Domestic Chip Makers Experience Major Shifts in Performance

08/29 2025

08/29 2025

674

674

More than half of 2025 has elapsed, and recently, a growing number of chip manufacturers have unveiled their first-half financial results.

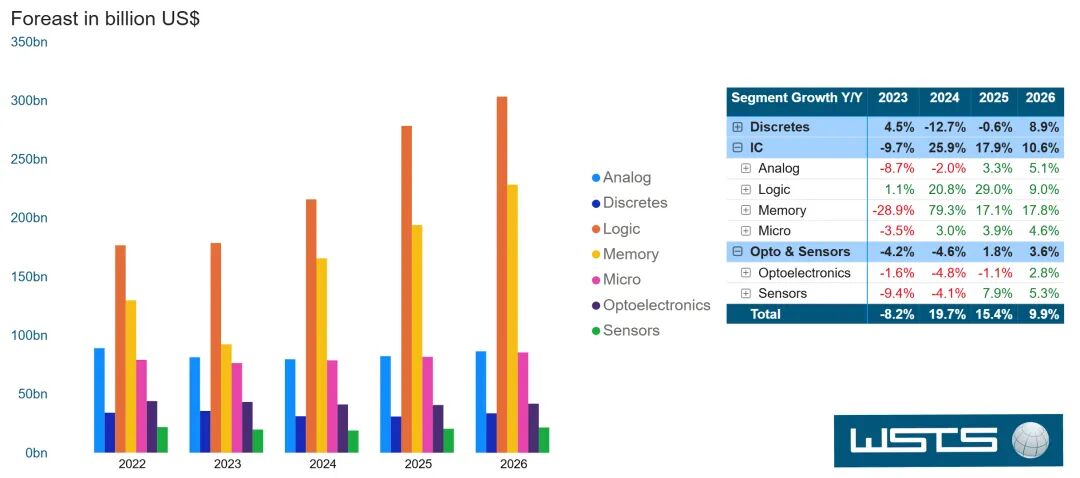

Globally, according to World Semiconductor Trade Statistics (WSTS), the semiconductor market reached a size of $346 billion in the first half, marking an 18.9% increase year-on-year, indicating a clear trend of recovery and growth within the industry.

Among various segments, the logic semiconductor market grew by 7%, memory semiconductors by 20%, and sensors by 16%. Both analog and discrete devices showed modest growth of 4%, while discrete devices and optoelectronic devices experienced quarterly declines of 4% and 0.5%, respectively.

Reviewing the first-half financial reports of domestic chip manufacturers, it becomes evident that they have kept pace with this wave of recovery, with numerous enterprises delivering impressive results. Let's delve into the performance of chip enterprises in the first half of 2025.

01

Who is Making Money?

Computing Power Companies Witness Surge in Net Profits

In the semiconductor industry during the first half of the year, the buzzword was undoubtedly 'computing power'.

The Ministry of Industry and Information Technology reported that by the end of June this year, China had 10.85 million standard racks of in-use computing power centers, with intelligent computing power reaching 788 EFLOPS. The China Computing Power Platform was officially launched, completing the integration of sub-platforms in 10 provinces and cities, including Shanxi, Liaoning, Shanghai, Jiangsu, Zhejiang, Shandong, Henan, Qinghai, Ningxia, and Xinjiang. On the corporate front, Huawei introduced the Ascend 384 super node, boasting an overall computing power 1.6 times that of NVIDIA's top-tier GB200 cabinet.

As market attention focused on the explosive growth in demand for AI computing power, domestic computing power-related enterprises also delivered remarkable results, with a surge in net profits, making them the most eye-catching sector in industry growth.

