Has Baidu Finally Made the Right Bet in the AI Era?

07/09 2026

07/09 2026

333

333

Source | Bohu Finance (bohuFN)

Author | Kaikai

The side business Baidu launched to 'save money' is now reaping rewards—Kunlunxin is going public.

According to foreign media The Information, Baidu's AI chip subsidiary, Kunlunxin, plans to list in Hong Kong with a target valuation of approximately $50 billion (around RMB 340 billion).

Notably, when Kunlunxin completed its Series D funding in July 2025, its post-money valuation was only about RMB 21 billion (approximately $3 billion). In less than a year, Kunlunxin's valuation has surged nearly 16-fold.

As of June 30, Baidu's total market capitalization in Hong Kong was approximately HK$298.3 billion (around $38 billion), meaning Kunlunxin's target valuation now exceeds that of its parent company, Baidu—a case of the 'child surpassing the parent.'

Such a valuation is not surprising. Across the entire AI industry chain, soaring stock prices have become the norm: Cambricon, the leader in computing chips, has surpassed a trillion in market cap, while InnoLight, the leader in optical modules, has reached 1.5 trillion...

Kunlunxin's listing is almost a foregone conclusion.

The real test lies in whether Kunlunxin can translate the capital market's fervent expectations into sustained commercial viability after achieving a higher valuation than its parent company.

Can Baidu once again seize a 'moment in the spotlight?'

01 To Invest, You Must 'Bundle Orders'

In January of this year, Baidu announced that Kunlunxin had submitted its listing application to the Hong Kong Stock Exchange through its joint sponsors; in May, the China Securities Regulatory Commission disclosed that Kunlunxin had completed its Sci-Tech innovation board (Science and Technology Innovation Board) listing Tutoring registration (coaching and filing).

Kunlunxin's IPO is poised for launch, but securing a spot on this ride is no easy feat.

According to foreign media reports, Kunlunxin has set a rare subscription condition for some potential investors—to participate in the investment, they must first purchase chips equivalent to 3-7 times the subscription amount.

Kunlunxin isn't just seeking capital; it's also demanding orders. This is the true essence of this IPO. To understand the market dynamics behind this rule, we must revisit 2011.

That year, Baidu established an in-house AI accelerated computing team to explore the possibility of developing its own chips. Li Yanhong has mentioned on multiple occasions the original intent behind building chips: 'Buying others' chips is simply too expensive.'

Li Yanhong recognized earlier than most that in the digital age, computing power is productivity. He once publicly calculated, 'Buying others' chips costs $10,000 per chip, while we can make them for RMB 20,000.'

In the AI era, computing power has indeed become the lifeblood of all major companies, with chips holding the throat of this lifeblood.

Thus, Baidu gained a time window at least five years ahead of its domestic peers. While most internet companies were still spinning stories and scaling up, Baidu had already embarked on the path of chip development.

In 2018, Baidu unveiled its first-generation self-developed AI chip, 'Kunlun'; by 2020, the first-generation series began mass deployment in Baidu's businesses; in 2021, Kunlunxin officially spun off from Baidu.

Baidu chose a more difficult path but happened to bet correctly on the shift in growth logic within the internet industry—from 'narratives of traffic' to 'narratives of hard technology.'

In the past, the internet industry relied on user scale, market share, and growth prospects to support valuations. The bigger the story, the higher the market pricing, with everyone betting that scale would eventually become a moat.

But in the AI era, industry logic has been Thoroughly Refactoring (completely restructured). It's no longer about scale reducing marginal costs; instead, every additional DAU incurs another computing power bill, with scale increasing costs.

Against this backdrop, internet giants can no longer just talk about long-term investments; they must also discuss capital returns. Thus, hard tech assets previously hidden within these giants, like AI chips, are being revalued by the market.

They are no longer just money-burning, non-revenue-generating departments within giants but can independently enter the market with a complete business model.

According to IDC data, by 2025, domestic vendors' combined shipments in China's AI accelerator card market will reach approximately 1.65 million units, with Huawei Ascend shipping about 812,000 units, Alibaba T-Head about 265,000 units, and both Kunlunxin and Cambricon shipping about 116,000 units each, ranking third domestically.

This explains why Kunlunxin's equity requires 'bundling orders.' Kunlunxin isn't short on capital but needs proof of its transformation from a 'Baidu in-house chip department' to an 'independent AI chip supplier.'

It hopes to preemptively integrate Kunlunxin into clients' business ecosystems, bind their continued procurement intention (willingness), and form a 'bidirectional mutual benefit' strategic alliance while other giants accelerate their self-developed chip efforts.

