Mocked as a 'Transitional Living Fossil', It Withstood the Toughest Half-Year in the 2026 Auto Market

07/10 2026

07/10 2026

418

418

Lead

Introduction

How dare you!

"(Recommending someone to) buy a Japanese hybrid in this day and age? How thick must one's information bubble be?"

In early June, a reader with an IP address from Jilin Province posted this comment in the comment section of an article titled "Without a Private Charging Pile, I Advise You Not to Buy a Pure Electric Vehicle," published by the author on C Dimensions.

First, let me clarify that there is no intention to single anyone out here. The comment is quoted at the beginning of the article purely out of astonishment—despite the main text thoroughly explaining the reasons for such a recommendation, it still could not withstand the wave of online fandom culture in this day and age, which extends from brands to models and even to basic powertrain forms.

Indeed, HEVs, or hybrid electric vehicles, can only be registered with blue license plates in China due to their inability to be externally charged. In the current context of the Chinese internet, their position is quite delicate. Some mock them as 'living fossils of transitional technology.' In previous years, Chinese domestic brands preferred to invest in plug-in hybrids and pure electric vehicles. As a result, HEVs seemed like orphaned technologies until the major market correction in 2026.

What's even more intriguing is the comment from the reader in Jilin. Their province experiences a frost-free period of 100-160 days annually, with winter temperatures of -25°C being the norm. In such extreme cold environments, the range of pure electric vehicles shrinks by 40%, and the fuel consumption of plug-in hybrids spikes from 5L to 8L when running low on battery—details often omitted when automakers tout CLTC range figures in their marketing. While they accused others of being trapped in an 'information bubble,' think backwards (reverse the perspective)—in a country spanning 35 latitudes from Mohe to Sanya, considering pure electric vehicles as the only answer for new energy vehicles, isn't that itself a manifestation of being deeply entrenched in an 'information bubble'?

Figure: In January 2024, Tesla owners spontaneously organized a trip to Northeast China for cold-weather challenges.

Their conclusion was that 'once you leave the city, you can recharge every 200km, so there's no issue of being stranded halfway.'

In fact, HEVs themselves haven't changed much in the past two years. What has changed is the group of people who had been swept up in the narrative of pure electric/plug-in hybrids for five years. They finally took a second look at the vehicle parked next to the gas station downstairs—a car that requires no plugging in, has low fuel consumption, and isn't afraid of cold temperatures.

This leads us to the following story—in the auto market of the first half of 2026, which can be described as 'dark,' there existed an inconspicuous yet unyielding curve.

01 The 'Mainstay' in the First Half of 2026

According to the statistical methodology of the China Passenger Car Association (CPCA), HEV models, which can only be registered with blue license plates, have long been classified under the broader category of 'traditional fuel passenger vehicles (including HEVs),' representing a niche within a niche. Coupled with the rapid development of new energy vehicles in China, such models are often overlooked.

However, upon closer inspection, this 'niche within a niche' has shown remarkable resilience in recent years—

Entering 2026, whether in terms of wholesale or retail, HEVs have held their ground while others have 'collapsed.'

