2026 618 Refrigerator and Washing Machine Market Review: Freezers Lead with Strong Growth, Refrigerators Face Slight Pressure, Washing Machines Demonstrate Strongest Resilience

06/24 2026

06/24 2026

403

403

The 2026 618 promotion period was further extended and brought forward. Platforms initiated multi-phase marketing campaigns starting in May, coupled with industry anti-price-war policy guidance, resulting in notable changes in the competitive environment, sales pace, and channel landscape of the home appliance market.

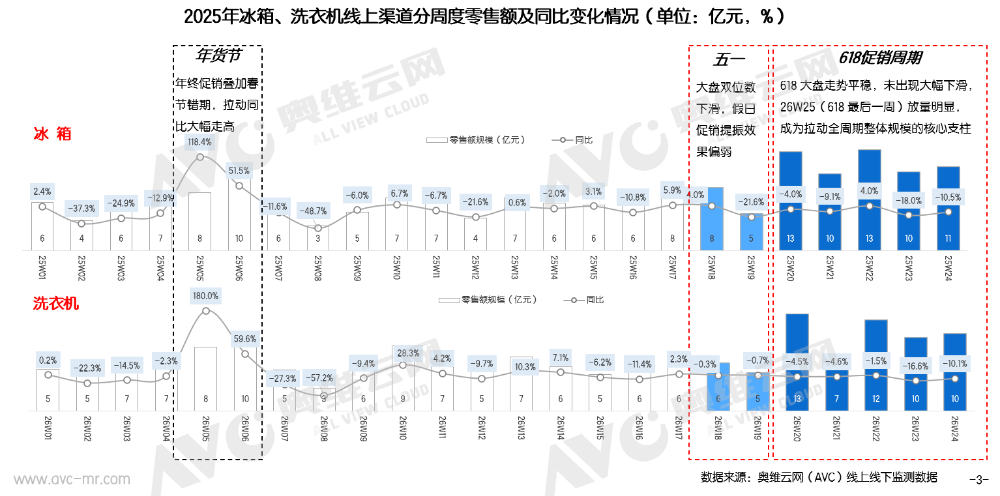

Extended 618 Promotion Period Sees Concentrated Sales Surge in Final Week, Amplifying Matthew Effect Across Channels The 2026 618 promotion period was further extended compared to previous years, with platforms launching pre-promotion activities as early as May 1st. This created three distinct sales peaks throughout the year: a minor traffic surge on May 13th, a marketing node from May 18th-20th, and the main closing period from June 18th-20th. The schedule fully covered multiple consumer holidays, including May Day, 520, and the Dragon Boat Festival.

In terms of sales pace, the pre-sale phase at the beginning of the promotion showed weak market momentum. It was not until the final week of the 618 event that platforms and brands concentrated their marketing resources, driving a surge in terminal sales and providing core support for the overall scale of the promotion. Influenced by anti-price-war discussions in the early stages of the promotion, major e-commerce platforms adopted a more conservative approach in terms of promotional hype and traffic allocation, with overall marketing investment significantly reduced compared to previous years. The competitive landscape among channels showed clear differentiation: The Matthew effect continued to intensify for traditional shelf e-commerce platforms like JD.com and Tmall, with market share further concentrating among top brands. Although instant retail channels maintained rapid growth, their overall sales base remained low, making it difficult to effectively drive the overall home appliance market in the short term.

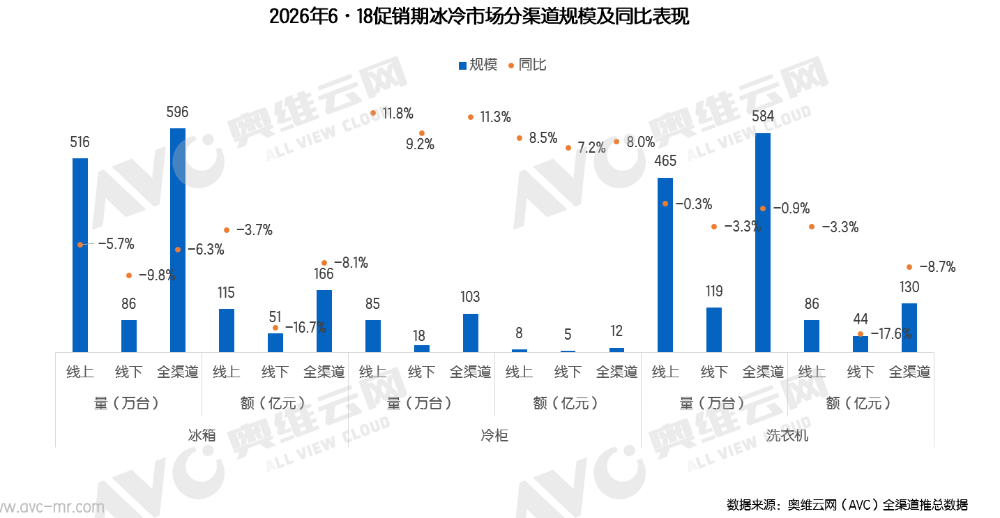

Overall Market Performance: Freezers Surge, Refrigerators Face Slight Pressure, Washing Machines Demonstrate Strongest Resilience

