India's New Energy Vehicle Dream: From Tata Leak to Tesla's Exit - A Closing Argument

07/14 2026

07/14 2026

446

446

Lead

Introduction

"What a bitterly cold winter."

In late June 2026, a notice from the dark web sent Cupertino and Palo Alto into a simultaneous panic. Tata Electronics, Apple's core manufacturing partner in India, had its internal network breached by the ransomware group WorldLeaks. Over 200,000 confidential files totaling 630GB were leaked online for anyone to download.

These included not just schematics for the iPhone18 Pro's motherboard, A20 Pro chip parameters, and camera module specifications, but also Apple's top-secret supplier lists—considered the crown jewels of its commercial confidentiality.

Yet beyond the mainstream media frenzy, Tata Group's unprecedented commercial breach also ensnared Tesla. The global new energy vehicle giant had entrusted numerous component design documents to Tata for manufacturing in recent years, which were now exposed alongside Apple's secrets.

On one side stood Apple, reeling from catastrophic leaks; on the other, Tesla, collateral damage in someone else's war. Two global tech titans had their most closely guarded secrets laid bare in a single hack.

Tata, India's largest conglomerate, had devoured Wistron's Indian iPhone factory in 2023, acquired 60% of Pegatron's India subsidiary in 2025, and was projected to produce 26% of global iPhones by 2026. Yet this company, hailed by Modi as the "face of Make in India," had exposed servers to the public internet, implemented shoddy permission isolation, and surrendered high-level accounts to phishing emails with trivial ease.

From the automotive industry's perspective, Tata's debacle becomes truly intriguing when viewed alongside several other concurrent developments.

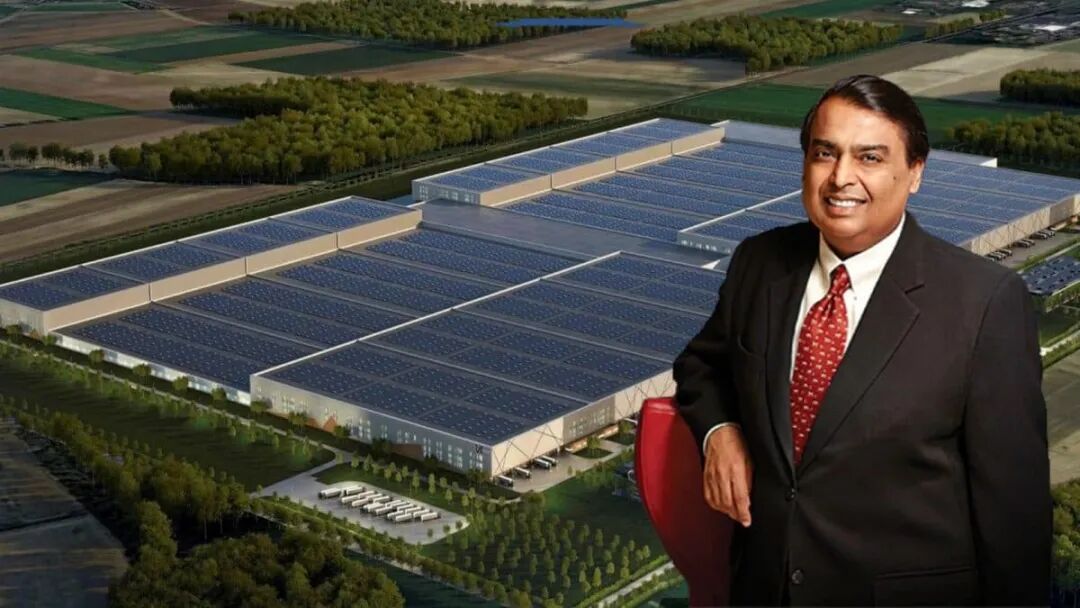

In the first half of 2026, Reliance Industries' power battery cell project in Jamnagar—dubbed "India's CATL"—finally collapsed. After three delays since 2021, its scheme to reverse-engineer Chinese equipment for technology transfer failed spectacularly. The fallback plan—scaling back from full vertical integration to importing finished cells from China for assembly—yielded just 1.4GWh annual capacity.

Figure: Reliance Group promotional image of its battery mega-factory in Jamnagar, Gujarat, featuring Chairman Mukesh Ambani

Reliance's failure symbolized far more than a single project's collapse. It reflected the systemic breakdown of India's five-year new energy vehicle industrial plan. In 2021, New Delhi had pledged₹181 billion (~$2 billion) for its PLI-ACC (Production-Linked Incentive for Advanced Chemistry Cell) program, aiming to establish 50GWh of domestic battery capacity within five years and create over 1 million upstream-downstream jobs.