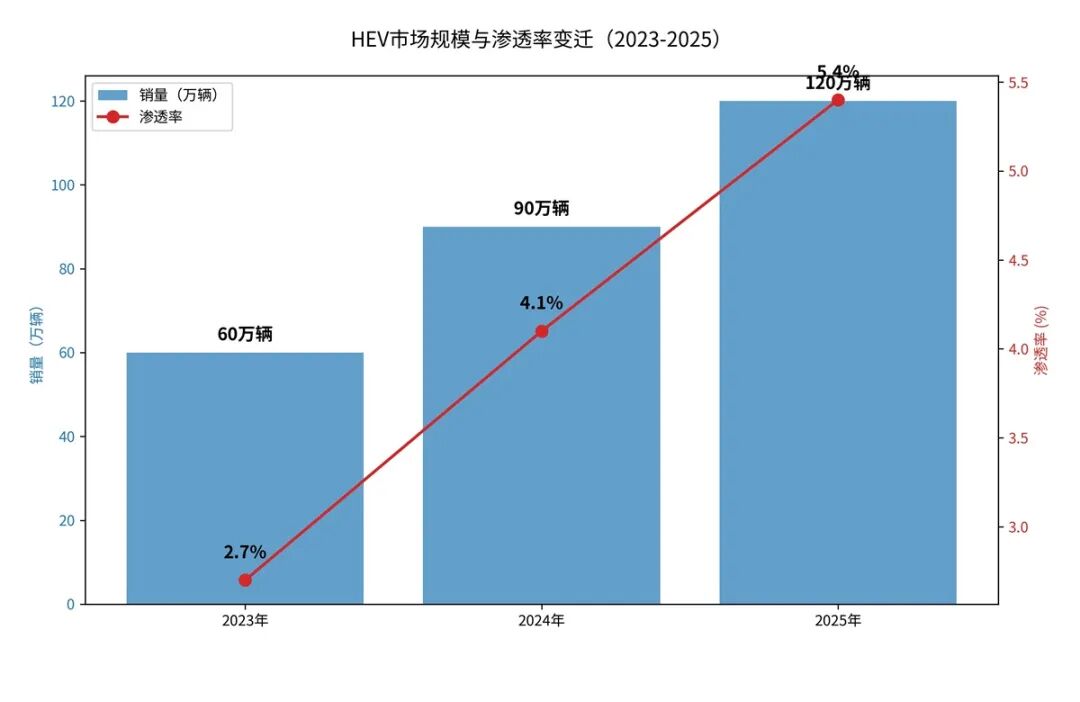

Let's first look at the wholesale data. In the first quarter of 2026, HEV wholesale volumes reached 218,400 units, up 2.7% year-on-year, making them the only category among the five major powertrain types (fuel, pure electric, plug-in hybrid, extended-range, and HEV) to achieve positive growth. From January to April, cumulative volumes reached 300,000 units, up 4.5% year-on-year. Do not underestimate this increase of less than 5%; during the same period, domestic passenger vehicle wholesale volumes fell 6.1% year-on-year, and even new energy vehicle wholesales declined by 1% year-on-year. Looking at January to May, domestic HEV wholesale volumes reached 392,000 units, with 92,000 units sold in May alone, up 26% year-on-year and 28% month-on-month, outpacing the growth rates of pure electric vehicles (16.6%) and narrowly defined plug-in hybrids (10.5%).

Some may question the reference value of wholesale data, arguing that it relies on export support and makes it difficult to gauge inventory levels at dealerships. So, let's turn to retail data, which paints an even starker picture. From January to May 2026, HEV retail volumes were approximately 360,000-380,000 units, down 4.5% year-on-year based on insurance registration figures; in May alone, retail volumes were around 77,000 units, down 10% year-on-year.

Figure: In fact, since 2023, domestic HEV models have been steadily growing in terms of sales and penetration rates, but the industry has been more focused on the development of new energy vehicle models.

Having presented these figures, some may point out—look, hasn't this also turned negative?

However, everything is relative. Under the same methodology, pure electric vehicle retail volumes from January to May were approximately 2.41 million units, down 8% year-on-year; narrowly defined plug-in hybrids reached 930,000 units, down 24% year-on-year; extended-range vehicles reached 380,000-400,000 units, down 25%-28% year-on-year. As for fuel vehicles, the situation was even more dire, with total domestic sales slightly exceeding 3 million units from January to May, down more than 35% year-on-year, according to different statistical sources.

Thus, among the five powertrain categories, HEVs experienced the smallest retail decline. While they did not increase, they held their ground amidst an overall collapse.

Currently, the CPCA has only released preliminary data for June, without separately breaking down HEVs. Official data is expected to be released in mid-to-late July. However, based on seasonal production patterns, it is estimated that HEV wholesale volumes in June were around 85,000-90,000 units, down slightly from May but still maintaining year-on-year growth of 15%-20%. Based on this, it is projected that domestic HEV wholesale volumes in the first half of 2026 were approximately 477,000-482,000 units, roughly flat to slightly up year-on-year compared to the 460,000-480,000 units in the same period of 2025.

Against the backdrop of a roughly 6% year-on-year decline in passenger vehicle wholesale volumes and a roughly 1% decline in new energy vehicle wholesales, HEVs can be considered the only blue-license-plate category that managed to 'hold firm' during this year's major market adjustment.

02 A Brief Analysis of Why HEVs Are Favored by the Market

Why have HEVs been able to 'hold firm'? The reasons stem from a combination of three layers of constraints, each closely tied to the unique characteristics of the Chinese market.

If we shift our gaze from the sleek office buildings in the Yangtze River Delta and Pearl River Delta to the vast expanse of the country, we will find that the resilience of HEVs is deeply rooted in the most authentic folds of this land.

