The Trillion-Dollar Arena for Humanoid Robots: Two Trajectories, One Shared Future

05/26 2026

05/26 2026

542

542

At its core, the Sino-US robotics industry competition is a symbiotic contest, where neither side can truly thrive without the other.

Recently, US President Trump arrived in Beijing aboard Air Force One, with NVIDIA CEO Jensen Huang joining the delegation at the eleventh hour. The US's intensified export controls on H20 chips had already compelled NVIDIA to write down $4.5 billion in assets; Huang's primary mission on this trip was to advocate for the normalization of civilian AI computing power supplies to China.

(Image source: Internet)

Trump's delegation included not only Huang but also Elon Musk, CEO of Tesla and creator of Optimus. The simultaneous presence of these two tech titans, who are shaping the future of US robotics, underscores an industrial reality rather than mere diplomatic formality: while the US government attempts to stifle China's access to robotics computing power, it simultaneously dispatches its own tech leaders to seek collaboration.

This paradoxical stance unveils a fundamental truth about humanoid robotics: technological rivalry at the 'brain' level is inherently interdependent and complementary.

01 US 'Superbrain' Faces Production Bottlenecks

Globally, the US continues to dominate the 'brain' layer of humanoid robotics, with strengths concentrated in three distinct technical approaches:

The first approach involves the refined development of general-purpose embodied AI models, exemplified by Figure AI. In February 2025, Figure AI unveiled Helix, the industry's inaugural dual-system VLA model tailored for robots. It employs a 7 billion-parameter visual-language model (S2) for deliberative thinking—comprehending scenes, parsing semantics, and planning tasks—while an 80 million-parameter Transformer (S1) executes fine-grained actions at 200Hz. This decoupled 'brain + cerebellum' architecture enables robots to manipulate thousands of unfamiliar objects using only natural language instructions. In a kitchen demonstration, the Figure 03 robot autonomously performed 61 consecutive actions over four minutes without human intervention—marking the highest-complexity autonomous sequence ever publicly showcased.

(Figure AI's Helix system)

The second approach centers on algorithm migration driven by data flywheels, with Tesla as the prime example. It systematically transfers algorithms, data, and computing power from its intelligent vehicle domain to humanoid robots. Tesla directly adapted its FSD (Full Self-Driving) algorithm, validated across millions of vehicles, for the Optimus robot. With over 6 million Tesla vehicles worldwide generating 160 billion frames of real-world video data daily, Tesla has created an unparalleled data flywheel. Musk relaunched the Dojo 3 supercomputing project, planning to densely integrate 512 self-developed AI5 chips (each with 2,500 TOPS) to provide massive computing power for Optimus training. By 2026, Tesla's AI and robotics capital expenditures are projected to exceed $25 billion.

The third approach focuses on open-source ecosystem platformization, led by NVIDIA. In March 2025, NVIDIA introduced GR00T N1, touted as the world's first open-source foundational model for humanoid robots. Designed to serve the broader robotics community rather than just NVIDIA products, it integrates with the Omniverse synthetic data engine to create an Android-like system for robots. Huang identified robotics as the next trillion-dollar market following AI.

This 'brain' dominance determines whether US humanoid robots can adapt and make autonomous decisions in unfamiliar environments. However, the US faces structural challenges.

