Everyone Chases AI, Yet Overlooks the Most Valuable AI of All

04/02 2026

04/02 2026

586

586

Once the market becomes fixated on pursuing hot trends and hyping up concepts, genuinely valuable opportunities often go unnoticed.

In 2026, as companies like Zhipu and MiniMax surge ahead at a breakneck pace, and the frenzy for "lobster farming" (a metaphor for trendy but potentially overhyped ventures) sweeps across the globe, Robotaxi—an established AI sector with tangible near-term deployment and profitability prospects—has been sidelined.

[Closed-loop Business Model, Imminent Explosion]

If we were to pinpoint the industry that has evolved most rapidly in recent years, Robotaxi would undoubtedly be a strong contender.

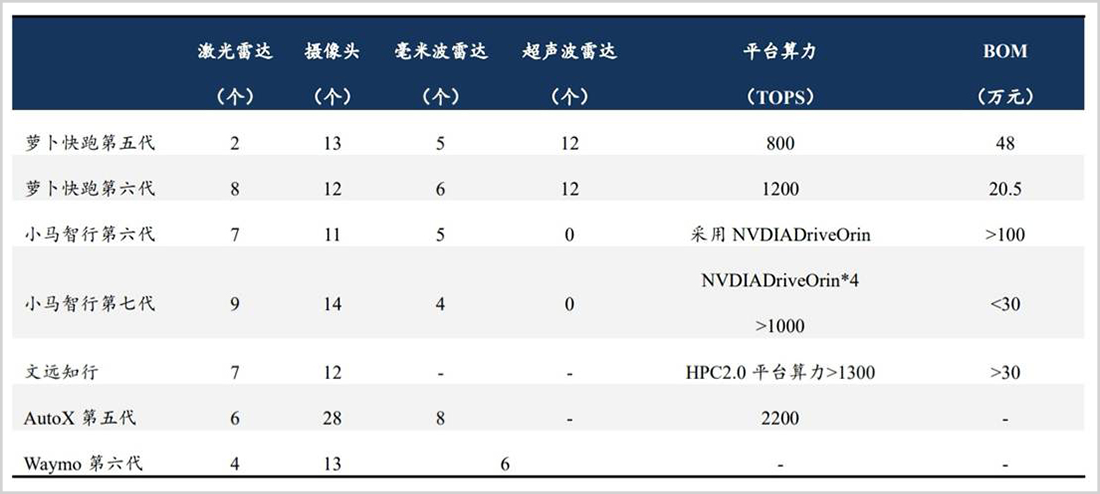

Over the past five years, the sector has achieved a historic leap from technology introduction to commercial deployment, making disruptive progress across three core dimensions: technology, cost, and policy.

Rewind to 2021, when intelligent driving was still at L2 level, Robotaxi operations were primarily confined to parks and closed road sections, with highly unstable performance at complex intersections and in extreme weather conditions. Today, however, algorithm and perception architectures have undergone a comprehensive upgrade, with L4 technology advancing at a breakneck speed, while policies have gradually shifted from "cautious pilot" to "orderly opening."

Five years ago, the total cost of a single Robotaxi exceeded RMB 1 million, with the laser radar alone costing nearly RMB 100,000. However, driven by the domestic supply chain and mass production, hardware costs such as laser radar have dropped by 90%. Currently, the BOM cost of new-generation Robotaxi models from leading companies has dipped to RMB 300,000.

Many fail to realize that this once seemingly distant industry has quietly overcome cost barriers and achieved closed-loop commercialization.

In November of the previous year, Pony.ai officially announced that its Robotaxi service in Guangzhou had achieved positive profitability on a per-vehicle basis. In early March of this year, the company once again announced that its seventh-generation Robotaxi in Shenzhen had also achieved positive profitability on a per-vehicle basis.

Around the same time, WeRide also announced that it had taken the lead in achieving single-city profitability in the Middle East market.

Then there's OnTime, whose Robotaxi fleet has rapidly expanded to over 600 vehicles, signifying a doubling of its operational capacity compared to the previous period.

But that's not the most crucial point.

According to OnTime's latest plan, its Robotaxi service will cover 100 core cities across China over the next five years. Simultaneously, it will collaborate with partners to build a fleet of over 10,000 Robotaxis and launch a RMB 1 billion-level investment plan to establish a total of 1,000 Robotaxi tertiary operation and maintenance networks across 100 core cities. These networks will include OnTime Robotaxi rapid response sites, maintenance stations, and hub centers, forming a comprehensive capability to support the offline operation and maintenance of 100,000 Robotaxis annually.

