The Stock Competition Era Unveils the True Nature of All Brands

07/14 2026

07/14 2026

366

366

Lead

Introduction

In a downturn, strategic direction outweighs speed.

Warren Buffett famously remarked, "Only when the tide goes out do you discover who's been swimming naked." By mid-2026, many in the automotive sector can attest that the ebb has been thorough.

A decade ago, the Chinese auto market thrived on growth dividends, with talk of "overtaking on bends" prevalent. As the new energy vehicle (NEV) era dawned, all players were eager to seize the moment. Tesla and BYD surged ahead, while NIO, XPeng, and Li Auto became emblematic of the times.

It was an era of coexistence. Traditional fuel vehicles maintained their dominance, while NEVs carved out a growing market share. Joint venture brands remained relatively unscathed, and domestic brands were just beginning to gain traction. Few foresaw that more than half of the names on the leaderboard would be replaced within five years.

Fast forward to today, and the market has transitioned from growth to stagnation, and now to contraction. Many of the former high-flyers have now fallen back to earth. The Tesla myth has faded, the era of joint venture brand dominance has ended, new forces like Lingmi Hua have emerged, and BYD, Geely, Changan, Chery, and Great Wall remain at the forefront...

The sales trajectories of major automakers over the past few years have traced a clear path: from a flourishing market to a reshaped landscape, and now to dominance by a select few. Each stage has seen eliminations, with the pace quickening. By mid-2026, the elimination race has reached its most brutal phase.

01 The Elimination Race in the Era of Reshuffling

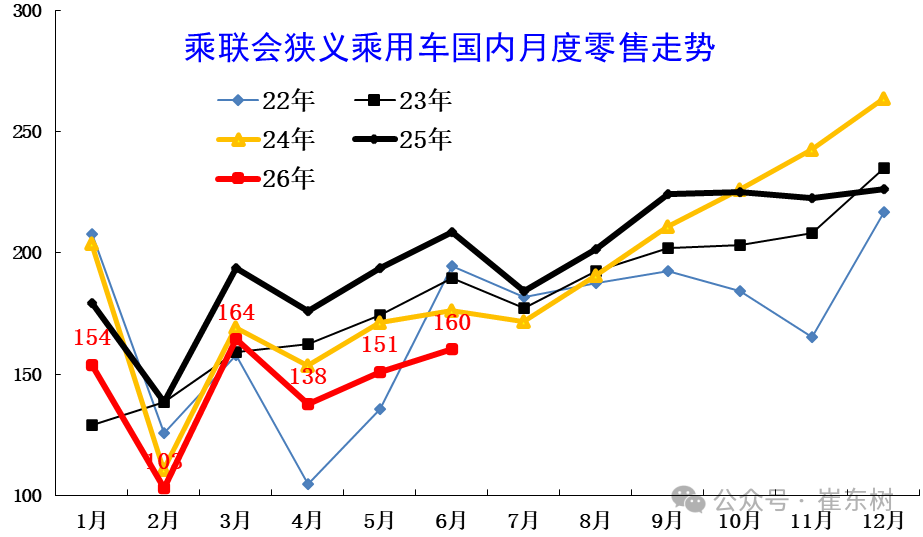

The Chinese auto market in the first half of 2026 can be characterized by two words: overall pressure, structural disintegration. Data from the China Association of Automobile Manufacturers (CAAM) shows domestic auto sales reached 9.921 million units, down 21.1% year-on-year. The China Passenger Car Association (CPCA) reported cumulative retail sales of passenger vehicles at 8.701 million units, a 20.2% decline.

The more than two million vehicles not sold domestically were offset entirely by exports, which reached 5.096 million units in the first half, up 65.3% year-on-year. Chen Shihua, Deputy Secretary-General of CAAM, bluntly stated, "Auto market sales in the first half were primarily driven by exports." The phrase "cold inside, hot outside" aptly summarizes the situation.

Furthermore, the fuel vehicle market has nearly collapsed, with domestic sales of traditional fuel passenger vehicles nearly halving in June. The penetration rate of the NEV market remains high, but growth has slowed significantly. In other words, NEVs are expanding at the expense of fuel vehicles declining even faster.