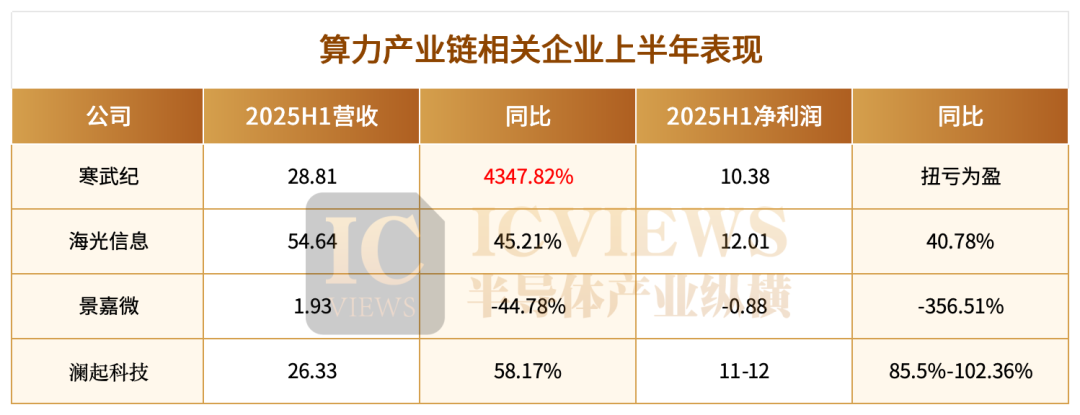

On August 28, Cambrian Innovation's share price surged 15.73% to close at RMB 1,587.91 per share, surpassing Kweichow Moutai to rank first in A-shares. On August 27, Cambrian Innovation's share price also briefly exceeded that of Moutai. A 'historically strongest' first-half financial report, with revenue growing by over 43 times year-on-year and a turnaround in net profit, propelled Cambrian Innovation to the top of A-shares.

In the first half of this year, Cambrian Innovation achieved revenue of RMB 2.881 billion, up 4347.82% year-on-year, with a net profit of RMB 1.038 billion, reversing a loss from the same period last year. In the fourth quarter of last year, Cambrian Innovation achieved its first quarterly profit since going public and has now recorded profits for three consecutive quarters.

The surge in performance in the first half was primarily attributed to the significant increase in the cloud AI chip business. Data shows that in the first half, the company's cloud intelligent chips and accelerator cards generated revenue of RMB 2.87 billion, up 4600% year-on-year. From the revenue structure, the cloud product line has become Cambrian Innovation's absolute core business, accounting for up to 99.6% in the first half of this year; the edge product line generated revenue of RMB 1.56 million in the first half of 2025, accounting for only 0.05%.

Cambrian Innovation was not alone in experiencing improved performance in the first half. Among AI chip-related companies, Hygon Information Technology also recorded growth in revenue and net profit in the first half.

Hygon Information Technology released its first-half 2025 financial report, with revenue reaching RMB 5.464 billion, up 45.21% year-on-year; net profit attributable to shareholders amounted to RMB 1.201 billion, up 40.78% year-on-year. This was the first time that Hygon Information Technology's net profit attributable to shareholders exceeded RMB 1 billion in a single half-year since its listing.

Regarding the reasons for the revenue growth in the first half, Hygon Information Technology stated that during the reporting period, demand for domestic high-end chips continued to rise. The company accelerated its introduction to clients by deepening cooperation with system manufacturers and ecological partners in key industries and fields, driving the expansion of its high-end processor product market and achieving significant revenue growth.

Montage Technology expected to achieve revenue of approximately RMB 2.633 billion in the first half, up approximately 58.17% year-on-year, of which interconnect chip sales revenue was approximately RMB 2.461 billion, up approximately 61% year-on-year; net profit attributable to shareholders ranged from RMB 1.1 billion to RMB 1.2 billion, up approximately 85.5% to 102.36% year-on-year.

For the significant growth in performance in the first half, Montage Technology pointed to the following three main reasons:

Firstly, benefiting from the AI industry trend and strong industry demand, the company's DDR5 memory interface and module supporting chip shipments increased significantly, with the proportion of second-generation and third-generation RCD chip shipments increasing, driving a substantial increase in the company's memory interface and module supporting chip sales revenue.