Freezers: The only white goods category to achieve growth in both volume and value during 618, with total channel sales of 1.03 million units (+11.3% YoY) and retail value of RMB 800 million (+8.0% YoY). Both online and offline sales increased, driven by stockpiling demand, effectively offsetting weakness in the refrigerator and washing machine markets.

Refrigerators: Total channel sales reached 5.96 million units, down 6.3% YoY, with retail value of RMB 16.6 billion, down 8.1% YoY. Despite the slight decline in overall scale, market performance exceeded expectations due to base effects. Compared to the heavily pressured air conditioning category, the refrigerator market demonstrated notable resilience.

Washing Machines: Total channel sales reached 5.84 million units, down 0.9% YoY, with retail value of RMB 13 billion, down 8.7% YoY. Sales volumes remained largely stable, while retail value saw a slight decline. Online sales reached 4.65 million units, nearly flat YoY, with only a slight offline decline. Online channels absorbed most replacement demand, supporting overall stability.

Weekly data analysis reveals that the May Day retail period in 2026 had a relatively weak boosting effect on refrigerator and washing machine sales, with only minor fluctuations online. After entering the extended 618 promotion period, both online and offline sales remained under pressure during the pre-heating phases, with no significant surge in pre-sale transactions. It was not until the final week (26W25) that brands and platforms concentrated their resource investments, leading to simultaneous surges in both online and offline sales and significantly narrowing declines. Relying on concentrated sales in the final week, the full 618 promotion cycle scale was supported, while the overall product mix for refrigerators and washing machines was simultaneously optimized. Throughout the year, online sales demonstrated stronger elasticity in response to promotional activities, while offline sales experienced deeper declines due to reduced foot traffic and seasonal factors. The extended pre-promotion model had limited pulling effect on washing machine sales, with only the final promotion week providing effective sales support.

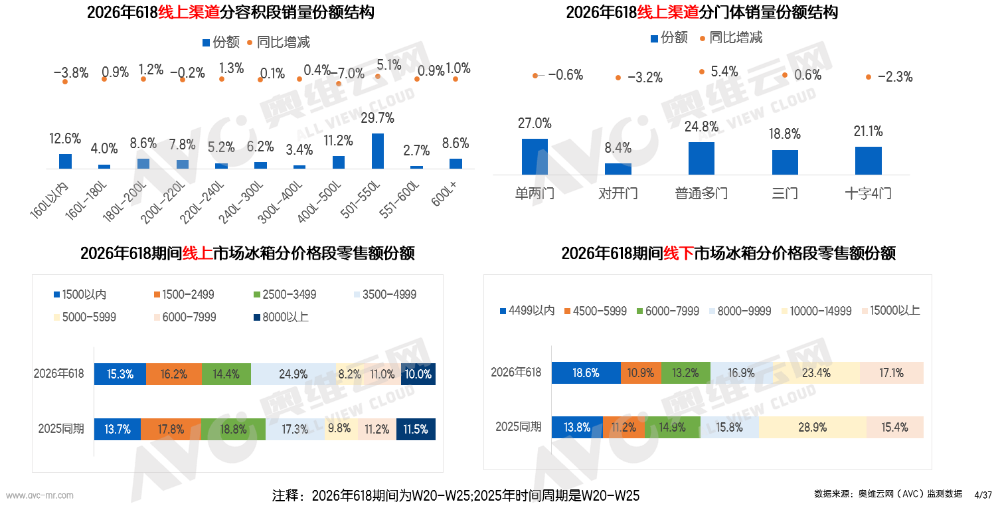

Refrigerators: In a competitive market with limited growth opportunities, the window of opportunity for product selling points is rapidly narrowing. Structural upgrades coexist with price declines: Observing from a product structure perspective, during the 2026 618 event, phenomena such as low-price dumping and disorderly price competition significantly decreased, with the industry's overall average transaction price increasing year-on-year. However, to drive sales of mid-to-high-end models, brands increased discounts, leading to notable price declines in the high-end product segment. This resulted in characteristics of structural upgrades coexisting with price declines.