Ultimately, capital is just the entry ticket; the industry is the real leverage.

02 'Selling Shovels' Is More Valuable

With Kunlunxin as a new asset, the market is reevaluating Baidu, the internet veteran.

In the past, discussing internet giants' AI strategies meant annual investments of tens or even hundreds of billions, yet without immediate tangible returns, making it difficult for the market to maintain optimistic performance expectations.

But now, Kunlunxin has the opportunity to turn 'investments' into 'outputs': with products, clients, and a new narrative binding large models and cloud businesses, Baidu has a new valuation logic.

Moreover, Kunlunxin holds a unique position in the domestic AI chip breakthrough battle.

First, Kunlunxin was born within Baidu's vast ecosystem. Since Baidu began developing its own AI chips, they have undergone over a decade of Practical polishing (real-world refinement) in Baidu's data centers, autonomous driving systems, and other massive real-world scenarios.

Second, Kunlunxin's greatest feature is Baidu's self-developed XPU architecture, designed specifically for AI and deeply optimized for large model training and inference, rather than pursuing all-around capabilities like graphics rendering.

Other vendors follow different technical routes: Moore Threads is a general-purpose GPU vendor; Biren and MetaX are AI-accelerated GPGPU vendors with stronger versatility, capable of both graphics rendering and AI training/inference.

Cambricon uses a self-developed NPU architecture and is China's largest third-party independent AI chip supplier; Huawei Ascend is a full-stack autonomous player pursuing complete controllability from chips to software to hardware.

As model deployment scales expand, inference computing power demand will continue to surge, and Kunlunxin's XPU architecture can run more inferences at lower costs, which is the underlying logic of its breakthrough in the domestic chip fray.

Currently, Kunlunxin's main product is the P800, which has secured orders from clients like State Grid, China Steel Research, China Merchants Bank, and China Mobile. According to foreign media The Information, Tencent has also become an important client of Kunlunxin.

Of course, manufacturing chips is just the first hurdle; whether Kunlunxin can secure more clients will determine if it can truly step out of Baidu's shadow and become an AI chip company with separately calculable revenue, profits, and market share.

Reuters revealed that Kunlunxin's 2024 revenue was approximately RMB 2 billion, with 2025 projections exceeding RMB 3.5 billion, and external sales expected to surpass half of total revenue. JPMorgan estimates that its 2026 revenue could further rise to RMB 8.3 billion.

Kunlunxin has achieved impressive results, and the fact that even competitors are willing to pay for its products is a stronger endorsement than any prospectus.

However, Kunlunxin's greatest value lies not just in being a 'rare' chip company but in providing Baidu with a new valuation anchor, telling a more imaginative story than traditional search—'selling shovels' in the AI era.

Chips are the root, models the trunk, and cloud the branches. Baidu's 'chip foundation' must be stable to better support its large models and intelligent cloud businesses. The true value of chips must be viewed within Baidu's full-stack AI layout of 'chips-models-cloud services.'

This is also Li Yanhong's proposed 'inverted pyramid' theory: No matter how much chip vendors earn, models built atop chips must generate 10x the value, and applications developed based on those models must create 100x the value to form a healthy industrial ecosystem.

Over the past few quarters, Baidu's AI business revenue share has continuously risen, from 39% in Q3 2025 to 43% in Q4, and reaching 52% in Q1 2026. Li Yanhong stated that AI has become Baidu's core driver.

The business logic is sound, but Kunlunxin still faces several mountains to climb.

First is independence.

Born within Baidu, Kunlunxin has technical accumulation, in-house orders, and ready application scenarios—its greatest advantages. However, this also means Kunlunxin is hard to completely detach from Baidu.

Although Kunlunxin has operated independently for years, Baidu remains the controlling shareholder with about a 57.67% stake and is one of its primary clients. This 'backed-by-a-giant' relationship places Kunlunxin in a delicate position with government and enterprise clients.

Government and enterprise clients often emphasize 'autonomy and controllability,' preferring not to bind their computing infrastructure to a single internet giant's ecosystem. Independent third-party suppliers like Cambricon and Moore Threads are more likely to secure entry tickets.

Whether the market truly accepts Kunlunxin as an independent third-party supplier will determine its future ceiling. According to multiple media reports, Kunlunxin is negotiating cooperation with SMIC, intending to shift some production back to domestic facilities—a crucial step.

Second is technological iteration.

