Voyah's Listing Boosts Dongfeng Group's Strategy, Sending Share Prices Soaring 70%

08/28 2025

08/28 2025

731

731

Strategic Retreat for Advancement

Author|Wang Lei

Editor|Qin Zhangyong

Dongfeng Motor Group's strategy of "retreating to advance" is ingeniously conceived.

Recently, Dongfeng Motor Group unexpectedly announced that its subsidiary, Voyah Auto, would list on the Hong Kong stock market via an "introduction listing" method, with plans to distribute Voyah Auto shares to existing shareholders. Simultaneously, Dongfeng Group shares (the H-share entity holding non-core businesses such as fuel vehicles and components) will undergo a merger and acquisition through its subsidiary Dongfeng Motor Group (Wuhan) Investment Co., Ltd., achieving privatization and delisting from the Hong Kong stock market.

Following a weekend of anticipation, Dongfeng Group shares surged upon the opening of the Hong Kong stock market, peaking at HK$10.10, representing a nearly 70% jump. As of press time, the closing price was HK$9.2.

Renowned investment institution Citigroup also revised its target price for Dongfeng Motor Group upward from HK$6.20 to HK$10.34, maintaining a "buy" rating.

01 Dongfeng's Strategic Retreat

The simultaneous delisting of the parent company and listing of the subsidiary may initially seem confusing, but it essentially boils down to "independent new energy business + liquidation of traditional business."

Dongfeng Motor Group's announcement clearly explains the rationale behind this move. In essence, it is driven by the company's persistently low valuation in the capital market.

Moreover, its market value has long been in a state of "net worth breaking." As of July 31, 2025, Dongfeng Group's closing price was HK$4.74 per share, with a total market value of only HK$39.12 billion. The stock value was significantly below net assets, with a corresponding price-to-book ratio of approximately 0.24 times.

The price-to-book ratio often serves as a reference indicator for the capital market to assess the future potential of a listed enterprise. A long-term market value below net asset levels suggests that the financing function of the H-share listing platform has been largely lost.

In Dongfeng Motor Group's view, such a low valuation hardly reflects the true value of the enterprise itself.

In fact, this phenomenon of inverted valuation is not uncommon among traditional automakers, especially during the current challenging period of transition towards electrification in the automotive industry.

In terms of sales, Dongfeng has been constrained by the painful transition of the industry and the pressure of internal competition, with sales declining for several years, from a peak of 4.27 million vehicles in 2016 to 2.48 million in 2024, a decrease of nearly 1.8 million vehicles.

According to Dongfeng Motor's financial report for the first half of 2025, cumulative sales amounted to 823,900 vehicles, representing a year-on-year decline of 14.7%. Notably, the performance of joint venture brands was particularly bleak, with Dongfeng Nissan (including Dongfeng Infiniti and Venucia) reporting a cumulative sales decline of 23.5% to 252,800 vehicles, Dongfeng Honda down 37.4% to 149,000 vehicles, and DPCA down 28.3% to 27,000 vehicles.