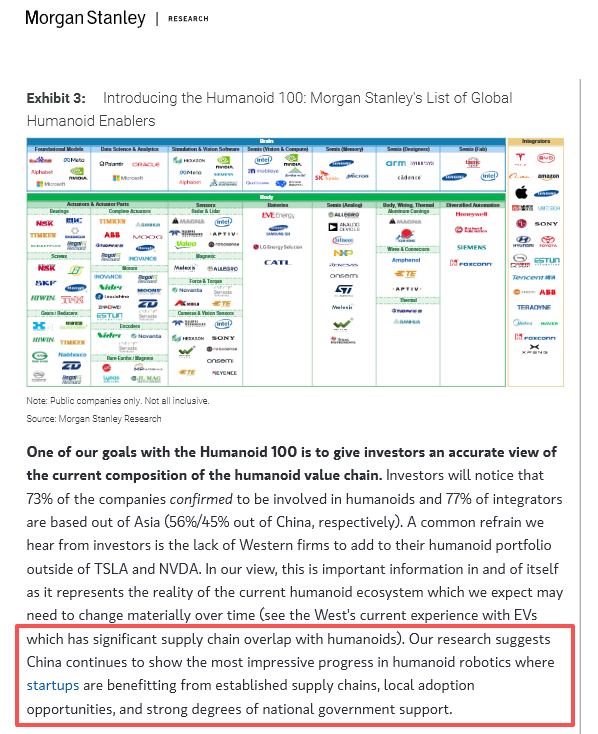

Morgan Stanley's 2025 'Robotics Yearbook' report highlights that China has developed systemic advantages in mass production and scenario application for humanoid robots. Despite US policy efforts, the industrialization gap is widening rapidly due to a fundamental mismatch between US manufacturing ecosystems and robotics industrialization needs.

(Screenshot source: Morgan Stanley 2025 'Robotics Yearbook')

First, the hollowed-out US robotics supply chain restricts rapid hardware iteration and cost control. Less than 50% of the US robotics industrial chain is localized, with critical components like harmonic reducers, high-precision servo motors, and force-control sensors heavily reliant on Japanese and South Korean suppliers. This prolongs R&D cycles and keeps costs elevated, hindering large-scale, low-cost manufacturing for consumer or industrial robots.

Second, cutting-edge US algorithms lack sufficient physical bodies for validation. Figure AI, valued at $40 billion for its Helix system, plans annual production of just 12,000 units; Tesla's Optimus monthly output remains in the hundreds. This lab-leading, factory-lagging gap means advanced algorithms cannot continuously collect data and iterate through massive real-world deployments, limiting intelligence evolution speed and practicality.

Finally, US robotics commercialization lacks breadth and depth in deployment scenarios. While strong in high-value, low-volume fields like healthcare and space exploration, the US lacks China's rich application scenarios and urgent labor replacement needs for scalable industrial manufacturing, logistics, and commercial services. Without scenarios, data flywheels cannot form, preventing algorithm advantages from converting into market and cost advantages.

In essence, even the most sophisticated algorithms require physical bodies to execute. The US 'body'—mature supply chains, scalable manufacturing, and rich mass-production scenarios—cannot keep pace with its 'brain' evolution, posing its greatest challenge in this humanoid robotics marathon.

02 China's Scenario-Driven Sprint Lacks Computing Power

While US robotics 'brains' rely on algorithmic refinement, China's approach achieves differentiation through massive real-world scenario data.

In April 2026, Zhiyuan Robotics conducted an eight-hour unedited live broadcast from a Longcheer Technology factory: its Elf G2 robot completed 2,283 precise material handling cycles at the MMIT test station with a 99.5% success rate, processing 18–20 seconds per step and 310 units hourly—equivalent to two human shifts. This was real deployment, not a demo. Zhiyuan declared 2026 the 'Year of Deployment,' with robots working 7×24 hours on production lines. To date, Zhiyuan has deployed over 10,000 robots, ranking first globally in 2025 with 5,100 units shipped and a 39% market share. Its open-source AGIBOT WORLD 2026 dataset derives entirely from real-world commercial and industrial scenarios.

Unitree Robotics excels further. Its G1/H1 series became the default hardware platform for global researchers, capturing 60% of the global quadruped robot market in 2025. Unitree's strategy is straightforward: flood markets with ultra-cost-effective hardware (G1 priced at just ¥99,000) to let global labs and factories collect data and refine algorithms.

