Switch Transition from Copper to Optical: From 500 Wafers to a $10 Billion Market

07/09 2026

07/09 2026

497

497

The delivery timeline of a single switch model is sending ripples through a $10 billion market.

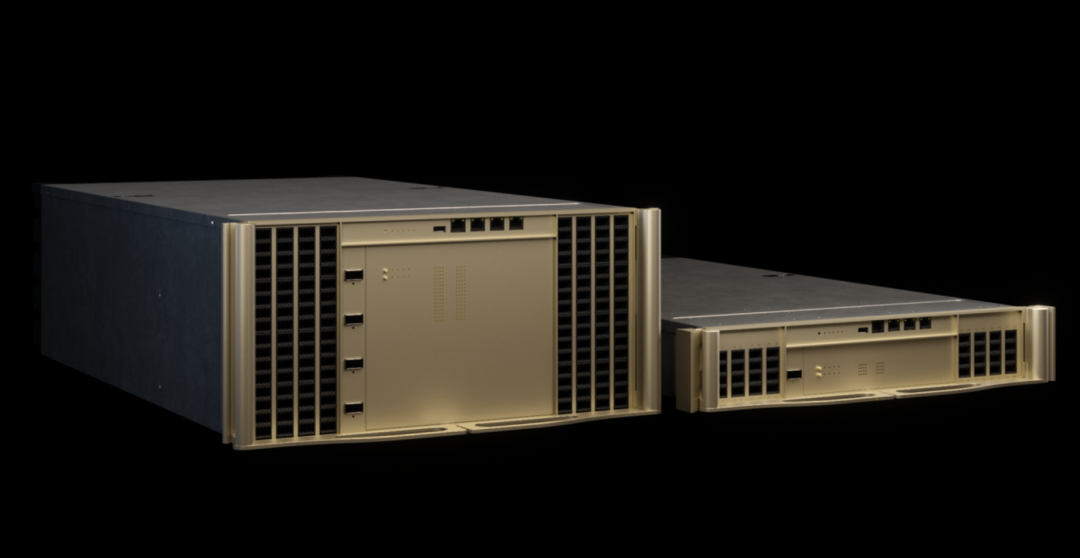

On June 2, 2026, NVIDIA launched the world's first Spectrum-X Ethernet switch based on Co-Packaged Optics (CPO) technology at Computex Taipei, with mass production slated for the second half of 2026.

A week later, third-party agency SemiAnalysis released an industry report suggesting CPO mass production might delay until 2028-2029. NVIDIA's Senior Vice President of Networking Gilad Shainer countered in an exclusive interview, confirming Spectrum's H2 delivery plan remains unchanged without delays.

Figure: NVIDIA Spectrum-X Ethernet Photonics Switch

Source: NVIDIA Official Website

The delivery timeline of a single switch model has both Wall Street and industry players on edge.

Traditional copper cables and pluggable optical modules struggle to meet AI clusters' bandwidth demands, with signal degradation, power surges, and latency spikes challenging physical limits. The industry consensus: Move optical communication units directly adjacent to switching chips. CPO embodies this approach.

This represents not incremental improvement but a fundamental restructuring of switch architecture. Electrical signal paths shrink from dozens of centimeters to millimeters.

How is this restructuring reshaping the $10 billion market? Why is CPO inevitable? What barriers remain to mass production? Which players truly benefit along the supply chain?

NVIDIA's Two-Year Ascent Reshuffles Switch Market Rankings

Image Source: Huawei, Head Research Institute

Switches serve as the central nervous system of data center networks. Data center switches for GPU clusters form the core of computing networks, while enterprise switches for office networks serve government and corporate campuses. By network hierarchy, they divide into access, aggregation, and core switches.

AI computing investments are rapidly rewriting market rankings.

IDC's Q1 2026 Ethernet Switch Tracker reports the global market reached $15.4 billion, surging 39.8% YoY. Data center switches for AI supercomputing and enterprise clusters accounted for $10 billion, skyrocketing 61% YoY. General enterprise switches for campuses and branches generated $5.4 billion, growing 12.3% YoY.