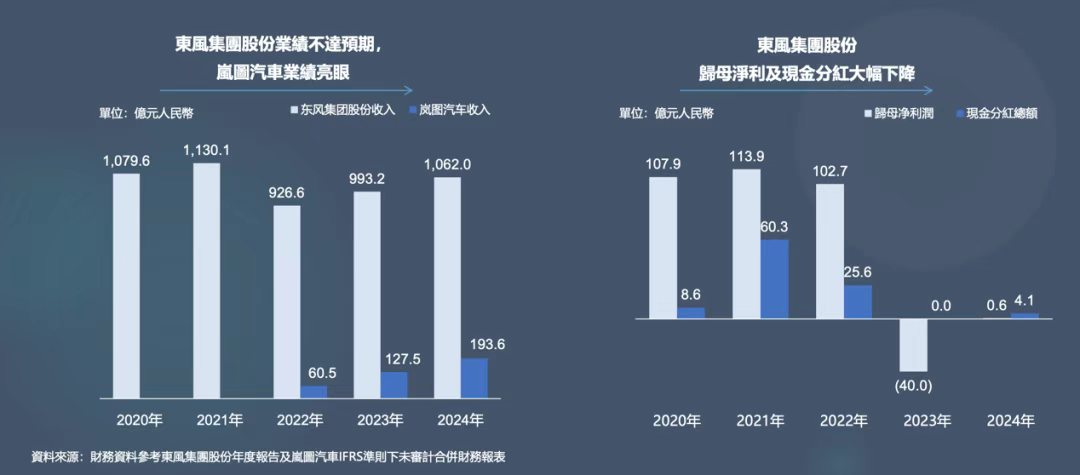

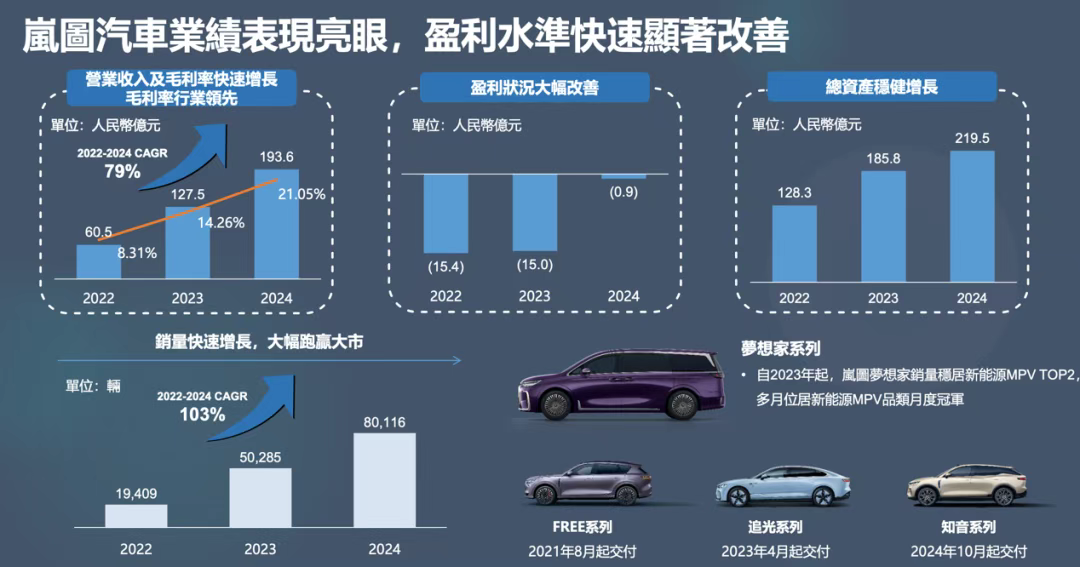

The pressure on sales is even more alarming when reflected in financial performance. The first-half performance report for 2025 shows that while the group's revenue reached RMB 54.533 billion, an increase of 6.6% year-on-year, and gross profit was RMB 7.599 billion, an increase of 28.0% year-on-year, net profit attributable to shareholders of listed companies was only RMB 55 million, a steep drop of nearly 92% compared to the same period last year's RMB 684 million.

From an overall performance perspective, it is indeed underwhelming, but when isolating the new energy vehicle business, the picture is vastly different. In the first half of the year, Dongfeng Motor Group's new energy vehicle sales reached 204,400 vehicles, a year-on-year increase of over 33%.

It is worth noting that behind the net profit of only RMB 55 million, the joint venture segment suffered a net loss of RMB 107 million, while the net profit of associated enterprises was RMB 161 million. In other words, the profits earned by Dongfeng's independent business were instead consumed by the larger joint venture segment.

This comparison highlights that the previously large and sluggish traditional joint venture business has overshadowed the rapid progress of the new energy vehicle business.

In other words, the value of high-quality assets has not been fully recognized in Dongfeng Group's overall valuation.

This unreasonable situation needed to be addressed.

Prior to its delisting, Dongfeng Motor was akin to a complex mixture of internal asset sectors, encompassing both traditional automotive and new energy vehicle businesses. The valuation logic was convoluted, making it difficult for the capital market to discover investment value.

Furthermore, precisely because of this, Dongfeng Motor Group was more often classified as a "traditional automaker," leading to two critical issues: low overall performance resulting in lower valuation, and the success of the new energy business being overshadowed.

Therefore, the new energy business, with its greater growth potential and representation of future development, can break free from the constraints of the existing system and become the company's new value anchor.

02 Voyah's Ascent

Clearly, this significant responsibility falls on Voyah's shoulders.