Monitoring data from Aowei Cloud shows that in the online channel during 618 2026, the market share of the mid-range price band of RMB 3,500-4,999 increased from 17.3% to 24.9%, expanding by 7.6 percentage points year-on-year, while the share of low-end models below RMB 3,500 experienced the largest decline. In contrast, the offline channel showed a different trend, with the overall product structure continuing to weaken.

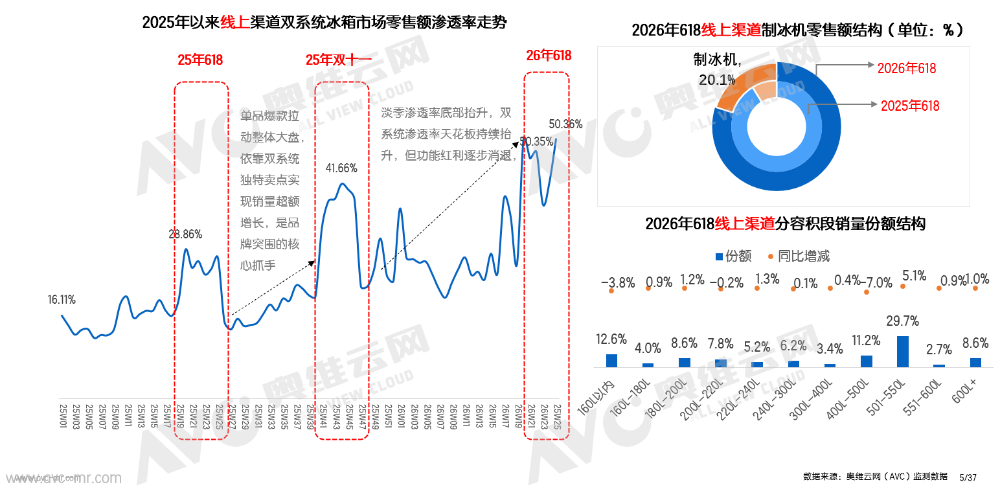

From a product form perspective, during major promotion cycles in 2025, dual-system refrigerators were a key strategy for brands to differentiate themselves and achieve market breakthroughs. During 618 that year, the retail value penetration rate of dual-system refrigerators peaked at only 28.86%. By 618 2026, dual-system refrigerators had become standard in mid-to-high-end models, with penetration reaching a new historical high during the pre-promotion phase. However, the growth dividend from the single function of dual systems continued to diminish.

Notably, the ice maker segment performed outstandingly during this 618, with its penetration rate achieving leapfrog growth. Monitoring data from Aowei Cloud shows that the retail value penetration rate of ice makers surged from 8.7% last year to 20.1%, driven by rapid release of demand in high-end scenarios. Secondly, the mainstream capacity segment of 501-550L continued its growth trend, with its market share increasing by 5 percentage points year-on-year, remaining the foundational segment for online replacement sales.

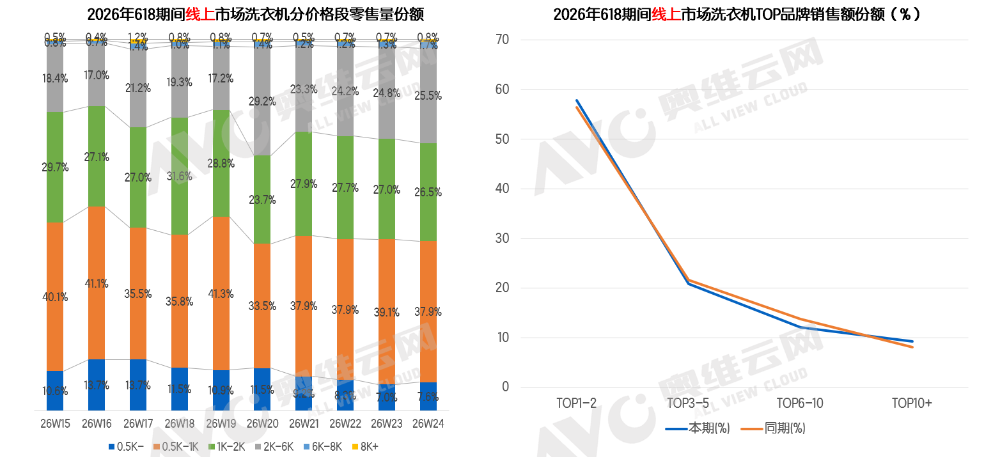

Washing Machines: Demonstrating Resilience Amid High Base, Structural Upgrades Deepen Against the Trend Entry-level models for traffic attraction play a supporting role, while structural upgrades remain the main focus: From a price segment perspective, although traffic-driving models such as 10KG front-load washers priced around RMB 800 and 8KG top-load washers priced around RMB 600 remained important traffic attractors on 618 day, this did not hinder overall structural optimization. As the promotion period progressed, the price structure steadily improved.

