Volkswagen Implements Drastic Measures for a Strategic Rebirth

07/14 2026

07/14 2026

472

472

Recently, Volkswagen Group unveiled a sweeping retrenchment plan that takes immediate effect. According to reports, Volkswagen Group is set to streamline its model lineup across all brands by up to 50%, retaining only those products that cater to the "most attractive market segments." For the models that remain, the range of available configurations will also undergo a significant reduction, by as much as 75%.

At present, the production of the Volkswagen Touareg and Touran has ceased; the Audi A1 and Q2 are no longer available for purchase; and the Porsche 718 Boxster and Cayman were discontinued in October of the previous year. Concurrently, Volkswagen aims to scale down its global annual production capacity from 12 million vehicles to 9 million vehicles, slashing production by 3 million vehicles in one fell swoop.

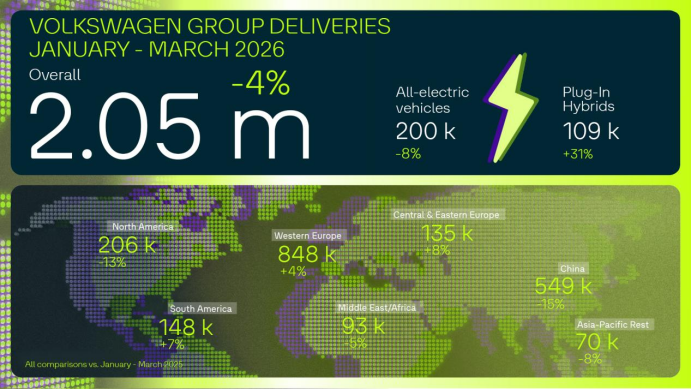

In fact, the roots of this round of retrenchment plans can be traced back to earlier signs. The financial report for the first quarter of 2026 revealed that Volkswagen's revenue stood at €75.7 billion, marking a year-on-year decrease of approximately 2.5%. Its operating profit was around €2.463 billion, with the operating profit margin dipping to 3.3%. During the first quarter, Volkswagen sold roughly 2 million vehicles, a year-on-year decline of 7%. Global deliveries amounted to about 2.049 million vehicles, representing a year-on-year decrease of 4%. The persistent profit decline has compelled Volkswagen to take decisive action on its product lines and production capacity, striving to arrest the downward profit trend by streamlining products and reducing capacity. Additionally, Volkswagen intends to lay off up to 100,000 employees worldwide to further trim costs.

From a regional market perspective, Volkswagen's first-quarter market delivery performance exhibited notable divergence. Deliveries in the South American market rose by 3% year-on-year; the European market experienced a 1% growth; the Central and Eastern European market saw a 7% increase. However, the Chinese market witnessed a 20% year-on-year decline, and the North American market dropped by 13.3% year-on-year.

Among these, the decline in Volkswagen's global core market—the Chinese market—was particularly striking. In the first quarter of 2026, FAW-Volkswagen sold 318,200 vehicles, a year-on-year decrease of 12.8%. SAIC Volkswagen sold 189,900 vehicles, marking a year-on-year decline of 16.75%. The sales downturn at both FAW-Volkswagen and SAIC Volkswagen led to a drop in Volkswagen's overall sales in China from 644,100 vehicles in the first quarter of 2025 to 548,000 vehicles in the same period in 2026, a year-on-year decrease of nearly 15%. This sales slump was also mirrored in profits. In 2014, Volkswagen's profit contribution from China was as high as €5.2 billion, accounting for nearly 30% of the group's global profits. By 2025, it had plummeted to €958 million. Over the past decade, the Chinese market's profit contribution to Volkswagen has dwindled from nearly 30% to just around 10%.

Behind the sales and profit losses, the Chinese automotive market is undergoing profound transformations. The penetration rate of the new energy vehicle market has surpassed 63%, eroding the market position of fuel vehicles and making Volkswagen's situation in China more challenging than anticipated. Volkswagen's former scale advantage has now become its biggest liability. It is reported that Volkswagen Group encompasses multiple brands, including Volkswagen, Audi, and Porsche, with a plethora of inefficient models that fail to contribute to profits. Overcapacity is also prevalent, with some domestic factories operating at low capacity utilization rates and experiencing relatively pronounced issues of idle capacity.

Simultaneously, new energy and local premium brands continue to capture market share, while Volkswagen's electric transformation has been sluggish, with only 9,400 pure electric vehicle sales in the first quarter. In terms of intelligence, the gap between Volkswagen and local brands has become glaring, with shortcomings that are difficult to rectify in the short term. This implies that Volkswagen's situation in China is far from rosy.

Besides the Chinese market, Volkswagen's performance in the North American market is also far from optimistic. In the North American market, Volkswagen's market performance is under pressure primarily due to factors such as the policy environment and consumer demand. In the first quarter of 2026, Volkswagen delivered 205,500 vehicles in the North American market, a year-on-year decrease of 13.3%, with the U.S. market experiencing a 20.5% decline, mainly impacted by the U.S. imposing an additional 25% tariff on imported complete vehicles. In recent years, U.S. automotive policies have gradually favored domestic manufacturing, with imported models facing higher cost pressures, further escalating the operating costs for overseas automakers like Volkswagen.

