African Mobile Phone King Battles Global Challenges Amid Overseas Expansion

06/06 2025

06/06 2025

989

989

Concerns arise for the "King of African Phones."

By Xie Yingjie, Investor Network

Shenzhen Transsion Holdings Co., Ltd. (hereinafter referred to as "Transsion Holdings", 688036.SH), a Shenzhen-based mobile phone manufacturer that has flourished in Africa, earning it the moniker "King of African Phones," is now facing unprecedented challenges.

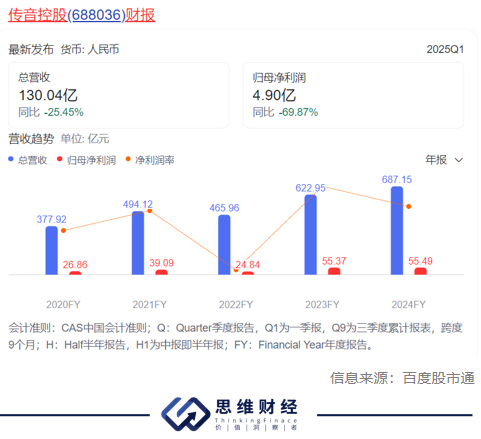

In the first quarter of 2025, Transsion Holdings' operating revenue amounted to 13.004 billion yuan, marking a year-on-year decrease of 25.45%. Net profit attributable to shareholders of the listed company was only 490 million yuan, a significant year-on-year drop of 69.87%, representing the largest single-quarter decline in net profit since its listing.

For three consecutive quarters, Transsion Holdings has seen performance declines, with its share price plummeting by nearly 40% from its one-year high.

Low-price strategy falters

Listed on the STAR Market in September 2019, Transsion Holdings derives most of its revenue from mobile phone sales. The company was favored by investors due to its high market share in Africa and rapid expansion into underdeveloped regions.

According to the company, Transsion was the first to enter Africa and has maintained a high and stable market share. Subsequently, it ventured into South Asia, achieving a significant market share in Pakistan and Bangladesh.

In 2024, the growth rate of Transsion Holdings' revenue and net profit notably slowed down, with operating revenue reaching 68.715 billion yuan, a year-on-year increase of 10.31%, and net profit attributable to shareholders of the listed company amounting to 5.549 billion yuan, a year-on-year increase of 0.22%.

The performance decline in the first quarter of 2025 further underscores the company's pressure from market competition and supply chain costs. Transsion Holdings attributes the performance decline primarily to the combined impact of market competition and supply chain costs, leading to a decrease in operating revenue and gross profit. Additionally, the high base in the same period of 2024 also contributed to the profit decline.

Notably, according to the previously released annual report, the salary of founder Zhu Zhaojiang underwent a significant change, decreasing from 12.5276 million yuan in 2023 to 78.431 million yuan in 2024, a drop of 46.845 million yuan or 37.39%.

In terms of market competition, Transsion Holdings' dominant position in the African market is being encroached upon by other brands. Xiaomi, Honor, Realme, Lenovo, and other brands have entered the African market to compete for market share. Xiaomi, with its sub-brands such as Redmi, has swiftly gained a foothold in the African market with highly competitive prices and robust technological research and development capabilities. In the fourth quarter of 2024, Xiaomi achieved a year-on-year growth rate of 22% in Africa, with its market share reaching 13%.

According to Canalys statistics, in the fourth quarter of 2024, Transsion Holdings' shipment share in Africa was 49%. However, Xiaomi Group President Lu Weibing shared first-quarter data for 2025, indicating that Transsion's shipment share in the African market dropped to 47%, a year-on-year decrease of 5%. Conversely, Xiaomi's shipment share in the African market was 13%, a year-on-year increase of 32%, making it the second-largest mobile phone brand in Africa after Transsion and Samsung.

Among the top five mobile phone brands in the African market, except for Samsung in second place (with a share of 21%), all are Chinese brands. OPPO's market share was 3%, a year-on-year increase of 17%, and Honor's market share was 3%, a year-on-year increase of 283%. This suggests that Transsion's advantage in its home market of Africa is rapidly eroding.

This competitive landscape not only affects Transsion Holdings' market share but also has a detrimental impact on its profitability.

In recent years, the company has also accelerated its expansion into markets beyond Africa and South Asia, including Southeast Asia, Latin America, the Middle East, and Eastern Europe. Compared to Africa, Bangladesh, Pakistan, and other countries and regions, Transsion's current market share in these emerging markets is still relatively low.

The risk persists that Transsion Holdings' progress in expanding into these emerging markets may not meet expectations, and the challenge of recreating the "African myth" remains.