In this stock competition, joint venture brands are facing the toughest challenges. In June, retail sales of mainstream joint venture brands reached 330,000 units, down 34% year-on-year. Giants that once sold a million vehicles annually now struggle to surpass 50,000 units monthly. The decline stems from the rapid shrinkage of the fuel vehicle base and their inability to establish a foothold in the NEV market, leaving them caught in between.

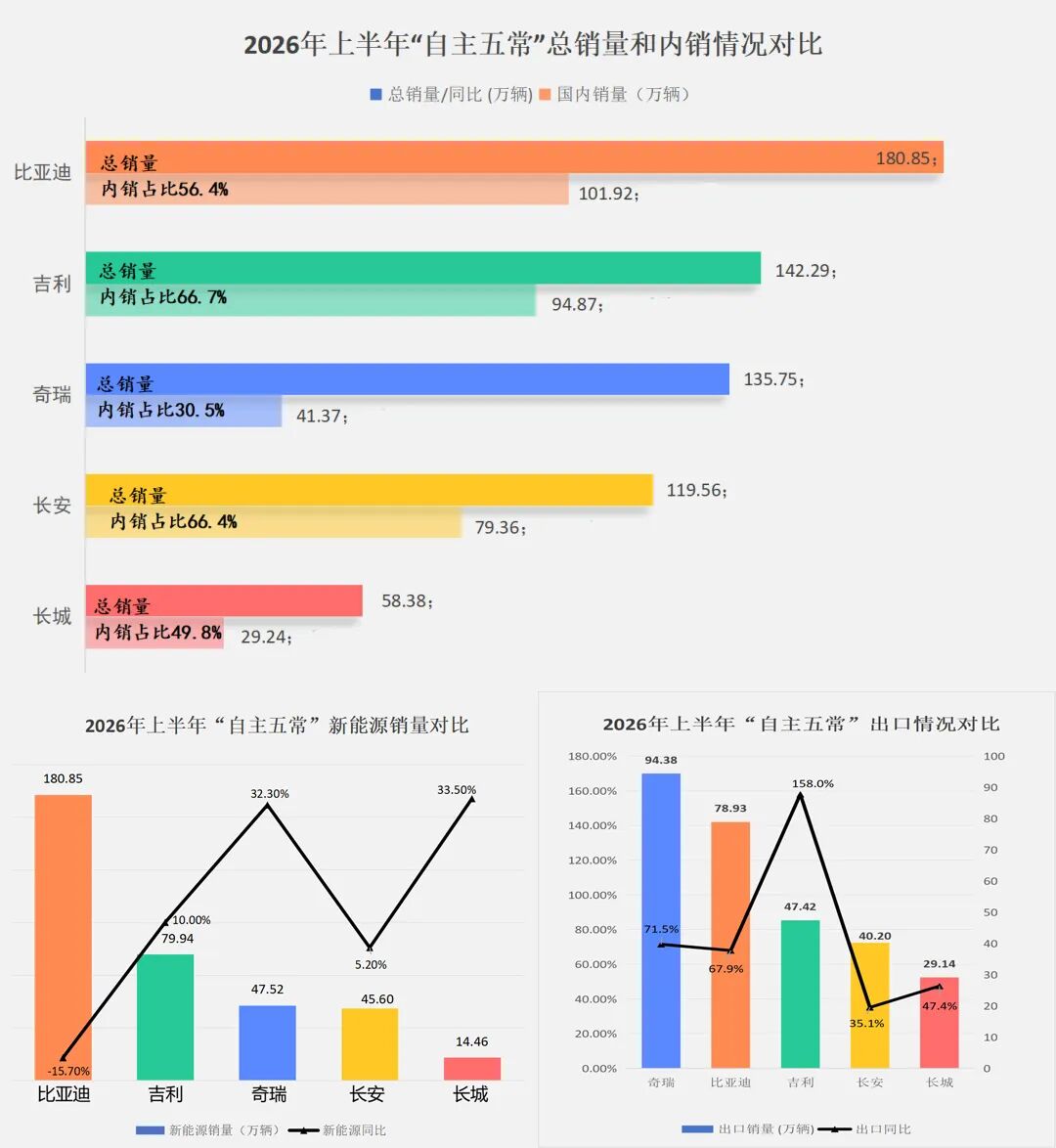

In contrast, domestic brands have emerged as the biggest winners. In June, Chinese brand passenger vehicles captured a 75.5% market share, the highest in nearly three years. Despite a market contraction of over 20%, BYD, Geely, Chery, and Changan maintained volumes at the million-unit level, indicating a widening gap within domestic brands.

