Explosion of AI Upstream Materials

07/09 2026

07/09 2026

330

330

The A-share market's top performer in terms of year-to-date gains may surprise many.

It is not the most eye-catching 'light' or 'chip' in the AI supply chain but an electronic fabric company at the forefront of AI's upstream—soaring over 28-fold since the beginning of the year.

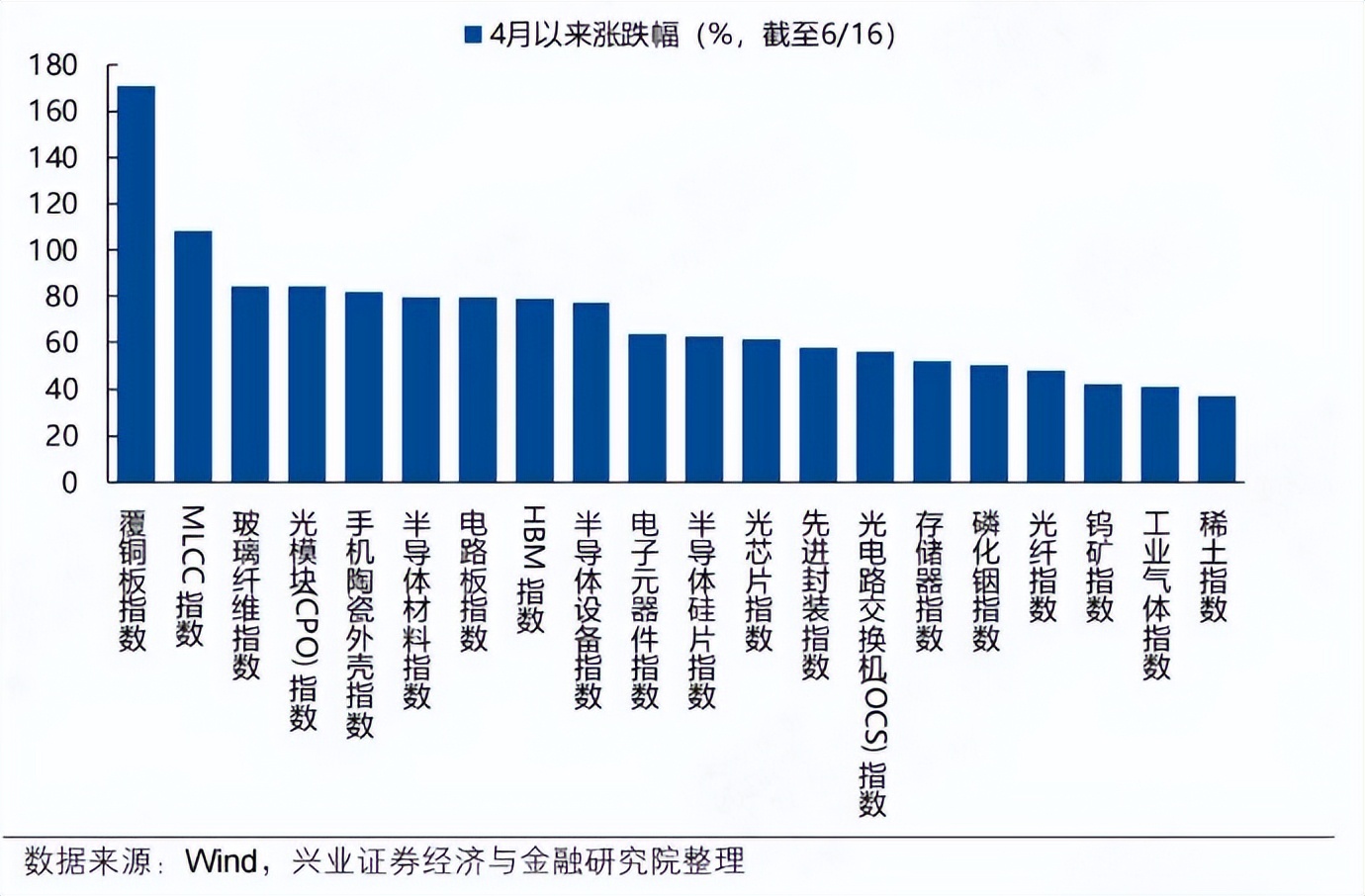

The explosive growth of AI upstream companies is not an isolated case. Since April, the three sub-sectors with the highest gains in the AI supply chain have been copper-clad laminates, MLCCs, and fiberglass. These more fundamental upstream material sectors have outperformed the previously hot hard tech sectors.