By May 2026, total operational battery capacity in India—including imported cells for assembly—stood at a paltry 1.4GWh, achieving just 2.8% of the target. At 70kWh per electric vehicle, this would supply only 20,000 cars. Not surprisingly, Modi's promised subsidies remained largely unpaid.

After five years of negotiations, Tesla confirmed in May 2026 that its Indian "superfactory" plan was "permanently terminated," as stated by the Heavy Industries Minister himself.

With autonomous battery production in ruins, subsidies at zero, and industry leaders exiting, even Tata's tier-one manufacturing could expose unreleased products from Apple and Tesla simultaneously. Modi's 2017-announced Indian new energy vehicle plan had not just slowed by mid-2026—it had fundamentally collapsed.

01 Paper Ambitions vs. Crushing Reality

On March 31, 2024, New Delhi's Ministry of Heavy Industries prematurely terminated the FAMEⅡ subsidy program (Faster Adoption and Manufacturing of Electric VehiclesⅡ) 15 months ahead of schedule. This flagship ₹100 billion initiative, meant to catalyze India's electric vehicle revolution with hard cash, ended not with industrial prosperity but regulatory chaos.

The program collapsed amid investigations into Hero Electric, Benling India, and other leading firms for allegedly defrauding nearly ₹3 billion in subsidies. The abrupt closure epitomized India's new energy vehicle policy: grand beginnings, ignominious endings.

Since 2016, India had woven an elaborate policy web to catch the global decarbonization wave. From demand-side FAME incentives to manufacturing-side Production-Linked Incentive (PLI) schemes, and the SPMEPCI (Scheme for Promotion of Manufacturing of Electric Passenger Vehicles in India) to attract foreign investment, its toolkit rivaled any manufacturing powerhouse. Yet the gap between policy white papers and execution revealed a different story—a grand narrative systematically unraveling.

Reliance's battery debacle, as noted earlier, stemmed directly from the PLI program. By late 2025, not a single rupee of the promised subsidies had been disbursed. Beyond Reliance's wasted investments in rusting equipment, the root problem lay in the initial bid winners: aside from energy giants like Reliance, the roster included battery novices like Ola Electric (e-scooters) and Rajesh Exports (gold trading). By prioritizing local content over technical merit, the Review Rules (evaluation criteria) excluded established foreign battery makers, reducing "battery self-reliance" to mere rhetoric.

If the battery plan faltered from overreach, the SPMEPCI vehicle manufacturing scheme repelled foreign investors through sheer adversarial design.

Intended to lure Tesla, BYD, and others with tariff reductions, the program demanded $500 million minimum investment, escalating localization rates, and 3% penalties for non-compliance. This "kill-the-pig" approach, compounded by India's notorious retrospective taxation and capricious foreign investment reviews, guaranteed failure.

Figure: Persistence Market Research's 2016 forecast of India's new energy vehicle market trends over 15 years.

Frankly speaking, viewed through today's lens, this resembles wishful thinking more than serious market analysis.

When the application window closed on October 21, 2025, zero applications had been received. India's "market-for-technology" gambit had failed. BYD had exploratory (tentatively) proposed a $1 billion CKD assembly plant for 100,000 vehicles annually in 2023, but Indian authorities rejected CKD models, demanding full supply chain relocation. BYD withdrew, preferring to pay steep tariffs rather than surrender control.

Tesla similarly abandoned factory plans, opting to test the market with high-priced imports. On treat (dealing with) India, both Chinese and American EV giants reached identical conclusions.

Policy chaos immediately impacted consumers. While PM E-DRIVE (India's national EV program) extended subsidies to 2028, it slashed per-vehicle incentives by half and capped two-wheeler allocations at 2.48 million units. This crippled Ola Electric, once hyped by SoftBank and Indian media as a revolutionary "new force" in car manufacturing. Now mired in quality complaints, with over 95% of its showrooms shuttered for lacking licenses, Ola's sales plummeted. Its plight mirrored the entire sector: without core technologies, local assemblers cannot survive subsidy cuts and supply chain gaps.

Today, Indian streets roar with combustion engines. Despite official rhetoric about "30% EV penetration by 2030," passenger EV adoption lingers at 4%, with a 235:1 vehicle-to-charger ratio. From FAME II's premature death to PLI-ACC's barren outcomes and SPMEPCI's rejection, India's new energy strategy is trapped in a vicious cycle: high tariffs protect infant industries but cripple supply chains; foreign technology is desired but foreign investors are distrusted.

The policy drums keep beating, but all India has to show are half-built factory shells. This gamble has failed completely.

02 The Protectionism-Dependency Paradox

India's new energy strategy didn't fail due to a single misstep—it was strangled at birth by structural contradictions that reinforced each other.

The first knot: the delusion of "de-Sinicizing" supply chains.

