European Auto Market | UK March 2025: MG and BYD Excel

04/10 2025

04/10 2025

590

590

The UK auto market witnessed a surge in new car registrations in March 2025, with sales jumping 12.4% year-on-year to 357,103 units, setting a new March record since 2019. This uptick was primarily fueled by a 43.2% increase in battery electric vehicle (BEV) sales and robust performances from brands such as Volkswagen and Ford.

The UK market has seen a deepening penetration of Chinese brands, with BYD and MG demonstrating significant growth momentum, alongside emerging players like Omoda and Jaecoo.

In this article by ZhiNeng Technology, we delve into the latest dynamics of the UK market through sales data, focusing on powertrain performance, brand competition, and the ascendancy of Chinese brands.

01

Overview of UK Sales:

Powertrain & Brand Performance

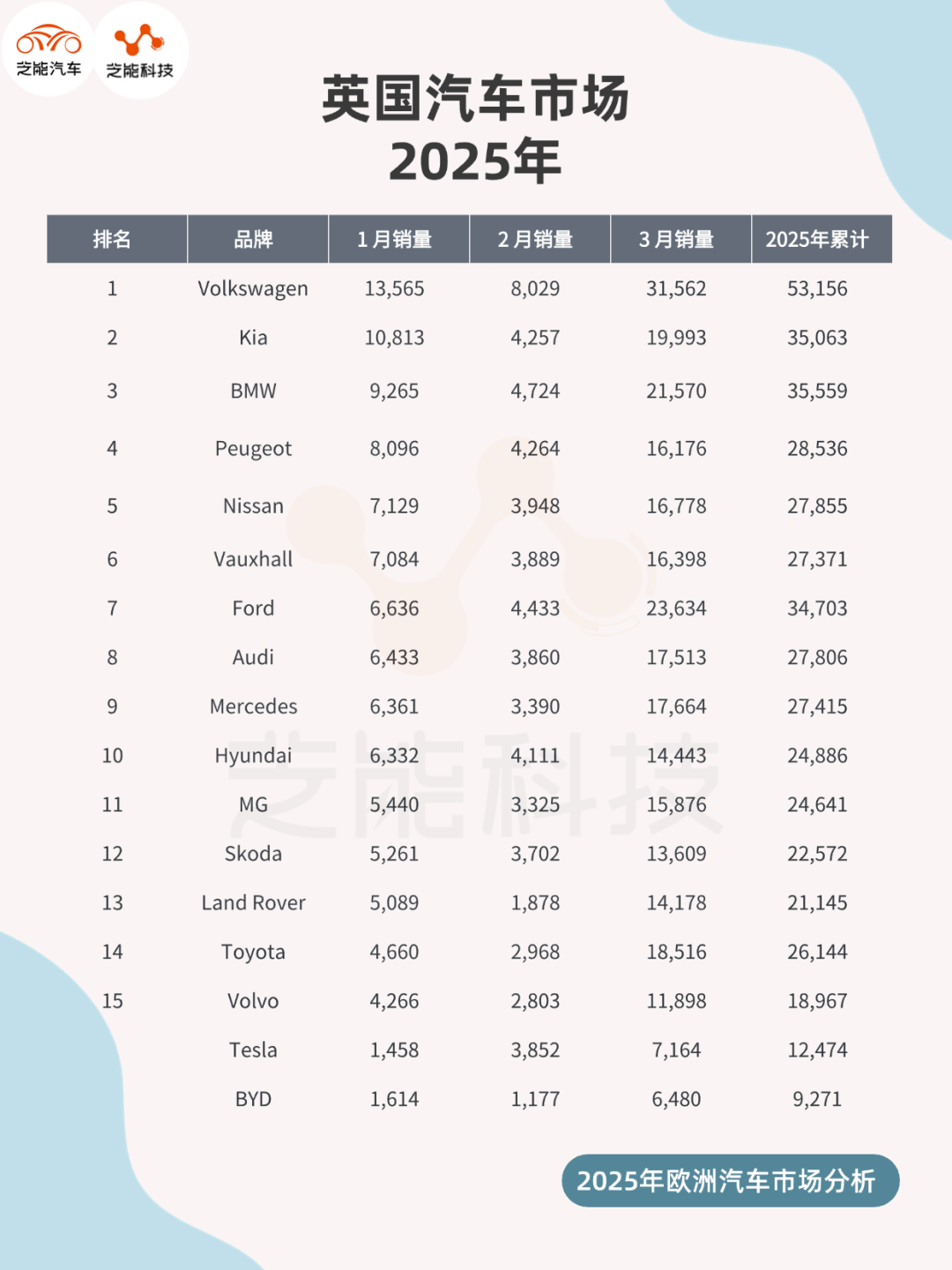

According to the Society of Motor Manufacturers and Traders (SMMT), new car registrations in the UK reached 357,103 units in March 2025, marking a 12.4% year-on-year increase. Cumulative sales for the first quarter stood at 580,502 units, up 6.4% from the previous year.

● March Highlights:

◎ Private purchases surged 14.5% to 147,041 units (41.2% of total sales),

◎ Fleet sales increased 11.5% to 202,171 units (56.6% of total sales),

◎ Commercial sales remained relatively flat at 7,891 units (2.2% of total sales).

● Powertrain Trends:

◎ BEVs emerged as the star performers, with sales soaring 43.2% to 69,313 units, setting a new monthly sales record and increasing market share to 19.4% (from 15.2% in March 2024).

◎ Plug-in hybrid electric vehicles (PHEVs) saw sales rise 37.9% to 33,815 units, boosting their market share to 9.5% (up from 7.7% last year).

◎ Hybrid electric vehicles (HEVs) grew 27.7% to 56,161 units, accounting for 15.7% of the market (up from 13.8% in 2024).