Among product segments, 800G switches captured 35.8% of data center revenue, with 200G/400G models combining for 34.1%. High-speed products now dominate nearly 70% of data center switch procurement spending.

The competitive landscape shifts even more dramatically. In Q1 2026, NVIDIA's data center Ethernet switch revenue hit $2.1 billion, capturing 21.5% of the $10 billion market with 192.7% YoY growth - surpassing previous leader Arista Networks for the first time. IDC called this "one of the most significant vendor landscape changes tracked in enterprise networking."

NVIDIA's rise stems from its Spectrum-X platform strategy, bundling Spectrum switches with BlueField DPUs, LinkX cables, and CUDA software stacks into an integrated AI platform. IDC Research Manager Brandon Butler noted Spectrum-X's rapid adoption comes from selling as part of tightly integrated GPU-network suites optimized for AI factory workloads, with network purchasing decisions tied to GPUs, software, and overall cluster architecture rather than standalone purchases.

Globally, Arista Networks reported $2.71 billion in Q1 switch revenue (+35% YoY). Cisco's data center switch market share has been surpassed by NVIDIA. Huawei maintains competitiveness in carrier networks, particularly strong in China and emerging markets.

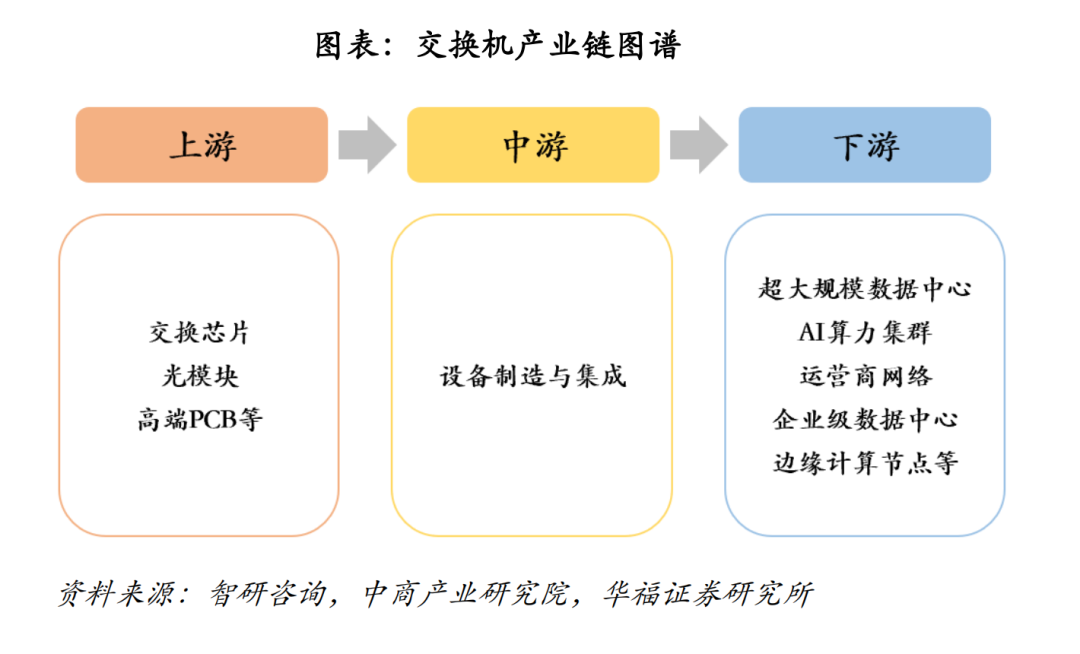

Industry Chain Overview: Value Distribution from Chips to Complete Systems

The switch industry chain comprises three segments: upstream core components, midstream equipment manufacturing, and downstream industry applications.

