Record-Breaking! Surpassing Japan is Just the Beginning

04/08 2026

04/08 2026

481

481

A Shift in Eras Has Already Occurred

Recently, Nihon Keizai Shimbun cited data from automakers and statistics from MarkLines Information Consulting, revealing that by 2025, Chinese automakers will have sold nearly 27 million vehicles globally (including brands like BYD, Geely, Chery, and SAIC), compared to around 25 million for Japanese automakers. China will secure the top spot in global sales for the first time, while Japan will fall from its position for the first time since 2000.

This is not the first time China has reshaped the global automotive industry. As early as 2023, China surpassed Japan to become the world's largest automobile exporter. Driven by the trends of electrification and intelligence, China's auto industry has once again overtaken traditional automotive powers in terms of scale.

In response to the change in the global automotive sales crown, some netizens offered a vivid analogy: It's like Nokia witnessing the rise of Apple or Kodak seeing the dawn of the digital age—a shift between old and new eras has already taken place.

True Scale Leadership

Today, China's auto industry has built scale advantages across export structures, domestic foundations, and the global landscape.

In exports, China sold 7.098 million vehicles in 2025, up 21.1% year-on-year, continuing to rank first globally. Unlike 2023, when China first became the top exporter, the 2025 exports represent a qualitative shift. High-value-added NEVs now account for a significantly larger share. More importantly, Chinese automakers have begun establishing localized models of "overseas factories + supply chains" in Thailand, Brazil, Hungary, and other locations, marking a transition from mere commodity trade to capacity and standard exports.

Data from the China Association of Automobile Manufacturers shows that in 2025, China's auto sales reached 34.4 million vehicles, up 9.4% year-on-year, maintaining the top Production and sales scale for 17 consecutive years. This vast market not only provides growth space for automakers but also serves as a testing ground for technological iteration and product optimization. Chinese brand passenger vehicle sales hit 20.936 million units, up 16.5% year-on-year, capturing nearly 70% of the market and shattering the long-dominant market pattern of joint-venture brands.

Cui Dongshu, Secretary-General of the China Passenger Car Association, noted in an article that by 2025, Chinese automakers will account for 35.6% of global market share, up 1.4 percentage points year-on-year. Among the top 20 global automakers by sales, six are Chinese—surpassing Japan's five. BYD, SAIC, and Geely rank in the global top 10, while Chery, Changan, and Great Wall have also made the list, forming a tiered global competitive landscape.

In contrast, Japanese automakers are generally experiencing scale contraction. Among Japan's seven major passenger vehicle manufacturers in 2025, Honda's sales fell 7.5%, and Nissan dropped out of the global top 10 for the first time since 2004. Even Toyota, which defended its title as the top-selling automaker with 11.32 million units, showed sluggish growth. Japanese brands are being squeezed in China and face "dimensionality reduction" competition from Chinese brands in terms of intelligence and cost-effectiveness in traditional strongholds like North America and Southeast Asia, fundamentally tilting the global auto industry balance.

China's automotive scale advantages continue to solidify. On April 1, multiple Chinese automakers released their Q1 2026 sales results, with strong overall performance. Geely Auto led Chinese brands with 709,400 vehicles sold in Q1; new energy startups also surged, with Leapmotor selling 110,200 units (up 25.82% year-on-year) and NIO delivering 83,500 new vehicles (up 98.3% year-on-year).

China's New Energy Vehicles Continue to Gain Momentum

Particularly noteworthy is the immense boost China's NEV rise has provided to the entire industry.

In 2025, China's NEV production and sales reached new heights, with annual sales hitting 16.49 million units, up 28.2% year-on-year, ranking first globally for 11 consecutive years.

Over the past year, NEVs have also become the core driver of export growth, with 2.615 million units exported in 2025, surging 103.7% year-on-year and accounting for nearly 40% of total exports. Leading companies performed exceptionally well: Chery led with 1.344 million units exported, followed by BYD and SAIC.

China's NEV market is highly dynamic, with a constant stream of new technologies and products. In early 2026 alone, heavyweight models like the Lynk & Co 08 EM-P, 2026 XPENG P7+, and BYD Seal 07 EV were launched, covering plug-in hybrid, pure electric, and extended-range powertrains.

