Liu Jingkang's Verbal Misstep and Insta360's 'Strategic Blunder'

05/21 2026

05/21 2026

460

460

The 2026 June 18 shopping extravaganza has just commenced, and the consumer electronics sector has already been swept up in an unexpected wave of public sentiment.

Recently, Insta360 Innovation (688775.SH) initiated blind pre-orders for its highly anticipated inaugural dual-lens gimbal camera, the 'Luna Ultra,' with an official launch slated for June 9.

Previously, numerous details about the Luna Ultra had been leaked online, with pricing being the sole remaining mystery. Following the commencement of pre-sales, rumors swirled that its price point was substantially higher than anticipated by the market, swiftly igniting accusations of 'exorbitant pricing' within the tech community.

In response, founder Liu Jingkang promptly issued a clarification, yet his comments only served to intensify the situation.

The 'Pricing Philosophy' Blunder

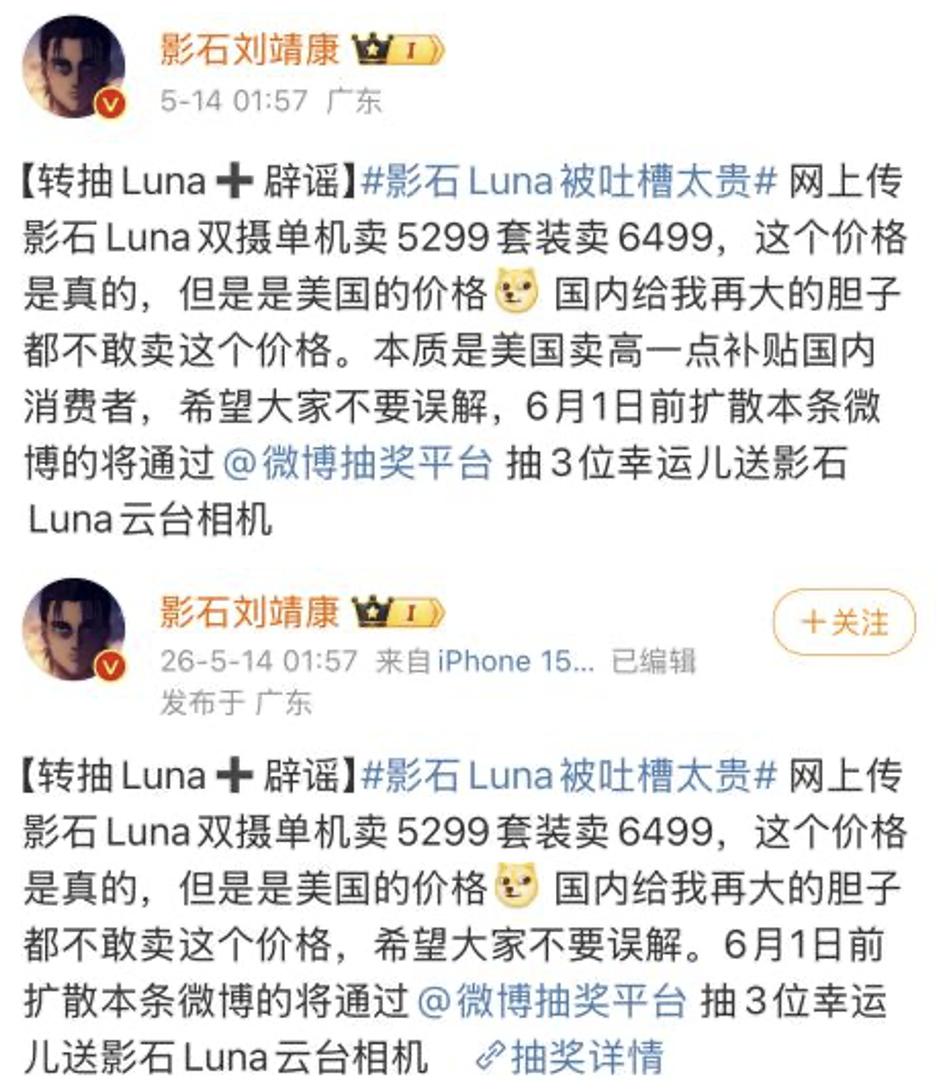

The controversy originated from a post-pre-sale price revelation by a blogger, disclosing a standalone price of 5,299 yuan and a full kit price of 6,499 yuan.

