These Chips Soar to the Trending List

07/11 2025

07/11 2025

738

738

The chip market is never devoid of trending topics, but the list for the first half of 2025 is particularly noteworthy.

Last year, in the article "These Chips Sold Out," the author delved into the 20 models that topped the chip trending list for the first half of 2024. Now, with the release of the new list for 2025, let's explore which chips have ascended to the pinnacle.

01

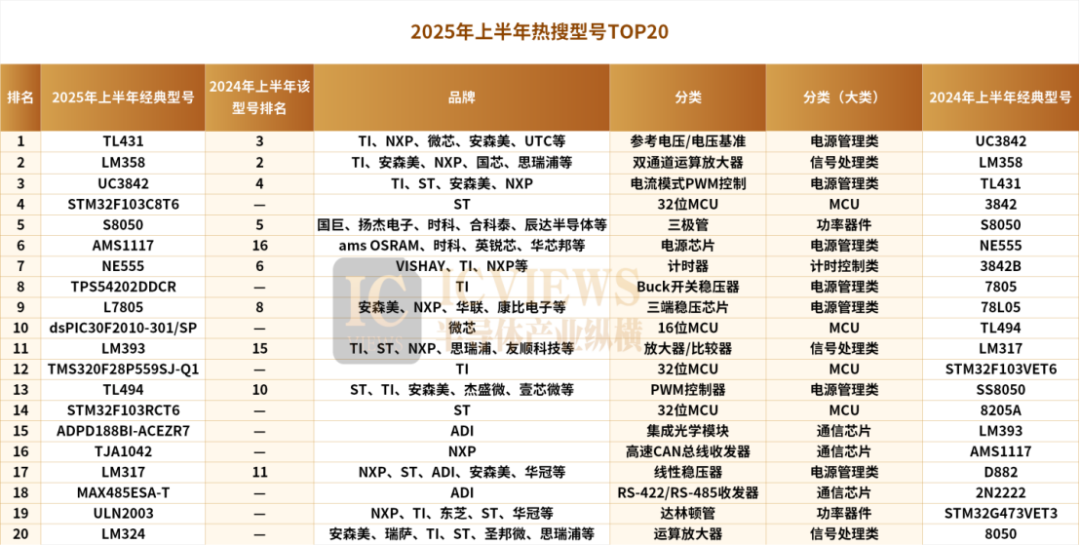

Top 20 Trending Chips of the First Half of the Year

Microcontrollers (MCUs) and power integrated circuits (ICs) accounted for over 50% of the top 20 trending chips in the first half of 2025.

Upon comparison, it was found that 10 out of the 20 chips on the trending list for the first half of 2025 have previously appeared on earlier lists. For example: TL431, LM358, UC3842, S8050, AMS1117, NE555, L7805, etc. In terms of chip performance, most of these "returning" products have undergone extensive market validation, boasting stable performance and robust compatibility.

Additionally, the chips marked with "—" in the table above are newly listed products. Upon closer inspection, it is evident that all four of the aforementioned MCU chips are new additions.

Now, let's delve into the characteristics of these "veterans" and "newcomers".

Analog Chips Maintain Top Spots

The top three power management chips—TL431, signal processing chip LM358, and power management chip UC3842—are all "classic materials" renowned for their versatility and mature technology. The functional definitions, pin packages, and performance parameters of these chips have become industry-standard defaults.

TL431 serves as a precision voltage reference in power management, utilized in linear voltage regulation, switching voltage regulation (such as UC3842 architecture), and battery management. Its advantages include high precision, stability, and low cost.

In industrial and automotive electronics, it excels in harsh environments such as motor control and sensor circuits; in consumer electronics, it is found in chargers, LED drivers, and audio amplifiers.

LM358 is a dual-channel operational amplifier with low static power consumption, effectively reducing system energy consumption. It boasts a wide common-mode input voltage range and strong compatibility with signals of varying amplitudes. Its advantages are flexibility, energy efficiency, and a wide range of applications.

In signal processing, it is used in audio amplifiers, sensor interfaces, filter designs, etc.; in industrial control, it serves as a signal conditioning component in automation equipment and instrumentation; in consumer electronics, it is suitable for audio and video signal processing in portable devices like mobile phones and tablets.

UC3842 is a Pulse Width Modulation (PWM) controller used in AC-DC power converters, adapters, and other switching power supply designs. Its advantages include high efficiency, simplicity, and energy savings.

In charger design, it is widely used in electric vehicle chargers and notebook computer power adapters; in industrial control, it is ideal for scenarios requiring precise voltage control, such as servo drives and frequency converters.

MCUs Make a Strong Showing on the List

This time around, the trending list also features numerous MCU products.