Secondly, Montage Technology's three high-performance transport chips (PCIe Retimer, MRCD/MDB, and CKD) generated combined sales revenue of RMB 294 million, a significant increase over the same period last year.

Thirdly, as the proportion of sales revenue from DDR5 memory interface chips and high-performance transport chips increased, the company's gross profit margin increased compared to the same period last year.

However, not all computing power-related enterprises could enjoy industry dividends, as InnoSilicon temporarily fell into a performance dilemma in the first half. InnoSilicon reported a loss in the first half, with a net loss of RMB 87.61 million. Regarding the reasons for the decline in revenue, the company stated that it was mainly due to the decline in industry demand and the postponement of acceptance of some projects. Currently, the company mainly has three product lines: graphics display and control, small specialized radars, and chips. Among them, graphics display and control is both the company's existing core business and traditional strength, but the revenue from this business segment experienced a significant decline. In the first half of 2025, revenue from the graphics display and control segment amounted to RMB 84.5883 million, down 62.91% year-on-year.

Overall, the computing power sector continued to exhibit high-growth vitality in the first half of 2025.

Edge AI Chips, All Making Money

In addition to computing power companies, edge AI chip enterprises also turned a profit this year.

DeepSeek launched and open-sourced the DeepSeek-V3 model, significantly reducing the cost of introducing large models into AIoT, making it possible for large models to penetrate the consumer end, and officially ushering in an era of explosive growth for the AIoT industry. Rockchip, Espressif Systems, and other enterprises saw double-digit growth in revenue and net profit, demonstrating the profitability of the industry.

Rockchip's first-half financial report data was particularly outstanding, with revenue reaching RMB 2.046 billion in the first half of 2025, up 63.85% year-on-year; net profit attributable to shareholders amounted to RMB 531 million, up 190.61% year-on-year. For the second quarter alone, the company's revenue reached RMB 1.161 billion, up 31.18% quarter-on-quarter; net profit attributable to shareholders was RMB 322 million, up 54% quarter-on-quarter.

The profit growth rate far exceeded the revenue growth rate. In its financial report, Rockchip attributed its revenue growth to 'flagship products such as RK3588 and newer products like RK3576 leading the AIoT product lines to continue their high-speed growth, especially in key areas such as automotive electronics, industrial applications, machine vision, and various types of robots.'

Aispeech Technology also performed impressively, achieving revenue of RMB 1.938 billion in the first half, up 26.58% year-on-year. More surprisingly, net profit attributable to shareholders amounted to RMB 305 million, up 106.45% year-on-year, while net profit after deducting non-recurring gains and losses even increased by 153.37% year-on-year to RMB 284 million.

Regarding the change in performance, Aispeech Technology stated that during the reporting period, as the downstream smart wearable market continued to grow, the company's market share increased, driving revenue growth. Meanwhile, the overall gross profit margin in the first half was 39.3%, an increase of 6.1 percentage points year-on-year, laying the foundation for the year-on-year increase in net profit.

Specifically, during the reporting period, Aispeech Technology's new-generation smart wearable chip BES2800 was applied in clients' TWS earphones, smartwatches, smart glasses, and other terminal products, with rapid volume increases. In the smartwatch market, Aispeech Technology successfully introduced new domestic and foreign clients such as Xiaotiancai and Suunto and commenced mass production. In the first half of this year, the company's smartwatch chip shipments increased.

In addition to Bluetooth earphones and smartwatches, Aispeech Technology's chips are gradually extending to low-power wireless application scenarios such as smart glasses and wireless microphones. As of the end of the reporting period, chips such as BES2700 and BES2800 from Aispeech Technology have been mass-produced in clients' smart glasses and wireless microphone projects, gradually transforming the company into a platform chip company in the field of low-power wireless computing SoCs.