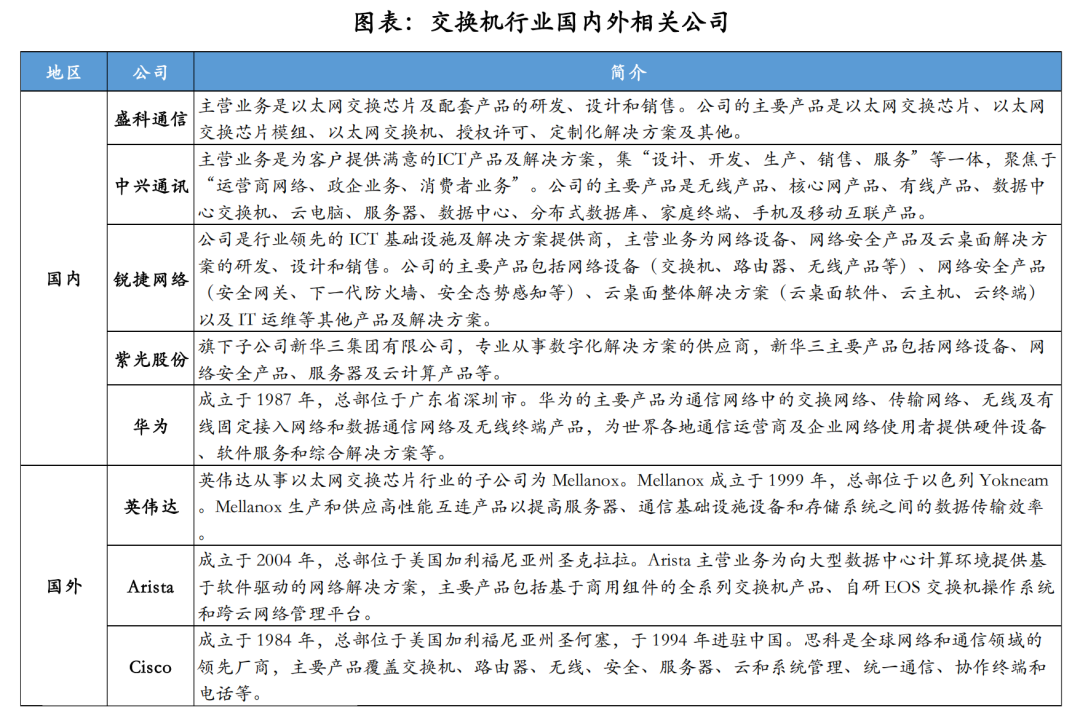

Upstream focuses on switching chips, optical modules, and PCBs. Switching chips account for ~32% of switch costs - the highest value segment. High-end switching chips have long been dominated by international players like Broadcom, Marvell, NVIDIA, and Cisco. Broadcom leads globally with its Tomahawk series setting industry standards. Domestic players like Cernet Communications offer full-range products from access to core layers, entering mainstream equipment supplier chains.

Midstream covers switch design, manufacturing, and integration. Global leaders include Cisco, Arista, Huawei, New H3C (Unisplendour), and Ruijie Networks. Domestically, New H3C leads. For OEM production, Foxconn exclusively manufactures NVIDIA's CPO switches.

