AI Stranded at the Dock of the Era

05/28 2026

05/28 2026

430

430

Starred Focus: Embarking on the Age of AI Technology and Great Navigation  Columbus' Santa Maria

Columbus' Santa Maria

Agents are becoming the most sought-after “workers” in the tech world. However, while agents can work, they can't spend money—the AI industry has waves but no shore. — Brother Shui

Over the past two decades, digitization has democratized information flow, transforming it from scarce to abundant and from asymmetric to symmetric. However, the core of commercial transactions has never been just about information flow; it is more critically about value transfer.

In traditional e-commerce models, information flow and value flow are deeply intertwined: users search, compare prices, add items to their cart, and pay, with information processing and fund transfers completed by the same person in a single operation. Payment is merely the final confirmation step in the transaction.

Today, the agent economy seeks to break this bond—users only need to express their intentions and set budget boundaries, such as “Book me a flight to Hangzhou tomorrow within a budget of 800 yuan, avoiding red-eye flights,” and AI can independently complete the entire process of searching, comparing prices, filtering, and placing the order. Intelligence can now handle the entire value creation chain but gets stuck at the final step of value exchange.

Trillions in waves dare not reach the shore

The capabilities of intelligent agents are now undergoing exponential growth, enabling tasks like price comparison negotiations, tool utilization, and inter-agent transactions to be completed in seconds—tasks that would take humans half an hour. Juniper Research predicts that global agent-based commerce transaction volumes will skyrocket from $8 billion in 2026 to $1.5 trillion in 2030. Capital is rushing in, platforms are competing to lay out their strategies, and technical teams are delving deep into reasoning and multi-step execution capabilities, creating a massive wave of AI commercialization.

The smarter AI becomes, the more fragile commerce becomes. Every significant leap in convenience brings about the collapse of the underlying logic of security. In the old commercial world, payment was the final step of a transaction; in the new AI world, payment is the foundational base for intelligent commerce—first, a credible rule system must be established, followed by autonomous machine commerce. History has repeatedly proven: it is never transaction explosions that generate trust; rather, it is the refinement of trust mechanisms that unleash transaction potential. What holds back AI commercial development is not code or technology but the lack of a unified consensus across the industry—the consensus on rules for A2A (Agent-to-Agent) and A2M (Agent-to-Merchant) transactions.

On May 26th, at the recently held AI Payment Ecosystem Conference, Ant Group CEO Han Xinyi responded to this industry proposition: “When 1.4 billion people may have 140 billion agents active in economic activities in the future,” the industry will undergo a fundamental change: the subjects of commercial interaction are shifting from trust between people to trust between people and agents, as well as between agents themselves.

This means that in every future price comparison, order placement, and settlement, the initiator will no longer be a human but a digital intelligent agent representing a human. How to make agents trusted by users and by other agents is the true underlying proposition of the agent era. Trust is no longer a security patch but a prerequisite for commercial operation.

This scene is reminiscent of ports at the end of the 19th century: steamships had already been built, with far greater power than traditional sailing ships, yet the dock berths, cranes, and storage facilities were still designed for sailing ships. The current commercial and payment systems are not yet prepared for “machines actively spending money.”

After 300 million transactions, rules begin to take shape

Commerce truly enters the AI era when intelligent agents start spending money.

Many mistakenly believe the issue lies in interface connectivity, when in fact, payment systems have long opened up APIs, and agent access channels are unimpeded.

AI payment is not merely adding an API interface to existing systems; that is just a simplistic channel mindset. True AI payment is a complete transaction operating system, encompassing a full-chain rule system for authorization management, intention translation, execution monitoring, and accountability tracing.

At this ecosystem conference, Alipay also presented its answers for large-scale implementation: AI agent payments have surpassed 300 million transactions, supporting 95% of general-purpose agent frameworks, becoming a large-scale commercially viable AI-native payment infrastructure. Simultaneously, it officially released a full-stack AI payment product matrix, including four core products—AI Pay, AI Collect, AI Wallet, and Token Pay—building a complete ecosystem covering users, developers, and merchants.

The core significance of 300 million AI-native payment transactions is that AI payment is no longer a concept on paper; the entire transaction rule system has been validated in real-world scenarios, and transactions between agents are now occurring.