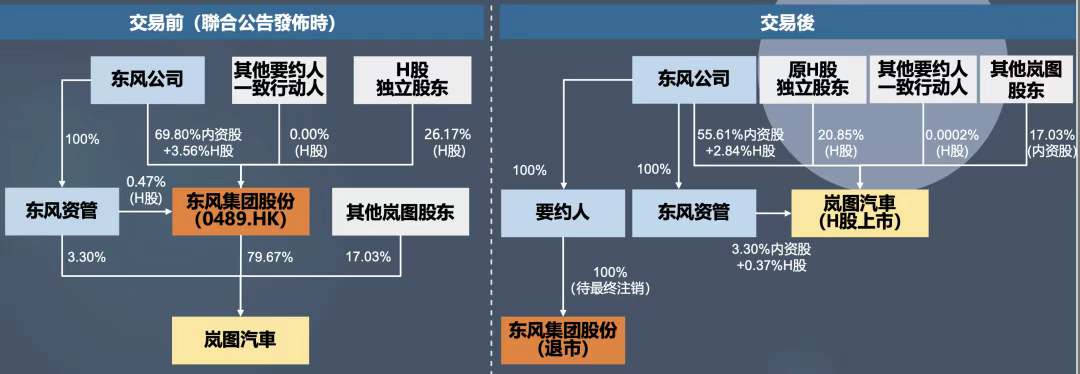

Let's first review Dongfeng Motor Group's current operation. This transaction comprises two core elements: "equity distribution + merger and acquisition."

The first aspect is equity distribution. Dongfeng Group shares will distribute 79.67% of its equity in Voyah Auto to all shareholders according to their shareholding ratio and share class. Following the distribution, Voyah Auto will list on the Hong Kong Stock Exchange via an "introduction listing" method.

It is worth mentioning that "introduction listing" is a special listing path that does not involve the issuance of new shares or fundraising. The core is that the company only lists its already issued shares for trading on the stock exchange, transitioning from a non-public to a public trading state. Essentially, it is "listing for circulation" rather than "fundraising listing," fundamentally differing from IPOs that require new share issuance for fundraising.

Moreover, for Voyah, its equity has already been clearly allocated within the Dongfeng Group system, eliminating the need for new share issuance for financing. Therefore, it can bypass the processes of new share issuance, roadshows, pricing, etc., allowing Voyah to obtain a Hong Kong stock listing status at a rapid pace.

Additionally, the merger and acquisition aspect involves Dongfeng Motor's wholly-owned subsidiary in China, Dongfeng Motor Group (Wuhan) Investment Co., Ltd., as the subject. It will pay equity consideration to Dongfeng Motor Group Co., Ltd., the controlling shareholder of Dongfeng Group shares, and cash consideration to other shareholders, ultimately achieving 100% control of Dongfeng Group shares.