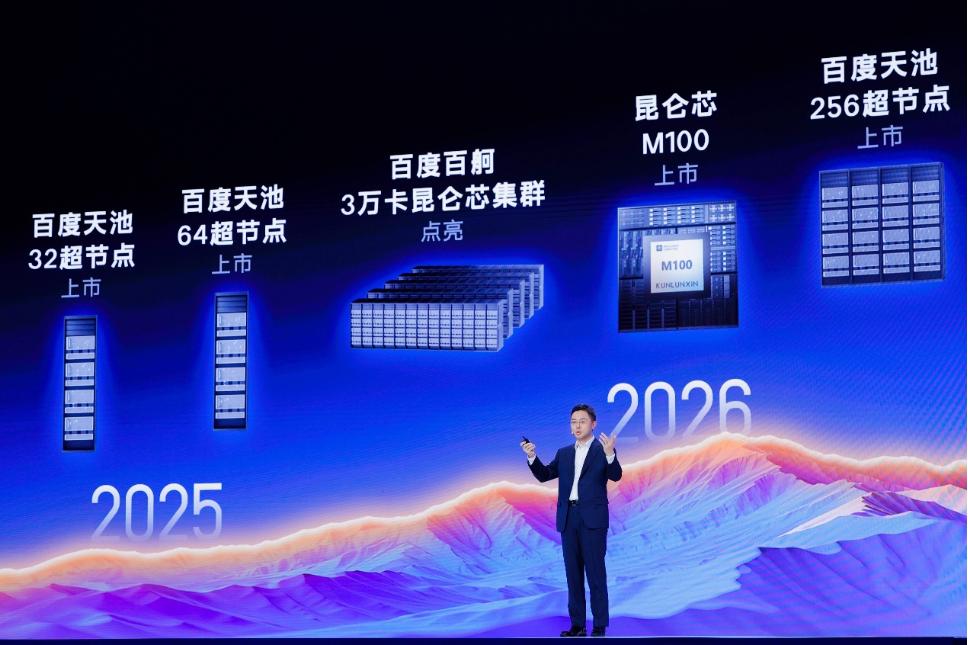

Currently, Kunlunxin's P800 chip has completed large-scale validation, and the fourth-generation P900 has completed design and tape-out, with performance reportedly double that of the P800.

However, the real challenge lies in large-scale training scenarios, the hard nut to crack for domestic substitution.

Reportedly, Kunlunxin's M100, optimized for large-scale inference scenarios, launched in early 2026; the M300, targeting ultra-large-scale multimodal models, is planned for 2027.

However, with advanced node capacity constraints, whether Kunlunxin can secure sufficient tape-out shares domestically will determine if the M100 can ramp up production quickly and if capacity can keep pace with order growth remains a major question mark.

Finally is the software ecosystem.

Ecosystem influence is key to determining chip value, and Kunlunxin is well aware of this.

Currently, Huawei has built an ecosystem-level platform with vertical integration from chips to applications, hardware, and software; Cambricon also offers 'cloud-edge-end integrated' cross-platform development tools, with more mature toolchains reducing cross-platform migration costs and making clients less likely to churn.

While Kunlunxin is striving to catch up, it still has a long way to go in terms of developer community and toolchain completeness—the truly challenging part.

For Kunlunxin, the IPO is a phased victory and an important starting point.

As Li Yanhong said, 'Seize the AI opportunity, and in five to ten years, Baidu will become a completely different company.'

But let's not forget that the latter half of a marathon is often where endurance is truly tested.

The cover image and illustrations belong to their respective copyright owners. If the copyright holders deem their works unsuitable for public browsing or gratuitous use, please contact us promptly, and our platform will immediately make corrections.

-

![]()

Model Giant Jieyue Xingchen Steps into Smartphone Arena: A Strategic Alliance with Huaqin Technology

-

![]()

Big Model Firm Dives into Phone Market: StepFun and Wingtech Forge a ‘Dynamic Duo’

-

![]()

Zhongrun Optics Makes a Bold Move with 1 Billion Yuan Investment: Is a Turning Point on the Horizon for the Precision Optics Industry?

-

![]()

Deploy CLBO Crystals and YIG Single Crystals! Erythritol Leader Invests 30 Million in Youwei Optoelectronics

-

CXMT’s July 16 Subscription: Leading Domestic Memory Manufacturer—What’s the Earning Potential per Lot?

-

![]()

Rhythm Discrepancy and Premium Value Erosion: Foreign Luxury Brands Must Re-evaluate Their China Strategy

-

![]()

Half-Year, 1 Billion Yuan Financing, 7 Billion Yuan Valuation: A New Dark Horse Emerges in the Embodied AI Sector

-

![]()

Strong Rebound for Tech Stocks in Hong Kong Stock Market: Is It Time to Bottom-Fish?