"Miracles Stem from Great Efforts": Will This Continue in 2025?

01/14 2025

01/14 2025

748

748

Introduction

Do the auto market's trade-in programs and equal rights for oil and electric vehicles indicate a need for salvation?

"Rising and falling/Coming and going/Life and death/Eternal tides!"

In "A Study of History," Toynbee quotes Goethe's poem "Faust," paying tribute to scholars who inspire powerful forces through intense ideological conflicts. Goethe's confession encapsulates the rhythm of life's cyclic nature.

For the auto market, which recently concluded the "fierce competition" of 2024 and encountered "unprecedented changes," ideological conflicts and internal and external struggles were undeniably intense. However, this has also spurred the formidable endogenous strength of Chinese brands.

"Market competition in 2025 will undoubtedly intensify. I even boldly predict that the price war will ignite in January." He Xiaopeng, CEO of Xpeng Motors, recently reiterated his stance.

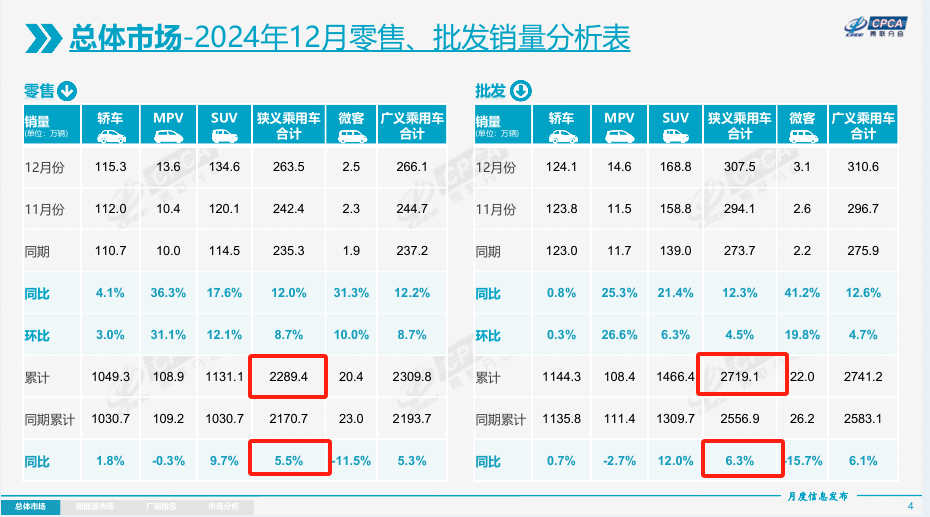

Unfortunately, He Xiaopeng's prediction materialized. Yet, when crunching the numbers, sales in the "extremely competitive" auto market of 2024 actually surged significantly. Data from the China Passenger Car Association (CPCA) reveals that wholesale sales reached 27.191 million units.

One factor largely overlooked is that, apart from the halved vehicle purchase tax policy, no other policy in the automotive industry has served as a vital engine for stimulating domestic demand and promoting consumption like the 2024 "trade-in" policy.

Furthermore, the "equal rights for oil and electric vehicles" discussed throughout the year prompts us to revisit the question: It's 2025 now; why does the auto market still need policy rescues?

Policy: "Miracles Stem from Great Efforts"

For the auto market in 2024, whether you like it or not, "fierce competition" was the name of the game.

However, the auto market kicked off the fourth quarter on a high note, evident from the sales of pure electric vehicles in October. Many vehicles set all-time sales records, particularly entry-level or around 100,000 yuan pure electric vehicles.

The continuous release of car purchase demand kept the auto market hot in the subsequent two months, with auto production and sales continuing to grow year-on-year, and monthly production and sales hitting record highs.

According to CPCA data, 2.941 million and 3.075 million vehicles were produced and sold in December, respectively, up 9.7% and 12.3% year-on-year. From January to December, 26.848 million and 27.191 million vehicles were produced and sold, respectively, up 5.0% and 6.3% year-on-year.

