Is Zhipu's AGI Option Really Worth HK$400 Billion?

04/02 2026

04/02 2026

636

636

The Ice and Fire of Large Models: The Reality and Illusion of a Trillion-Dollar Market Cap

Zhipu's first financial report directly propelled its market value beyond HK$400 billion.

On the evening of March 31, Zhipu released its first annual report since listing in Hong Kong in January, followed by an annual performance briefing. The report revealed rapid revenue growth but a widening year-on-year loss, with total revenue surging 131.9% to RMB 724 million and a comprehensive gross margin of 41% for the year. Annual losses expanded to RMB 4.718 billion, up 59.5% year-on-year.

Despite the widening losses, capital market enthusiasm remained undiminished. On the morning of April 1, Zhipu's shares opened 15% higher and continued to rise, with its market value briefly surpassing HK$400 billion.

So, what information does this annual report convey? Why did it drive a sharp jump in the stock price? Has Zhipu's fundamentals changed compared to its listing?

01

Driving Up Stock Price with Future Expectations?

Zhipu's stock surge stems partly from its precise alignment with current capital market preferences: not just absolute revenue scale but also future-oriented business narratives.

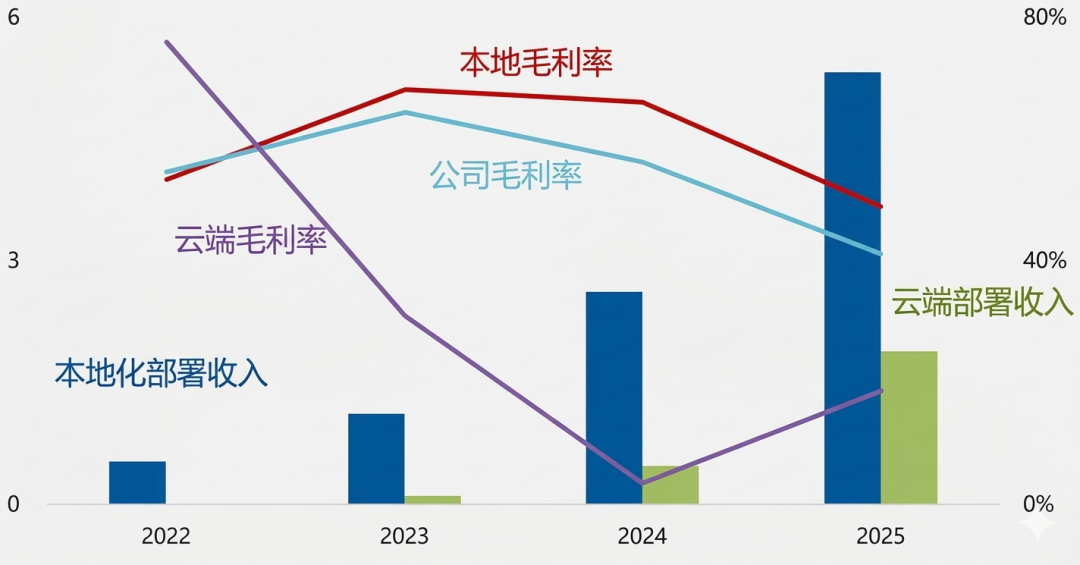

In terms of revenue, Zhipu's localized deployment income reached RMB 50 million, RMB 110 million, RMB 260 million, and RMB 530 million from 2022 to 2025, with a four-year CAGR of 119.7%. Meanwhile, cloud-based deployment income, seen as the future, reached RMB 3 million, RMB 10 million, RMB 50 million, and RMB 190 million, with a four-year CAGR of approximately 298.6%.

Notably, as absolute revenue continues to rise, revenue growth rates remain robust, and the proportion of cloud-based deployment income has surged, aligning with market enthusiasm for the MaaS model.

More importantly, Zhipu reinforced these expectations during its earnings call. Management attributed the revenue surge to continuous breakthroughs in the model's "intelligence ceiling."

"From GLM-4.5 to GLM-5, Zhipu underwent several key iterations in 2025. Notably, GLM-5, released in February 2026, achieved performance close to leading international closed-source models, positioning Zhipu favorably in pricing power."