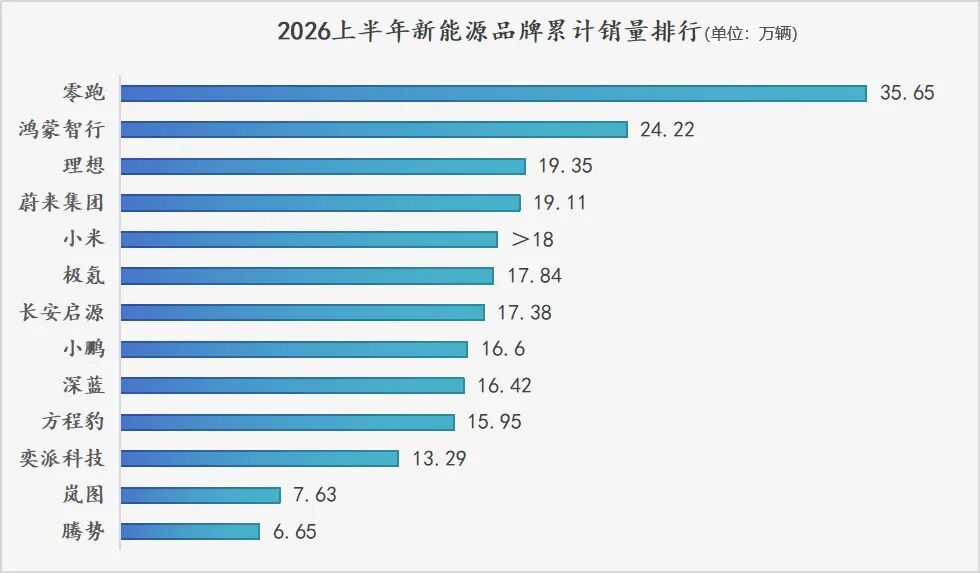

Internal differentiation is even more pronounced among new force automakers. The "NIO, XPeng, Li Auto, and Leapmotor" pattern has been completely rewritten. However, it's worth noting that none of the new force automakers have achieved an annual target completion rate exceeding 50%. Conversely, NEV brands incubated by traditional automakers, such as Zeekr, Changan Aito, and Seres, are rapidly catching up, competing on par with "NIO, XPeng, Li Auto," and Xiaomi.

In fact, most automakers, including BYD, Geely, Changan, and Chery, have an annual target completion rate below 50% in the first half. If this is the case for the top players, the situation for mid- and lower-tier brands is even more dire. This raises a question: should everyone continue to chase volume at all costs, or slow down to focus on qualitative development?

Cui Dongshu, Secretary-General of the CPCA, predicts that July will mark a watershed for the restructuring of auto market rules. The implementation of mandatory national safety standards for NEVs, combined with the expiration of the 2027 tax exemption policy for hybrid vehicle boat taxes, will introduce mandatory requirements for collision safety and battery "thermal runaway without fire." These measures will add thousands of yuan in cost per vehicle and significantly raise the technological bar.

In plain terms, costs will rise, and technological barriers will increase, further compressing the living space for small and medium-sized brands that rely on low prices and insufficient R&D investment. Li Bin, Chairman of NIO, aptly stated, "The Chinese auto industry has fully entered a cycle of stock replacement, which is a normal manifestation of industry maturity."

While a normal manifestation, not everyone will survive to see it. Stock replacement is a zero-sum game—one brand's gain is another's loss, with no middle ground. Brands hoping for a market recovery will likely be disappointed, as the recovery's benefits will not be evenly distributed.

The data from the first half of 2026 proves one thing: after the tide recedes, there are far more naked swimmers than imagined. Competition in the second half will only intensify. How deep will the price war go, and who will survive this round of elimination? These questions will be answered in six months. But one thing is certain: the era of surviving on wind and luck is over.

