Musk’s Tech Tree Surpasses That of a G7 Nation

05/26 2026

05/26 2026

559

559

If you’ve ever played the Civilization series, you’re likely familiar with the abstract mechanics that govern global tech development.

Achieving a phased victory doesn’t always hinge on short-term resource or productivity advantages—it depends on choices. Selecting the right “tech tree” during development can grant temporary technological superiority.

Many players have experienced the frustration of constructing wonders and amassing wealth, only to find, mid-game, that rivals—once considered inferior—are advancing with elite legions or deploying bombers behind their lines.

In hindsight, every move seemed “correct”: deepening advantageous paths, maintaining existing wonders, and generating consistent surpluses. Yet, the game doesn’t reward mediocrity—it rewards strategic route selection.

Applying this experience to reality, Japan in 2026 epitomizes this “frustrating loss.” Holding the world’s strongest industrial system in 1989—with leadership in semiconductors, automotive, consumer electronics, and a treasure trove of anime/gaming IP—it now finds its technological edge nearly erased after three decades. The problem? Its rival isn’t another nation—it’s one man: Musk.

To explain, we borrow a concept from Civilization VI players: the “tech tree.”

By May 2026, Musk’s companies (with xAI merged into SpaceX, avoiding double-counting) are valued at roughly $2.63 trillion.

Japan’s top 10 tech firms by market cap? Combined, $800 billion.

That’s a 3.3x difference. A single individual’s 2026 “tech empire” is valued 3.3 times higher than all of Japan’s leading tech firms combined.

This comparison isn’t perfectly rigorous—valuations differ from market caps, and Musk doesn’t own 100% of these firms. But being “tech-rich enough to rival a nation” isn’t hyperbole.

This shouldn’t happen, but it did. To Civilization VI players, the cause is simple: the two players’ tech tree strategies differ fundamentally.

1. Musk’s Approach

Many call him a genius. After reviewing his career, I see him as a different breed—not a Newton discovering formulas, nor a PhD-driven academic, but a “systemic arbitrage genius” who decoded the 21st-century tech tree unlock order and bet heavily on it.

Many understand the rules, but only Musk systematically built wonders according to them—a talent in itself.

He didn’t start with space or AI; he began with PayPal. Civilization VI players know: wonders require money. Early turns must prioritize cash. He sold PayPal for $180 million, then did something quintessentially “Civilization”: bet on two high-risk tech nodes simultaneously—Tesla and SpaceX.

These seem unrelated—electric vehicles and rockets share no direct tech lineage. But in game terms, they’re identical assets: long build times, multiple prerequisites, but once completed, they unlock entire downstream tech ecosystems. Tesla’s completion unlocks FSD, Optimus, and physical AI; SpaceX’s unlocks Starlink, satellite internet, and global communications dominance. Each unlock jumps his valuation, which he uses to fund the next critical node.