Chinese companies' core advantage lies in the scale of real-world operational data. While US robots learn to grasp cups in labs, Chinese robots have already tightened hundreds of thousands of screws at BYD factories, moved millions of packages in logistics warehouses, and operated for thousands of hours on high-temperature production lines. This 'dirty data' from the physical world is irreplaceable by synthetic or internet video data for three reasons:

First, physical interaction complexity. Zhiyuan engineers shared a case where Elf G2 initially failed to account for summer heat-induced plastic deformation in workshops, causing repeated positioning errors. Such physical intuitions only emerge in real production lines, beyond synthetic data's reach.

Second, unpredictable failure modes. Real-world robots encounter bizarre scenarios—long-tail events impossible to fully simulate but crucial for robustness. Zhiyuan's AGIBOT WORLD 2026 dataset explicitly labels over 2,000 abnormal conditions, a treasure trove no simulator can replicate.

Third, socio-collaborative dimensions. In Chinese factories, robots work alongside thousands of workers, learning to interpret gestures, avoid busy colleagues, and discern commands in noisy environments. Such social intelligence can only develop in real human-robot-information flow intersections.

Industry estimates suggest Chinese leaders have 10× more real industrial deployment data than US peers. More critically, China's complete manufacturing ecosystem—from 3C electronics to automotive parts, food processing to chemical production—generates unique robotics scenarios in nearly every subsector. This scenario density is an unreplicable strategic asset for the US.

But data floods need an outlet—computing power, China's Achilles' heel.

03 NVIDIA's $4.5 Billion Lesson

NVIDIA's Q1 2026 earnings report revealed a staggering figure: $4.5 billion. This represents inventory write-downs and purchase obligation losses forced by US H20 chip export controls to China.

The H20, NVIDIA's China-customized AI chip compliant with prior export rules, was its flagship product for Chinese data centers and humanoid robotics computing needs. In April 2025, the US government abruptly tightened controls, requiring reapplication for H20 export licenses—effectively freezing mass shipments.

This policy shock translated directly into financials: a $4.5 billion Q1 2026 write-down. NVIDIA warned in its earnings call to expect another $8 billion in Q2 2026 revenue losses, with Hopper architecture effectively halted in China.

Huang had forewarned this. At Computex 2025, he admitted NVIDIA's China AI market share had collapsed from 95% in early 2021 to 50%. Recently, at a Castle Securities event, Huang stated the share had fallen to 0%: 'China has many domestic AI chips. Without NVIDIA, customers will use local technologies.'

Those local technologies are growing rapidly. Huawei's Ascend 950PR chip delivers 2.87× the inference performance of NVIDIA's H20, with 75% lower memory usage and over 50× lower cost. Its 384-chip supernode architecture provides 1.7× more total computing power than NVIDIA's GB200 cluster. DeepSeek-V4 migrated fully from CUDA to Huawei's CANN framework, boosting inference speed 35×. Horizon Robotics' Journey 6P chip achieves 6 TOPS/W energy efficiency, surpassing international peers, and captured 33.97% of the L2+ autonomous driving market in 2025—overtaking NVIDIA.

Algorithmically, China is catching up. Zhiyuan's G0-1 model introduced the ViLLA architecture, combining VLM and Mixture-of-Experts systems. Star Motion Era's ERA-42 became China's first end-to-end native robot large model. ByteDance's GR-3, with 4 billion parameters, outperforms Physical Intelligence's π0 in generalized grasping. These models' iteration speeds depend heavily on computing power access.

Yet gaps remain in high-end training. NVIDIA's H200 still leads in single-card training performance and memory bandwidth, and CUDA's 30-year ecosystem cannot be easily replaced. Huawei's CANN framework is ~95% compatible, but migration costs persist. Critically, advanced manufacturing (5nm and below) remains constrained.

This explains Huang's Beijing visit. He faces a $50 billion and growing market, while Washington's controls spawn a formidable rival—China's domestic AI chip ecosystem. Normalizing civilian mid-to-low-end computing power supplies is NVIDIA's attempt to maintain a computing lifeline for China's robotics industry amid sanctions.

