Global Automotive Supply Chain Dynamics: China Surpasses U.S. to Secure Third Place

07/08 2026

07/08 2026

420

420

A transformed landscape, with power gravitating eastward.

The recently unveiled

A transformed landscape, with power gravitating eastward.

The rankings unveil a discernible 'west-to-east' transition in the global automotive supply chain, marking the most profound reshuffling in recent years. The era of multi-center competition and cooperation has dawned.

European and American Giants Face Mounting Performance Pressure

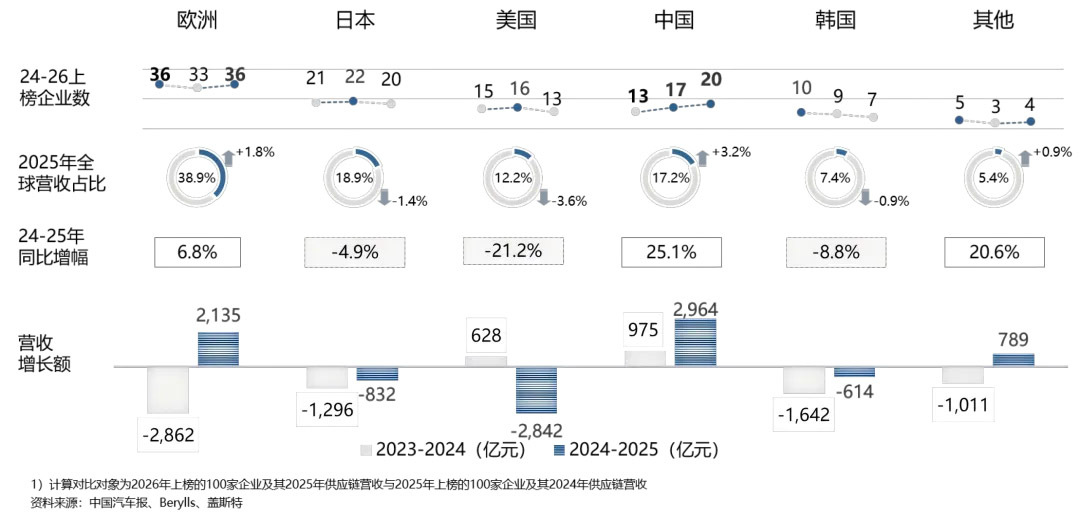

According to the report, the 2025 revenue data indicates that the aggregate revenue of the top 100 global supply chains reached RMB 8.61 trillion, reflecting a modest year-on-year uptick of 1.9%. Leading the pack are Bosch, Denso, and CATL, with the number of Chinese enterprises swelling to 20.

This signifies a fundamental shift.

Across various major markets, the reshuffling of the landscape is palpable. There is a clear alternation between established and emerging enterprises, with mounting pressure on the U.S., Japan, and South Korea, and a notable ascent for China.

The industry's overall moderate recovery, coupled with the sluggish growth of established players, emerges as the primary contradiction highlighted in this ranking, intricately intertwined with the actual industrial stratification.

Despite the aggregate revenue of the top 100 global automotive supply chains not experiencing a decline, when excluding newly added entities due to ranking iterations, it is observed that nearly a hundred longstanding companies that have maintained their positions for two consecutive years have witnessed a year-on-year revenue downturn.

The 1.9% increase is entirely attributable to new entrants. Among them, CATL from the Chinese market catapulted from 7th to 3rd globally, Weichai Group ascended to 7th, Huayu Auto climbed to 11th, and Luxshare Precision made its debut on the list at 66th.

These ranking advancements underscore a collective upward trajectory for Chinese suppliers, signaling that the local supply chain has transcended the stage of mere scale expansion and is progressively augmenting its global market influence.

As Chinese supply chain enterprises ascend in prominence, the role of the Chinese market within the global supply chain is further solidified. The number of Chinese auto parts companies has surged to 20, with their global revenue share escalating from 14% to 17.2%.

Europe, as a longstanding automotive powerhouse, continues to dominate the regional revenue rankings among the global top 100, with the number of listed companies rebounding to 36, accounting for 38.9% of total revenue. Data reveals that European traditional system suppliers have fortified their positions by leveraging their deeply entrenched global vehicle support networks.

Bosch remains at the forefront. However, the 2025 financial report underscores that Bosch's future transformation is heavily contingent on the Chinese market. In FY2025, Bosch's profit margin dwindled to 2%, ensnared in the throes of transformation, with the Chinese region emerging as one of the few bright spots in its performance.

Amidst increasing revenue but dwindling profits, Bosch Group announced the premature resignation of its Chairman of the Board, Stefan Hartung. He previously remarked, '2025 has been an arduous and, at times, even agonizing year for Bosch.'

Through the strategy of 'In China, For the Globe,' Bosch aspires to deeply synergize with the efficiency and rapid iteration capabilities of the Chinese industrial chain, accelerating technological innovation and business model transformation as the linchpin to reversing performance and outpacing the transformation cycle. Currently, Bosch boasts 38 production bases and 28 R&D centers in China, continually bolstering its local R&D and manufacturing prowess.

However, from the top 100 list, it is evident that it is not these established European companies that are exerting pressure on the U.S., Japan, and South Korea and driving the reshuffling of the landscape, but rather the formidable strength emanating from the Chinese market. With the market expansion of multiple suppliers such as CATL, Weichai Group, and Huayu Auto, China has eclipsed the U.S. to claim the third place previously held by the U.S. supply chain top 100.

The report reveals that the number of U.S. companies has dwindled to 13, with their share plummeting from 15.8% to 12.2%, marking the steepest decline across all regions. From last year's performance, the U.S. automotive supply chain is currently grappling with multiple challenges, with core contradictions centered on three fronts: the impact of tariff policies, dependence on rare earth resources, and bottlenecks in localized production.