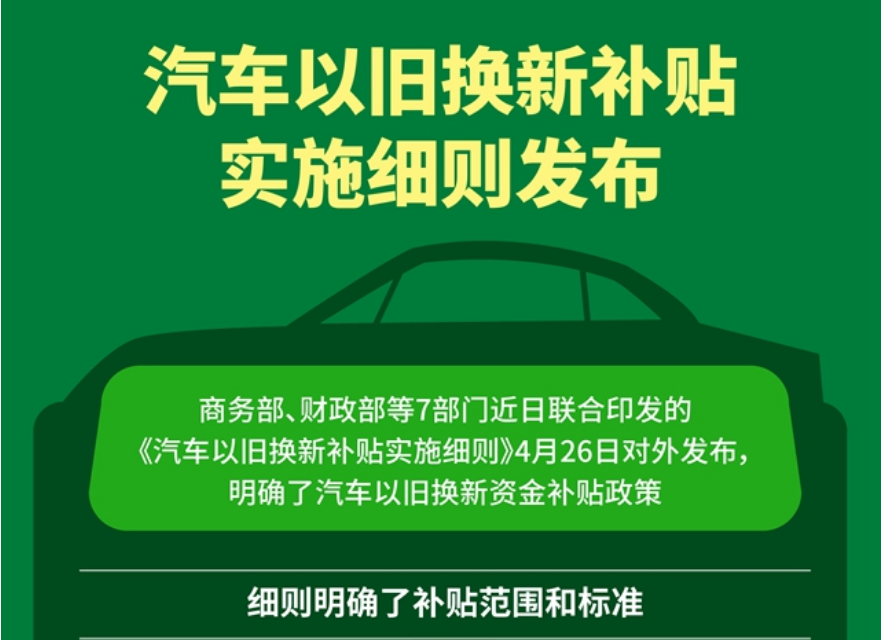

The "trade-in" policy, implemented only in April, continued with a new round of subsidies for trade-ins of up to 20,000 yuan in August. By December 13, it had driven passenger vehicle sales of over 5.2 million units, meaning over 5.2 million car owners realized their dream of driving new cars. Among them, over 2.51 million vehicles were scrapped and replaced, and over 2.72 million were replaced. The policy played a monumental role in incentivizing sales.

This policy, the "Detailed Rules for the Implementation of Car Trade-in Subsidies" issued by the Ministry of Commerce and six other departments in April last year, stipulated subsidies of 10,000 yuan and 7,000 yuan for the scrapping and purchase of new energy vehicles/fuel vehicles, respectively. However, the initial effect was modest. By the end of June, the trade-in information platform had received fewer than 200,000 applications for vehicle scrapping and replacement subsidies.

However, after the Ministry of Commerce and six other departments issued the "Notice on Further Improving the Work of Car Trade-ins" on August 16, increasing subsidies to 20,000 yuan and 15,000 yuan, it seemed to open the floodgates.

At a press conference in October, Li Gang, Director of the Department of Consumption Promotion of the Ministry of Commerce, stated that the national car trade-in information platform had achieved "one-stop processing" of vehicle scrapping and replacement subsidy applications. The cumulative number of access users exceeded 50 million, with over 330 million visits. More than 2.3 million consumers planning to apply for subsidies completed registration on the platform.

Now, car trade-ins have driven passenger vehicle sales of over 6.5 million units. This was announced by Zhao Chenxin, Deputy Director of the National Development and Reform Commission, at the regular briefing on State Council policies held by the State Council Information Office on January 8.

Additionally, the domestic market penetration rate of new energy passenger vehicles has surpassed 50% for seven consecutive months since June last year, with domestic retail sales reaching 11 million units throughout the year.

By shifting subsidies from the production end to the consumption end, with national and local rewards stacked up, a 100,000 yuan new energy vehicle can be discounted by 30%. For a pure electric microcar, which may originally cost 30,000 to 40,000 yuan, with some subsidies, it feels like "it's free." This is a significant temptation for potential consumers who might change their minds over a 2,000 yuan price difference, fueling the explosive growth of pure electric vehicles.

