Plummeting to Limit Down? Don’t Just Blame Seres—It’s a Sector-Wide Profit Meltdown

07/14 2026

07/14 2026

341

341

Industry Pressure Ripple Effect

Author|Wang Lei

Editor|Qin Zhangyong

Today, Seres opened at its limit down.

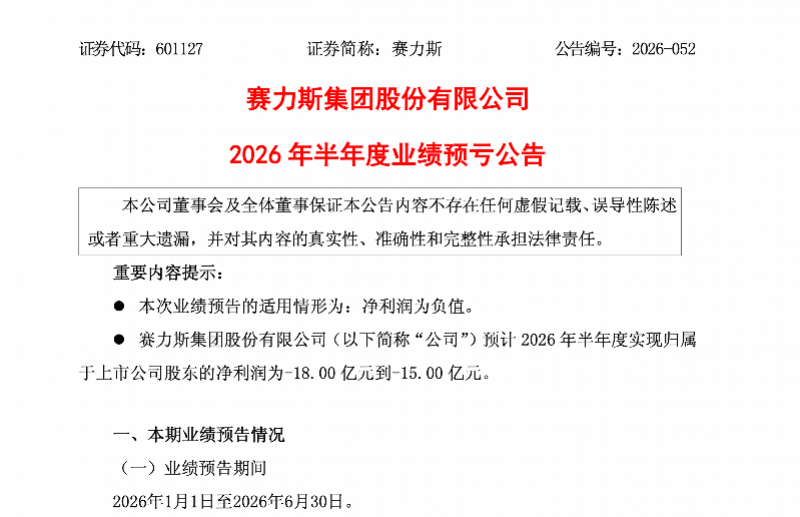

As of press time, the stock closed at RMB 53.91, down 10%, marking a new low since February 2024, with a market capitalization of RMB 93.91 billion.

The catalyst for the stock price decline was the announcement of a projected performance loss for the first half of the year: The net profit attributable to shareholders for the first half of 2026 is expected to range between -RMB 1.8 billion and -RMB 1.5 billion.

The announcement of such a significant projected loss sent shockwaves through the market.

It’s crucial to note that during the same period last year, Seres reported a net profit of RMB 2.941 billion. The nearly RMB 4.8 billion swing from profit to loss is no small feat for any company, let alone Seres, which was once lauded as an "industry turnaround exemplar."

However, Seres' shift from profitability to losses is not an isolated incident.

A glance across the entire industry reveals a widespread collapse in profits.

Wei Jianjun recently disclosed that their small electric vehicles, selling over 20,000 units monthly, incur a loss of RMB 13,000 per unit, resulting in a monthly loss of RMB 260 million for that segment alone. Tesla's situation is even more dire. According to a recent statistic from Nikkei Asia, Tesla's profit per vehicle has plummeted by 40%, from RMB 557,000 in the previous fiscal year to RMB 348,000 (approximately USD 2,150), nearing Toyota's level.

Therefore, Seres' interim report must be viewed within this broader context.

01 Sales Have Actually Grown

Seres was genuinely profitable in the first half of last year:

In the first half of 2025, Seres' total revenue reached RMB 62.402 billion, a 4% year-on-year decline, but net profit surged by 81.03% to RMB 2.941 billion, with a comprehensive gross profit margin of 28.93% and profit per vehicle rising to RMB 16,000, firmly placing it at the industry's top tier.

At the beginning of the year, investment banks widely predicted that Seres' annual profit would exceed RMB 10 billion, expressing optimism about its business model. Even in May this year, based on market conditions, investment banks updated their forecasts, still projecting annual profits of over RMB 5 billion.

However, today's announcement has completely shattered this confidence. Seres expects a net loss attributable to shareholders of RMB 1.5 billion to RMB 1.8 billion for the first half of the year, with a net loss after non-recurring items as high as RMB 2.2 billion to RMB 2.5 billion. According to the announcement, Seres is losing over RMB 8,000 per vehicle.