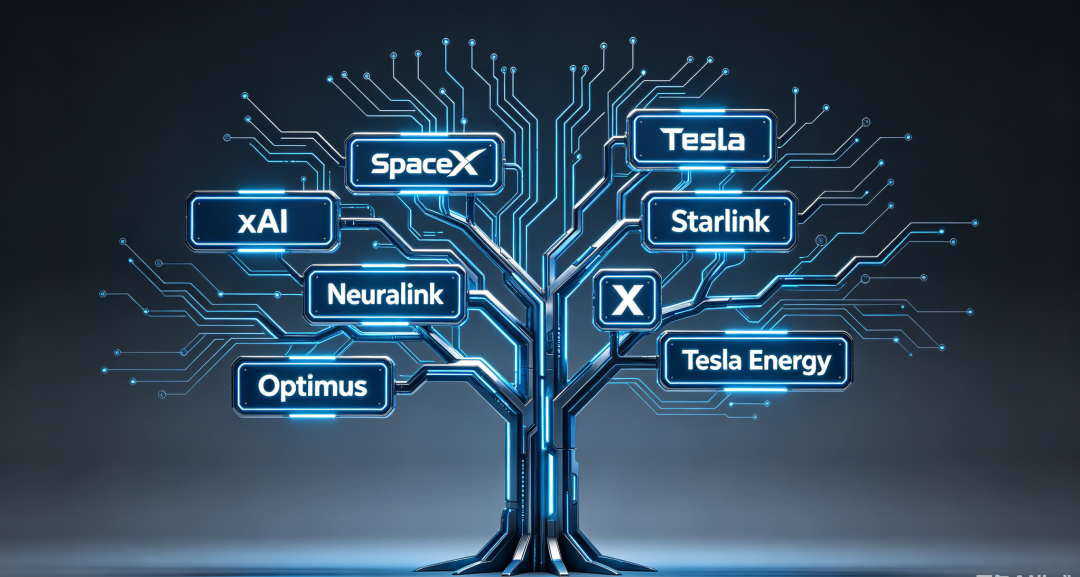

By 2026, this strategy has spawned eight main branches: SpaceX ($800B independent, $1.25T post-xAI merger), Tesla ($1.35T), xAI ($250B independent, merged into SpaceX), Starlink, Neuralink, Optimus, X, and Tesla Energy. Each aligns with a Civilization VI victory condition—scientific, cultural, political, or diplomatic.

Image generated by AI

He’s made mistakes: Twitter lost 72%, The Boring Company burned for a decade without traction, Hyperloop failed entirely, and Robotaxi took nine years to launch 39 vehicles in 2025.

But everyone understands: long-term bets require accepting partial failures. Success in one downstream tech node makes him a winner.

So what did he do right? He grasped the 21st-century tech tree’s rules—rewarding players who fuse “unknown tech points into frontier tech” and punishing those who deepen “known tech.” His failures (Hyperloop/X/Boring) are multi-billion-dollar write-offs, but the tech tree’s logic dictates: a player who bets on 10 and hits 3 is valued 10x higher than one who bets on 5 and hits all 5.

In other words: no risk, no excess return.

Yet this strategy isn’t purely individual brilliance. SpaceX secured NASA’s commercial resupply contracts, accumulating over $10B in government orders. Tesla survived early years via California’s ZEV carbon credit sales.

The Fed’s post-2008 low-rate environment created unprecedented financing for “visionary companies.” Musk’s “long-term wonder bets” only worked under “government orders + capital market premiums + low rates.” His other strength? Choosing a nation that allowed this approach.

Later, he unlocked soft power tech: buying X for $44B (a 72% paper loss) but gaining “public opinion + political influence,” which landed him in the White House during the 2024 election. He then used xAI to register AGI—the “scientific victory” endpoint—before Anthropic.

Twitter’s paper loss became “religious units + political influence” in Civilization VI terms—a perspective needed to grasp the trade-off.

To clarify: “an individual buying media platforms to influence national policy” is far more serious than a Civilization VI metaphor suggests—it’s a true test of 21st-century democracy against super-individuals. This article uses gaming frameworks for structural description, not trivialization.

2. Japan’s Approach

In 1989, Japan was among the highest-rated players globally. No. 1 in semiconductors, automotive, consumer electronics, and anime/gaming IP, with a treasure pool so vast it fueled bubbles—Sony bought Columbia Pictures, Mitsubishi Estate acquired Rockefeller Center. Japanese players thought victory was assured.

Then the bubble burst.

Over 30 years, Japan’s new tech branches have been limited: quantum computing (Fujitsu/RIKEN 256-qubit), new materials (carbon fiber/solid-state batteries), Rapidus’s 2nm project, biopharma (Takeda/Astellas). All followed the same pattern: either stunted or grew into dwarfs. Its main strategy? Maintaining existing wonders.

And it succeeded. FANUC dominated industrial robots for 50 years, holding 11-17% of the global market by 2026. Combined with Yaskawa, Kawasaki, Epson, and Denso, Japanese firms controlled 40-50%. Tokyo Electron held 90% of global coating/developing machines, Lasertec dominated EUV mask inspection, and Sony led CMOS image sensors with 43%—all fruits of Japan’s “maintain existing wonders” strategy.

Japan’s tech bets over 30 years were “correct”—deepening specialized paths and maximizing existing wonders. A stable strategy with decent financials. The issue isn’t specific tech missteps but the absence of nearly all derivative tech bets.

1990s: Skipped the internet. 2000s: Skipped smartphone OS. 2010s: Skipped EVs, AI, commercial space. 2020s: Failed bets on AFEELA and ASIMO.

Each seemingly minor tech node grew into $1.3T, $800B, or $250B wonders by 2026. Japan missed them all.

By 2026, contradictions erupted: AI’s top Japanese unicorn, Sakana AI, was valued at $2.65B—1/94th of xAI. In space, JAXA’s $1B annual budget was 1/800th of SpaceX’s valuation. Honda announced its first annual loss in 70 years on May 14, 2026.