From Pony.ai to WeRide, and now to OnTime, all these developments point to the same conclusion: Robotaxi is crossing the inflection point and entering a moment of explosive large-scale adoption.

According to the latest data from Soochow Securities, the global Robotaxi market is expected to reach RMB 83.1 billion by 2030 and further grow to RMB 709.6 billion by 2035, representing at least a tenfold increase in incremental growth space over the next decade.

In this process, the entire mobility industry may undergo a new reshuffling, giving rise to a new batch of more influential and promising platforms in China. Besides tech giants like Baidu and Didi, as well as new tech elites like Pony.ai and WeRide, the relatively under-the-radar OnTime will also emerge as a key player worthy of close attention.

[Pricing Logic Shift, Recovery Imminent]

The reason for singling out OnTime for discussion is that the company boasts many unique advantages.

There have always been two valuation frameworks in the mobility sector: one for traditional platforms like Didi, Caocao, and OnTime, which have entered a stable development phase and consistently trade at a low valuation; the other for tech-focused Robotaxi companies like Pony.ai and WeRide, which are seen as promising and imaginative, thus easily commanding a valuation premium in the capital markets.

For a long time, OnTime has been valued according to the traditional ride-hailing platform framework. However, as global Robotaxi services embark on large-scale commercialization and consensus builds around Robotaxi as a new growth engine for the mobility services industry, the market has begun to recognize that Robotaxi will reshape the valuation logic of global mobility service platform companies.

Against this backdrop, coupled with OnTime's commercialization of Robotaxi services in multiple locations across the Greater Bay Area and the recent significant expansion of its Robotaxi fleet, this shift in internal valuation framework represents a latent and intangible positive for the company.

Moreover, business model is another core competitive strength of OnTime.

Unlike Pony.ai and WeRide, which focus solely on technology, OnTime's strategy is to build a Robotaxi ecosystem. Using an open operation platform as its foundation, it integrates all compliant Robotaxis (such as those from WeRide and Pony.ai) and then consolidates resources from various parties to provide operational capacity to the market.

Don't underestimate the moat of "building an ecosystem" compared to "focusing on technology." Connecting the entire chain of "automakers + technology + operations + infrastructure + compliance" is an extremely challenging endeavor.

Furthermore, from a commercialization perspective, this may be the fastest way to achieve network formation and scale.

According to the latest news, Uber has officially announced its shift from "in-house Robotaxi development" to "Robotaxi aggregation operations."

As a global leader in mobility platforms, Uber has long been seen as an industry bellwether, and its pivot largely represents a new consensus within the industry on this matter.

Barring any surprises, against the backdrop of a closed-loop business model and accelerating fleet expansion, aggregation operation platforms will become the top priority in the entire Robotaxi sector in the coming years, and OnTime's shareholder advantages will be significantly highlighted.

Backed by GAC Group, Tencent, Didi, Pony.ai/WeRide, OnTime's shareholder lineup is truly unparalleled in the industry. Leveraging this "circle of friends," the company has constructed a formidable competitive barrier encompassing vehicle manufacturing, internet traffic, and intelligent driving technology.

GAC Group provides low-cost compliant new energy vehicles and front-end mass production, Tencent offers access to its billion-user WeChat traffic pool along with high-precision mapping and cloud computing capabilities, Pony.ai/WeRide supply L4 autonomous driving technology, and combined with OnTime's years of platform operation experience, the entire package is nothing short of perfect.

While other companies may lack vehicles, technology, operations, infrastructure, or compliance, OnTime has everything in place except perhaps a final catalyst.

Across the entire mobility industry, it may not be the most powerful or influential, but it is certainly the most imaginative.

In its latest research report, Soochow Securities gave OnTime a "Buy" rating, expressing optimism about OnTime's advantages in the Robotaxi commercialization wave, leveraging shareholder synergies and its broad access to mainstream L4 technology suppliers through its Robotaxi platform.

[Enhanced Profitability, Significant Safety Margin]

In fact, even without considering the future narrative of Robotaxi and focusing solely on the present, OnTime remains noteworthy.

According to the latest data from Soochow Securities, OnTime's price-to-sales (PS) ratio stands at just 0.3x, not only well below the industry average but also the lowest among all comparable companies.

In other words, OnTime offers a relatively high safety margin.