In the October rankings, seven of the top ten models were entry-level cars priced around 100,000 yuan or less. Among the top 40 pure electric vehicles, six "spicy fish head" models entered the list. The fourth-quarter data is not yet out, but the retail market may exceed many people's expectations, including the penetration rate of new energy vehicles, and the stimulus effect on consumption is evident.

Furthermore, according to a survey by the China Automobile Dealers Association, nearly 90% of dealers believe that the "trade-in" policy has had a significant effect, and dealers' new car inventories have continued to decline.

Combining another set of data, in November last year, China's auto dealer inventory warning index was 51.8%, down 8.6% year-on-year. It is clear that the "trade-in" policy has played a significant role in alleviating and supporting the tottering dealer system.

The issue is that industry insiders have observed that the trade-in policy primarily benefits models priced at 100,000 yuan and below. For some models that should have been phased out, this is more akin to a revival of assistance. Therefore, the CEO of a joint venture brand also called for and suggested that the "trade-in" subsidy policy should be implemented according to the proportion of the car price and the maximum limit, which would be more reasonable.

Additionally, if subsidy policies continue this year, how long can this inherent overdraft in the auto market last?

"Hyundai sold over 6 million vehicles globally in 2023, but its profitability was very high. Last year, our entire auto industry had a profit of 60 billion yuan, but there was a lot of water in it, as well as a large amount of state subsidies. International evaluation agencies definitely gave low scores to Chinese cars," Wei Jianjun, Chairman of Great Wall Motors, compared the role of price wars and subsidies.

According to data disclosed by Hyundai Motor Group, its net profit in 2023 reached 12.27 trillion Korean won (approximately 66.0126 billion yuan), up 53.7% year-on-year. The profit of one enterprise is equivalent to the profit of our entire industry. This account truly needs careful scrutiny.

We know that the money for "trade-ins" comes from the 1 trillion yuan ultra-long-term treasury bonds issued by the Ministry of Finance. With state endorsement, future money is spent today, of course, considering the auto industry from the perspective of the overall economic situation. That is, although automobiles only account for 6% of the national economy, their importance in driving the economy exceeds this proportion.

From a macro perspective, Europe and the United States have adopted a defensive approach towards China's new energy sector, and the impact will tend to be long-term. To hedge against this impact and expand domestic demand, it also means that the subsidy intensity will not be reduced and is expected to continue at least until the end of 2025.

However, for the auto industry, which has been engaged in price wars for two years, will more continued policies and new policies bring greater market increments?

"Equal Rights for Oil and Electric Vehicles" Surfaces

A highly praised comment by a netizen, "Suggest canceling new energy subsidies," highlights an issue: "equal rights for oil and electric vehicles," which is two sides of the same coin as the "trade-in" policy.

At the beginning of December, a "document" about the collection of road maintenance fees for new energy vehicles in Hainan Province was widely circulated online. "A gale arises from the end of a green Ping," from a traffic perspective, why did the call for "equal rights for oil and electric vehicles" rise at the end of the year?

In fact, in June last year, Zeng Qinghong, Chairman of GAC Group, spoke at the 2024 China Auto Chongqing Forum, saying, "Equal rights! Equal rights for oil and electric vehicles! You say the market share of new energy vehicles has reached 50%, so how do we still support new energy vehicles?" This unreasonable phenomenon in the auto industry, amid the continuous increase in the penetration rate of new energy, has attracted industry attention.

An important data point is that starting in July last year, the retail penetration rate of new energy vehicles in China surpassed 50% for the first time. Shortly thereafter, in November, a new record was set with annual production and sales of new energy vehicles exceeding 10 million units.

In mid-to-late November, Guo Shougang, Deputy Director of the Equipment Industry Department of the Ministry of Industry and Information Technology, mentioned "continuing to tap the value of internal combustion engines" and "synchronously promoting the development of internal combustion engine technology" at a forum in Chongqing, once again fueling heated discussions on "equal rights for oil and electric vehicles".