ThaiMicro, a leading domestic low-power Bluetooth company, also achieved fruitful results in the edge AI chip sector. In the first half of this year, ThaiMicro achieved revenue of RMB 503 million, up 37.72% year-on-year; net profit attributable to shareholders amounted to RMB 101 million, up 274.58% year-on-year; and net profit after deducting non-recurring gains and losses was RMB 93 million, up 257.53% year-on-year.

ThaiMicro stated that the revenue increase was mainly due to growing customer demand and the mass production and shipment of new products, resulting in an increase in sales volume and sales revenue across all product lines compared to the same period last year. Specifically, in terms of new products, during the reporting period, ThaiMicro's newly launched edge AI chips entered mass production, with sales revenue in the second quarter alone reaching tens of millions of RMB; the company's chips were shipped in bulk in the overseas smart home sector, and as the first certified enterprise, its Bluetooth 6.0 chips supporting new functions such as Channel Sounding also entered mass production with global clients; the company's newly launched WiFi-6 multi-mode chips also achieved mass shipments.

Overall, in the first half of 2025, edge AI chip enterprises rode the wave of the AIoT industry's explosion, leveraging the iterative upgrading of their products and market expansion to achieve success in multiple areas of their respective strengths.

Power Semiconductors, Turning the Corner

In the first half of the year, from a global perspective, the power semiconductor market was still in a negative state. 'Weak demand' and 'high inventory' were prevalent, with giants such as Infineon and ON Semiconductor directly stating that 'traditional businesses were under pressure.' STMicroelectronics reported an operating loss of $130 million in the first half, with revenue from its Power & Discrete (P&D) sub-product segment declining by 22.2% in Q2.

However, the perception of domestic power semiconductors was quite different. Unlike the fluctuations in some niche segments, multiple domestic power semiconductor enterprises achieved double breakthroughs in revenue and profit by leveraging their technological accumulation and production capacity advantages. They shed the constraints of previous industry cycles and emerged from a 'turning the corner' growth curve.

Currently, six major power semiconductor manufacturers have successively released their first-half 2025 financial reports. In terms of revenue, each company recorded approximately 20% year-on-year growth, with net profits also increasing significantly.