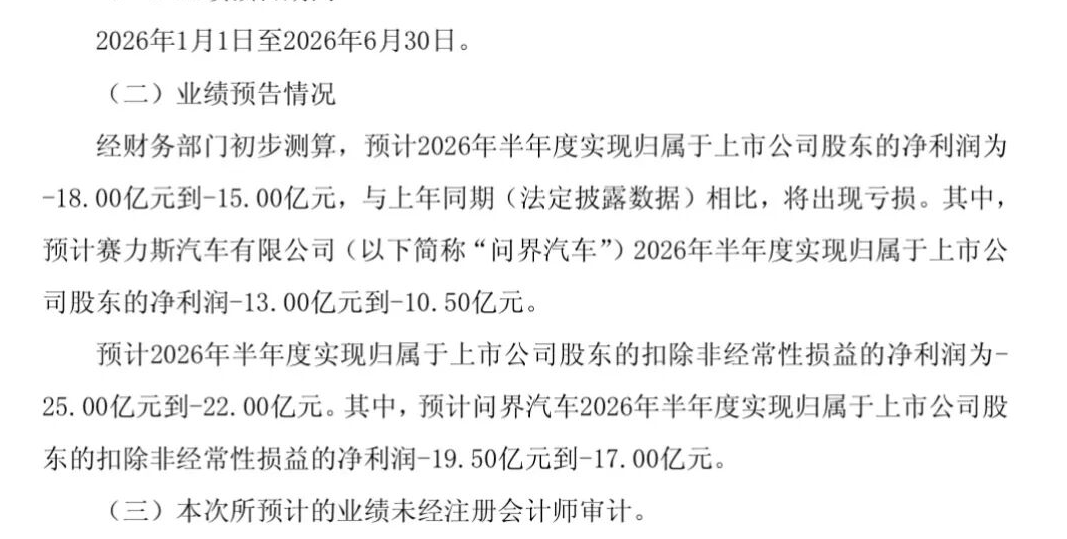

Regarding the projected performance loss, Seres primarily attributed it to rising production costs due to increases in the prices of major raw materials such as memory chips, industrial metals, and lithium carbonate, as well as adjustments to the book value of existing assets.

Breaking it down by quarter, the performance is more revealing. According to Seres' first-quarter financial report released not long ago, it was still profitable by RMB 750 million. Combined with the projected loss range for the first half of the year, this implies that Seres' net loss for the second quarter is expected to reach RMB 2.2 billion to RMB 2.5 billion.

In just one quarter, profits have plummeted by over RMB 3 billion sequentially, with a sudden downward turn in profitability, effectively erasing all profits from the first half of last year in a single quarter.

AITO, Seres' core subsidiary, is the direct point of loss. The announcement shows that the net loss attributable to shareholders for the first half of the year is expected to be RMB 1.05 billion to RMB 1.3 billion, becoming the primary source of loss for the listed company. After non-recurring items, the net loss reaches RMB 1.7 billion to RMB 1.95 billion.

Even so, the announcement emphasizes that Seres still maintains ample cash reserves and a robust balance sheet structure, providing solid support for business development, technological research and development, and strategic investments, with good sustainable operation capabilities and risk resistance.

The most perplexing aspect is that this loss is not due to a collapse in sales. From a sales perspective, Seres has actually experienced counter-trend growth amid an overall industry decline.

Data shows that in June 2026, Seres' new energy vehicle sales reached 33,700 units, a 26.94% year-on-year decline; however, sales of core Seres vehicles (AITO series) were 30,300 units, a 30.19% year-on-year decline.

Looking at the longer term, overall sales for the first half of the year have increased. In the first half of 2026, Seres' cumulative new energy vehicle sales reached 178,800 units, a 3.87% year-on-year increase; cumulative sales of the Seres AITO series reached 160,800 units, a 5.60% year-on-year increase. The M9 delivered over 10,000 units in just three weeks, and the M6 sold over 30,000 units within 54 days of its launch.

Against the backdrop of a more than 20% decline in domestic passenger vehicle retail sales in the first half of this year, these figures are certainly commendable.

Sales have not declined, and have even slightly increased, yet profits have completely collapsed, indicating a severe deterioration in the cost-profit model per vehicle.

02 Dual Pressures

In its announcement, Seres also pointed out that the core contradiction of "increasing revenue without increasing profit" lies in the uncontrolled rise in costs, primarily covering two major aspects.

Firstly, influenced by factors such as rising prices of major raw materials like memory chips, industrial metals, and lithium carbonate, the company's production costs have increased.

Secondly, based on the principle of prudence and to further consolidate overall asset quality, combined with expectations of future asset returns, adjustments have been made to the book value of certain existing assets with limited adaptability due to technological iterations and model updates.

In simpler terms, the soaring prices of upstream raw materials have directly led to an increase in costs per vehicle, and with no change in market prices, the profit margin per vehicle has been squeezed.

Indeed, since the beginning of this year, the surge in raw material prices has become a challenge faced by the entire automotive industry.

In June this year, Zhang Xinghai, Chairman of Seres Group, stated at the 2026 China Automotive Chongqing Forum that current vehicle manufacturers face numerous challenges, with the greatest being the fivefold increase in memory chip prices; meanwhile, the price of lithium carbonate has risen from RMB 80,000 per ton in the same period last year to RMB 180,000 per ton today.

He also mentioned that as a result, the average manufacturing cost per AITO vehicle has increased by RMB 15,000 to RMB 20,000, with 168,200 AITO vehicles delivered in the first half of the year. The increase in raw material prices alone has cost an additional RMB 2.9 billion.