Indian policymakers understood clearly: EVs' core lies not in vehicles but in the "three electrics" (battery, motor, control) systems, nearly all dominated by Chinese suppliers. From PLI-ACC to PM E-DRIVE's DVA (Domestic Value Addition) requirements, the unspoken logic was transparent—use China's cost-effective supply chain to boost penetration, but deny Chinese firms profits.

The calculation proved self-defeating.

India imports 75% of its lithium batteries and over 60% of electric motor magnetic materials from China. Without Chinese imports, only Japan and South Korea remain options, leaving local battery production at 12% (PACK only) and motor control below 8%. Meanwhile, after India rejected BYD's $1 billion joint venture and stalled executive (executive) visas, tax authorities slapped $64 million in "transfer pricing" penalties. BYD responded by exporting finished vehicles and paying 100% tariffs—yet still sold 5,400 units in India during 2025, 15 times Tesla's volume. Refusing factories while paying tariffs sent a clear message.

The PLI-ACC evaluation process became farcical. With few qualified bidders, lead-acid battery suppliers Exide and Amara Raja were eliminated, leaving aside from Reliance only two-wheeler maker Ola Electric and gold exporter Rajesh Exports.

Figure: Ola Electric, a PLI-ACC participant, primarily makes electric two-wheelers. Its involvement resembles NIU announcing plans to build lithium battery factories in China today—a notion everyone would dismiss as absurd. Especially since Rajesh Exports trades gold...

The second knot: the "fatten-then-slaughter" investment model that fooled no one by 2026.

SPMEPCI's design logic was quintessentially Indian: investors must first spend $500 million on factories, then achieve 25% localization within three years and 50% within five years to qualify for 15% tariff discounts (from 70–110%) on vehicles above $35,000. But annual quotas were capped at 8,000 units, with local sales targets of ₹50 billion by Year 4 and ₹75 billion by Year 5—failing which, 3% penalties applied.

Commercial negotiations often involve extreme opening positions. But Musk, who had negotiated with Indian officials for five years since 2021, balked at the sequence: India demanded factory construction before tariff cuts; Tesla insisted on testing market viability first. By 2026, Musk walked away.

India's reputation as a "foreign enterprise graveyard" due to retrospective taxes—epitomized by the Vodafone case—had already bankrupted its credibility among automakers. Ford had been burned before. When applications closed on October 21, 2025, not a single global automaker applied, despite Hyundai, Kia, Mercedes, and Volkswagen having conducted due diligence. All expressed "interest," but none submitted bids.

The third knot: policy instability harmed domestic players too.

Some argue foreign firms avoid India due to fear of exploitation. The truth is, India exploits everyone equally—including local companies.

FAME II, initially a three-year, ₹100 billion flagship program, slashed per-kWh subsidies from ₹15,000 to ₹10,000 in May 2023, then terminated it entirely on March 31, 2024—15 months early. Though officials claimed a successor (PM E-DRIVE) would launch, its 2028 deadline came with halved two-wheeler subsidies (₹5,000) and a 2.48 million-unit cap. L5 three-wheeler quotas exhausted by December 2025.

The cost of frequent policy changes is that the local model Ola Electric is first affected by its own subsidy rules. Due to a sudden reduction in subsidies, sales have also plummeted. Desperate, Ola Electric attempted to circumvent the FAME subsidy cap, only to be caught and ordered to repay 1.42 billion rupees. Further investigations revealed that over 95% of its showrooms across India lacked basic business licenses, resulting in vehicles being seized by state transportation authorities.

Ola Electric, which underwent a major purge, saw its stock price plummet, and its CTO, CMO, and CBO announced their collective resignations. An Indian new force nurtured by policy resources suffered the most when the policy took a sudden turn.

The final knot is that the market and infrastructure cannot support the slogan of 'achieving 30% by 2030.'

India's per capita GDP remains around $2,500, with a thin middle-class pool capable of affording EVs priced at $35,000. PM E-DRIVE's move to introduce subsidies for two-wheelers priced below 150,000 rupees (currently equivalent to less than $1,600) indicates that the main market is for affordable two-wheelers, not advanced four-wheeled passenger vehicles. With a vehicle-to-charging-pile ratio of 235:1 and only about 26,000 public charging piles nationwide, it lags behind even a county-level city in eastern China.

When we consider these four knots together, it becomes clear that India's new energy strategy has been self-defeating from the outset—

It attempts to use high tariffs to keep foreign companies out and force them to build factories, but the local supply chain cannot support it;

It restricts foreign investment to force an increase in domestic value addition (DVA), but this further strains the supply chain;

It throws money to boost the local supply chain, but the evaluation process eliminates experienced players in favor of novices;

It frequently changes subsidy policies to control finances, but this backfires on the newly supported models.