The shift in the top gainer is partly due to sector valuation differences. However, the core rationale is that AI investment is transitioning from 'superficial narratives' to the 'upstream bottleneck pricing' phase. Upstream material companies, with their high demand certainty and strong supply constraints, can deterministically convert orders into profits through substantial price hikes.

The driving force behind this AI upstream explosion is a series of price increase notices: for instance, electronic fabric has undergone five rounds of price hikes this year, with the average price of mainstream specifications doubling from last year's low.

The rationale behind the price hikes of upstream materials is the continuously widening supply-demand gap.

From 2026 to 2027, the annual supply-demand gap for high-grade HVLP copper foil will expand from 1,500 tons to 2,500 tons; meanwhile, the supply gap for electronic fabric looms will reach 6.1% and 10.6% in 2026 and 2027, respectively.

The root cause of the supply-demand imbalance, besides the rigid demand surge from AI servers, lies in the 'generational production contraction curse' on the supply side: AI significantly raises the physical thresholds for materials, and with each upgrade in high-end materials, effective capacity plummets during the transition between old and new generations due to processing difficulties and yield rates.

Demand is expanding, while effective supply is shrinking. This presents a highly deterministic opportunity in the supply chain, although current A-share valuations have already factored in excessive expectations.

In the past few years, AI investment has focused on the most visible links such as large models, GPUs, and optical modules. Standing in the light and close to the chips was considered the ultimate wealth code.

However, in recent months, if you are still 'chasing the light and chips' in the A-share market, while you can still achieve significant excess returns, you are likely missing out on the most substantial rewards of AI investment.

Since the beginning of the year, the highest gainer in the A-share market has been an electronic fabric company, surging 28-fold. Electronic fabric, a core insulating and stabilizing material for PCBs and IC substrates in the AI upstream, acts as the backbone of PCBs, directly affecting signal transmission speed and stability.

The explosion of AI upstream materials like electronic fabric is not an isolated case. Since April, the three sectors with the highest gains in the AI supply chain—copper-clad laminates, MLCCs, and fiberglass—are all upstream areas, outperforming previously highly regarded core hardware such as optical modules and HBM.

While this change is influenced by sector valuation differences, the core factor is the shift in AI pricing logic. Sectors with high demand certainty and strong supply constraints are beginning to enjoy a 'premium.' Upstream material companies, with their high demand certainty and strong supply constraints, can deterministically achieve price hikes and convert orders into higher profits.

This is already reflected in the performance of upstream material companies. Taking the most followed (attention-grabbing) upstream material companies this year, such as HVLP copper foil, electronic fabric, and resin, as examples, in the first quarter of this year, Tongguan Copper Foil's net profit surged over 20-fold, while electronic fabric leader Honghe Technology's net profit increased by 354% year-on-year, and resin leader Dongcai Technology's net profit grew by 103.3% year-on-year.

This profit growth is likely to continue, as evidenced by the recent wave of price hikes in the upstream material industry.

Electronic fabric has seen a flurry of price increase notices, with at least five rounds of price hikes completed this year, and the average price of mainstream fabrics doubling from last year's low.

Tongguan Copper Foil raised processing fees for all copper foil categories by RMB 2,000 per ton in June, marking the second price adjustment in the second quarter; the unit price of HVLP4 copper foil increased from RMB 180,000 per ton to RMB 200,000 per ton, an 11% increase in a single round.

Electronic PPE resin saw the most dramatic price increase, soaring over fourfold due to not only demand growth but also the impact of a shutdown at a core production line in the Middle East.

How did this widespread and intense price surge come about?

Price increases for most products stem from a simple mismatch between supply and demand, and many AI upstream materials are experiencing a widening supply-demand gap.

From 2026 to 2027, the annual supply-demand gap for HVLP copper foil will expand from 1,500 tons to 2,500 tons. The supply gap for electronic fabric looms will reach 6.1% and 10.6% in 2026 and 2027, respectively.

The reason for the widening supply-demand gap is that while demand is expanding, effective supply is contracting.

First, let's look at the demand side. The architectural upgrades of AI servers have created an extremely steep consumption curve for materials.

According to Morgan Stanley's research, H100 servers shipped in 2022 generally had 16 to 20 layers of PCBs. However, the new generation Rubin (VR200) architecture, set for mass production in the second half of 2026, will directly jump to 32 to 40 layers or more of PCBs.

As the underlying raw material for PCBs, the consumption of electronic fabric, copper foil, and resin multiplies with the increase in layers. For example, a high-end AI server consumes 4 to 5 times the area of electronic fabric compared to an ordinary server.

More critically, AI not only brings about a breakthrough in quantity but also a generational leap in material properties—requiring materials to evolve from 'consumer-grade' to 'semiconductor-grade.'