"Our API call pricing increased by 83% in the first quarter. Despite this, demand outstripped supply, with call volumes surging 400%. This reaffirms that high-quality tokens are scarce resources today—whoever controls the intelligence ceiling controls pricing power."

"Currently, Zhipu's MaaS platform ARR is approximately RMB 1.7 billion, a 60-fold increase over the past 12 months. Through extreme engineering optimization on the inference side, we significantly reduced token unit costs, dramatically improving profitability. MaaS platform gross margins rose nearly fivefold to 18.9%, far exceeding industry standards."

Zhang Peng's logic is clear: Zhipu has invested heavily in training powerful large models, enabling it to raise prices and increase token sales. The additional revenue can be reinvested in R&D, creating a virtuous cycle.

While emphasizing its model's strength, Zhipu also shifted its growth narrative from localized deployments to MaaS.

Initially, Zhipu focused on localized deployments, installing large models and their environments directly on clients' (often government agencies, large SOEs, or financial institutions) private servers or data centers.

This model's advantages are obvious: client data remains in-house, ensuring high privacy and security, with per-project contracts often worth millions or even tens of millions. However, its drawbacks are fatal—it is essentially a "labor-intensive IT outsourcing project." Each project requires significant algorithm engineer involvement for fine-tuning, testing, and maintenance, making standardization difficult, marginal costs high, and scalability poor.

This is why AI companies focused on localized deployments often fall into the trap of "higher revenue, higher labor costs, greater losses." Zhipu's emphasis on MaaS in capital markets aims to escape this traditional software outsourcing valuation pitfall.

While localized deployments remain the primary revenue contributor in the 2025 financial report, the MaaS model shows sustainable growth trends.

To portray a bright MaaS future, Zhipu's management introduced a new concept: TAC (Token Architecture Capability).

Zhipu argues that in 2026, intelligent paradigms will achieve closed-loop execution of multi-step, logically consistent Long-horizon Tasks, further breaking through intelligence ceilings and driving exponential token usage growth. Zhipu aims to become the infrastructure enhancing societal TAC, turning every token into deliverable economic value.

This rapid revenue growth, coupled with management's even more aggressive growth guidance and a visionary future blueprint, would excite any investor, making the stock surge understandable.

02

Zhipu Remains Unchanged, Still the Same Zhipu

However, after the grand narratives, the company must continue operating. Business sustainability requires examining profitability and expenses, not just revenue.

Currently, this remains Zhipu's Achilles' heel. The 2025 financial report disclosed a 59.5% year-on-year loss increase, reaching RMB 4.718 billion. Compared to RMB 724 million in revenue, this means Zhipu loses RMB 6.5 for every RMB 1 earned—the core theme of its current operations.

By business segment, the localized deployment business, the revenue mainstay, is seeing accelerating gross margin declines. Data shows localized deployment margins peaked at 68% in 2023 before plummeting to 49% in 2025.

This indicates that as the business penetrates more traditional industries, Zhipu must invest heavily in customized development to secure non-standardized government and enterprise orders. This "labor-intensive" nature traps localized business in "diseconomies of scale"—more projects mean harder-earned profits.

While the cloud-based MaaS business restored positive margins through price hikes (previously negative due to price wars), its 19% gross margin lags far behind the 70% achieved by leading cloud companies' MaaS businesses.

Moreover, the recent token consumption surge was driven by the "lobster craze" from Openclaw. Sustaining growth when model capabilities are on par with competitors remains Zhipu's challenge. Otherwise, ARR-based revenue projections remain mirages.

After examining profitability, let's review the three major expense categories: selling, general, and administrative (SG&A), and R&D.

