Seres' 'Profit Predicament' and Zhang Xinghai's 'Strategic Calm'

07/14 2026

07/14 2026

341

341

On the evening of July 12th, a bolt from the blue struck the new energy vehicle (NEV) sector.

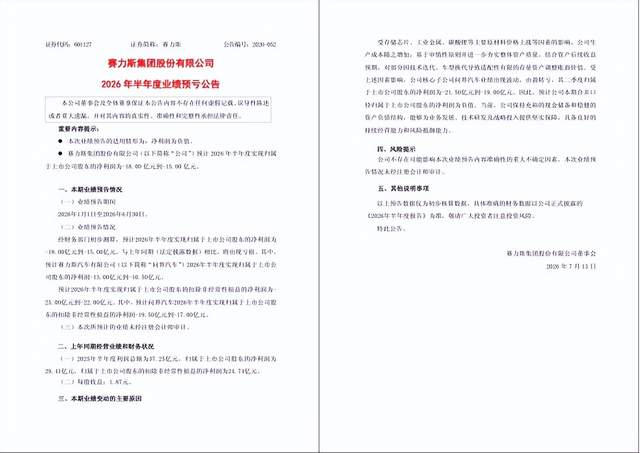

Seres disclosed that it anticipates a net loss attributable to shareholders of listed companies between 1.5 billion yuan and 1.8 billion yuan for the first half of 2026. Its main subsidiary, Aito Automotive, is expected to suffer a loss of 1.05 billion yuan to 1.3 billion yuan during the same period, becoming the main contributor to the losses.

Before this article was finalized, Seres' A-share stock price had nosedived from its annual peak of around 130 yuan to 53.9 yuan. This once-glorified star automaker, hailed by the market as the 'flagship of the Huawei ecosystem,' is now grappling with growing pains.

Performance 'Reversal': Core Business Struggling

Indications of Seres' mid-year losses were apparent in its first-quarter financial statement.

Summarizing this report in one sentence: 'Sales and revenue rose, but profits stagnated.' In the first quarter of this year, Seres sold 78,500 NEVs, marking a 43.9% year-on-year increase, with revenue reaching 25.746 billion yuan, up 34.46% year-on-year.

However, Seres' net profit attributable to shareholders for the period was merely 754 million yuan, a slight uptick of 0.89% compared to the same period last year. Net profit excluding non-recurring items was just 103 million yuan, a substantial decrease of 73.87% year-on-year.

Vehicle sales were robust, yet profits remained thin. Moreover, due to support from state-owned shareholders, over 650 million yuan of the 754 million yuan net profit in the first quarter came from non-recurring gains like government subsidies. If these 'extra earnings' were excluded, Seres' profitability in its core vehicle manufacturing business would seem feeble.

A significant surge in R&D investment was the primary cause of the profit squeeze. R&D expenses in the first quarter reached 1.794 billion yuan, a 70.68% year-on-year increase. The additional 743 million yuan in expenses nearly wiped out the quarter's profits. These funds were mainly invested in the independent development of the three electric systems (battery, motor, and electronic control), vehicle development, and new ventures such as robotics, aiming to lessen reliance on Huawei.

Continued high-intensity R&D also brings pressure from asset impairment. The NEV industry is evolving rapidly, with technological updates occurring frequently, leading to major upgrades roughly every two years. The production line equipment previously invested in by Seres may not be fully utilized and currently can only be written down.

At this juncture, the rationale behind Seres' losses is evident. There was virtually no profit in the first quarter, and pressure persisted in the second quarter, resulting in an unfavorable performance in the first half of the year.

Zhang Xinghai's 'Cost Dilemma': Pressure from Both Sides

Seres' increased R&D investment can be viewed as a proactive strategic decision. However, the dual pressure from upstream and downstream industries poses a passive challenge.

In June, at the China Automobile Chongqing Forum, Zhang Xinghai, Chairman of Seres Group, raised the alarm by revealing a staggering cost breakdown.

On the upstream side of the industry, prices of core raw materials and components have soared. Zhang mentioned that the unit price of memory chips procured by Seres recently jumped from 20 yuan to nearly 100 yuan, a fivefold increase. The price of lithium carbonate, a key material for power batteries, also rose from 80,000 yuan per ton last year to around 180,000 yuan per ton.

On the downstream side, the price war in the automotive market has intensified, with terminal selling prices continuing to decline. Zhang stated at the forum that while material costs have risen, new car prices have continued to drop, posing a significant challenge for vehicle manufacturers. Data from the China Association of Automobile Manufacturers also indicates that the average transaction price of domestic NEV passenger vehicles in the first half of this year decreased by 6.2% year-on-year.

The domestic automotive market is now in a phase of market share competition, and relying on price cuts to boost sales has become commonplace. While Seres' Aito series has not implemented significant official price cuts, it has offered discounts through rights upgrades and product refreshes.

