brand manufacturers defined products and integrated supply chains, and ODM contract manufacturers handled manufacturing. Brand owners were the hub of the entire value chain.

However, in the AI terminal era, the hub may shift. Major models define the core experience of agent systems—what users perceive is not 'how fast the Snapdragon chip runs' but 'whether this AI can understand me, remember my habits, arrange my schedule, and operate apps for me.' This capability is not determined by brand owners but by major model companies.

When major model companies become the definers of experience, the brand owners' core position in the value chain is shaken. Brand owners remain important—channels, user recognition, after-sales service, and quality endorsement are capabilities major model companies cannot quickly replicate. However, brand owners are no longer the sole dominators. A new industrial division of labor has emerged:

Major model companies output intelligent capabilities, brand manufacturers provide market entry points and user trust, and ODM contract manufacturers offer manufacturing and supply chains. Each party has an irreplaceable role, but who occupies the hub position in the value chain depends on who can grasp the core decision-making factors for users.

Jieyue Xingchen's approach takes this new division of labor further. It is not just pre-installing an AI assistant on Nubia smartphones but creating a standalone AI terminal brand, treating the smartphone as a physical shell for the agent system.

Who manufactures the phone itself or what chips it uses may matter less to users; what matters is whose agent is inside and what it can do. If this logic holds, major model companies will wield far greater influence in the industry chain than any App developer today, potentially redefining the power boundaries between hardware and software vendors.

Of course, from an industrial history perspective, whether this model can scale successfully remains to be seen over time. The existence of Huawei's HarmonyOS AI and Apple's closed ecosystem means major model companies will never secure the top brand entry points. Current agent smartphones are more of an attempt to open these entry points. If, in this experimental field, AI smartphones can deliver differentiated experiences, then the model of 'major models defining experiences, ODMs handling manufacturing, and brands providing channels' could expand across the industry.

Ultimately, this topic returns to the industry: In the agent era, can major model companies, contract manufacturers, and brand owners find a more efficient cooperation model than traditional supply chain relationships? If the answer is yes, then today's Jieyue and Huaqin may just be the first dominoes in a larger-scale restructuring.

Source: Songguo Finance

-

![]()

Model Giant Jieyue Xingchen Steps into Smartphone Arena: A Strategic Alliance with Huaqin Technology

-

![]()

Big Model Firm Dives into Phone Market: StepFun and Wingtech Forge a ‘Dynamic Duo’

-

![]()

Zhongrun Optics Makes a Bold Move with 1 Billion Yuan Investment: Is a Turning Point on the Horizon for the Precision Optics Industry?

-

![]()

Deploy CLBO Crystals and YIG Single Crystals! Erythritol Leader Invests 30 Million in Youwei Optoelectronics

-

CXMT’s July 16 Subscription: Leading Domestic Memory Manufacturer—What’s the Earning Potential per Lot?

-

![]()

Rhythm Discrepancy and Premium Value Erosion: Foreign Luxury Brands Must Re-evaluate Their China Strategy

-

![]()

Half-Year, 1 Billion Yuan Financing, 7 Billion Yuan Valuation: A New Dark Horse Emerges in the Embodied AI Sector

-

![]()

Strong Rebound for Tech Stocks in Hong Kong Stock Market: Is It Time to Bottom-Fish?