02 Strategies to Resist the Downturn at the Forefront

It's clear that the auto market situation in the first half of 2026 presents a stark conclusion: the market is shrinking, and only a few automakers are faring well. The dividends of the current industry's price war are fading, and simple price cuts and promotions cannot sustain growth. So, what have the risk-resistant brands done right? Different automakers have provided vastly different answers.

The first strategy is to go all-in on globalization. Leading domestic brands like BYD, Chery, Geely, and Changan have made overseas markets a core means of hedging against domestic contraction. The surge in export data in the first half illustrates this point. For example, Changan's overseas business now accounts for about 33.6% of total sales, with its Rayong plant in Thailand and Brazil plant going into operation. This is not an accidental outbreak by a single company but an inevitable trend of the entire Chinese auto industry chain exporting outward.

The second strategy is to deepen structural optimization in the domestic market, with some brands focusing on adjusting their product mix. For example, Changan, Geely, and Chery have all started to focus on the HEV sector this year, while Great Wall Motor adheres to the SUV and pickup truck segments. NIO expands its customer base through the Leapmotor and Firefly brands.

The third strategy is to continuously tackle frontier technologies. BYD's "Divine Eye," Geely's "Vast Expanse," and Changan's "Tianshu Intelligence" are all focusing on catching up in the field of intelligence. Huawei's Harmony Intelligent Mobility, Xiaomi, NIO, Li Auto, and XPeng continue to deepen their self-developed systems. These investments may not yield direct returns in the short term, but once technological barriers are established, they become the deepest moat.

There is also a fourth strategy: accelerating the pace of new product iterations to stimulate consumer desire through frequent launches. New force automakers and NEV brands incubated by traditional automakers are the quickest in this regard. For example, Leapmotor updates its product line every six months, with over 65% of core components self-developed and manufactured, forming a cost-effectiveness barrier in the 60,000 to 200,000 yuan price range, using extreme cost control to counter the cycle. Brands like Zeekr, Aito, and Seres also maintain a high frequency of new product launches, using freshness to combat market fatigue.

There is no one-size-fits-all answer to these strategies. An analyst's judgment hits the nail on the head: for automakers that simultaneously focus on both NEVs and overseas markets, growth space can still be found during a downturn. However, for brands with slow transformation rhythms and over-reliance on a single market, pressure is accumulating rapidly.

What truly tests automakers is not judgment but resolve. When market sentiment is at its most pessimistic, they can still advance long-term strategies according to a set rhythm rather than being led by short-term sales pressure. Companies that waver in their technological routes or frequently change their product plans are the most likely to lose their way amid cyclical fluctuations.

In the end, cycles always pass, but the premise is that you haven't lost your composure at the bottom of the cycle. By relying on their strengths and choosing suitable strategies, companies can navigate through the cycle towards better development in the next stage. That's why we've seen so many examples concentrated among traditional players like BYD, Geely, Changan, and Chery, as well as new force leaders like Leapmotor and Harmony Intelligent Mobility.

In fact, in the short term, these strategies may not bring explosive growth, but each is accumulating potential energy for the next cycle. When the tide rises again, those who persisted during the ebb will be the first to surface. So, at the bottom of the cycle, rhythm and direction matter more than speed.

Editor-in-Charge: Cao Jiadong Editor: He Zengrong

THE END

-

It's Time to Tally the ROI for Tokens

-

![]()

WPS, with 678 Million Users, Seeks Equilibrium Between Revenue Growth and User Experience

-

![]()

Seres, Once a Profit Leader, Shifts from Gains to Losses in H1: It’s Not Entirely Huawei’s Fault | MIRROR Pro

-

![]()

Why Google Remains 'Others' After 16 Years in the Smartphone Business

-

![]()

The Theory of Distillation Threat

-

![]()

Iterative Communication in Automotive Electronics: ADI's Innovative AB, GMSL, and EB Solutions

-

![]()

Despite AITO’s Explosive Sales, Why is Seres Still Struggling Financially?

-

![]()

For Seres, Losses Aren't the Toughest Challenge