For Chinese firms, this is delicate. Fully rejecting NVIDIA means short-term training efficiency losses and 3–6 month algorithm iteration delays. Full dependence creates strategic vulnerability—another policy clampdown could rupture R&D chains. The optimal path: use domestic chips for baseline security, NVIDIA chips for speed.

04 Brain Competition Shouldn't End in Replacement

Trump's visit won't rewrite humanoid robotics' industrial landscape, but it confirms a reality: in embodied AI, China and the US have formed a de facto technological symbiosis.

What does the US need from China? It's manufacturing capacity, supply chains, and a vast array of real-world deployment scenarios. Morgan Stanley estimates that without Chinese companies' participation, the supply chain cost for Tesla's Optimus Gen 2 would be three times higher than it is now. It's no coincidence that Musk came to China with his mass production anxiety over Optimus.

What does China need from the US? It's cutting-edge breakthroughs in general AI models, high-end computing chips, and original innovations in multimodal algorithms. No matter how powerful the 10,000 robots from Zhiyuan are, their underlying model architectures are still constrained by computing power and algorithmic paradigms.

Two distinct paths are accelerating their divergence—

The US Path: Represented by Figure AI and Tesla, this approach follows a 'general intelligence + software subscription' model, building technological barriers with algorithmic sophistication and generating profits through high-value-added scenarios such as healthcare, military, and high-end manufacturing.

The China Path: Represented by Zhiyuan and Unitree, this approach follows a 'scenario data + hardware mass production' model, diluting trial-and-error costs through scale and cost advantages while accumulating data flywheels through widespread deployment in industrial, logistics, and service scenarios.

There is no inherent superiority between these two paths; they mirror and drive each other. The US's algorithmic advantages require China's manufacturing capabilities for realization, while China's hardware strengths need the US's algorithmic advancements for empowerment. Without algorithms, even the best body is just an empty shell; without a body, even the strongest algorithm is a tree without roots.

Musk and Huang Renxun, both on the visiting delegation list, embody this 'symbiotic relationship'—one is an explorer of the robot's body, and the other is a builder of the robot's brain. Their simultaneous visits to China demonstrate that industrial realities are far more honest than political narratives.

The contest for supremacy in the brainpower of humanoid robots is far from a zero-sum game; rather, it resembles a two-way marathon. The harmonious integration of algorithms with steel, computing power with practical scenarios, and laboratories with factories, constitutes the true essence of this burgeoning industry.

In fact, this paradigm of 'technological symbiosis' is not without historical parallels. During the 1980s, Japan's automotive industry captivated the global market with its remarkably low manufacturing costs and efficient lean production systems. However, when it came to high-end engine control chips and automotive electronic systems, the United States and Germany remained the dominant suppliers. Through fierce competition, these two sides became deeply intertwined, ultimately jointly propelling the global automotive industry to unprecedented heights.

The humanoid robot industry is now unfolding a grander and more accelerated version of this very scenario. In this race, the only certainty is that no one can afford to sit on the sidelines, and no one can succeed in isolation.

*The image is sourced from the internet. Should any infringement occur, please contact us for its removal.

-

![]()

The Dishes of HaiDiLao Are Now Being Served by Autonomous Vehicles! Cold Chain Delivery Costs Plummet by 50%

-

![]()

The Game Changer in Embodied AI: More Important Than Being 'Number One in Evaluation' is Starting to Deliver

-

![]()

Junao Panshi Secures New Financing Round: Investing in Brain-Inspired Intelligence for Cognitive World Models, Propelling Embodied Intelligence into the Next Era

-

![]()

Musk’s Tech Tree Surpasses That of a G7 Nation

-

![]()

XPENG GX: Another Blockbuster Hits the Market

-

![]()

The Trillion-Dollar Arena for Humanoid Robots: Two Trajectories, One Shared Future

-

![]()

Why Is a 'Non-Sexy' Robot Dog Company Worth 13.9 Billion Based on Its IPO from DeepCloud Robotics?

-

![]()

The Whole Story of Great Wall Motors' Foray into Heavy Trucks