◎ Conversely, traditional internal combustion engine vehicles struggled, with petrol car sales dipping 0.4% to 176,847 units (market share down from 55.9% to 49.5%), and diesel car sales falling 10.1% to 20,967 units (market share down from 7.3% to 5.9%).

Data from the start of 2025 further underscores this trend: BEV sales grew 42.6% to 120,191 units (20.7% market share), while PHEVs and HEVs increased by 26.1% and 18.7% respectively. Petrol and diesel car sales, however, declined by 7.1% and 10.2%.

● Brand Performance:

◎ Volkswagen led the pack with 31,562 units (8.8% market share), up 42.5% year-on-year.

◎ Ford followed closely with 23,634 units (6.6% market share), up 38.8% year-on-year.

Together, these two brands contributed significantly to market growth.

Other mainstream brands performed mixedly:

◎ Toyota increased 9.7% to 18,516 units,

◎ Kia grew 8.2% to 19,993 units,

◎ BMW rose 7.5% to 21,570 units.

◎ Meanwhile, Nissan, Mercedes, and Audi witnessed declines of 18.4%, 10.8%, and 5.1% respectively.

◎ Volvo and Skoda, on the other hand, exhibited strong recovery momentum with growth rates of 58.1% and 36.3% respectively.

● Chinese Brand Performance:

◎ MG: Sold 15,876 units, up 22.7% year-on-year, ranking 11th with a market share of 4.4%. Year-to-date sales reached 24,641 units, up 6.5%.

◎ BYD: Sold 6,480 units, up a staggering 753.8% year-on-year, ranking 19th with a market share of 1.8%. Year-to-date sales stood at 9,271 units, up 625.4%.

◎ Omoda: As a newcomer, sold 2,082 units, ranking 31st with a market share of 0.6%. Year-to-date sales reached 3,194 units, indicating initial market acceptance.

◎ Jaecoo: Sold 1,786 units, ranking 33rd with a market share of 0.5%. Year-to-date sales reached 3,235 units. Along with Omoda, Jaecoo belongs to Chery and targets the premium SUV market.