In addition to ST's STM32F103C8T6 and STM32F103RCT6, there are also Microchip's 16-bit MCU product dsPIC30F2010-30I/SP and TI's 32-bit MCU product TMS320F28P559SJ-Q1.

Although ST's STM32F103 series is a decade-old classic, its cost-effectiveness and ecological maturity (such as CubeIDE development tools and an abundance of reference designs) still make it highly competitive. In cost-sensitive fields like industrial control (PLC, sensor nodes) and consumer electronics (home appliance control, smart sockets), its unit price of 5-10 RMB has become the "go-to" choice for engineers.

The global acceleration of automotive electrification and intelligence directly drives the demand for automotive-grade MCUs.

As a member of the C2000 series, TI's TMS320F28P559SJ-Q1 features automotive-grade characteristics (supporting ASIL-D functional safety, high reliability) and technical advantages (GaN/SiC drive, real-time control) that perfectly align with the core scenarios of new energy vehicles. It is suitable for motor drives, hybrid, electric, and powertrain systems, solar and electric vehicle charging, digital power supplies, body electronics, lighting, and other fields.

The certification cycle for automotive-grade MCUs is as long as 2-3 years. TI's C2000 series has passed AEC-Q100 certification and meets ISO 26262 functional safety requirements with 100% documentation coverage, a feat most domestic manufacturers find challenging to achieve in the short term.

Microchip's dsPIC30F2010-30I/SP, as a 16-bit DSC (Digital Signal Controller), is irreplaceable in fields like motor control and digital power supply due to the combined effect of global industrial automation upgrades and "dual carbon" goals. Microchip's dsPIC30F series has forged a technological moat in the field of motor control through the Harvard architecture and an independent DSP instruction set, maintaining a long-term leading market share.

It is evident from these trending products that international leading enterprises hold a firm position in the MCU market. The moat formed by their technological accumulation, ecological barriers, and market penetration remains difficult to shake in the short term. However, domestic manufacturers have launched benchmarking solutions in multiple fields and achieved mass applications in scenarios such as consumer electronics and industrial control.

02

Popular Chips with Domestic Benchmarking

Let's start with the conclusion: strong versatility, mature technology, and significant cost advantages are the hallmarks of the above 20 chips. Under these characteristics, multiple domestic chips have emerged. In the future, we may see more domestic manufacturers on this list.

TI's Boom is Fading

Currently, the power management chip market presents a "three-way split" competitive landscape: the first tier represented by overseas giants such as TI, ADI, Infineon, NXP, Skyworks, and ST; the second tier represented by domestic power management chip listed manufacturers such as JFM, SGB, Fullhan, Mingwei, BL, LXM, Silan, Weier, Xinpeng, and Di'ao; and the third tier represented by other small and medium-sized domestic power management chip enterprises.

Among them, overseas giants like TI and ADI maintain a leading edge in product line completeness and overall technological level, occupying over 80% of the global power management chip market, especially in high-end markets where they hold absolute sway.

However, it must be acknowledged that in the fiercely competitive analog sector, international manufacturers are also facing challenges.

Moreover, chips like TL431 and LM358 belong to the "basic models" in analog chips, with annual demand reaching billions or even tens of billions. While international manufacturers like TI and NXP dominate, for domestic chip companies, launching products of the same model serves as the "stepping stone" to enter the analog chip market—accumulating mass production experience and customer resources through mature models, and gradually penetrating into high-end analog chips (such as high-precision operational amplifiers and automotive-grade amplifiers). Simultaneously, it can also meet customers' needs for "second suppliers" to mitigate the risk of supply disruption due to sole dependency.

Taking Di'ao as an example, its signal chain products highly overlap with TI's price-increased materials, and it has achieved technological breakthroughs in fields such as consumer electronics and automotive electronics. Its automotive-grade analog switches, high-precision sensors, and other products are accelerating their introduction into the supply chain.

In addition to overseas manufacturers like TI, ST, ON Semiconductor, and NXP, domestic manufacturers such as Huafuqin, Huaxuanyang, Kexin, Hongmao Semiconductor, Huazhimei, Yixinwei, and Huaguan also have relevant products for UC3842. These domestic manufacturers' products are gradually closing the performance gap with foreign counterparts and offer certain price advantages, providing more options for domestic power product manufacturers and reducing production costs.

Shanghai Belling's BL358 and other products are comparable to LM358 in key parameters such as accuracy and bandwidth and can be directly replaced for use, widely applied in various consumer electronics and industrial control equipment, occupying a certain market share with their cost-effectiveness advantage.

It is reported that amidst the intense internal competition in the analog market, at the end of last year, TI's LM358 market price ranged from 0.26 to 0.55 RMB, while some domestic brand manufacturers' prices have been as low as around 0.11-0.15 RMB, and some batches within two years are only 0.08 RMB. This phenomenon can also be observed in another analog chip leader, ADI. If ADI's price for a model is 12 RMB, then domestic brands can directly drop it to within 6 RMB, and the general and other replaceable ones basically follow this ratio.