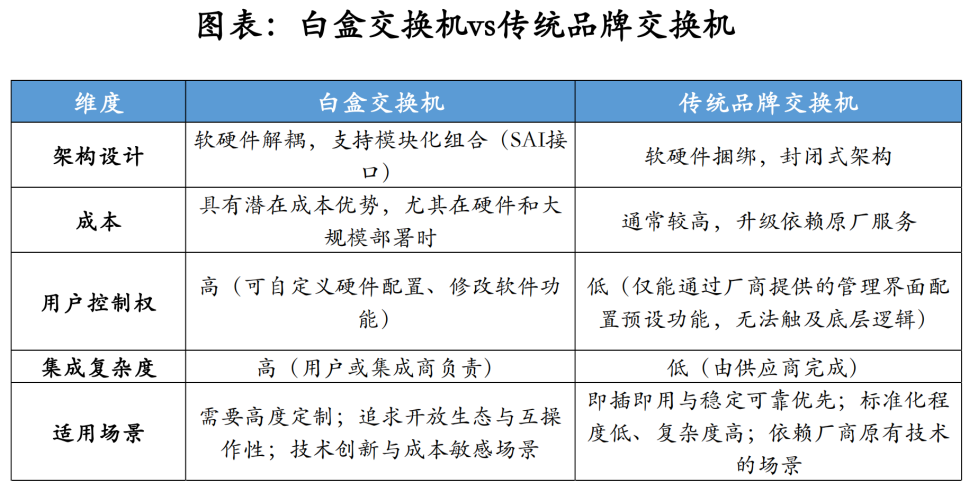

White-box switches represent a key trend in data center networking. These adopt open "software-hardware decoupled" architectures, separating hardware from operating systems to let users freely choose or develop their own network OS. By 2026, white-box/ODM switches captured ~20-25% of the data center switch market. In hyperscale data centers, penetration exceeded 45%. This trend challenges traditional brand dominance, empowering ODM manufacturers and significantly strengthening cloud providers' network control.

Downstream primarily comprises cloud providers, telecom operators, and large enterprises. Hyperscale cloud services like Google, Microsoft, Meta, and Amazon are the largest buyers of high-speed data center switches.

Why Switches Must Transition from Electrical to Optical

Understanding CPO's value requires recognizing AI data centers' core challenges.

In traditional pluggable optical module designs, electrical signals travel 15-30cm across circuit boards from switching chips to front-panel optical modules. Higher speeds exacerbate signal degradation, requiring complex compensation circuits and increasing power consumption. By 800G/1.6T generations, electrical interconnects' physical limits become clear.

TrendForce noted in its June silicon photonics report that as data rates upgrade from 100G/lane to 200G/lane and toward 400G/lane, traditional copper's limitations in signal loss, compensation costs, and power consumption become increasingly apparent. Bringing optical transmission closer to switching chips, shortening electrical paths, and reducing system power consumption have become central to next-gen AI data center design.

CPO relocates optical engines from switch front panels to beside switching chips on the same substrate. Co-packaging optical engines with switching chips reduces electrical distances from 300mm to under 50mm, cutting power consumption by 60-68% while significantly improving signal integrity.

A CPO switch's core components include: a central host ASIC switching chip, surrounding optical engines, external Continuous Wave Laser (ELS) modules, and FAU fiber array units for precise fiber-chip coupling.

The optical engine comprises two integrated modules: Electronic Integrated Circuits (EIC) for electrical signal processing and Photonic Integrated Circuits (PIC) for photon manipulation. TSMC's COUPE platform uses SoIC technology for 3D stacking of EIC and PIC, bringing components closer to enhance bandwidth and power efficiency while reducing electrical coupling losses.

Modulator selection represents the most significant technical divergence among CPO vendors. Two main routes exist: NVIDIA pursues full-stack CPO systems deeply integrated with GPUs using 3D packaging and Micro-Ring Modulators (MRM) - technically challenging but offering compact size, high density, and low power; Broadcom emphasizes compatibility with cloud providers' network architectures using more mature Mach-Zehnder Modulators (MZM) with better temperature stability and signal robustness. Neither approach is universally superior - they reflect different tradeoffs for target scenarios.

For external lasers, CPO uses external Continuous Wave Laser solutions for three reasons: thermal isolation (host chips generate hundreds of watts, while lasers are temperature-sensitive); serviceability (laser diodes have shorter lifespans, and external modules allow field replacement); and manufacturing yield (laser materials differ completely from silicon, making separate production more practical).

TrendForce projects CPO/NPO market size will surge from ~$100 million in 2025 to over $39 billion by 2030. Growth will accelerate sharply between 2028-2029 as Scale-up architectures adopt optical interconnects.