When compared to DJI's Pocket 4, which was released around the same time and priced at 2,999 yuan for the standard kit and 3,799 yuan for the full kit, the Luna Ultra's pricing immediately sparked heated debate within the tech community. Accusations of 'price gouging' and 'taking advantage of fans' proliferated across social media platforms.

Liu Jingkang took to Weibo to respond, confirming the prices but emphasizing that they were for the U.S. market. He further stated, 'Essentially, we charge more in the U.S. to offset costs for domestic consumers.'

This 'offset theory' rapidly ignited public outrage, but the backlash was contrary to Liu's intentions. Domestic consumers rejected this 'differential treatment,' while overseas markets, particularly the U.S.—Insta360's largest single market—also reacted strongly. American consumers felt they were being treated as 'money trees.'

Observing the situation spiraling out of control, Liu swiftly deleted the 'offset domestic costs' remarks shortly after posting.

Image source: Weibo

For Insta360, this was no ordinary public relations misstep—it shook the very foundation of the company.

In 2025, overseas revenue accounted for 69.03% of Insta360's total, with a gross profit margin of 47.87%, surpassing the domestic margin of 42.10%.

The U.S. market stood out as a key segment. Although not detailed in the 2025 financial report, IPO filings revealed that the U.S. contributed 23.38% of revenue in 2024, making it the largest regional market outside mainland China. Revenue from the U.S. was 17.58 percentage points higher than that from Japan, the third-largest market.

Liu's comment about 'charging more in the U.S. to offset costs for domestic consumers' may appear to be fan-friendly, but in reality, it involves using profits from the core overseas market to subsidize the fiercely competitive domestic market.

This 'robbing Peter to pay Paul' pricing strategy seems shortsighted in the context of global operations. The Luna Ultra's stumble ahead of the shopping festival has exposed this structural risk.

Net Profit Margin Plummets to 1.3%

Setting aside the emotional factors of the June 18 controversy and focusing on financial data reveals that Insta360's seemingly unstoppable growth narrative has already shown signs of fatigue.

Shortly before the controversy, Insta360 released its first full 2025 annual report and Q1 2026 earnings, revealing an alarming truth: the company is in a precarious position of 'increasing revenue but stagnant profits.'

Financially, Insta360 has experienced rapid expansion. From 2023 to 2025, revenue soared from 3.636 billion yuan to 9.741 billion yuan, with a Compound Annual Growth Rate (CAGR) of 63.67%, nearing the 10 billion yuan threshold.

However, alongside revenue growth, net profits have declined post-IPO. From 2023 to 2025, net profits attributable to shareholders were 830 million, 995 million, and 929 million yuan, respectively.

In Q1 2026, the situation did not improve. Revenue grew by 83.11% year-over-year to 2.481 billion yuan, but net profits attributable to shareholders plummeted by 52.02% year-over-year to 84.62 million yuan.

The declining profit margins are even more striking. From 2023 to 2025 and Q1 2026, gross margins were 55.95%, 52.20%, 45.74%, and 45.20%, respectively, while net margins were 22.81%, 17.85%, 9.15%, and 1.3%, teetering on the brink of breaking even.

Insta360 attributed this to 'strategic investments' in its 2025 report, revealing R&D efforts for two drones, gimbal cameras, wireless lavalier microphones, and three custom chips.

From 2023 to 2025, R&D spending rose from 448 million to 1.53 billion yuan, with the R&D-to-revenue ratio increasing from 12.31% to 15.70%, further rising to 18.73% in Q1 2026.

In 2025 and Q1 2026, strategic investments in new businesses reached 762 million and 262 million yuan, respectively, equivalent to 80% and 300% of net profits in those periods.

Facing such 'aggressive' R&D expansion, Insta360 stated in its financial report, 'Our current core business stems from bold attempts made 7-8 years ago.' Liu Jingkang is betting heavily on the same logic for the future.