MCU, a Must-Compete Field

Looking at MCUs, under the spotlight of the semiconductor industry, the MCU market has always been a must-compete field. The MCU products on this list primarily come from ST, TI, and Microchip.

Intense competition is a common thread in both the analog chip and MCU markets. In the MCU field, many domestic manufacturers have also achieved new milestones through competition.

The TMS320F28P559SJ-Q1 mentioned earlier is a member of TI's C2000 series. Over the years, TI's C2000 has dominated the field of real-time control. Even giants like Microchip, ST, and Renesas, which have made strides in the power supply and motor fields, have failed to unseat TI's C2000.

In recent years, with the rise of local MCU manufacturers, many markets have begun to witness the presence of domestic MCU manufacturers. Even the previously seemingly impenetrable C2000 is gradually losing ground in the motor control, frequency converter, and servo markets.

Taking Naxinwei as an example, its two products, NS800RT5 and NS800RT3, precisely target TI C2000's F280039, F280049, and other models. Not long ago, Jihai Semiconductor also officially released the G32R501 real-time control MCU based on the Arm Cortex-M52 dual-core architecture and supporting Arm Helium technology, officially declaring its entry into the market dominated by TI's C2000.

In the general-purpose MCU market, the competition between domestic MCU brands such as GD32 and STM32 is also intensifying.

As a leader in China's 32-bit general-purpose MCU field, GigaDevice's GD32, with a cumulative shipment of over 200 million units, over 10,000 users, and a vast array of over 300 product models in 20 series, occupies a pivotal position in the market. GD32 adopts the Cortex-M3 core, achieving full compatibility with the same models of STM32, facilitating user replacement, and featuring a higher main frequency. There are numerous successful cases of replacing STM32 in many fields such as smart homes and industrial control.

In addition to the above companies, many domestic MCU enterprises such as China Sciences Chip, MindMotion, Artesyn, Nationz, Chipsea, and HuaDa Semiconductor have products that can directly benchmark STM32.

Faced with the lower cost advantage of domestic MCUs, imported brands have "lost" in this price war. Not only ST and TI are affected. It is reported that in some product fields, frequent price comparisons have become the norm, and even if a certain domestic MCU has been selected, it may switch to a lower-priced product at any time.

03

Potential Chip Stocks for the Second Half of the Year

From the perspective of popular categories, MCU chips are expected to continue to shine.

The popularity of the four MCU chips on the first-half list has already demonstrated robust market demand. With the deepening development of industrial automation and smart homes, the demand for MCUs with high cost-effectiveness and stable performance will further escalate. Especially domestic mid-to-high-end MCUs, driven by policy support and technological breakthroughs, may achieve rapid growth in market share in the second half of the year, with their narrowing performance gap with international brands and more competitive pricing.

Power semiconductor chips will usher in new growth opportunities. The increasing penetration rate of new energy vehicles and the accelerated construction of charging piles have placed higher demands on power semiconductors. Devices such as IGBT and MOSFET are not only in high demand in the automotive electronics field but are also continuously expanding their applications in fields such as industrial control and energy management. It is anticipated that in the second half of the year, power semiconductor chips with high voltage and high current characteristics will become the focal point of the market.

Under the wave of localization, domestic chips that benchmark popular overseas models hold immense potential. With the continuous improvement of the domestic industrial chain, domestic chips are performing increasingly well in terms of reliability and compatibility. Alternative products for popular chips such as UC3842 and STM32F103C8T6 have been validated in multiple fields. In the future, with the further release of domestic manufacturers' production capacity and the enhancement of market recognition, these domestic chips are expected to be applied in more scenarios and emerge as "dark horses" in the market.

-

![]()

OFILM Reports Colossal 460 Million Yuan Loss: Founder Quietly Shifts Focus to Optical Modules!

-

![]()

Yutong Optics and Zeiss Forge Partnership to Develop Quality Measurement System and Launch "Optical Communication Joint Measurement Class"

-

![]()

AutoNavi Revises Splash Screen Ads with Precision Amid Controversy

-

![]()

Unlicensed Vehicle Disputes: AutoNavi Ensnared in the Aggregation Model

-

![]()

Agent: The 'Hard Requirement' for Entering Core Enterprise Systems for the First Time

-

![]()

Global Auto Market Outlook: Sales Decline in China, US, and Europe, Chinese Exports Approach 10 Million

-

![]()

AI Pioneer Breaks Free from the 'Doldrums'

-

![]()

Valuation Exceeds $26 Billion! Three Chinese "Gold Medalists" Shake Up the AI Industry