Industry Trends: Ethernet Surpasses InfiniBand, White-Box Captures 45% of Hyperscale Data Centers

Beyond CPO, two major trends are reshaping the switch industry.

Ethernet is overtaking InfiniBand. In 2023, InfiniBand held ~80% of the AI backend network market. Just over two years later, Ethernet surpassed it in data center switch and server port counts. Dell'Oro Group reports AI backend network Ethernet switch sales more than doubled in Q1 2026, accounting for ~2/3 of AI cluster data center switch sales. 800G switches dominated AI backend network shipments and revenue this quarter, with 1600Gbps models beginning sampling for H2 2026 ramp-up.

Ethernet's rise stems from engineering familiarity and integration of lossless technologies previously exclusive to InfiniBand. As standardized protocols like Ultra Ethernet advance, Ethernet's compatibility and cost advantages will further emerge.

White-box switches are reshaping supply chain dynamics. By decoupling software and hardware, they let cloud providers freely combine hardware and operating systems. This trend challenges traditional brand switches' dominance. By 2026, white-box/ODM switches captured ~20-25% of the data center switch market. In hyperscale data centers, penetration exceeded 45%. Traditional brand premiums shrink as ODM influence grows and cloud providers strengthen network control.

Source: Huafu Securities Research Report

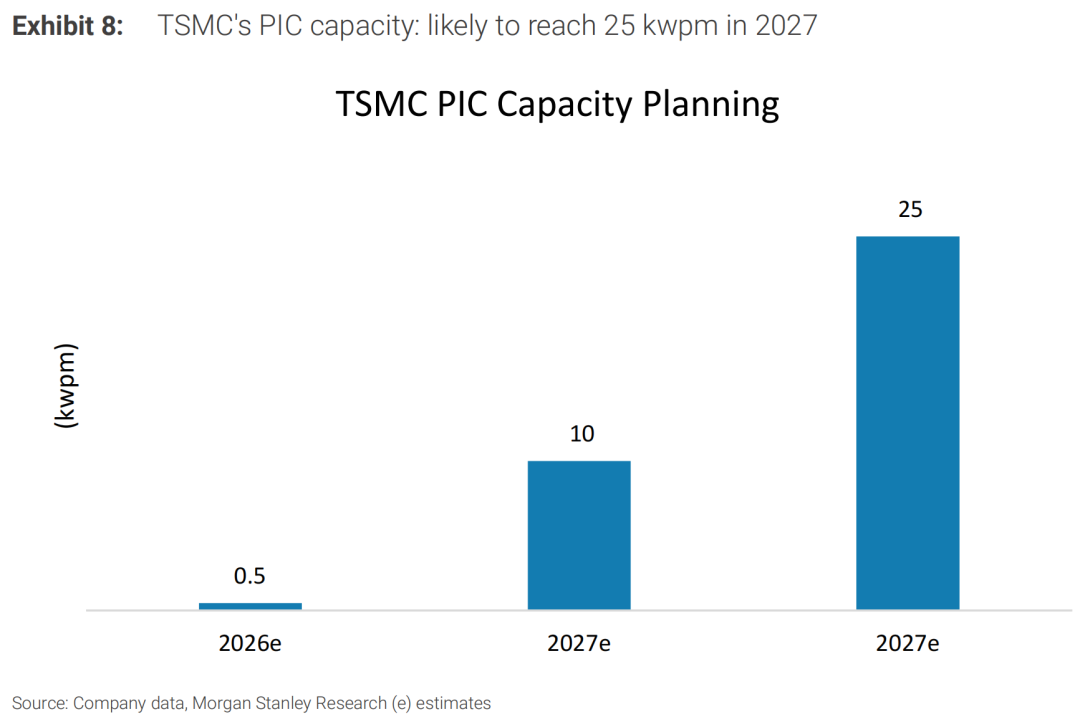

From 500 to 25,000 Wafers: TSMC's Capacity Determines CPO Rollout Pace

CPO's true mass production depends not on technology but on TSMC's capacity.