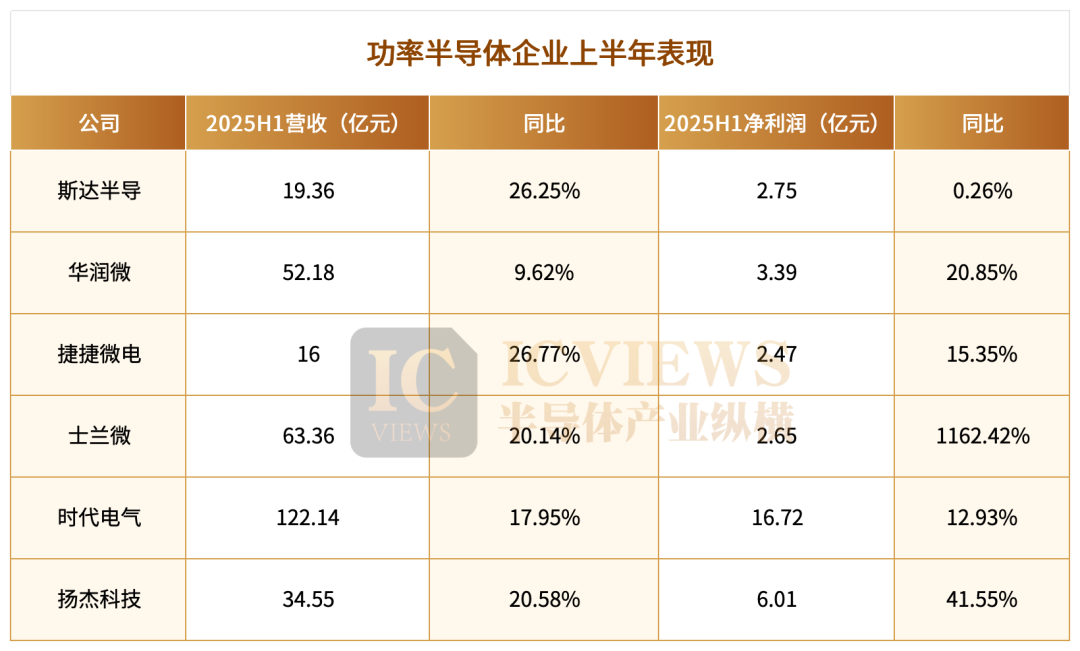

Silan Microelectronics released its first-half 2025 financial report, showing that the company achieved revenue of RMB 6.336 billion in the first half, up 20.14% year-on-year; net profit attributable to the parent company reached an impressive RMB 265 million, surging 1162.42% year-on-year, demonstrating robust growth momentum.

In terms of power semiconductors, Silan Microelectronics' revenue in the first half reached RMB 3.008 billion, up 25% year-on-year. Notably, revenue from its automotive and photovoltaic IGBT and SiC (modules, devices) increased by over 80% compared to the same period last year.

According to Silan Microelectronics, its subsidiaries Silan Integrated's 5-inch and 6-inch chip production lines, Silan Jixin's 8-inch chip production line, and the important equity participation enterprise Silan Jike's 12-inch chip production line all maintained full-capacity production.

Yangjie Technology's half-year financial report indicated that the company achieved revenue of RMB 3.455 billion in the first half, up 20.58% year-on-year; net profit attributable to shareholders amounted to RMB 601 million, up 41.55% year-on-year.

Why could Yangjie Technology achieve significant growth in net profit and revenue in the first half of this year? The financial report revealed that in the first half of this year, the semiconductor industry continued to recover, with strong demand in multiple areas, particularly in automotive electronics and AI-related businesses. The company's power devices such as MOSFET, IGBT, and SiC accelerated breakthroughs in high-growth markets such as new energy vehicles and AI servers.

Currently, Yangjie Technology's initial overseas packaging facility, MCC (Vietnam) Factory Phase I, has commenced mass production and attained full operational capacity, with Phase II also successfully concluded. The company's pioneering SiC chip production line has effectively scaled up to mass production, with its processes and quality reaching domestic benchmarks. Furthermore, the company's initial SiC automotive-grade power semiconductor module packaging project has been finalized and is now in production.

Moreover, in the first half of the year, Jiejie Microelectronics, CRRC Times Electric, and StarPower Semiconductor witnessed revenue increases of 26.77%, 17.95%, and 26.25% respectively, all exhibiting positive growth trends.

02

Who is experiencing financial losses?

In terms of performance, memory enterprises are displaying signs of recovery following an earlier downturn, with most companies reporting year-over-year revenue growth. However, due to fluctuations in market prices, substantial R&D investments, and ongoing inventory pressures, the net profit performance of most firms remains challenging.

Revenue growth has been a common theme among memory enterprises in the first half.