But with a net margin of just 1.3% and deteriorating cash flow, the margin for error in this gamble is rapidly shrinking. In Q1 2026, net cash from operating activities turned negative, plunging to -1.471 billion yuan.

The Battle with DJI on Home Turf

If internal financial pressures are a 'hidden illness,' then competition from DJI is an 'open wound.'

In the global 360-degree camera market, Insta360 has held the top spot for eight consecutive years. However, the market's ceiling is within sight. Frost & Sullivan predicts that the global 360-degree camera market will grow from 5.03 billion yuan in 2023 to 7.85 billion yuan in 2027.

This means that even if Insta360 captures the entire market, its core business is unlikely to surpass 10 billion yuan in the near future.

To expand growth, Insta360 is betting on drones as its 'new growth engine.' In December 2025, it launched its first 360-degree drone, the 'Yingling A1,' with a standard package priced at 6,799 yuan, directly entering DJI's territory.

Liu Jingkang revealed in an internal letter that sales in China exceeded 30 million yuan within 48 hours. However, just three months later, DJI released the Avata 360, forcing Insta360 to officially cut the Yingling A1's price.

During the June 18 promotions on JD.com, the Yingling A1's standard package dropped to 5,499 yuan, a reduction of 1,300 yuan. To date, cumulative sales remain just over 1,000 units.

In contrast, DJI dominates JD.com's best-selling drone list, occupying the top 10 spots. The new Avata 360 ranks 17th, while the Yingling A1 fails to crack the top 30.

Insta360 is on the offensive, but DJI is counterattacking. Five months before Insta360's drone launch, DJI released its first 360-degree camera, the Osmo 360, priced at 2,999 yuan, directly targeting Insta360's flagship X4 at a nearly 800 yuan lower price point.

DJI's offensive didn't stop there. In October 2025, it slashed prices by about 30% across models like the Pocket 3, Action 4, and Osmo 360. In May 2026, the new Pocket 4's standard package was priced as low as 2,499 yuan.

Facing DJI's pincer attack, Galaxy Securities noted that this directly compresses the pricing space for Insta360's Luna series. Pricing too high fails to attract DJI's existing users, while pricing too low exacerbates profit pressures.

More critically, DJI has escalated competition to the legal front.

In March 2026, DJI sued Insta360 for infringing on six core drone patents, alleging that the technologies were developed by former employees within a year of their departure and thus constituted job-related inventions. This marks DJI's first domestic patent infringement lawsuit, which, if successful, could directly impact Insta360's R&D direction.

Market share shifts are even more telling. IDC data shows that in 2025, DJI surged to first place in global handheld smart imaging devices (including action cameras and 360-degree cameras) with a 62% shipment share, while Insta360's share shrank to 20.4%. DJI rose from third to first, while Insta360 fell to second.

Under DJI's pressure, Insta360 is losing ground in its core market while burning cash on new ventures. Liu Jingkang's comment about 'charging more in the U.S. to offset costs for domestic consumers' was intended to address these challenges but has instead become part of the problem.

DJI's offensive continues, and Insta360's remaining options are dwindling.

-

![]()

The Surprisingly Significant Impact Difference Between Quiet and Noisy Cars!

-

![]()

Breaking Through Storage Cycle Barriers: How AI Large Models and Coding Technology Synergize to Drive Transformation in the Security Industry

-

Facilitating the Slimming of Camera Modules! O-film Obtains Utility Model Patent for Periscope-Type Reflective Component

-

![]()

Hikvision Raytine’s Millimeter-Wave Body Imaging Security Inspection Device Achieves ECAC SSc Category A Standard Level 2.1 Certification for European Civil Aviation

-

![]()

Global Market Share for Security Windows Hits 26%! This Optical 'Little Giant' Makes Its Debut on NEEQ

-

![]()

The Evolutionary Path of Agent Engineering: From Prompt to Harness by Zhang Yutao, Co-founder of Moonshot AI

-

![]()

Profits and stock prices are both declining, so why are executives from these auto companies increasing their purchases?

-

![]()

Burning Tens of Billions of Dollars, Yet No Unified Definition for World Models