According to Morgan Stanley's early-July report, TSMC's PIC (Photonic Integrated Circuit) capacity is ramping from 500 wafers/month to 25,000 wafers/month - the "master switch" for CPO industrialization. PICs are CPO optical engines' core components, handling electrical-to-optical signal conversion, guidance, and coupling.

Figure: TSMC's PIC Capacity Planning

Source: Morgan Stanley Report

Calculated at 648 dies per wafer, annualized PIC output will surge from approximately 4 million units to nearly 200 million units. However, due to limited initial resources, TSMC's COUPE platform will primarily serve NVIDIA, Broadcom, and AMD as its key mass production clients between 2026 and 2027. After further capacity expansion in 2028, more vendors such as MediaTek, Marvell, and Ayar Labs are expected to achieve mass production of their CPO projects at TSMC.

However, wafers alone are not enough. Morgan Stanley points out that the current downstream assembly yield is estimated at only 20%, expected to rise to 50% by 2028. Actual optical engine shipments will reach approximately 3.9 million units in 2026, 7.78 million units in 2027, and surge to 48.6 million units in 2028.

Another major bottleneck in mass production is testing. The Insertion 2 wafer-level optoelectronic synchronous test for CPO marks the first critical node where optical and electrical signal tests are conducted simultaneously. Previously, inspecting a single wafer took 24 hours, but this has now been reduced to 6 hours. Skipping this testing phase would cause the final system yield to plummet by over 40%. Technological breakthroughs in the three key areas of wafer testing, fiber array unit assembly, and high-speed optical packaging will be crucial in determining whether CPO can achieve successful scalability.

Morgan Stanley projects that global CPO switch shipments will reach approximately 23,000 units in 2026, increasing to 59,000 units in 2027 and 200,000 units by 2030, with a compound annual growth rate (CAGR) of 144% from 2024 to 2030. Nomura Securities experts predict that CPO penetration will reach 3%-5% in 2026, accelerating and scaling up from the second half of 2027.

Who Benefits in the Industrial Chain: Value Restructuring from Components to Systems

The implementation of CPO is redistributing value across the industrial chain.

In the core components segment, the Fiber Array Unit (FAU) is the most directly benefiting component. The FAU is responsible for the high-precision coupling between optical fibers and silicon photonics optical engines, with multiple FAUs required for a single CPO switch. Key suppliers include TFC Communication (TFC), FOCI, Senko, and others. Morgan Stanley estimates that FOCI will hold a 35%-40% market share in the CPO FAU market, with its SiPh/CPO revenue share rising from 7% in 2024 to 80% by 2028.

Regarding lasers, CPO light sources primarily adopt external continuous-wave lasers. Manufacturers such as Lumentum, Coherent, and Sumitomo are accelerating capacity expansion. In March 2026, NVIDIA invested $2 billion each in Lumentum and Coherent and signed substantial purchase commitments, which the market views as a final confirmation of the CPO technology roadmap.

In the midstream packaging and manufacturing sector, TSMC's COUPE platform serves as the core hub, with final development to be completed and formal mass production to commence in 2026. Broadcom's Tomahawk 6 Davisson switch is also built on TSMC's COUPE technology. ASE is responsible for chip-level packaging, assembly, and testing.

In the downstream system segment, Foxconn Group is NVIDIA's system assembly partner for all-optical CPO switches. According to Taiwan Economic Daily, Foxconn has already started shipping all-optical CPO switch cabinets to NVIDIA ahead of schedule, with supply being extremely tight—even demonstration cabinets have been handed over to NVIDIA, leaving "none left." Foxconn's shipment expectations have been significantly raised, with over 10,000 units expected to be shipped in 2026 and a total of over 50,000 units from 2026 to 2027.

