2026 AI Unicorn Distribution: Nearly 40% Gather in Zhongguancun Science Park

07/10 2026

07/10 2026

527

527

According to Hurun's '2026 Global Unicorn Index', artificial intelligence (AI) emerges as the most prominent growth sector this year. Globally, there are 215 AI unicorn companies, marking an increase of 87 from the previous year. Their combined value accounts for 36% of the total value of all global unicorn companies, representing the highest proportion across all industries.

China boasts 47 AI unicorns, ranking second globally. Supported by an analysis from Huoshi Create's 'Huoshi Xinglan' industrial investment intelligence model, this article dissects the industrial landscape of these 47 AI unicorns from three perspectives: valuation landscape, regional distribution, and industrial chain distribution.

01 Valuation Landscape

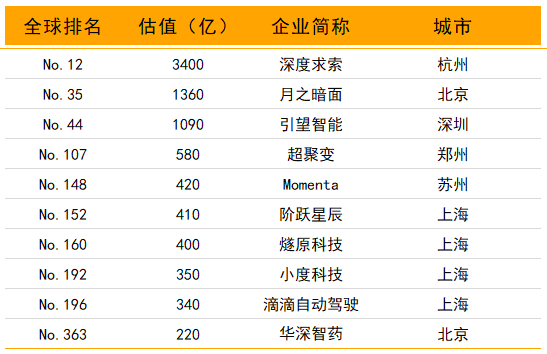

The combined valuation of the 47 AI unicorn companies stands at RMB 1.2 trillion, with Deepseek leading by a substantial margin at RMB 340 billion, accounting for roughly 28% of the total valuation.

Top 10 AI Unicorns in China

Source: '2026 Global Unicorn Index'

Overall, the valuation concentration among AI unicorn companies is extremely high at the top. The top three companies (Deepseek, Yuezhi'anmian, Yinwang Intelligence) collectively hold a valuation of RMB 585 billion, accounting for over 45% of the total valuation of all 47 companies.

Competition is fierce in the mid-tier range. The valuation range of RMB 10 billion to RMB 60 billion encompasses 22 companies, spanning various sub-sectors such as AI chips, autonomous driving, and AI applications, making it the most competitive segment.

At the tail end, companies have similar valuations. The valuation range of RMB 6.8 billion to RMB 10 billion also includes 22 companies, with relatively minor valuation differences, indicating that these companies have not yet established significant differentiation.

02 Regional Distribution

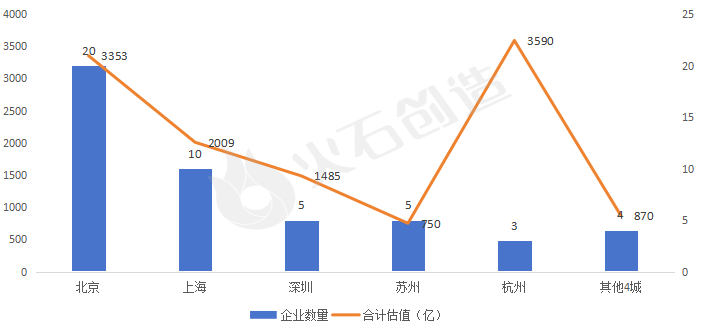

The 47 AI unicorns are primarily located across eight cities: Beijing, Shanghai, Suzhou, Hangzhou, Shenzhen, Wuhan, Zhengzhou, and Chongqing. Beijing leads with 20 companies, accounting for 42.5% of the total, with a high concentration in large model foundations, AI underlying computing power, and cutting-edge AI applications. Shanghai follows with 11 companies, covering autonomous driving, AI chips, and vertical domains. Additionally, Suzhou and Shenzhen each have five companies on the list, while Hangzhou has three.

Distribution of AI Unicorns by City. Source: 'Huoshi Xinglan' Industrial Investment Intelligence Model

From the perspective of development zone distribution, over 85% of AI unicorns are situated in national-level development zones, with national-level high-tech zones accounting for 70%.