China spans 35 latitudes from Mohe to Sanya, a geographical expanse that not only brings climatic differences but also creates vast disparities in energy replenishment environments. In Northeast, Northwest, and Qinghai-Tibet regions, the annual freezing period lasting four to five months is a nightmare for pure electric vehicles. In environments of minus twenty degrees Celsius, it is common for the claimed 500-kilometer range to be halved, with heat pump air conditioning efficiency plummeting or even failing entirely in extreme cold.

In the South, what plagues users is not temperature but more stubborn spatial constraints. In older residential communities such as those in Shanghai's Inner Ring or early commercial housing communities in Guangzhou, ambiguous parking space ownership and inadequate grid load are the norms. In such communities built over twenty years ago, the installation rate of private charging piles has long been low. Relevant surveys show that over 40% of households in China do not meet the conditions for installing private charging piles. For these users, purchasing a plug-in hybrid vehicle often means driving it purely as a fuel vehicle, making the ideal mode of 'commuting on electricity and traveling long distances on fuel' nearly unattainable.

Additionally, policy changes are also a major factor. If the steady development from 2023 to 2025 was still riding the wave of market growth dividends, then in 2026, amidst a market correction, policies such as the halving of new energy vehicle purchase taxes and the raising of pure electric range thresholds for plug-in hybrids played a crucial role.

The new GB 27999—2025 'Evaluation Methods and Indicators for Fuel Consumption of Passenger Vehicles,' which mandates a national average WLTC fuel consumption of 3.3L/100km for domestic automakers by 2030, has put significant pressure on vehicle manufacturers. After all, for companies unwilling to exit fuel vehicle production, relying solely on new energy vehicle models to 'subsidize' the compliance costs of fuel vehicles is too costly. HEVs, which can achieve fuel consumption of 3.5L/100km or even lower without external charging, provide a compliant pathway for companies intending to retain fuel vehicle models. This also explains why the notion of 'HEVs being a dignified exit for fuel vehicles' first gained traction on the industrial side.

The final layer is the rational return of users. With new energy vehicle penetration rates hovering around the 50% mark for nearly a year, user fatigue with 'mandatory charging' has become increasingly evident. HEVs are regaining attention at this time not because of any technological breakthroughs but because the competing options have been too 'noisy'—tired of the online fandom marketing rhetoric, ordinary consumers are yearning for a car that 'doesn't require me to understand the difference between WLTC and CLTC.'

It is precisely this double dilemma of North and South that has reshaped the value of HEVs. They require no dedicated charging piles and are unafraid of winter range shrinkage, returning to the essence of 'refuel and go.' This 'unfussy' trait is particularly precious in the context of the 2026 auto market correction.

03 The Gradual Rise of Domestic HEVs

If geography and infrastructure are the soil for HEVs' survival, then the collective shift of Chinese domestic brands has been the catalyst for their rise. For a long time, HEV strategic deployment by domestic automakers was often seen as a reluctant response to dual-credit policies or a cover for insufficient technological reserves in new energy vehicles.