The domestic optical communication industry is deeply integrated with the CPO industrial chain. Leading optical module companies dominate the global market with their 800G products, while their 1.6T CPO products have entered NVIDIA's Spectrum-X CPO switch verification chain. In the exchange chip sector, Centec Communications is a leading domestic design enterprise, offering a full range of products from access to core layers. New H3C (Unisplendour Corporation)'s 51.2T CPO silicon photonics data center switch has already achieved bulk delivery and deployment at customer sites in 2025.

From a broader perspective, the value of the CPO industrial chain is shifting from traditional optical module assembly to upstream segments such as optical chip design, PIC manufacturing, and advanced packaging. Companies that can deeply bind with leading clients and possess technological barriers in core components will be the first to deliver performance.

Source: Huafu Securities Research Report

GlassBridge: Balancing Long-Term Variables and Short-Term Logic

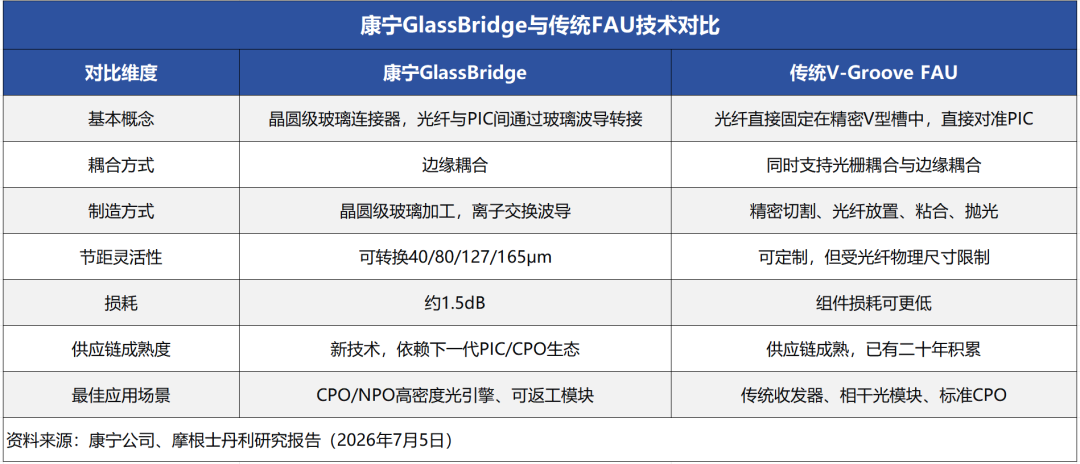

Recent market attention has been highly focused on Corning's GlassBridge technology. This is a fiber-to-PIC connection platform based on wafer-level ion-exchange waveguides, seen as an evolutionary alternative to fiber array units in CPO architectures.

GlassBridge's advantages lie in wafer-level mass manufacturing, customizable pitch, detachability, and passive alignment, making it particularly suitable for high-density CPO/NPO optical engines. TrendForce notes that detachable fiber connection solutions, including Corning GlassBridge, Teramount, Senko Alliance, and Intel OCI, are still developing in parallel, with a phenomenon of technological Hundred Schools of Thought Contend (hundred schools of thought contending).

However, Morgan Stanley's assessment is far milder than market concerns. Existing CPO solutions (including the Quantum and Spectrum series) have already completed mass production finalization and are expected to remain unaffected by GlassBridge. More critically, GlassBridge currently primarily supports edge coupling, while TSMC's mainstream COUPE platform and its core clients' solutions in the coming years will still prioritize grating coupling, which is easier to achieve scalable mass production.

The more fundamental logic is that the industrialization of CPO is a systematic endeavor. A CPO solution, from PIC design and optical engine packaging to system integration, requires collaboration across the entire industrial chain. Any adjustment in a single link requires a verification cycle of over six months. Corning also positions GlassBridge cautiously, defining it as a "complement" rather than a replacement for traditional FAU solutions.

Industry judgment suggests that the commercialization window for GlassBridge will be between 2028 and 2030, with no impact on finalized CPO solutions within the next one to two years.

The Tipping Point of "Optics Replacing Copper"

The switch industry is undergoing a profound restructuring, from underlying architecture to market competition.