AI Wallet—implementation of tiered authorization. It is also the world's first native product to incorporate agent permission management into personal financial systems. Users can set limits and permissions for different agents, monitor transactions in real-time, and halt them at any time. This institutional design transforms users' entrusted trust in agents and the trust verified by other agents into fully controllable, deterministic rules—eliminating users' fears of machines spending irresponsibly. Data shows that in the first month of the product's launch, users set an average of over 12 million authorization rules per day, proving that fine-grained authorization is a universal necessity.

Token Pay—fills the gap in intention settlement, compressing payment granularity from “monthly subscriptions” to “per-token billing,” enabling independent pricing and settlement for every minor AI service invocation, establishing a unified value benchmark for agent interactions.

Paired with the previously implemented ACT protocol (Agent Common Interaction Language, iterated from 1.0 to 2.0 within five months, co-built with over 20 manufacturers including Xiaomi, Zhipu, and BYD), AI Pay and AI Collect (covering C-end payments and B-end collections), and an intelligent security system (four-layer risk control, scoring full marks in security evaluations by China Academy of Information and Communications Technology's Taier Laboratory), Alipay has constructed a complete chain from trust protocols, risk control execution, payment closure, asset management, to unified settlement. It is not a simple superposition (superposition) of products but a vertically integrated transaction operating system.

This operating system is the infrastructure for trust logic. It is not a payment channel but the foundational rules of AI commerce. More profoundly, what it is doing goes beyond the scope of “payment infrastructure”—essentially, it is customizing a set of rule consensuses for AI commercial civilization, not making decisions for users but enabling all participants to act autonomously within a trustworthy framework.

Commercial Space is Opening Up

Once the foundational rules are in place, the potential of AI commerce is fully unleashed.

Gartner predicts that by 2028, 15% of daily work decisions will be made by AI agents, and two-thirds of enterprise software applications will incorporate agent-based AI capabilities. However, Deloitte surveys show that currently, only 11% of enterprises have deployed agent AI in actual production, with the vast majority still wait and see (on the sidelines). Once the “last mile” of payment is fully connected, various innovative scenarios will transition from concept to reality.

Automatic commerce between agents spurs the microservice economy

A user's travel agent interfaces with a hotel booking agent to complete a room reservation, involving two layers of value exchange: the user purchasing room service and the capability invocation between the two agents. Services provided by the hotel agent, such as inventory queries, quote locking, and room reservations, inherently possess commercial value.

Token Pay's per-token billing model enables independent settlement for every API call, image generation, and inventory query. Complex business negotiations and large upfront deposit requirements are eliminated, allowing numerous small and medium-sized developers to package their AI capabilities as paid services, charging per invocation. Projects like AutoToll, ElevenLabs, and Replicate have already validated feasibility, with micropayment models becoming the mainstream settlement method for AI services.

Explosion of personal agent clusters and proliferation of multi-terminal scenarios

In the future, everyone will have a suite of agent teams specializing in travel, shopping, finance, scheduling, and subscription management. AI glasses, smart car cockpits, and AI earphones will serve as extended entry points for agents. Relying on fine-grained authorization and safety cutoff mechanisms, these AI assistants can autonomously complete tasks within their permissions. Fetch.ai has already achieved fully autonomous cases: while the user is offline, their personal AI proactively interfaces with a friend's agent to coordinate gatherings, book restaurants, and complete payments without human intervention. The personal assistant economy will fundamentally transform people's lives and service models.

Intelligent merchant operations and upgrades for millions of offline stores

Agents are not just for C-end users; they are also core tools for merchants to reduce costs and increase efficiency. Alipay's merchant agent “Xiaoyu,” acting as an AI store clerk, can be directly deployed in stores to provide order-taking services, product recommendations, member operations, and customer acquisition marketing throughout the entire process. Combined with the “Tap to Pay” terminal, it enables automated offline store operations. Small and medium-sized merchants deploying dedicated operational agents can automatically respond to inquiry, comparison, and ordering requests, achieving full automation in negotiation, contracting, and settlement, drastically reducing operational costs. Even individuals with only inventory can rely on an agent system to complete the entire operational chain from marketing to after-sales, launching online businesses with zero team requirements.