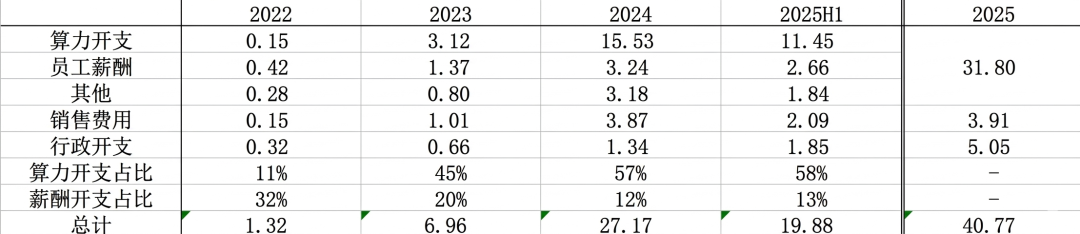

The 2025 annual report differs slightly from the prospectus. Previously, SG&A and R&D were broken down into computing power expenses, R&D staff salaries, others, selling expenses, and administrative expenses. However, the annual report no longer sub-divides R&D expenses. Nevertheless, based on previously disclosed 25H1 data, the 2025 full-year expense structure is largely clear.

The expense table reveals a core evolutionary theme in Zhipu's cost structure: starting with labor as the focus, then shifting to computing power as the dominant expense amid business growth and model iterations. Today, as the competitive landscape expands, all expenses continue to surge.

In 2022, Zhipu's total expenses were just RMB 132 million, with computing power expenses a mere RMB 15 million (11%), while staff salaries accounted for 32% (RMB 42 million). In this startup phase, Zhipu epitomized a "labor-intensive" model, earning profits through algorithm engineers' on-site localized deployment work.

However, as the large model competition intensified, Zhipu's cost structure underwent a dramatic reversal to support management's claimed "intelligence ceiling" breakthroughs.

From 2023, computing power expenses exploded geometrically, surging to RMB 312 million (45%) in 2023 and RMB 1.553 billion (57%) in 2024. Computing power completely replaced labor as the primary cash drain. Zhipu's core driver officially shifted from "manpower" to "computing power cards."

Critically, this "labor-to-computing power" transition has not delivered expected economies of scale or cost reductions. In 2025, all expense categories continued to rise sharply.

Of the RMB 4.077 billion in total expenses, RMB 3.18 billion went to computing power and R&D salaries, while selling and administrative expenses reached RMB 391 million and RMB 505 million, respectively. This shows Zhipu must not only invest heavily in computing cards for its foundational models but also spend heavily on sales networks and operational systems for commercialization.

Indeed, Zhipu has transformed from a labor-intensive outsourcing team to a computing power-driven MaaS platform. Yet fundamentally, it remains trapped in "surging expenses, trading losses for future growth."

In this cash-burning race with no finish line in sight, the HK$400 billion market cap resembles an expensive call option placed by capital. If cloud revenue growth fails to outpace escalating expenses before depleting cash reserves and investor confidence, the virtuous cycle will collapse.

This dilemma faces all independent large model companies: running out of cash means exiting the game, but not burning cash means never entering it.

However, as AI rapidly disrupts business models, Zhipu and its peers will encounter one "lobster moment" after another. Each blockbuster application launch offers a chance for large model companies to take flight. Whoever first bridges the gap from "burning cash for scale" to "technological innovation for profits" will secure the final ticket to the AGI era.

- END -

-

![]()

Model Giant Jieyue Xingchen Steps into Smartphone Arena: A Strategic Alliance with Huaqin Technology

-

![]()

Big Model Firm Dives into Phone Market: StepFun and Wingtech Forge a ‘Dynamic Duo’

-

![]()

Zhongrun Optics Makes a Bold Move with 1 Billion Yuan Investment: Is a Turning Point on the Horizon for the Precision Optics Industry?

-

![]()

Deploy CLBO Crystals and YIG Single Crystals! Erythritol Leader Invests 30 Million in Youwei Optoelectronics

-

CXMT’s July 16 Subscription: Leading Domestic Memory Manufacturer—What’s the Earning Potential per Lot?

-

![]()

Rhythm Discrepancy and Premium Value Erosion: Foreign Luxury Brands Must Re-evaluate Their China Strategy

-

![]()

Half-Year, 1 Billion Yuan Financing, 7 Billion Yuan Valuation: A New Dark Horse Emerges in the Embodied AI Sector

-

![]()

Strong Rebound for Tech Stocks in Hong Kong Stock Market: Is It Time to Bottom-Fish?