BMW Group: Three Years of Performance Guideline Downgrades Amidst a Shrinking Chinese Market Share

07/08 2026

07/08 2026

484

484

The BMW Group is currently navigating through its most intense transformation challenges since its entry into the Chinese market. Recently, the company has, for the third consecutive year, revised its full-year performance forecast downward. The automotive segment's EBIT margin has been halved to the range of 1%-3%, and the pre-tax profit has been adjusted to reflect a significant decline. The primary driver behind this adjustment is the intensifying competition within the Chinese market. In the first quarter of 2026, BMW Group's deliveries in China experienced a 10% year-on-year decrease, marking the largest drop among major global markets, and its market share in China has been continuously shrinking.

Securities Star observed that, in preparation for the launch of new-generation models, the BMW brand (hereinafter referred to as "BMW") will suspend production of all domestically manufactured pure electric models in July. However, this move will result in a product gap of at least three months. This bold product iteration underscores the transformation anxiety faced by traditional luxury automakers amidst the wave of electrification and intelligentization. The success of these new-generation models in reshaping brand competitiveness remains to be tested by the market.

01. Q1 Sales in China Lead the Decline

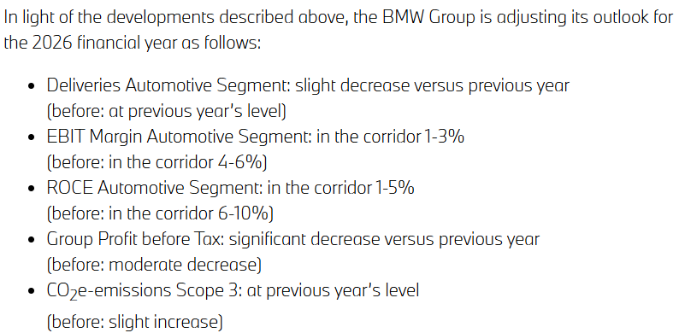

On June 16, the BMW Group downgraded three core operating indicators. The full-year automotive segment's EBIT margin was adjusted from 4%-6% to 1%-3%, and the group's pre-tax profit was revised from a moderate decline to a significant decrease. New vehicle deliveries were adjusted from flat to a slight decline.

Additionally, the automotive segment's return on invested capital was significantly downgraded from 6%-10% to 1%-5%. The automotive segment's free cash flow is expected to exceed €2.5 billion, with the net income dividend payout ratio and share buyback program remaining unchanged.

Securities Star noted that this marks the third consecutive year that BMW Group has downgraded its full-year performance forecast, with pessimistic expectations continuing to rise. In September 2024, due to prolonged sluggishness in the Chinese market, BMW Group downgraded the automotive segment's EBIT margin from 8%-10% to 6%-7%. In 2025, due to lower-than-expected sales in China and financial support provided to dealers, BMW Group's full-year pre-tax profit expectation was downgraded from 5%-7% to 5%-6%.

The primary reasons for this performance forecast downgrade center on intensifying competition in the Chinese market, cost pressures stemming from geopolitical conflicts in the Middle East, tariff increases, and one-time expenses from accelerated structural reforms. Among these, the intensifying competition in the Chinese market is the main factor impacting BMW Group's profits.

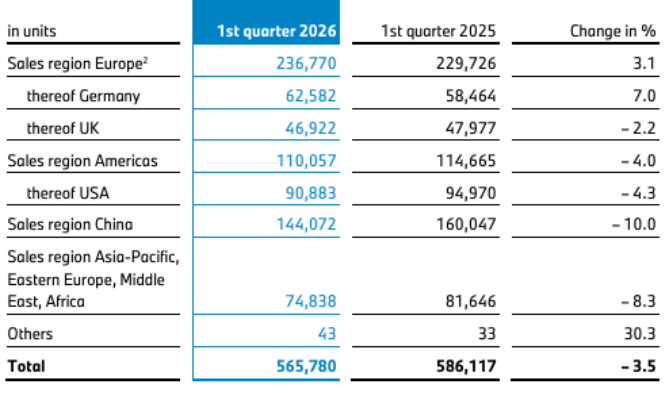

China has long been BMW Group's largest single market globally. However, the rapid rise of local automakers in the electrification and intelligentization sectors has directly squeezed its market share. In the first quarter of 2026, BMW Group's deliveries in China reached 144,100 units, down 10% year-on-year, marking the largest drop among global core markets. Notably, these sales figures heavily relied on significant terminal price reductions, with BMW slashing list prices for 31 models in January of this year. In the first quarter of 2026, only Europe saw a year-on-year delivery increase of 3.1%, with the German market growing by 7%, representing one of the few bright spots among major markets.

At its peak, China accounted for up to 30% of BMW Group's global sales. Since 2024, sales in China have continuously contracted, falling 13.4% in 2024 and another 12.5% in 2025. Notably, in the fourth quarter of 2025, BMW Group's sales in China dropped by 15.9%. China's share of BMW Group's global sales has declined from 32.3% in 2023 to 25.46% in the first quarter of 2026.

BMW Group stated that the downward trend in the Chinese automotive market intensified further in the second quarter, with particularly strong pressure on fuel-powered models. The current situation in China has heightened competition across the entire Asia-Pacific region, while sales in Europe and the U.S. remain positive but insufficient to offset the decline in China and Asia-Pacific.