A more daunting issue is Seres' high proportion of fixed expenses, which exacerbates the squeezing effect in the current industry environment. In Seres' production costs per vehicle, core components such as Huawei's intelligent driving solutions, HarmonyOS cockpit systems, and core hardware procurement constitute a significant fixed expense.

When the NEV market was still expanding, Seres' product premiums could serve as a buffer. However, once the industry enters a price war and terminal prices plummet, these fixed costs may erode the company's profitability.

Deep Integration with Huawei: A 'Double-Edged Sword'

The pressure from industry cycles upstream and downstream is a common challenge in the automotive industry. However, Seres' current loss magnitude is more pronounced than most of its peers, with the core difference lying in its 'Smart Selection' cooperation model with Huawei.

As the industry transitions from incremental competition to market share battles, the vulnerabilities of this model for automakers are exposed.

Seres lacks strong bargaining power and cannot reduce costs internally. Its core business areas, such as driving assistance, the three electric systems, and brand marketing, are highly dependent on Huawei. According to Seres' Hong Kong IPO prospectus, its procurement from Huawei in the first half of 2025 will be approximately 20 billion yuan, roughly accounting for 30% of its revenue for the period.

Unlike BYD, which has full control over its supply chain, Seres has little say in its cooperation with Huawei and thus lacks cost-setting power. When raw material prices rise, the company cannot rely on internal measures to reduce costs.

Secondly, the hefty 'Huawei tax' compresses profit margins. Based on Seres' procurement data from Huawei in previous financial reports, an analysis post on the Snowball platform suggests that Huawei may charge Seres a comprehensive fee equivalent to 10% of the vehicle's selling price, with 2% for technology licensing and 8% for channel services.

If this fee is real and unaffected by raw material price hikes or terminal price cuts, it could significantly impact Seres' vehicle gross margins.

A long-term concern is Seres' lack of brand independence. Consumers perceive Aito's brand influence as primarily reliant on Huawei, with Seres having a weaker presence. This misperception means that brand value is largely attributed to Huawei, while Seres bears most of the heavy asset risks of manufacturing.

Moreover, as Huawei adjusts its cooperation approach and introduces new partner brands, if Huawei's resource allocation changes, Seres' supply chain security may face uncertainty.

Zhang Xinghai's Aces: Cash, R&D, and Overseas Expansion

Despite its losses, Chairman Zhang Xinghai is not passive. Leveraging previous accumulations and proactive measures, Seres still has aces to navigate cyclical fluctuations.

The most solid foundation comes from its ample cash reserves. By the end of the first quarter of 2026, Seres' monetary funds and trading financial assets totaled over 30 billion yuan. With these funds, even if the current loss scale continues, the company has sufficient resources to support strategic investments for several years.

Aggressive R&D catch-up is a more critical strategic move. Seres' 2025 annual report shows that its annual R&D investment reached 12.51 billion yuan, with over 9,000 R&D personnel. This R&D intensity ranks among the highest among independent Chinese automakers, positioning Seres to gradually reduce its external dependencies in production.

The primary focus of R&D investment is to address technological shortcomings and reduce reliance on Huawei's ecosystem. In the short term, this proactive R&D spending will squeeze profits, but in the long run, independent development of core technologies is essential.

Seres is also divesting its previous inefficient assets. Its wholly-owned subsidiary, Lantech, sold only 20,400 vehicles last year, a year-on-year decrease of 48.36%, which somewhat undermined investor confidence. In May this year, Lantech completed a capital increase and share expansion, transforming into Saidou Technology, with Seres' shareholding reduced to approximately 32.96%, thus lowering the asset's risk profile.

Finally, Seres is gradually advancing diversification and overseas expansion. In overseas markets, it is exploring Southeast Asia, the Middle East, Europe, and other regions, leveraging its cost-effectiveness to open up new growth spaces. In new business areas, the company is continuously investing in cutting-edge fields such as intelligent robots and Robo-taxis.

As Zhang Xinghai said, building a car is like running a marathon. The test in mid-2026 may be just the first hurdle in this marathon. Fortunately, Seres still has stamina and the opportunity to adjust its pace. Whether it can successfully complete the race remains to be seen, and time will tell the answer.

-

It's Time to Tally the ROI for Tokens

-

![]()

WPS, with 678 Million Users, Seeks Equilibrium Between Revenue Growth and User Experience

-

![]()

Seres, Once a Profit Leader, Shifts from Gains to Losses in H1: It’s Not Entirely Huawei’s Fault | MIRROR Pro

-

![]()

Why Google Remains 'Others' After 16 Years in the Smartphone Business

-

![]()

The Theory of Distillation Threat

-

![]()

Iterative Communication in Automotive Electronics: ADI's Innovative AB, GMSL, and EB Solutions

-

![]()

Despite AITO’s Explosive Sales, Why is Seres Still Struggling Financially?

-

![]()

For Seres, Losses Aren't the Toughest Challenge