The collective performance of Chinese brands underscores their strategic focus amidst the electrification wave. BYD's explosive growth is attributed to its battery technology advantages and diverse product portfolio (e.g., Dolphin, Atto 3), while MG has solidified its position in the mainstream market with models like HS and ZS. As part of Chery's dual-brand strategy, Omoda and Jaecoo have quickly gained a foothold with their stylish designs and competitive pricing.

02

Model Sales & Competitive Landscape Analysis

● Top 10 Models in March:

◎ Ford Puma: 11,132 units (+33.8%), market share 3.1%, reclaiming the monthly sales crown.

◎ Kia Sportage: 7,874 units (+5.8%), market share 2.2%, firmly in second place.

◎ Vauxhall Corsa: 6,851 units (+15.1%), market share 1.9%, outperforming expectations.

◎ Nissan Qashqai: 6,844 units (-23.4%), market share 1.9%, experiencing a significant sales decline.

◎ Nissan Juke: 6,471 units (-11.9%), market share 1.8%, also showing a downturn.

◎ VW Golf: 6,447 units (+14.5%), market share 1.8%, with steady growth.

◎ MG HS: 6,337 units (+16.1%), market share 1.8%, representing Chinese brands.

◎ Ford Kuga: 5,949 units, market share 1.7%, entering the top 10 for the first time.

◎ MG ZS: 5,907 units, market share 1.7%, MG's second model in the top 10.

◎ VW Tiguan: 5,464 units, market share 1.5%, maintaining stable performance.

● Competitive Landscape Analysis:

◎ Compact SUVs and crossovers dominated the sales rankings, reflecting UK consumers' preference for practicality and versatility.

Ford Puma's strong comeback underscores its dominance in this segment, while Kia Sportage's consistent performance highlights the enduring appeal of Korean brands in terms of design and value for money. Vauxhall Corsa's emergence as a top seller may be linked to the promotion of its electric version, warranting close attention.

◎ Chinese brand models made a significant impact. MG HS and MG ZS ranked 7th and 9th respectively, becoming the only Chinese models in the top 10, showcasing MG's deep roots in the compact SUV market.

BYD's sales growth suggests that its electric models (e.g., Dolphin, Seal) may be gaining traction across a broader range of segments.

◎ In the competitive landscape, traditional brands like Volkswagen and Ford maintain their lead through brand influence and product updates, but the decline of models like Nissan Qashqai and Juke indicates the pressure for renewal.

The rise of Chinese brands has intensified market competition, particularly in the electric vehicle sector, where BYD's rapid expansion poses a direct threat to Tesla (ranked 17th with sales of 7,164 units, up 2.4%).

Summary

The UK auto market in March 2025 was characterized by the surge in electrification and the ascendancy of Chinese brands. Record BEV sales drove the market towards a low-carbon transformation, while Chinese brands like BYD and MG quickly captured market share with their technological advantages and price competitiveness. This reflects the globalization capabilities of the Chinese auto industry and offers UK consumers more choices.

-

![]()

120,000 Layoffs in Silicon Valley Due to AI

-

![]()

Volkswagen Group to Slash Model Range by Half, Cut 1 Million Units of Production Capacity in China and Europe

-

![]()

World Models 101: Fundamentals, Technical Debates, and Scientific Frontiers

-

Polibeli, Xingyun Technology’s Affiliate, Partners with Amazon AWS to Boost Computing Power in Southeast Asia

-

![]()

Computing Power Infrastructure: Sudden Pause or Strategic Shift?

-

![]()

Zhipu Unveils 'Touch High' Initiative: Prioritizing Long-Term AGI Advancement Over Immediate Monetization

-

![]()

July "MIIT Auto Show" Unveils Major News: BYD Shark Pickup Makes Debut, Xiaomi Pengcheng Releases Official Images

-

![]()

Who is the Imaging King Among 26-Year-Olds? A Head-to-Head Comparison of MiOV's Top Three Ultra Flagships: The Results Will Astound You