The aluminum shortage crisis epitomizes the predicament of the U.S. supply chain. The 50% tariff imposed by the U.S. on imported aluminum has inflicted significant costs on automakers seeking overseas alternative supplies.

Sam Fiorani, an analyst at consulting firm AutoForecast Solutions, commented, 'We've never witnessed such a scenario before. The lessons gleaned from the semiconductor crisis should have equipped manufacturers to tackle supply chain issues, but the concentrated eruption of all problems is unexpected and exceedingly challenging to respond to.'

While analysts often find the U.S. automotive supply chain 'unexpected,' from a global market vantage point, it is not surprising that the Chinese automotive supply chain has supplanted the U.S.

Because, amidst the changing fortunes, there is a multi-year migration of the supply chain's power center, with the underlying competitive rules of the supply chain accelerating their evolution.

Japanese and Korean automakers are not immune to this migration. Although Japanese companies still command 20 seats, their revenue share has receded from 20.3% to 18.9%. South Korean companies have been whittled down to 7, with overall operations still under duress.

While the reasons for the pressure on the U.S., Japan, and South Korea vary, they confront the same trend and are simultaneously 'losing momentum,' reflecting the overall passivity of the old competitive order amidst the tide of electrification and intelligent transformation.

Power Gravitates Eastward

The analysis report posits that the triangular landscape of the global supply chain, previously dominated by 'Japan, Germany, and the U.S.,' has now shifted to 'Japan, Germany, and China.'

This signifies that the power center of the global automotive supply chain is gravitating 'eastward,' and the global automotive supply chain is undergoing a profound structural metamorphosis.

This process has merely commenced. In other words, for traditional established suppliers in Europe, the U.S., Japan, and South Korea, the agony of transformation will persist.

The report highlights that power batteries, automotive electronics, wire-controlled chassis, and in-vehicle software have emerged as core growth areas, while the growth of fuel and low-end standard parts has contracted, with electrified and intelligent new forces diluting the market share of traditional giants.

The rise and fall among various segments unveil the direction of the migration of industrial focus, implying that the competitive rules in the automotive supply chain have shifted to the competition for discourse power in the integration capabilities of electrified and intelligent systems and the deep collaboration ecosystem between whole vehicle manufacturers and parts suppliers.

In this competition for ecological discourse power, China holds a pioneering vantage point. The revenue growth rate of the new energy sector for the top 100 Chinese supply chain companies reached 26.9% in 2025, with the overall profit margin of the sector soaring to 13.9%, leading among the seven major segments.

Taking the battery industry as an exemplar, CATL has ascended to the top three globally, with domestic battery companies such as Guoxuan High-Tech and CALB either making their debut in the global top 100 or steadily climbing in the rankings.

In the intelligent domain, the R&D investment intensity in the automotive electronics segment reached 6.8%, leading among all segments. Luxshare Precision made its debut on the list at 66th globally, while Desay SV steadily ascended in the rankings.

European established companies have also reaped the benefits of this stability. Bosch's early investments in electrification, intelligent transformation, and regional localized capacity布局 (layout) have gradually been actualized, stabilizing its operational data. International leading manufacturers such as Aptiv and Valeo have also relied on in-vehicle intelligence-related businesses to cement their positions.

However, stabilizing their positions is not the ultimate objective for European giants, as they still confront the dual pressure of shrinking traditional fuel vehicle businesses and investments in electrification transformation.

The replacement of seats in the top 100 is no longer a mere substitution but a systemic reshaping of the traditional parts industry landscape by the forces of electrified, intelligent, and systematic industrial chains. CATL's ascent to the top three globally and the continuous decline of Magna and ZF clearly illustrate the head-on competition between old and new industrial drivers in the first tier.

CATL is not an isolated case. In this reshaping process, Chinese companies have emerged as the core force in the global supply chain reconstruction, leveraging their vast local market advantages, complete industrial ecosystem, and rapid technological iteration speed.

What is being reshaped is not merely a change in competitive rules but also the reconstruction of the relationship between whole vehicle manufacturers and suppliers. In the past, the roles of suppliers were distinctly delineated by tier-one, tier-two, and tier-three levels, with a stable pyramid-like division of labor system prevailing for years.

Now, it has begun to loosen. With the acceleration of software-hardware decoupling, in-depth platform development, and the embedding of AI capabilities, technology companies capable of providing full-stack solutions are genuinely reshaping the new relationship between whole vehicle manufacturers and suppliers.

The

From this prediction, the power landscape of the global automotive supply chain is being redrawn.

The paintbrush is in China's hands.

Note: Some images are sourced from the internet. If there is any infringement, please contact us for deletion.

-END-

-

![]()

OFILM Reports Colossal 460 Million Yuan Loss: Founder Quietly Shifts Focus to Optical Modules!

-

![]()

Yutong Optics and Zeiss Forge Partnership to Develop Quality Measurement System and Launch "Optical Communication Joint Measurement Class"

-

![]()

AutoNavi Revises Splash Screen Ads with Precision Amid Controversy

-

![]()

Unlicensed Vehicle Disputes: AutoNavi Ensnared in the Aggregation Model

-

![]()

Agent: The 'Hard Requirement' for Entering Core Enterprise Systems for the First Time

-

![]()

Global Auto Market Outlook: Sales Decline in China, US, and Europe, Chinese Exports Approach 10 Million

-

![]()

AI Pioneer Breaks Free from the 'Doldrums'

-

![]()

Valuation Exceeds $26 Billion! Three Chinese "Gold Medalists" Shake Up the AI Industry