Meanwhile, the industry's technological frontier has seen dense breakthroughs: In intelligent driving, XPENG unveiled its second-generation VLA (Visual-Language-Action Model) architecture, enabling full-scenario intelligent driving capabilities. In all-solid-state batteries, Chery's Rhino all-solid-state battery achieved an energy density of 400Wh/kg (targeting 600Wh/kg), offering over 1,500km of range, with plans to debut in the Exeed ES8 in 2027.

From an industrial ecosystem perspective, China has built the world's largest NEV supply chain, spanning upstream lithium mining and battery materials, midstream power batteries, motors, and electric controls, to downstream vehicle manufacturing and charging infrastructure—achieving full self-developed and controllable and providing a solid foundation for NEV scale development. National Energy Administration data shows that as of late February 2026, China had 21.01 million electric vehicle charging ports, up 47.8% year-on-year, forming the world's largest EV charging network to support over 40 million NEVs.

Shifts in consumer demand have further solidified the market position of Chinese NEV makers. Cui Dongshu noted that consumers now focus less on price and more on the comprehensive value of product strength, ownership experience, and full-lifecycle services. Chinese automakers have acute captured this shift, continuously optimizing range, charging speed, intelligent features, and after-sales service, boosting product competitiveness.

From Scale Leadership to Comprehensive Global Leadership

China surpassing Japan in global auto sales in 2025 marks a significant reshaping of the global auto industry and a milestone for China's automotive development. However, Chinese automakers still lag behind international giants like Toyota and Volkswagen in profitability, brand value, and global operations.

In the first three quarters of FY2026, Toyota sold 7.302 million vehicles globally with an operating profit of approximately ¥3.2 trillion. Despite a 26.1% year-on-year drop in net profit, its 2025 per-vehicle net profit remained around ¥17,000. In contrast, leading Chinese automakers like BYD and Geely had per-vehicle net profits of about ¥6,900 and ¥4,770, respectively—Toyota's profits were 2.5x and 3.6x higher.

National Bureau of Statistics data shows that in 2025, China's auto industry revenue reached ¥11.18 trillion (up 7.1%), but profit was only ¥461 billion (up 0.6%), with cost growth (8.1%) far outpacing revenue. The 4.1% profit margin nearly halved from 7.8% in 2017.

Multiple factors contribute to this gap. In product mix, Japanese automakers dominate the mid-to-high-end market with strong brand premium capabilities, while Chinese automakers have yet to fully break through in high-end segments, and price wars further compress profits. In cost control, Japanese automakers leverage lean production and global supply chains for ultimate cost management across the board. In global operations, Japanese automakers have decades-old, stable overseas businesses, while Chinese automakers are in a high-investment phase of overseas factory and channel construction, making short-term profitability difficult.

Additionally, Chinese automakers still need to improve self-developed and controllable capabilities in core technologies and key components. While leading in power batteries and smart cockpits, they remain dependent on overseas suppliers for high-end chips, precision manufacturing equipment, and core materials, driving up costs and restricting profits. Meanwhile, heavy R&D investment (e.g., BYD's ¥63.4 billion in 2025, up 17%) faces long return cycles, limiting short-term profit gains.

Global automotive competition is now a multidimensional contest, and sales leadership is just the starting point. To transition from an automotive powerhouse to a global leader, Chinese automakers must address gaps and shortcomings, achieving a leap from "scale leadership" to "comprehensive global leadership."

-

![]()

Is Momenta’s “Physical AI” Premium Justified?

-

![]()

Memory Prices Soar, Budget Phones No Longer Just Watered-Down Flagships

-

Who Defines the Value of 'Office Environment' in the AI Era?

-

Why Did Insta360’s Market Cap Spike and Then Retreat After Taking on DJI as a Benchmark?

-

![]()

DeepSeek Interview Shatters the 'White Moonlight' Illusion of Former Huawei 'Genius Teen'

-

Four-Week Net Sales Reach $38 Billion: Institutions Flee En Masse as Retail Investors Continue Buying Spree

-

![]()

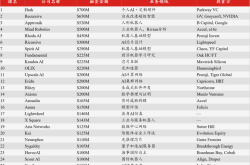

Dissecting 25 AI Startups with Over $50 Million in Series A Funding: The Top Three Areas Where Smart Money is Betting

-

![]()

Dissecting 25 Series A Financings Exceeding $50 Million: AI's Smart Money is Betting on These Three Directions