At the same time, the development pace of the U.S. electric vehicle market has fallen short of automakers' expectations. In 2025, pure electric vehicle sales in the U.S. accounted for about 7.4% of new vehicle sales, down from 8.1% in 2024, indicating relatively slow growth in the electric vehicle market. In this environment, Volkswagen's ID series models also face significant pressure in the U.S. market. Taking the Volkswagen ID.4 model as an example, its sales in 2025 were 22,400 vehicles, while in the first quarter of 2026, only 338 vehicles were sold, a year-on-year plunge of 95.6%. Another electric model, the ID.Buzz, also underperformed, leading Volkswagen to revise its product planning for the U.S. market and not introduce the 2026 ID.Buzz in the U.S.

Compared to the North American market, Volkswagen's performance in the European market is relatively commendable, but its past advantages in the traditional fuel vehicle sector are also being called into question. In the first quarter of this year, Volkswagen Group delivered 983,800 vehicles in the European market, a year-on-year increase of 4.7%, with growth observed in the German, Western European, and Central and Eastern European markets, indicating that Volkswagen still retains certain market advantages in Europe.

In the past, Volkswagen dominated the European market with fuel vehicle models such as the Golf, Passat, and Tiguan. However, with the advent of new energy vehicles, the growth prospects for the fuel vehicle market are continuously shrinking, and Volkswagen's original competitive edges are also being undermined. In the first quarter of this year, the market share of pure electric vehicles in the EU has risen to 19%. At the same time, Chinese automakers are accelerating their foray into the European market, continuously enhancing their competitiveness in Europe with cost advantages and new energy technology prowess. Faced with intensified competition in the European market and the encroachment from Chinese brands, Volkswagen's transformation path in the European market remains fraught with challenges.

However, Volkswagen was not oblivious to the impending electric transformation wave; it merely adopted an overly "aggressive" approach during the transformation process. Around 2016, it embarked on the electric transformation journey, aiming to become the world's largest electric vehicle manufacturer by 2025. To this end, Volkswagen invested over €35 billion to construct the MEB pure electric platform—the first dedicated platform developed by Volkswagen for producing pure electric vehicles. Simultaneously, approximately €20 billion was invested in Volkswagen's software subsidiary, CARIAD. But a decade later, Volkswagen finds itself in an even more precarious position. The first model on the MEB platform, the ID.3, was unveiled as early as 2019 but did not enter the Chinese market until 2021 due to software glitches, a full two years later. The platform itself has also failed to keep pace with the domestic competitive landscape: adopting a 400V voltage architecture with a maximum charging power of 125kW, it has already lagged behind in the Chinese market where 800V ultra-fast charging is gradually becoming the norm.

Volkswagen is not alone in paying the price for past aggressive strategies; automakers like Toyota and Honda are also feeling the heat. Around 2021, Honda took the lead in proposing the goal of completely halting sales of fuel vehicles by 2040, planning to invest ¥10 trillion in pure electric vehicles. Toyota set a goal of selling 1.5 million pure electric models by 2026, attempting to swiftly catch up with the transformation pace. However, neither automaker has achieved success as planned. Honda incurred its first net loss since going public in the 2025 fiscal year, forcing it to abandon the "fuel ban" goal and urgently halt multiple pure electric projects. Toyota also significantly lowered its sales expectations for pure electric models to 800,000 vehicles, with the bZ series performing poorly in the market.

Nevertheless, automakers that have encountered setbacks are also actively recalibrating their development strategies. For Volkswagen, it is accelerating its technological collaboration with Chinese partners. It fully embraces the CEA electronic and electrical architecture jointly developed with XPENG, which will be equipped on all pure electric models in China starting in 2026. The first model based on this architecture, the "Zony 07," has already been launched, with a starting price of ¥109,900, and over 40,000 orders have been secured at stores. Subsequent models, the Zony 09 and the FAW-Volkswagen ID. AURA T6, are slated for launch in the second half of the year. It is reported that more than 20 new energy models will be introduced in China in 2026, expanding to about 50 by 2030, including approximately 30 pure electric models.

Of course, Volkswagen's overseas markets are also undergoing strategic adjustments. In the European market, Volkswagen is, for the first time, evaluating the introduction of models such as the China-developed extended-range SUV ID.Era 9X for production in Europe, while focusing on the entry-level electric vehicle market, with plans to launch the ID. Polo and ID. Cross based on the MEB+ platform in 2026. In the North American market, it will adopt Rivian's software technology, planning to deliver off-road electric pickups and SUVs in 2028. Additionally, Volkswagen plans to set its global production capacity and sales target at approximately 9 million vehicles by 2026. Whether this goal can be realized remains to be seen by the market.

(Image sourced from the internet, removed if infringing)

-

It's Time to Tally the ROI for Tokens

-

![]()

WPS, with 678 Million Users, Seeks Equilibrium Between Revenue Growth and User Experience

-

![]()

Seres, Once a Profit Leader, Shifts from Gains to Losses in H1: It’s Not Entirely Huawei’s Fault | MIRROR Pro

-

![]()

Why Google Remains 'Others' After 16 Years in the Smartphone Business

-

![]()

The Theory of Distillation Threat

-

![]()

Iterative Communication in Automotive Electronics: ADI's Innovative AB, GMSL, and EB Solutions

-

![]()

Despite AITO’s Explosive Sales, Why is Seres Still Struggling Financially?

-

![]()

For Seres, Losses Aren't the Toughest Challenge