This attribute becomes even more pronounced when considering the company's current earnings growth rate.

On March 31, OnTime released its full-year 2025 financial results, reporting total revenue of RMB 5.286 billion for the year, a substantial year-on-year increase of 114.6%, with profits improving significantly by 48.1%.

It's worth noting that in the first half of 2025, OnTime's revenue was only RMB 1.676 billion. Based on the full-year total revenue of RMB 5.286 billion, the company's revenue in the second half of 2025 reached RMB 3.6 billion, more than double that of the first half.

This significant profit breakthrough can be attributed to OnTime's adoption of a more refined and efficient development strategy.

On one hand, the company has adopted a "ripple model" to deeply cultivate core markets, optimizing operational efficiency to the highest level before rapidly replicating this model in emerging markets to expand its operational scale. On the other hand, it has fully embraced new technologies such as AI to drive a transformation in its revenue structure from a single mobility model in the past to a "mobility + technology" model.

This strategy has significantly accelerated the development of OnTime's core businesses. In 2025, the company's revenue from mobility services and technology services grew by 131.8% and 487.4% year-on-year, respectively.

Moreover, it's important to note that the gross margin of the technology services business is higher than that of traditional mobility services.

Taking 2025 data as an example, the gross margin of mobility services increased from 5% to 11.7%, while the gross margin of technology services reached as high as 14.8%.

According to company disclosures, the primary revenue source for technology services is AI data service products and solutions, covering core areas such as data collection, annotation, and synthesis. These products have penetrated AI application scenarios across multiple key industries, including intelligent driving cabins, large language models, consumer electronics, financial services, and research institutions. This indicates that OnTime has begun commercial realization in the AI data services sector.

As AI technology accelerates its penetration into various fields, this segment holds immense future value potential. As of the end of 2025, OnTime had established three major service delivery bases across China, managing a professional annotation team of over 1,500 people. Simultaneously, the company had deployed over 300 intelligent driving data collection vehicles in Guangzhou to conduct compliant data collection.

What holds even greater future value is the strong synergistic effect between OnTime's technology services business and Robotaxi. On one hand, the continuously expanding Robotaxi operations provide rich data resources and application scenarios for technology services. On the other hand, the output of technology services feeds back into the continuous optimization of Robotaxi technology, forming a virtuous cycle of "operations - data - technology - commercialization."

With the gross margin of mobility services on the rise, the increasing proportion of technology services in revenue (from 1.1% to 3% in 2025), and their strong synergy with Robotaxi, OnTime's profitability and profit levels are theoretically set to continue rising.

This year, the explosion of AI applications has attracted everyone to chase the latest trends, with everyone focusing on the freshest and most fashionable things.

However, from an investment perspective, what truly matters is returning to rationality and identifying solid businesses that already possess conditions for deployment and profitability expectations.

Sectors like Robotaxi may well be the temporarily forgotten, yet ultimately shining, pearl on AI's crown.

Disclaimer

The content of this article concerning listed companies is based on the personal analysis and judgment of the author, derived from information publicly disclosed by the listed companies in accordance with their statutory obligations (including but not limited to interim announcements, periodic reports, and official interaction platforms). The information or opinions presented in this article do not constitute any investment or other commercial advice, and Market Value Observer shall not be held responsible for any actions taken based on this article.

--END--

-

![]()

Model Giant Jieyue Xingchen Steps into Smartphone Arena: A Strategic Alliance with Huaqin Technology

-

![]()

Big Model Firm Dives into Phone Market: StepFun and Wingtech Forge a ‘Dynamic Duo’

-

![]()

Zhongrun Optics Makes a Bold Move with 1 Billion Yuan Investment: Is a Turning Point on the Horizon for the Precision Optics Industry?

-

![]()

Deploy CLBO Crystals and YIG Single Crystals! Erythritol Leader Invests 30 Million in Youwei Optoelectronics

-

CXMT’s July 16 Subscription: Leading Domestic Memory Manufacturer—What’s the Earning Potential per Lot?

-

![]()

Rhythm Discrepancy and Premium Value Erosion: Foreign Luxury Brands Must Re-evaluate Their China Strategy

-

![]()

Half-Year, 1 Billion Yuan Financing, 7 Billion Yuan Valuation: A New Dark Horse Emerges in the Embodied AI Sector

-

![]()

Strong Rebound for Tech Stocks in Hong Kong Stock Market: Is It Time to Bottom-Fish?