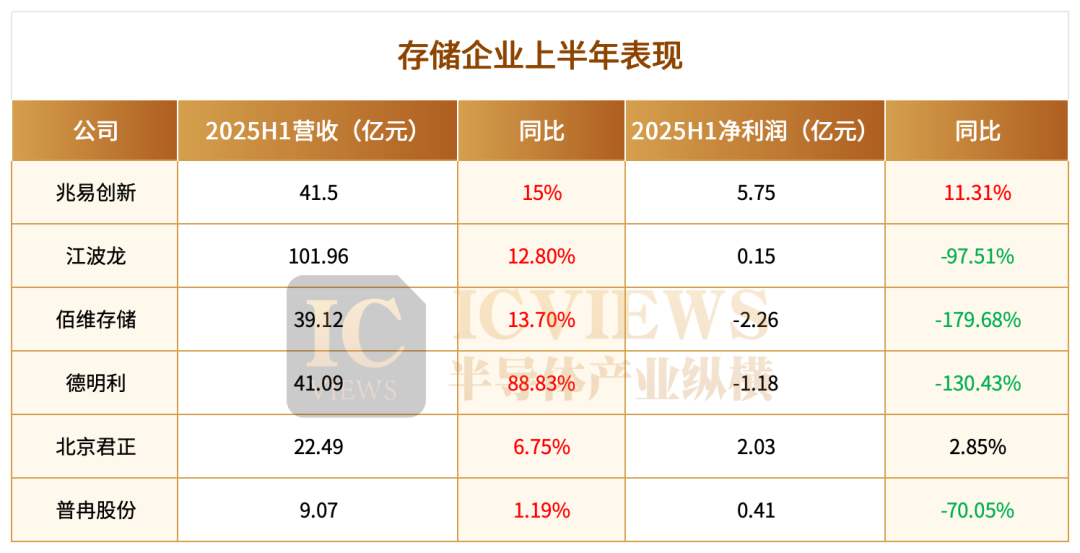

GigaDevice Semiconductor achieved revenues of RMB 4.15 billion, up 15% year-over-year, fueled by market expansion in various sectors such as consumer electronics, automotive, and industrial applications, as well as new demands spurred by AI technology. During the same period, net profit attributable to shareholders reached RMB 575 million, up 11.31% year-over-year, positioning it as one of the more profitable enterprises within its peer group.

Conversely, the net profit attributable to shareholders of ordinary shares of ProRAM Technology Co., Ltd. was RMB 40.73 million, a year-over-year decrease of 70.05%. ProRAM attributed this to the sluggish recovery of demand in the end-consumer market, leading to significant pressure on the market prices of some of its products. Additionally, product costs were slightly impacted by variations in historical inventory procurement costs, resulting in an overall slight increase. During the reporting period, the company's comprehensive gross profit margin was 31.03%, a decrease of 2.72 percentage points from the same period last year, with gross profit decreasing by RMB 21.0438 million year-over-year.

Overall, the memory chip industry has witnessed the dawn of recovery in the first half of 2025. Revenue growth underscores the gradual resurgence of market demand and the effectiveness of enterprises' expansion efforts. Nonetheless, the widespread pressure on net profits highlights that the industry is still constrained by multiple factors, including market price fluctuations, high R&D investments, and inventory pressures.

Moving forward, memory companies must actively address cost and price challenges while continuously optimizing their product structure, expanding market share, and enhancing profitability to steadily progress on the path to recovery, truly emerge from the downturn, and achieve overall industry prosperity.

03

Where is the semiconductor industry headed in the second half of 2025?

What direction will the semiconductor industry take in 2025? As a pivotal link in the industrial chain, the semi-annual report data and related forecasts of foundries offer crucial insights into industry trends.

SMIC and Hua Hong Semiconductor, two representative foundries, exhibited distinct performance and development trends in the first half of the year.

According to revenue data, SMIC's 2025 semi-annual report revealed that operating revenue increased by 23.1% year-over-year to RMB 32.348 billion, with net profit attributable to shareholders of listed companies rising by 39.8% year-over-year to RMB 2.301 billion. Meanwhile, Hua Hong Semiconductor achieved operating revenue of RMB 8.018 billion in the first half of 2025, up 19.09% year-over-year.

However, in terms of net profit, there are notable differences between the two companies. Hua Hong Semiconductor's net profit attributable to shareholders of listed companies was RMB 74 million, a year-over-year decrease of 71.95%, while net profit after deducting non-recurring gains and losses was RMB 55.3918 million, a year-over-year decrease of 76.31%. The company explained that revenue growth was attributed to increased wafer sales volume and the contribution of Hua Hong's manufacturing projects entering mass production. The decline in net profit was primarily due to capacity ramp-up costs in the initial production stages of Hua Hong's manufacturing projects and the continuous increase in the company's overall R&D investment.