Sony and Honda’s AFEELA EV launched a Delivery Hub in Torrance, California, on March 21, 2026, only to cancel the product four days later (per The Drive and others). In humanoid robots, Honda’s ASIMO retired in 2022 without a successor; SoftBank-controlled Boston Dynamics was sold to Hyundai in 2020—Japan even lost the parent company of Spot the robot dog.

Frankly, at this point, players should sigh. This isn’t about a single wrong move in one year—it’s 30 years without a new move. Japan’s strength (“defending old tech”) and weakness (“30 years without new branches”) are structurally linked. Now, the real question.

3. Can Japan Emulate Musk?

Some argue Japan tried. SoftBank’s Masayoshi Son is the counterexample.

He’s Japan’s closest approximation to Musk—bold bets, visionary, mobilizing billions in capital. Vision Fund I alone invested $100B in AI and future tech.

But here’s the kicker: all his big wins were outside Japan’s tech tree. Alibaba profits came from China’s internet, Arm from British semiconductors, OpenAI from America’s AGI.

Son—the Japanese player most resembling Musk—built his tech tree abroad.

This stings more than “Japan’s tech stagnation.” It shows: Japan isn’t incapable of producing Musk-like figures—it just can’t retain them. They must go to the U.S. or China to win.

Can Japan emulate Musk and build 21st-century tech trees domestically?

Almost certainly not. Not because Japan lacks desire, but because five structural constraints weigh it down. Each is debatable alone, but together, they lock the system.

First, capital mechanisms. Musk grew Tesla to $1.3T because U.S. secondary markets reward “vision” with premiums—P/E ratios detach from current profits, discounting 30 years for “if AGI happens.” Japanese investors distrust this. Japan’s markets prefer dividends, stability, and PE ratios around 10x, rarely opening windows for “long-term visionary firms.” Telling Tesla’s story to Tokyo’s First Section would likely yield 1/100th the U.S. funding. Sakana AI raised $135M Series B at $2.65B valuation in Silicon Valley—if it IPO’d in Tokyo, its valuation might start at 1/10th.

Second, talent drain. Silicon Valley attracts global top talent—immigration-friendly, English-speaking, loose visas, fully marketized salaries. Japan is insular—Japanese-language workplaces, closed to foreigners, and seniority-based pay (wages by tenure, not ability). AI experts in Japan earn 1/3rd of Silicon Valley salaries. Sakana AI founder David Ha returned from Google Brain—an exception—but its core tech staff were still globally recruited, not homegrown.

Third, decision-making. Musk decides alone. Tesla’s FSD bet went from idea to execution in <24 hours—a tweet sufficed as announcement. Japanese firms use the ringi-sei (proposal) system, requiring layered approvals, averaging 6-12 months. Sony’s AFEELA cancellation took ~2 years of governance review. While U.S. firms pivot in 24 hours, Japanese firms await next month’s management meeting.

Fourth, education and social tolerance. America rewards “dropout entrepreneurs”—Gates, Zuckerberg, and pre-PayPal Musk left formal PhD programs. Japan’s top engineers from Tokyo University most likely join Sony/Toyota/Hitachi as lifetime employees, not to create a Tesla. Japanese society stigmatizes failure—a 30-year-old entrepreneur who fails is permanently marginalized in big firms. Under this culture, no one bets on “10-year maybes,” let alone three simultaneously.

The fifth is political structure. Musk can buy X to control the media, enter the White House to influence policies, and stir up elections—this kind of 'super-individual bypassing the state' approach is impossible in Japan. Japan's postwar political tradition suppresses the political influence of super-individuals. After the disintegration of the zaibatsu era, no one has been able to control enterprises, media, politics, and capital in one hand like Musk. Even if Japan produced a player of Musk's caliber, the state apparatus would use various means to make him 'gently shrink.'

Putting these five constraints together, it becomes clear that Japan is not unwilling to pursue new technologies in the 21st century. Rather, its capital mechanisms, talent systems, decision-making systems, educational culture, and political structure have collectively locked away its ability to do so. This is not a question of 'willingness' but of 'capability.'

Going deeper, these five constraints are interconnected. Modifying any one of them requires adjusting the other four. To loosen capital mechanisms, corporate laws and Tokyo Stock Exchange rules must be revised. To enable talent siphoning, immigration laws must be changed. To accelerate decision-making, the ringi system must be dismantled. To incentivize entrepreneurship, the education system must be reformed. To allow super-individuals, postwar political traditions must be altered.

Any one of these is a 20-year project. Combined, they explain why Japan has not truly altered this structure in the 36 years since 1989.

4. The Numbers Speak

Only by revisiting these numbers can we truly grasp their weight.