Notably, front-load washers saw a significant increase in market share within the mid-range price band of RMB 2,000-4,000, while the trend toward larger 12KG drum diameters in top-load washers continued to deepen. During this promotion cycle, structural upgrades became an industry consensus. Strengthening of the leader effect and stabilization of mid-tier market share: During 618 2026, the top 1-2 brands significantly increased their market share through substantial investments. In the mid-tier segment, although the increased sales of multi-drum products last year had already driven up the market share of related brands, the penetration rate of multi-drum products continued to grow this year, further boosting the market share of these brands. Overall, mid-tier brands maintained stable market share.

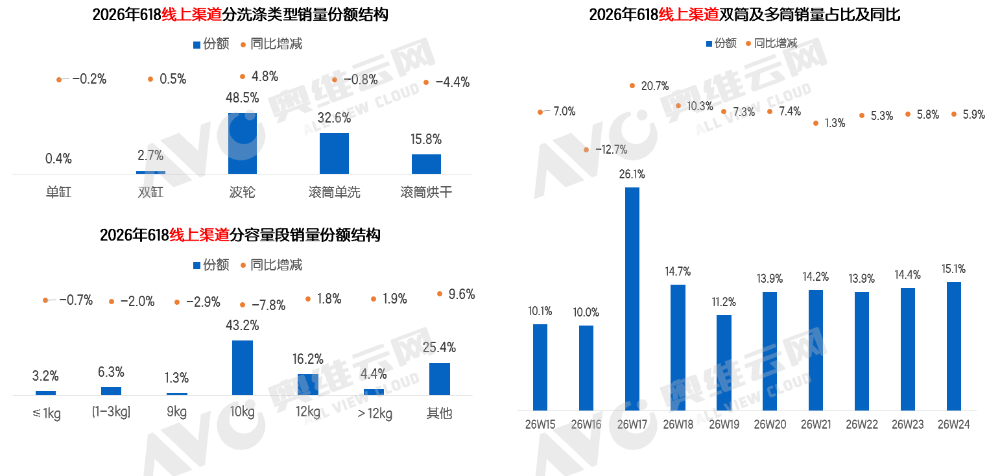

Large capacity and niche scenarios emerge as dual growth engines. The product structure showed clear differentiation, with large capacity (12KG+) becoming a definitive trend in the existing market. Multi-compartment/multi-drum products remained hot sellers, ranking highly in sales. In terms of new products, models such as the Leader Smart Sticker Wash, Hisense Quad-Drum, and Panasonic Stackable began to gain traction. Meanwhile, Midea's "Cute Duo" maintained its focus on single best-selling models.

Notably, top-load washers demonstrated strong vitality in this promotion, with their market share increasing against the trend. In particular, 12KG top-load models grew rapidly, highlighting their experience advantages in washing large items and potentially remaining highly attractive to some users during the promotion.

Overall, the 2026 618 refrigerator and washing machine market exhibited clear structural differentiation: The ultra-long pre-promotion period led to insufficient pre-sale volumes in the early stages, with consumer demand only concentratedly released in the final week. Online sales formed the market's foundation, while offline sales remained under pressure, further exacerbating the Matthew effect across channels. By category, freezers achieved growth in both volume and value due to stockpiling demand, refrigerators faced slight pressure, and washing machines demonstrated strong resilience through product upgrades. The industry saw a relief from low-price, disorderly competition. This is an original article from Aowei Cloud. Unauthorized use or scraping of this content by any organization or individual for purposes such as AI large model training is strictly prohibited.

-

![]()

Total Investment Hits Nearly 3.28 Billion! Goertek Launches Mass Production of 12-Inch Transparent Substrate Wafer for AR Glasses’ Micro-Nano Optical Components

-

![]()

Why Is This Precision Optical Film Leader Worth Reevaluating with a Tens of Millions Procurement?

-

![]()

AI Costs Plummet by 90% Over Nine Years: Key Insights from Davos You Shouldn’t Miss

-

Doubao, Your Late-Night AI Companion, Now Eyes Profitability

-

![]()

SRC Empowers SEER Intelligence to Reach a Market Cap of Tens of Billions, Yet Fails to Sustain Profitability

-

![]()

China’s Embodied AI Industry Faces Fierce Domestic Competition, Making Overseas Expansion Essential for Survival

-

![]()

32.8 Billion Yuan Investment! Goertek’s 12-Inch AR Glasses Optical Wafer Base in Lingang Begins Operations

-

![]()

How Far is the All-New Li Auto L8 from Being the Best Five-Seat SUV with In-House Full-Stack Development?