Capacity utilization serves as a key metric to gauge the operating conditions of foundries. In this year's Q2 financial report data, SMIC approached full capacity, while Hua Hong Semiconductor's utilization rate even surpassed 100% again.

Specifically, regarding various business segments, SMIC highlighted at the Q2 exchange meeting:

First, shipments of automotive electronics products continued to grow steadily, with significant revenue contributions from various automotive-grade chips, such as analog and power management chips. Furthermore, the "China for China" supply chain is taking shape, particularly in the automotive industry, and the company will also collaborate with international customers to establish third-generation semiconductor capacities, including SiC (silicon carbide) and GaN (gallium nitride).

Second, despite the expansion of new power device capacity, demand still outstrips supply. The company is deploying power device capacity to meet the needs of strategic customers.

Third, across different downstream market segments, domestic customers in the network field exhibit an extremely high substitution rate, the capacity of the domestic memory industry has increased markedly, orders in the mobile phone sector are stable, and domestic industrial and automotive demand has recovered significantly.

04

Where is the AI wind blowing?

From the preceding analysis of domestic chip manufacturers' first-half performance and the industry trends revealed by foundries, it is evident that artificial intelligence (AI) is emerging as an unstoppable force reshaping the semiconductor industry landscape.

Whether it's the surge in net profits of computing power enterprises, the overall profitability of edge AI chip enterprises, or the strategic focus of foundries on automotive-grade chips and power devices, these trends are all driven by AI demand.

This driving force is first and foremost fueled by top-level policy support. On August 26, the State Council issued the "Opinions on Deepening the Implementation of the 'AI+' Action" (hereinafter referred to as the "Opinions"), which clearly outlines that by 2027, China aims to lead in achieving widespread and in-depth integration of AI with six key areas, with the application penetration rate of new-generation intelligent terminals and intelligent agents exceeding 70%, and the role of AI in public governance significantly enhanced. By 2030, the application penetration rate of new-generation intelligent terminals and intelligent agents is expected to surpass 90%, with the intelligent economy becoming a vital growth pole for China's economic development. By 2035, China aims to fully enter a new era of intelligent economy and intelligent social development.

From an industrial competition perspective, China's AI race is akin to the emergence of new forces in the new energy vehicle sector. It necessitates activating effective demand on the consumer side, integrating AI into daily life through new-generation intelligent terminals, intelligent agents, and other products, and propelling the economy towards a consumption-driven growth model. Additionally, it requires pushing for breakthroughs in core technologies on the industrial side, focusing on sectors such as GPUs, HBM memory chips, Chiplet advanced packaging, semiconductor equipment and materials, to pave the way for independent control of key industrial chains.

It is no exaggeration to state that this is a battle for a trillion-level market and an even more intense national competition.

Market feedback also underscores the high enthusiasm for the AI race. Today, both Cambricon and SMIC have reached new historic highs. So far, the AI computing power index has risen by 57.94% within the year. With the country's long-term support for AI firmly in place, the "AI+" policy will continue to gain momentum, and the domestic share of China's subsequent computing power demand will continue to grow.

The era of AI for all has arrived.

-

![]()

OFILM Reports Colossal 460 Million Yuan Loss: Founder Quietly Shifts Focus to Optical Modules!

-

![]()

Yutong Optics and Zeiss Forge Partnership to Develop Quality Measurement System and Launch "Optical Communication Joint Measurement Class"

-

![]()

AutoNavi Revises Splash Screen Ads with Precision Amid Controversy

-

![]()

Unlicensed Vehicle Disputes: AutoNavi Ensnared in the Aggregation Model

-

![]()

Agent: The 'Hard Requirement' for Entering Core Enterprise Systems for the First Time

-

![]()

Global Auto Market Outlook: Sales Decline in China, US, and Europe, Chinese Exports Approach 10 Million

-

![]()

AI Pioneer Breaks Free from the 'Doldrums'

-

![]()

Valuation Exceeds $26 Billion! Three Chinese "Gold Medalists" Shake Up the AI Industry