Automation of financial intelligence drives upgrades in professional fields

In finance, AI agents can in real-time capture news, public sentiment, and financial report data, adjusting trading strategies in milliseconds to mitigate risks. Platforms like AgentSmyth integrate multi-module AI to automatically generate trading insights. With the implementation of a trustworthy payment system, such intelligent agents can not only read information but also automatically subscribe to paid data sources, procure algorithm services, and settle external invocations, forming a complete commercial closed loop (loop) for the entire intelligence industry chain.

Rise of long-tail AI applications and democratization of industry thresholds

Previously, developing AI applications required enterprises to independently build payment systems, design authorization rules, and handle transaction disputes, with high costs deterring long-tail developers. Now, AI Collect's low-threshold collection capabilities enable all types of entities, from large enterprise-level services to individual handicraft shops and solo developers, to easily enter the market. AI commercialization is no longer exclusive to big players; an ecosystem of all the people (universal) participation is gradually forming.

Smooth cross-border intelligent transactions reshape foreign trade

Leveraging Token Pay's global payment capabilities, agents can automatically handle currency conversions, tariff calculations, and cross-border settlements. Domestic users' shopping agents can directly interface with overseas e-commerce platforms, while overseas demand can precisely match domestic supply, evolving cross-border retail from “people finding goods” to “machine-precise matching.” Whoever first establishes a mature cross-border AI payment network will dominate the next generation of cross-border trade.

Tian Feng, Dean of the Fast Thinking Slow Research Institute, predicts: “In 5-8 years, the number of payment instructions issued by AI will surpass those manually issued by humans.” These scenarios are not mere fantasies; the implementation of AI payment infrastructure has already proven the formation of transaction rules adaptation (adapted) to the new economy. Next, it only requires attracting more scenarios, developers, and merchants to join, and transaction volumes will experience exponential growth.

The AI Payment Ship Has Arrived

Three hundred million transactions may seem light in volume, but the rules are now in place. Competition in the new commercial cycle has never been about chasing short-term trends but about pre-laying the foundational transaction order scarce across the entire industry and embedding infrastructure for cyclical growth.

Reviewing Alipay's over two decades of development, every time it launches a new payment product, it is essentially building a “great ship” to carry the next generation of commerce:

In 2004, escrow transactions resolved the issue of mistrust in online shopping, laying a solid foundation of trust for e-commerce, helping the industry grow its transaction volume by over 40,000 times in a decade, and forging the trillion-dollar e-commerce era;

In 2011, barcode payments illuminated offline mobile commerce, enabling China's mobile payment penetration rate to reach 86%, ranking first globally;

In 2026, facing the trust gap in the AI industry, the full-stack AI payment infrastructure was born. This is the third time Alipay has internalized new types of transaction costs into infrastructure shared by the entire industry.

Currently, industry exploration continues, with various solutions focusing on different aspects. Alipay's full-stack system is not the only path, nor necessarily the final standard, but it provides a set of vessels that promote the activity of 140 billion agents in the future and deliver value to AI commerce.

The AI industry never lacks surging waves; in an era of fierce winds and high tides, what is needed most is not a kickboard (float) that drifts with the waves but a giant ship (giant ship) capable of breaking through and sailing far.

Now, the ship has arrived. Beyond the dock, a new continent is in sight.

-

![]()

AI Stranded at the Dock of the Era

-

![]()

New Progress! OFILM's Acquisition of Minority Stake in OFILM Microelectronics Approved

-

![]()

From Setbacks to a Potential 1.6 Billion Yuan Deal: What Has Seer Technology Achieved?

-

![]()

Why Has a Former Bottom-of-the-Barrel Destination Become a New Hotspot for Chinese Brands Going Global? | Xiaguang FM

-

![]()

The Hidden Battle of 618 Efficiency: Kunshan Asia No.1, AI, and JD.com's Logistics Performance This Year

-

New Energy Vehicle Safety Baseline Further Strengthened: MIIT Initiates 2026 Safety Hazard Inspections

-

![]()

China Office Intelligent Agent Platform Market Research Report 2026

-

![]()

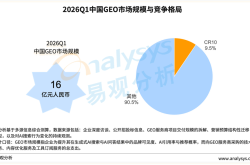

Analysys: China's GEO Service Provider Market to Reach Approximately 1.6 Billion Yuan in Q1 2026, with Top 10 Industry Concentration Below 10%