In fact, compared to the more active group of new energy vehicle owners and mainstream information hyped by the media, the group of fuel vehicle owners, as the "silent majority," seems invisible. Moreover, if you only look at online comments, it seems that fuel vehicles are almost extinct. But the "cold" data is the most convincing. The demand for fuel vehicles or "vehicles with engines" is real.

In the first ten months of last year, fuel vehicles still accounted for 48% of the demand share in the passenger vehicle market, almost keeping pace with new energy and occupying half of the market. Moreover, for some automakers like Chery, the sales proportion of fuel vehicles still reached 76-77%.

Undoubtedly, the market demand for fuel vehicles has actually been severely underestimated; nearly half of the potential users in the auto market hope for "equal rights for oil and electric vehicles" and receive the same rights as electric vehicles when purchasing fuel vehicles.

In fact, what is the price war all about? The call for "equal rights for oil and electric vehicles" evokes the inner needs of these "silent majorities." "We fuel vehicle owners are subsidizing new energy vehicle owners, but what we get is online attacks and demonization of us." Many fuel vehicle owners are indignant about being portrayed as representatives of the "old-fashioned" and "backward" on the internet.

In fact, over the years, new energy vehicle models have cunningly played the role of the "weak," garnering sympathy. In other words, they are a bit like "disguising oneself as a pig to devour a tiger".

Just the exemption of vehicle purchase tax alone makes fuel vehicle users pay more taxes than new energy vehicle users, including pure electric, plug-in hybrid, and extended-range vehicles, when purchasing vehicles. In daily use, fueling also requires paying more taxes than charging.

In fact, currently, apart from Tesla, the electric vehicle businesses of both new energy vehicle startups and traditional automakers are basically in a state of loss. The only one that seems to be profitable is Li Auto. By the end of the year, as more and more new forces like HiPhi and NIO falter, it seems "too difficult" for new energy enterprises to become profitable.

Therefore, when reviewing the situation mid-year, we must return to the question: Can "equal rights for oil and electric vehicles" be resolved?

We know that the real world is complex, and the solution is akin to "cooking a small fish," which is difficult to implement with a one-size-fits-all approach. Many pure electric brands either rely on capital market financing to survive, such as NIO, which has lost over 100 billion yuan, and it is unclear when it can recover its costs. Others rely on the profits of fuel vehicles within the group to subsidize their survival.

Reality is often cruel. To truly achieve "equal rights for oil and electric vehicles," it may still have to be gradual. The "doomed" fuel vehicles are still the major profit earners and the key to the survival of the upstream and downstream supply chains in the automotive industry. We cannot disregard the overall situation just because developing new energy is a national strategy.

Endure and Endure Again?

In 2024, we stood on the cusp of an impending wave, and by 2025, the technological tide spearheaded by AI was poised to surge forth. Have you witnessed the unprecedented scale of Huang Renxun's NVIDIA launch at CES?

The automotive industry, having "weathered" 2024, did not pause. Instead, it kicked off 2025 with intensified competition and a relentless price war. While automakers eagerly anticipate the end of enduring low margins or losses, it is evident that 2025 will not mark the conclusion of this rivalry.

During the regular briefing on State Council policies held by the State Council Information Office on January 8, relevant officials from the Ministry of Commerce noted that since the implementation of the "two new" policies in 2024, sales of automobiles and household appliances have witnessed an uptick. Notably, over 60% of car trade-ins involved the purchase or replacement of new energy vehicles.

However, the issue of "equal rights for oil and electric vehicles" appears to have been sidelined, with joint ventures primarily focusing on fuel vehicles still at a disadvantage in terms of market share and public sentiment. Nevertheless, the vitality of a market hinges on a healthy ecosystem, akin to a forest that thrives on diversity—not just a single type of tree, but also shrubs, weeds, and more.