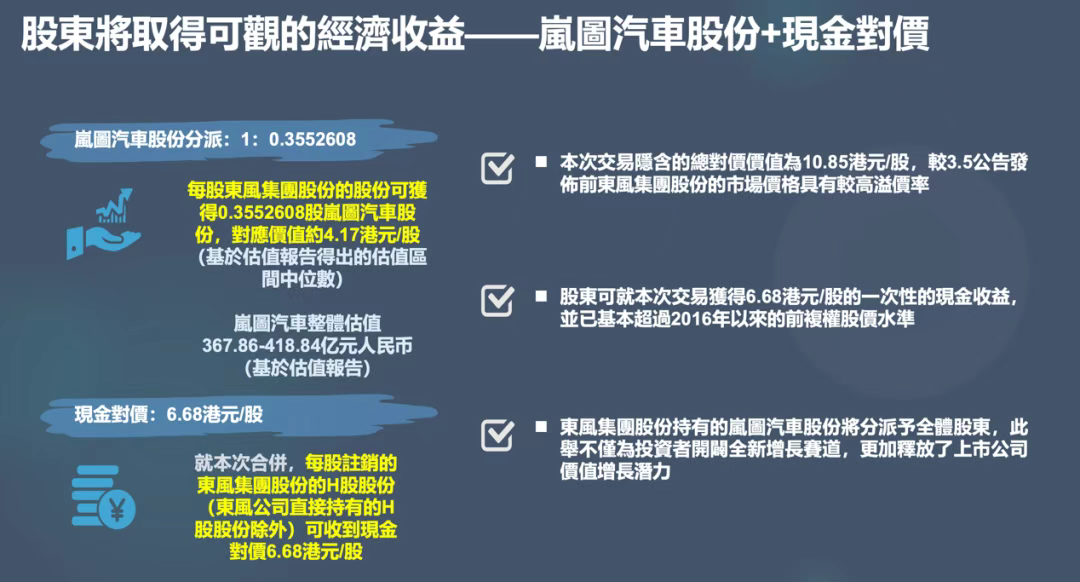

According to the repurchase plan, Dongfeng Motor's overall repurchase price is HK$10.85 per share, comprising HK$6.68 per share in cash and HK$4.17 per share in Voyah Auto equity, totaling HK$10.85. This price will be used to buy all shares held by small and medium shareholders in the market.

Simply put, if you hold Dongfeng Motor shares, upon resumption of trading, you will directly receive HK$6.68 in cash for each share you lose, which is higher than the price before trading suspension. Concurrently, you will also receive one share of Voyah Auto stock worth HK$4.17.

It is important to note that these two transaction elements are not "sequential" but are executed simultaneously.

For Voyah to successfully list, Dongfeng Group shares must be delisted. Conversely, for Dongfeng Group shares to be delisted, Voyah must also successfully list. Only when both sides are completed can the transaction be deemed successful.

Post-transaction, Voyah will replace Dongfeng Group shares and become the overall listed Hong Kong stock company representing Dongfeng's core businesses.

Why Choose Voyah Auto?

On one hand, within Dongfeng Motor, there have long been plans to pursue a listing for Voyah, and Voyah has emerged as one of the most valuable and growth-oriented quality assets under Dongfeng Motor.

As early as June 2021, Voyah Auto announced its independent operation and simultaneously launched an employee stock ownership plan. Since then, Voyah Auto has publicly discussed the possibility of an IPO on multiple occasions. In 2023, Voyah Auto's CFO Shen Jun stated that if monthly sales could reach around 10,000 vehicles, the conditions for listing would be met.

In terms of sales, Voyah has exceeded 10,000 sales for five consecutive months in 2025, and the prerequisites for listing have already been fulfilled.

Furthermore, Voyah Auto's performance has also started to "meet expectations," with its degree of loss gradually narrowing and standing at the brink of profitability.

Financial report data indicates that Voyah Auto's revenue in 2022, 2023, and 2024 was approximately RMB 6.052 billion, RMB 12.749 billion, and RMB 19.361 billion, respectively, with the magnitude of losses decreasing annually, at approximately RMB -1.538 billion, RMB -1.496 billion, and RMB -90 million, respectively. Notably, in the fourth quarter of 2024, it achieved quarterly profitability.

In 2025, in the first seven months, Voyah's cumulative sales exceeded 68,000 vehicles, nearing the annual sales of 2024. The net loss in the first half of the year has narrowed to RMB 18 million, approaching the breakeven point.

Voyah's rapid growth has been fully supported by Dongfeng Group. This transaction is not merely a replacement of old and new businesses but also marks the commencement of Dongfeng Motor's reform.

A brand-new and capable Voyah Auto is on the horizon.

-

![]()

Li Bin Claims, 'Denying the Pure EV Trend is Like Ostrichism.' What's Li Xiang's Take?

-

Lenovo: Liu Jun Turns Left, Yang Yuanqing Turns Right

-

Lenovo: Liu Jun Goes Left, Yang Yuanqing Goes Right

-

![]()

MiniMax Shares Unlock: Cornerstone Shareholders Show Long-Term Optimism, Yet Stock Plummets Nearly 30% in Two Days; Zhipu Also Sees Nearly 20% Drop Today

-

![]()

Single-Day Plunge of 40%: The 'First AGI Stock' Faces More Than Just Share Price Concerns

-

![]()

Ricoh and Fuji Hike Prices on Legacy Edge; Insta360 Poised to Disrupt Mirrorless Camera Market

-

![]()

Ricoh and Fujifilm Raise Prices in Tandem, Relying on Established Reputations; Insta360 Poised to Disrupt Mirrorless Camera Market

-

![]()

Strategic Shift in Photoelectric Sensing: Maxvision Secures Controlling Stake in CAS Optotech