Struggles with diversification transformation

In fact, doubts about the company's core technology have lingered for a considerable time. On the one hand, continuous R&D investment is crucial for the company's technological advancement. However, the data clearly shows that Transsion Holdings prioritizes marketing over technology.

The annual report reveals that in 2024, Transsion Holdings' R&D expenses amounted to 2.517 billion yuan, accounting for 3.66% of revenue. In comparison, Xiaomi's R&D rate in 2024 was 6.6%, and Huawei's R&D rate was 20.8%.

In 2024, Transsion Holdings' selling expenses reached 4.836 billion yuan, marking a significant increase of 11.72%; the sales ratio stood at 7.04%, accounting for more than 50% of the period expenses. The primary increase stemmed from a substantial rise in promotion and advertising expenses, which increased by 324 million yuan in 2024, a year-on-year increase of over 10%.

In terms of supply chain costs, Transsion Holdings also faces certain pressures. Although Transsion Holdings has some bargaining power in component procurement, its procurement costs are still impacted to some extent amidst global supply chain fluctuations. Additionally, Transsion Holdings predominantly uses non-leading suppliers for mobile phone components, which may limit its optimization space in supply chain costs to a certain extent.

Moreover, the company's lack of core technology increases the likelihood of patent disputes. The company's core technologies primarily encompass four aspects: deep-skin photography technology based on localization in emerging markets such as Africa, application innovation of new hardware materials, big data user behavior analysis, and OS systems and mobile internet product services.

Canalys Senior Analyst Manish Pravinkumar also noted that Transsion faces fierce competition in its main market of Africa, with fellow domestic mobile phone brands Xiaomi and OPPO experiencing rapid growth in shipments in Africa. In the fourth quarter of 2024, Xiaomi achieved a 22% increase in Africa, and Realme also recorded a year-on-year increase of 70% during the same period. Additionally, Qualcomm's patent litigation in India and Europe has led to an increase in Transsion's supply chain costs, further compressing its profit margins.

It is worth noting that Transsion Holdings' operating cash flow has also deteriorated. In the first quarter of 2025, the company's net cash flow from operating activities was -741 million yuan, a significant deterioration from the same period last year, reflecting that the company may face certain pressures in sales collection and capital turnover.

Despite these challenges, Transsion Holdings remains actively seeking breakthroughs. On the market front, Transsion Holdings has intensified its expansion into new markets such as Latin America, Southeast Asia, and the Middle East, collaborating with local manufacturers and operators to tap into the market demand for feature phone to smartphone upgrades. On the product side, Transsion Holdings has made AI and high-end positioning the core keywords of its product strategy, aiming to enhance product competitiveness through technological innovation.

However, the future of Transsion Holdings remains uncertain. The transition from feature phones to smartphones in the African market is sluggish, and the price difference between the two types of products is substantial, leading to slow market growth, which constrains Transsion Holdings' growth potential in the region. The uncertainties in the global economic environment and tariff policies have also squeezed the spending power of African consumers, further affecting Transsion Holdings' market performance.

The company acknowledges that channel construction, brand promotion, and gaining consumer recognition in new markets require investments in time, funds, and manpower. The high initial investment in exploring new markets may reduce the company's current profitability; if the exploration does not meet expected goals, it will also adversely affect the company's performance.

Transsion Holdings' experience underscores that even former industry leaders find it challenging to remain unscathed amidst intensifying global market competition and supply chain fluctuations. For Transsion Holdings, maintaining its advantages in the fiercely competitive market and sustaining profitability amidst rising supply chain costs will be crucial for its future development. (Produced by Siwei Finance)■

Source: Investor Network

-

![]()

OFILM Reports Colossal 460 Million Yuan Loss: Founder Quietly Shifts Focus to Optical Modules!

-

![]()

Yutong Optics and Zeiss Forge Partnership to Develop Quality Measurement System and Launch "Optical Communication Joint Measurement Class"

-

![]()

AutoNavi Revises Splash Screen Ads with Precision Amid Controversy

-

![]()

Unlicensed Vehicle Disputes: AutoNavi Ensnared in the Aggregation Model

-

![]()

Agent: The 'Hard Requirement' for Entering Core Enterprise Systems for the First Time

-

![]()

Global Auto Market Outlook: Sales Decline in China, US, and Europe, Chinese Exports Approach 10 Million

-

![]()

AI Pioneer Breaks Free from the 'Doldrums'

-

![]()

Valuation Exceeds $26 Billion! Three Chinese "Gold Medalists" Shake Up the AI Industry