Take copper foil as an example. In high-speed transmission scenarios, current generates a 'skin effect' (electrical signals concentrate on the conductor's surface). The rougher the copper foil surface, the worse the signal integrity. Materials that could suffice in ordinary servers begin to fail physically when faced with new-generation AI motherboards and 224G/1.6T high-speed switch boards.

This forces the AI supply chain to upgrade to extreme materials like HVLP-4 (ultra-low profile copper foil). Under high standards, the processing fee for HVLP-4 copper foil exceeds RMB 20,000 per ton, more than ten times that of traditional HTE copper foil.

However, the physical upgrades on the material side have triggered a 'generational production contraction curse' on the supply side.

Due to changes in physical properties such as hardness and brittleness, the processing difficulty and yield rates of new materials significantly deteriorate, leading to a cliff-like drop in ultimate capacity.

For example, the line speed of machines producing conventional copper foil can reach 12-15 meters per minute. When switched to AI-grade HVLP copper foil, to ensure uniformity and extremely low roughness of the physical microstructure, the line speed is forced down to 6-8 meters per minute. Additionally, HVLP copper foil uses more complex special composite additives, further reducing the yield rate to around 60%, far below the over 95% yield rate of traditional copper foil. Combined, the capacity of HTE copper foil is reduced by 40%-60% compared to traditional copper foil.

The demand pool is growing larger, while the supply pipe is narrowing, forming the underlying rationale for why AI upstream materials are favored by capital.

Against the backdrop of a widening supply-demand gap, the window for domestic substitution is also opening.

Previously, many AI upstream materials were bottlenecked by Japanese companies, which had accumulated deep expertise in product generations, process stability, and customer systems, leading the global market share.

For example, high-end HVLP copper foil is mainly dominated by Japanese manufacturers such as Mitsui Metals, Furukawa Electric, and Fukuda Metal. In the high-end T-type and NE-type electronic fabric market for integrated circuit substrates and advanced packaging, Nitto Boseki once held a nearly 90% global market share.

However, this landscape is now changing.

Besides 'generational production contraction' limiting the release of overseas high-end capacity, Japanese companies' characteristic cautious decision-making culture, complex compliance processes, and Japan's domestic labor bottlenecks have extended their critical material expansion cycles to generally 36 to 48 months.

The 'distant water cannot quench the immediate thirst' of overseas giants' expansion, forcing downstream CCL (copper-clad laminate) and PCB giants to more actively onboard domestic companies to ensure supply.

This is evident in the electronic fabric sector. Domestic high-end electronic fabric leaders have already passed certifications from Taiwanese, Japanese, and top domestic CCL giants. In the low-thermal-expansion-coefficient fabric (a core indicator for high-end AI substrates) sector, this company's first-quarter revenue Month-on-month growth a staggering 190.8%, the fastest growth rate globally. In the copper foil sector, some companies have also passed downstream customer verifications and are gradually achieving bulk shipments.

In the long run, the growth opportunities for domestic companies are relatively certain. AI servers are transforming the cyclical upstream materials into a more high-growth, high-profit-margin pro-cyclical sector. Under the supply-demand gap, domestic companies are seizing supply chain opportunities and gradually reflecting them in their performance.

Although the rationale is solid, it must be noted that the gains of related domestic companies have already been fully priced in, with some even reaching 900 times P/E.

Such valuations have already factored in the high growth prospects for the next few years. Once the supply chain development or performance fails to meet high expectations, the intensity of the valuation correction may not be milder than the rally.

-

![]()

Model Giant Jieyue Xingchen Steps into Smartphone Arena: A Strategic Alliance with Huaqin Technology

-

![]()

Big Model Firm Dives into Phone Market: StepFun and Wingtech Forge a ‘Dynamic Duo’

-

![]()

Zhongrun Optics Makes a Bold Move with 1 Billion Yuan Investment: Is a Turning Point on the Horizon for the Precision Optics Industry?

-

![]()

Deploy CLBO Crystals and YIG Single Crystals! Erythritol Leader Invests 30 Million in Youwei Optoelectronics

-

CXMT’s July 16 Subscription: Leading Domestic Memory Manufacturer—What’s the Earning Potential per Lot?

-

![]()

Rhythm Discrepancy and Premium Value Erosion: Foreign Luxury Brands Must Re-evaluate Their China Strategy

-

![]()

Half-Year, 1 Billion Yuan Financing, 7 Billion Yuan Valuation: A New Dark Horse Emerges in the Embodied AI Sector

-

![]()

Strong Rebound for Tech Stocks in Hong Kong Stock Market: Is It Time to Bottom-Fish?