Financially, in the first quarter of 2026, BMW Group reported revenue of €31.007 billion, down 8.1% year-on-year; pre-tax profit plummeted 24.6% to €2.348 billion; and net profit fell 23.1% to €1.672 billion. BMW Group stated that despite cost savings compared to the previous year, these could only partially offset the adverse impacts of sluggish market conditions in China, increased tariff expenditures, and rising depreciation and amortization expenses.

02. Halt of Domestically Produced Pure Electric Models Fails to Mask Short-Term Crisis

The first-quarter report for 2026 shows BMW Group delivered 565,800 units, down 3.5% year-on-year. Breaking down by sub-brands, BMW main brand deliveries fell 4.6% to 496,000 units; Rolls-Royce deliveries dropped 8% to 1,271 units, indicating fatigue in the high-end luxury market; only MINI saw a 6% increase to 68,500 units.

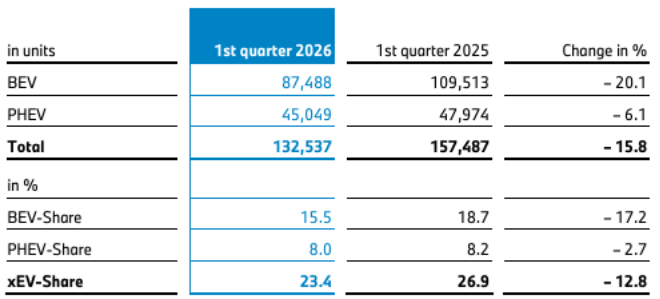

In the electrification sector, BMW Group's performance is equally concerning. In the first quarter of 2026, BMW Group delivered 132,500 electric vehicles, down 15.8% year-on-year, with their share of total deliveries dropping from 26.9% in the same period of 2025 to 23.4%. Among them, pure electric vehicle deliveries fell 20.1% to 87,500 units, accounting for only 15.5% of total deliveries.

Securities Star noted that, facing declining competitiveness in new energy products, BMW has initiated capacity restructuring. Starting this July, BMW will halt production of all domestically produced pure electric models, including the i3, i5, and iX1. These three models were developed based on BMW's CLAR fuel-vehicle platform, known as "retrofitted electric" models. However, amid accelerated industry electrification, these models significantly lag behind domestic new energy vehicles in the same price range in terms of smart cockpit and intelligent driving experiences.

Data from Chezhijia shows that from January to May 2026, combined sales of the i3, i5, and iX1 reached 10,700 units. The i3 performed the best but still averaged only around 1,000 units per month. Compared to domestic new energy models selling tens of thousands of units monthly, a significant gap remains.

Despite serving as BMW's mainstream pure electric market explorers over the past few years, the product strength of these three models can no longer support the brand's electrification strategy in China. BMW stated that this production halt is a routine capacity adjustment based on market rhythm and product lifecycle. The market views this move as paving the way for the introduction of new high-end pure electric products. According to plans, the first domestically produced new-generation model, the iX3 long-wheelbase version, will officially launch in the fourth quarter of this year.

Another core significance of halting "retrofitted electric" models lies in rectifying the imbalanced pricing system. In recent years, constrained by insufficient comprehensive product strength, these models have relied on significant price cuts to drive sales. The i3's bare-car terminal price once dropped to RMB 170,000-180,000, not only severely compressing per-unit profit margins but also eroding the brand's premium pricing power.

Notably, this strategic shift comes with real-world costs. From the production halt in July to the launch of the new BMW iX3 long-wheelbase version in the fourth quarter, BMW's domestically produced pure electric product line will face at least a three-month gap. In contrast, brands like NIO, XPeng, and Li Auto have already entered their 2.0 or even 3.0 product cycles, continuously capturing market share in the luxury pure electric sector with advantages in range, intelligent driving, and ecosystems. During this gap, whether potential customers will switch to competitors and the ultimate impact on terminal sales and dealers are real issues BMW must confront.

BMW's bold product adjustments reflect the development anxiety traditional luxury brands face amidst electrification transformation. The new-generation platform is also its core lever to reshape market competitiveness. However, success in narrowing the gap with domestic new energy brands and stabilizing the pricing system hinges on the localized implementation effectiveness of new-generation series in intelligentization and localization. (This article is first published by Securities Star, Author | Lu Wenyan)

- End -

-

![]()

OFILM Reports Colossal 460 Million Yuan Loss: Founder Quietly Shifts Focus to Optical Modules!

-

![]()

Yutong Optics and Zeiss Forge Partnership to Develop Quality Measurement System and Launch "Optical Communication Joint Measurement Class"

-

![]()

AutoNavi Revises Splash Screen Ads with Precision Amid Controversy

-

![]()

Unlicensed Vehicle Disputes: AutoNavi Ensnared in the Aggregation Model

-

![]()

Agent: The 'Hard Requirement' for Entering Core Enterprise Systems for the First Time

-

![]()

Global Auto Market Outlook: Sales Decline in China, US, and Europe, Chinese Exports Approach 10 Million

-

![]()

AI Pioneer Breaks Free from the 'Doldrums'

-

![]()

Valuation Exceeds $26 Billion! Three Chinese "Gold Medalists" Shake Up the AI Industry