At the market level, NVIDIA has risen to the top in data center switch revenue in just two years, riding the wave of AI computing power investment and rewriting the traditional landscape. Technologically, CPO has shortened the electrical distance from 300 millimeters to less than 50 millimeters, reducing power consumption by over 60% and driving data center networks to shift from "long-distance electrical signal transmission" to "nearby optical signal conversion."

TSMC's PIC capacity will expand from 500 wafers to 25,000 wafers, CPO switch shipments will increase from 23,000 units to 200,000 units, and the market size will surge from hundreds of millions to tens of billions of dollars. Behind this is a fundamental shift in industrial logic: In AI computing clusters, networks are no longer peripheral attachments to computing but critical infrastructure determining whether computing power can be effectively unleashed.

Meanwhile, Ethernet is surpassing InfiniBand in AI backend networks, white-boxization is reshaping the supply chain landscape, and pluggable optical modules can still maintain a scale of nearly $26 billion by 2030. The future of optical interconnects will not be dominated by a single technological route.

However, one thing is clear: CPO is moving from the lab to the factory. 2026 is the starting point, 2027 is the ramp-up phase, and true explosion will occur after 2028. For participants in the industrial chain, the real differentiation has only just begun.

Data Sources: IDC, SemiAnalysis, Publicly Disclosed Information from Companies

Research Report Sources:

Morgan Stanley, "Greater China Semiconductor Industry Report: CPO Supply Chain Update; Further Exploration of GlassBridge," July 5, 2026

TrendForce, "Silicon Photonics Industry Research Report," June 15, 2026

Nomura Securities, "AI Expert Conference Call #56: Latest CPO Market Dynamics," January 20, 2026

Huafu Securities, "In-Depth Report on the Switch Industry: Rapid Development of AI Large Models Drives Switch Market Expansion," December 23, 2025

Reporting Sources:

Official Announcements and Demonstration Materials from NVIDIA GTC 2026

TSMC COUPE Platform Technical Specifications

Disclaimer: This article is for reference only and does not constitute investment advice.

THE END

Copyright and Disclaimer

1.Content Copyright: Except for quoted public data, policies, and cases, all content in this article is original. Professional data is sourced from authorized databases and government websites, and cases are compiled from real events.

2.Image Authorization: Some images in this article are proprietary materials or officially licensed, and some are AI-generated; for network images without clear copyright, the copyright belongs to the original authors, and any infringement will be removed upon notification.

3.Reprinting Norms: Unauthorized reprinting is prohibited; reprinting must retain the complete source and author.

4.Responsibility Statement: This article is a commercial figure observation and industrial commentary compiled by the author based on publicly available information. The content is for reference only and does not constitute professional advice. Any risks arising from use shall be borne by the user. The Industrial Chain Social Security reserves the final interpretation rights of this article.

-

![]()

Model Giant Jieyue Xingchen Steps into Smartphone Arena: A Strategic Alliance with Huaqin Technology

-

![]()

Big Model Firm Dives into Phone Market: StepFun and Wingtech Forge a ‘Dynamic Duo’

-

![]()

Zhongrun Optics Makes a Bold Move with 1 Billion Yuan Investment: Is a Turning Point on the Horizon for the Precision Optics Industry?

-

![]()

Deploy CLBO Crystals and YIG Single Crystals! Erythritol Leader Invests 30 Million in Youwei Optoelectronics

-

CXMT’s July 16 Subscription: Leading Domestic Memory Manufacturer—What’s the Earning Potential per Lot?

-

![]()

Rhythm Discrepancy and Premium Value Erosion: Foreign Luxury Brands Must Re-evaluate Their China Strategy

-

![]()

Half-Year, 1 Billion Yuan Financing, 7 Billion Yuan Valuation: A New Dark Horse Emerges in the Embodied AI Sector

-

![]()

Strong Rebound for Tech Stocks in Hong Kong Stock Market: Is It Time to Bottom-Fish?