Musk's personal net worth was $728-820 billion in May 2026, equivalent to 17-19% of Japan's 2025 nominal GDP. One person's assets equal nearly one-fifth of a G7 nation's entire annual economic output.

The total valuation of Musk's companies is approximately $2.63 trillion, 3.3 times the combined market capitalization of Japan's top 10 tech companies (approximately $800 billion, including Kioxia AI's post-surge valuation). Even if Toyota and SoftBank Group are included, Japan's top firms reach about $1.24 trillion—Musk's companies still represent 2.1 times that.

SpaceX alone is valued at $800 billion to $1.25 trillion. JAXA's annual core budget is about $1.5 billion, rising to $3 billion with FY2025's ¥300 billion supplementary budget—SpaceX remains 300-500 times larger. Even factoring in Japan's Space Strategy Fund's 10-year ¥1 trillion (approximately $6.5 billion) total, SpaceX is still over 120 times its size.

Tesla invests $6.4 billion annually in R&D, supporting a $1.35 trillion market cap; Toyota invests $9.1 billion annually, supporting a $237 billion market cap. For every dollar of R&D, Tesla generates 12 times the market cap of Toyota. Japan's three largest automakers invest $18.6 billion annually in R&D—2.9 times Tesla's

In the bygone era, the 'nation' stood as the fundamental unit propelling technological progress. The United States entrusted NASA with the monumental task of landing on the moon, while Japan leaned on MITI to spearhead advancements in semiconductors.

However, under the contemporary framework, the 'nation' as a singular entity in this arena has become sluggish, costly, and fragmented. A nation necessitates a consensus among the government, corporations, academia, and society to make decisions—a super-individual, in contrast, relies solely on their own judgment. Technological strides in the 21st century are shrinking the smallest unit from the 'nation' to a novel type of participant, comprising a 'super-individual + globalized capital + AI leverage'.

This might seem like a phenomenon exclusive to the 21st century, but that's not entirely accurate. Back in 1916, Rockefeller's fortune approximated nearly 2% of the U.S. GDP. Carnegie's steel empire, Ford's automotive innovations, and Vanderbilt's railroad network all encountered 'individual vs. nation' scenarios at their zenith. Historically, this signifies a 'cyclical resurgence of capital concentration'—once during the late 19th-century Gilded Age, again in the 1920s, and now, for the third time, in 2026.

Yet, there's a difference in scale this time around: Rockefeller focused on a single technological domain (oil), Ford on another (automobiles)—Musk is pursuing eight simultaneously. This is the result of cyclical trends combined with technological intricacy. Hence, 'one individual vs. a G7 nation' is neither entirely novel nor a mere repetition—it's a fusion of historical patterns and technological acceleration. In this new paradigm, the 'national' aspect of G7 nations is undergoing redefinition.

Who will be next in line? Germany? France? The UK? All confront the same looming threat—not Musk per se, but the new type of participant he embodies.

The Japan of 1989, boasting the world's most robust industrial system, didn't succumb to South Korea or the U.S.—it fell to a new type of participant that only emerged in the 21st century. There's no resetting this game. Japan now has two paths: either acknowledge that the era has relegated 'nations' to a secondary role and embrace a 'component supplier + hidden champion' status, or remain mired in the 1989 mindset, pretending the rules haven't evolved.

But the tickets to the next wave of technological revolution will still be issued by those who can craft compelling visions, mobilize capital, and attract talent. Japan lacks all three: vision-driven super-individuals, capital mechanisms willing to take bold risks, and a cultural climate that welcomes global talent.

Some games aren't just about making the wrong strategic moves—the very environment of the game has transformed.

-

![]()

The Dishes of HaiDiLao Are Now Being Served by Autonomous Vehicles! Cold Chain Delivery Costs Plummet by 50%

-

![]()

The Game Changer in Embodied AI: More Important Than Being 'Number One in Evaluation' is Starting to Deliver

-

![]()

Junao Panshi Secures New Financing Round: Investing in Brain-Inspired Intelligence for Cognitive World Models, Propelling Embodied Intelligence into the Next Era

-

![]()

Musk’s Tech Tree Surpasses That of a G7 Nation

-

![]()

XPENG GX: Another Blockbuster Hits the Market

-

![]()

The Trillion-Dollar Arena for Humanoid Robots: Two Trajectories, One Shared Future

-

![]()

Why Is a 'Non-Sexy' Robot Dog Company Worth 13.9 Billion Based on Its IPO from DeepCloud Robotics?

-

![]()

The Whole Story of Great Wall Motors' Foray into Heavy Trucks