Each move is self-contradictory, and even its schemes to trap others are carried out openly and impatiently.

03 The Tragedy of India's Industry

Looking at the bigger picture, the collapse of India's new energy sector is not just a result of isolated industrial policy mistakes but is deeply tied to its approach toward foreign investment over the years.

Leaving aside older cases like Vodafone, in the past decade alone, Xiaomi faced tax recover (tax recovery), Vivo was investigated, Ford was hit with retroactive fines, and Tesla's negotiations stalled for five years—India's reputation as a 'foreign enterprise graveyard' is well-known, not just a black joke or meme. As a result, during the 2024-25 fiscal year, when the global economy was generally declining, India's manufacturing sector saw a 96.5% plunge in net foreign direct investment inflows, even experiencing a net outflow of $616 million.

Trying to seize the 'China + 1' position, only to see foreign investors take a look and leave: high tariff walls, unattainable subsidies, constant risk of fines, and poor infrastructure—why bother?

But don't just laugh at this. The logic behind such reckless behavior lies in India's chronic current account deficit. As a net importer of both energy and electronics, India burns through foreign exchange on crude oil, gold, and electronic components every year, putting long-term pressure on the rupee and keeping foreign reserves tight. Modi's 2017 call for 'fully electric by 2030' was half slogan, half a genuine attempt to cut crude oil import bills—a fiscal necessity.

The problem is that cutting oil bills requires the ability to manufacture batteries and the three core electric vehicle components (battery, motor, and electronic control system). Otherwise, it merely replaces oil imports with battery cell imports, failing to save money. As a result, between 2021 and 2025, India's lithium imports surged by 921%, cobalt by 85%, with zero local battery-grade lithium refining capacity and 95% of core materials reliant on China. This is hardly energy security; it's transferring control from oil-producing nations to a presumed 'ultimate rival.'

Looking at the attitudes of two types of companies toward India further reflects this: Apple's shift of production to India was a politically motivated decision rather than a purely commercial one, resulting first in a 38 billion rupee fine warning from the CCI based on global turnover, followed by Tata leaking confidential information online...

In contrast, Tesla's approach was purely commercial. The Indian market was not a must-have, so it simply walked away when things didn't work out.

India's mistake does not lie in setting unrealistic goals or adopting an extreme industrial policy mix of 'tariff walls + massive subsidies + connections with tycoons + sloganeering for political gain' under a simplistic view. Rather, it stems from the immense distributional pressures on its limited resources due to its massive population within a narrow landmass, as well as the historical debts accumulated since the Mughal Empire and East India Company eras.

In contrast, China's rise in the new energy sector never relied on a single genius document or a tycoon's flash of inspiration. From social governance and education popularization in the first three decades after 1949, to taking on global electronics contract manufacturing in the 1990s, to the 'Ten Cities, Thousand Vehicles' demonstration program in 2009, and later the dual-credit policy and full-industry-chain subsidies after 2015—China's new energy vehicle industry stands on foundations built by previous generations. Over 30 years, amid skepticism and subsidy fraud crackdowns, China has gradually mastered battery cathodes, anodes, separators, electrolytes, and even upstream lithium mining and refining. Behind this lies stable policy expectations, an open competitive environment, and a rule-of-law bottom line (bottom line) that treats private and foreign enterprises equally.

In 2026, Tata's servers are wide open, Reliance's battery cell factory has shrunk back to a PACK integration workshop, and Tesla's footprint has been erased from the doorstep. The Modi government's attempt to leapfrog the necessary accumulation period of industrialization through administrative means has only built castles on sand. When 'Made in India' becomes a global laughingstock and foreign investors vote with their feet, leaving behind a mess, what the country truly loses is not just a few factories or billions of rupees in foreign investment but its fragile credibility and precious time. What began as an ambitious dream of building a car industry has turned into a harsh lesson in the laws of development.

For a country that hasn't even laid the foundation, all the shortcuts taken in industrial policy will only lead to a dead end.

Editor-in-Charge: Cao Jiadong Editor: He Zengrong

THE END

-

It's Time to Tally the ROI for Tokens

-

![]()

WPS, with 678 Million Users, Seeks Equilibrium Between Revenue Growth and User Experience

-

![]()

Seres, Once a Profit Leader, Shifts from Gains to Losses in H1: It’s Not Entirely Huawei’s Fault | MIRROR Pro

-

![]()

Why Google Remains 'Others' After 16 Years in the Smartphone Business

-

![]()

The Theory of Distillation Threat

-

![]()

Iterative Communication in Automotive Electronics: ADI's Innovative AB, GMSL, and EB Solutions

-

![]()

Despite AITO’s Explosive Sales, Why is Seres Still Struggling Financially?

-

![]()

For Seres, Losses Aren't the Toughest Challenge