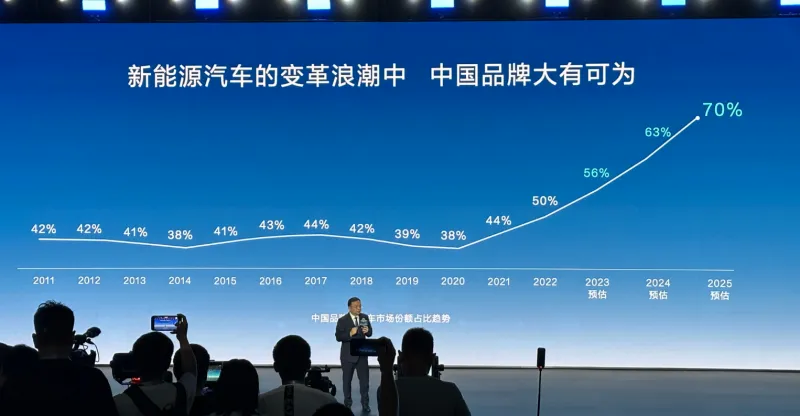

From January to November, Chinese brands captured 65% of the market share, edging closer to the 70% mentioned by BYD Chairman Wang Chuanfu, with estimates suggesting it will only take a few more months to reach that milestone.

Yet, a pivotal question arises: Wang Chuanfu also stated that joint venture brands would only account for 10% of the market in the next 3 to 5 years. If joint venture brands ultimately fail to sustain their presence in China, can the automotive industry's ecosystem be deemed healthy?

Recently, Yin Tongyue, Chairman of Chery Holding, offered a fair perspective in an interview, stating, "Foreign automakers have profited in China, but they have also left a significant impact. Their extensive localization efforts, encompassing talent, supply chains, and regulations, have bolstered the growth of our local enterprises, fostering advancements in quality, cost-effectiveness, and personnel capabilities."

In essence, market space should still be afforded to joint venture brands. We must embrace tolerance and refrain from "zero-sum games" or mortal combat. The "vicious competition" fostered by price wars is detrimental in every respect.

Furthermore, industry insiders caution that the departure of joint venture brands could impair our sensitivity and ability to keep pace with cutting-edge markets.

Another point to consider is the prediction by the China Passenger Car Association that domestic auto sales will reach 23.4 million units in 2025, with new energy passenger car sales surging to 13.3 million units, representing a 20% increase and a penetration rate of 57%. "The trade-in subsidy in 2025 will largely maintain the 2024 subsidy level. Roughly estimated, the overall demand for subsidy funds for scrapping and trade-ins is anticipated to exceed 200 billion yuan, far surpassing historical subsidy peaks. Therefore, regulating the upper limit of trade-in subsidies across regions is of utmost importance."

Both Volkswagen and Porsche have declared their intention to "return to China" (rekindle past glory) in 2026.

However, the seamless continuation of the price war into 2025 makes it challenging to foresee a swift turnaround for joint venture brands. The crux lies in ensuring a fair market environment; imbalance cannot be tolerated. 2025 must restore common sense and the core essence of business.

-

![]()

Model Giant Jieyue Xingchen Steps into Smartphone Arena: A Strategic Alliance with Huaqin Technology

-

![]()

Big Model Firm Dives into Phone Market: StepFun and Wingtech Forge a ‘Dynamic Duo’

-

![]()

Zhongrun Optics Makes a Bold Move with 1 Billion Yuan Investment: Is a Turning Point on the Horizon for the Precision Optics Industry?

-

![]()

Deploy CLBO Crystals and YIG Single Crystals! Erythritol Leader Invests 30 Million in Youwei Optoelectronics

-

CXMT’s July 16 Subscription: Leading Domestic Memory Manufacturer—What’s the Earning Potential per Lot?

-

![]()

Rhythm Discrepancy and Premium Value Erosion: Foreign Luxury Brands Must Re-evaluate Their China Strategy

-

![]()

Half-Year, 1 Billion Yuan Financing, 7 Billion Yuan Valuation: A New Dark Horse Emerges in the Embodied AI Sector

-

![]()

Strong Rebound for Tech Stocks in Hong Kong Stock Market: Is It Time to Bottom-Fish?