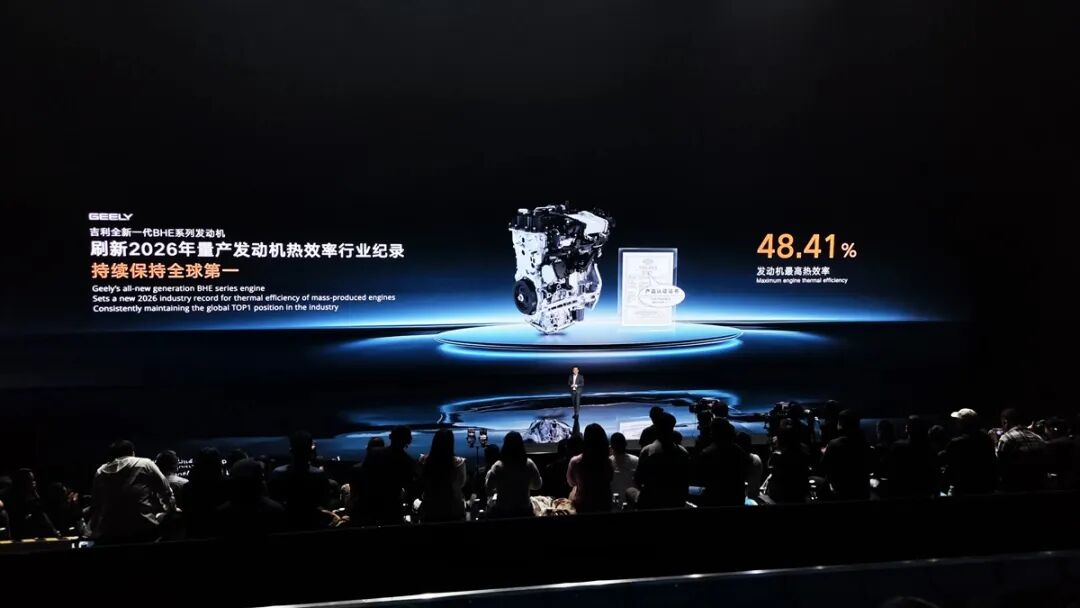

However, the winds have shifted in 2026. Toyota's core patents for the THS planetary gear system expired around 2023, dismantling the patent barriers. As a result, on this track, which has long been dominated by Japanese brands, domestic brands are gradually gaining a voice. Moreover, their breakthroughs are not solely reliant on expired Japanese patents.

Geely has been the most aggressive player in this wave. The Xingyue L i-HEV Smart Drive series, launched in late April this year, is equipped with a DHE15 dedicated engine boasting a thermal efficiency of 46.5%, surpassing Toyota's proud A25B series in parameters. More importantly, instead of following Toyota's planetary gear power-splitting architecture, it adopts a series-parallel DHT route that better suits Chinese driving habits—using electricity at low to medium speeds and fuel at high speeds, avoiding patent disputes while addressing the long-standing issues of high fuel consumption and significant noise during high-speed cruising in Toyota's THS system.

Changan and Chery are also quietly following suit. The former has equipped its mainstay models like the Eado with Blue Whale HEVs, more of a 'fuel vehicle HEV-ization' substitution strategy aimed at solidifying its base. Chery, on the other hand, has restarted an HEV branch within its mature Kunpeng powertrain system, attempting to regain its reputation for fuel efficiency through the Tiger sequence. Even GAC Trumpchi has built an HEV moat in the commercial and home market segments with models like the M8 MPV.

It is worth noting that the new generation of domestic HEVs has not repeated the mistakes of 'converting fuel vehicles to electric.' They insist on using nickel-metal hydride batteries or small-capacity ternary lithium batteries with better cold temperature resistance and employ software strategies to lock the battery charge within an efficient range, avoiding the early plight of plug-in hybrid models that 'become sluggish when low on battery.' Meanwhile, domestic HEVs are no longer fixated on single-handedly challenging the Japanese 'fuel-efficient king' label but have added quicker power responses and better cost control on top of 'fuel efficiency.'

Admittedly, we must be soberly aware that the so-called 'golden window' from 2026 to 2027 will not last long. It is more like a 'time substitution' to fill the gap before plug-in hybrid and pure electric technologies mature. Once solid-state battery technology achieves breakthroughs or 800V high-voltage fast-charging networks truly penetrate counties and even townships, resolving cold-weather degradation and range anxiety, the living space for HEVs will inevitably narrow further.

However, for the moment, for the millions of households living in older residential communities and commuting on icy roads, HEVs represent the lowest-cost path to electrification and their only realistic option. It has nothing to do with any earth-shattering technological revolution but is more like a silent substitution.

As the tide of market trends ebbs, it is the pragmatic consumers—those once overlooked by the fervent online fan culture—who have ultimately bolstered the sales volume of this market, reaching an impressive 1.2 million units. This phenomenon perhaps reveals the most genuine aspect of the Chinese auto market. While grand visions and lofty narratives hold significance, the ability to start a car's engine effortlessly on a frigid morning when temperatures plummet to minus thirty degrees is what truly resonates with consumers.

Editor-in-Chief: Li Sijia Editor: He Zengrong

THE END

-

![]()

Optical Communication and Robot Vision: OFILM’s Bold Transformation Amid a 460 Million Yuan Loss

-

![]()

OpenAI, Grok, and Meta Release Three Major Models: Who is the King of Cost-Effectiveness?

-

![]()

Momenta’s Backers in the Auto Industry Crave Blockbusters More Than Stock Dividends

-

![]()

China’s AI Computing Power: Embracing a New Organizational Paradigm

-

Same Bloodline, Two Fates: How Two AI Giants Took Divergent Paths?

-

![]()

Combined Market Value Plummets by Nearly One Trillion Yuan: What’s Behind the Decline of Two AI Powerhouses?

-

![]()

Detailed Explanation of the Impact of Hikvision Guanlan Coding on Video Quality and Key Frame Quality

-

![]()

The Key Distinctions Between AI-Driven Smart Coding and Traditional Coding