Zhongguancun Science Park (including its various sub-parks, hereinafter) is home to 18 unicorns, accounting for a high 38.3%. Representative companies include Yuezhi'anmian, Huashen Zhiyao, Kunlunxin, Megvii, and 01.AI. Leveraging resources from top universities like Tsinghua and Peking University, as well as a robust venture capital atmosphere, Zhongguancun has become China's core hub for AI fundamental research and algorithm innovation.

Zhangjiang High-Tech Zone is home to nine unicorns, accounting for 19%. Representative companies include Jieyue Xingchen, Enflame Technology, Xiaodu Technology, Didi Autonomous Driving, and Yitu Technology. Zhangjiang boasts unique industrial advantages in AI chips, autonomous driving, and the intersection of biopharmaceuticals and AI (AI for Science).

Shenzhen High-Tech Zone has three unicorns on the list, including Yinwang Intelligence, Xverse, and Zoyu Technology. Relying on its strong hardware manufacturing capabilities and electronic information industry foundation, Shenzhen excels in 'software-hardware integration' tracks such as AI hardware, smart cars, and embodied intelligence.

Distribution of AI Unicorns in Development Zones

Source: 'Huoshi Xinglan' Industrial Investment Intelligence Model

03 Industrial Chain Distribution

Based on a cross-analysis of the 'Huoshi Xinglan' Industrial Investment Intelligence Model's semiconductor industry dataset and the Hurun list, the distribution of unicorns across various segments is as follows:

Distribution of AI Unicorns Across the Industrial Chain

Source: 'Huoshi Xinglan' Industrial Investment Intelligence Model

Large models, autonomous driving, and AI chips represent the three core tracks. Among them, there are eight companies in the large model sector, characterized by high valuations and intense competition. From a technological standpoint, general-purpose large models are evolving towards multimodality and intelligent agents (Agents), with both open-source and closed-source approaches coexisting. There are nine companies in the autonomous driving sector, with accelerated commercialization of L3/L4 autonomous driving and collaborative evolution of algorithms, chips, and vehicles. There are five companies in the AI chips/computing power sector, where, influenced by geopolitical factors, the replacement of domestic computing power is accelerating, with equal emphasis on training and inference chips, making it a national strategic high ground.

Vertical applications are flourishing across various fields such as healthcare, finance, and industry, where AI companies with industry-specific know-how are gaining higher valuation premiums by leveraging data barriers and scenario advantages.

With large models as the foundation, infrastructure empowerment, and scenario-based implementation, a complete AI industrial ecosystem is taking shape. As large model technologies continue to mature and computing power infrastructure improves, AI will deeply penetrate various industries. Chinese AI unicorn companies need to continuously increase investment in fundamental technology R&D and accelerate commercialization efforts.

Regions should seize this historic opportunity to accelerate the cultivation of new quality productive forces through precise industrial investment and ecosystem construction. The 'Huoshi Xinglan' Industrial Investment Intelligence Model offers skills such as industrial chain attraction, supply chain enterprise sourcing, and enterprise attraction plans that can be deployed on demand, upgrading investment decisions from experience-driven to data-intelligence-driven, helping regions precisely position themselves and seize opportunities in the AI industrial landscape.

-

![]()

MiniMax Shares Unlock: Cornerstone Shareholders Show Long-Term Optimism, Yet Stock Plummets Nearly 30% in Two Days; Zhipu Also Sees Nearly 20% Drop Today

-

![]()

Single-Day Plunge of 40%: The 'First AGI Stock' Faces More Than Just Share Price Concerns

-

![]()

Ricoh and Fuji Hike Prices on Legacy Edge; Insta360 Poised to Disrupt Mirrorless Camera Market

-

![]()

Ricoh and Fujifilm Raise Prices in Tandem, Relying on Established Reputations; Insta360 Poised to Disrupt Mirrorless Camera Market

-

![]()

Strategic Shift in Photoelectric Sensing: Maxvision Secures Controlling Stake in CAS Optotech

-

![]()

Optical Communication and Robot Vision: OFILM’s Bold Transformation Amid a 460 Million Yuan Loss

-

![]()

From 100,000-GPU Computing Might to Industrial Efficiency: The Logic Behind AI4S-Driven Intelligence

-

![]()

OpenAI, Grok, and Meta Release Three Major Models: Who is the King of Cost-Effectiveness?