Under such circumstances, Seres is not the first A-share vehicle manufacturer to announce a projected loss. Not long ago, GAC Group and JAC Motors sequentially released their own projected loss announcements.

Secondly, there is the impairment of existing assets. Due to model upgrades and iterations, old platform molds and outdated supporting production lines cannot meet the production standards of new models, instantly becoming a burden on the books. The one-time write-down of these old assets is also a major factor in the collapse of profits.

Such non-operational book losses do not represent a complete loss of the company's ability to generate revenue from its daily vehicle sales business, but they do significantly lower the current net profit.

This recalls the popular internet meme of "25 models in 30 months," where frequent technological iterations also imply significant financial consequences from the write-down of old assets.

03 There's Also a Hidden Factor

One cut to gross profit margins and one cut to assets—these two factors combined resulted in Seres incurring a loss of RMB 2.2 billion to RMB 2.5 billion in the second quarter.

However, the reasons stated on the books are just the surface. There may be a hidden factor that Seres did not mention in its announcement: the cost of its high degree of integration with Huawei.

On the profit side, Seres has to pay significant fees to Huawei, such as technology licensing fees. Additionally, in terms of hardware, according to public data, from 2022 to the first half of 2025, Seres has paid a cumulative procurement fee of RMB 75 billion to Huawei. Based on sales volume during the same period, approximately RMB 136,000 per vehicle goes to Huawei.

This model can function when gross profit margins are high and sales growth is rapid. However, once the profit model per vehicle deteriorates, raw material prices rise, and terminal competition intensifies, driving up costs, hidden pressures will also surface.

Furthermore, within the entire HarmonyOS ecosystem, internal competition for AITO is intensifying, and the "Huawei halo" is beginning to dilute. Two years ago, AITO was the sole focus of HarmonyOS Intelligent Connected Vehicles, enjoying the full support of Huawei's resources.

However, today, the situation is completely different. New brands with "boundary" in their names are making successive appearances, and the "Jing series" successors are also preparing to enter the market, with Huawei's resources being continuously diluted.

As Huawei replicates its cooperation model with Seres to more vehicle manufacturers, and as everyone becomes a "Huawei ecosystem partner," Seres' advantages are naturally being diluted.

04 The Thinning Profit Margins of the Industry

According to data from Cui Dongshu, Secretary-General of the China Passenger Car Association, from January to May 2026, revenue in the automotive industry increased by 1.4% year-on-year, but costs rose by 2.3%, outpacing revenue growth and leading to a 20% year-on-year decline in profits.

From January to May this year, the profit of China's automotive industry was RMB 144 billion, with a profit margin of 3.4%, lower than the average of 6.1% in downstream industries.

It’s important to note that around 2020, the profit margin of China's domestic automotive industry could still be maintained at 6%-8%. In just a few years, it has been halved. This figure is even lower than that of the home appliance industry (around 5.2%) and is approaching the level of traditional manufacturing.

Previously, vehicle manufacturing was high-tech and high-profit; now, it increasingly resembles an advanced assembly plant.

BYD, through extreme cost control and economies of scale, has managed to keep its profit per vehicle at a few thousand RMB, representing the industry's ceiling. Most other new forces are still struggling to avoid selling each vehicle at a loss.

Seres' loss of RMB 1.5 billion to RMB 1.8 billion is essentially an individual case of the 3.4% average industry profit margin erupting. Fortunately, Seres has not exhausted all its options. Cumulative deliveries of the AITO series reached 160,000 units in the first half of the year, still showing year-on-year growth, indicating that market recognition of the product itself remains strong.

Furthermore, the AITO M9 has established a relatively stable position in the RMB 500,000 price range, and the M6 is rapidly increasing in sales volume. The gross profit margins of these two models are theoretically much thicker than those of lower-end models. As long as the sales proportion of these two models stabilizes, there is an opportunity to reverse the situation of losses per vehicle, with the key being whether Seres can navigate the dual pressures of costs and cycles.

-

It's Time to Tally the ROI for Tokens

-

![]()

WPS, with 678 Million Users, Seeks Equilibrium Between Revenue Growth and User Experience

-

![]()

Seres, Once a Profit Leader, Shifts from Gains to Losses in H1: It’s Not Entirely Huawei’s Fault | MIRROR Pro

-

![]()

Why Google Remains 'Others' After 16 Years in the Smartphone Business

-

![]()

The Theory of Distillation Threat

-

![]()

Iterative Communication in Automotive Electronics: ADI's Innovative AB, GMSL, and EB Solutions

-

![]()

Despite AITO’s Explosive Sales, Why is Seres Still Struggling Financially?

-

![]()

For Seres, Losses Aren't the Toughest Challenge