Single-Day Plunge of 40%: The 'First AGI Stock' Faces More Than Just Share Price Concerns

07/12 2026

07/12 2026

339

339

On the day its shares became tradable, Unisound's stock price plummeted by 41.19%, sending shockwaves through many investors.

The implications of Unisound's stock price trend extend beyond the company itself; it serves as a mirror reflecting the issues AI companies face in the capital markets—issues they are reluctant but compelled to confront. When the narrative of scarce opportunities ends, technological storytelling must still withstand the test of commercial realization. Can the 'AGI' label continue to support long-term valuations?

In late June 2025, Unisound listed on the Hong Kong Stock Exchange, earning the title of 'Hong Kong's First AGI Stock.' During its initial public offering phase, fueled by AI hype and scarce stock availability, the company's share price surged rapidly, peaking at HK$879 and briefly exceeding a market capitalization of over HK$62 billion.

By September 2025, Unisound's share price continued to decline, exacerbated by the impact of share lock-up expirations. The stock price fell to as low as HK$61.2. On July 9, 2026, it closed at HK$73.85, with a total market capitalization of approximately HK$5.5 billion, representing a vaporization of over 90% from its peak.

The selling pressure triggered by the lock-up expiration was merely superficial; beneath it lay a profound shift in the capital market's valuation logic for AI companies. During the large model craze, technological narratives could sustain imaginative valuations in the early stages of listing, but long-term value must ultimately return to rigorous assessments of business models and profitability.

However, signs of pressure on Unisound had emerged earlier.

Just half a year after its listing, Unisound embarked on intensive financing.

On January 16, 2026, Unisound conducted its first share placement, issuing 780,000 new H-shares at HK$252 each to no fewer than six placees, representing a discount of approximately 16% from the previous trading day's closing price. The net proceeds amounted to approximately HK$192 million.

Subsequently, the company carried out second and third placements in February and May, with placement prices of HK$310 and HK$228, respectively. The discount rates widened to 17.7% and 19.89%, raising net proceeds of HK$307 million and HK$380 million, respectively. Typically, the issue price should not be discounted by 20% or more from the benchmark price.

The cumulative proceeds from the three placements exceeded HK$880 million, more than four times the net proceeds of HK$206 million from its IPO.

For AI companies in the midst of large model competition, continuous funding is essential for R&D investment, computational infrastructure construction, and talent acquisition. Financing is thus justifiable.

Unisound's founder, Huang Wei, had previously stated that the period from 2023 to 2025 would be a 'warm-up race' for large model development, with true competition beginning only in 2026.

By the end of 2025, the company's cash and cash equivalents stood at approximately RMB 340 million. Generally, Hong Kong main board-listed companies are prohibited from issuing new shares within six months of listing. Unisound's first placement occurred around six and a half months after listing, indicating a clear intention to stockpile resources for future competition through sustained and urgent financing.

From the perspective of fund allocation, the proceeds from the three placements were directed toward several core aspects of the large model competition, including foundational computational infrastructure, cutting-edge technological R&D, and the exploration of new markets and scenarios.

Nevertheless, frequent financing has raised external doubts about the company's capital efficiency and resource allocation capabilities.

Announcements revealed that as of April 30, 2026, 55.7% of the approximately HK$192 million raised in the January placement remained idle. Of the approximately HK$307 million raised in the February placement, only about HK$7 million had been utilized, leaving over 97% of the funds untouched.

In response, an article by Sina Securities raised questions: Was the strategy overly forward-looking, necessitating continuous capital reserves for the future, or had current business progress fallen short of expectations, rendering previous funds undeployable as planned?

If the financing pace raised market doubts, the release of the U2 large model further amplified concerns about the 'gap between technology and commercialization.'

On June 8, Unisound unveiled its U2 large model, eschewing blind parameter accumulation and output length competition in favor of emphasizing continuous execution capabilities for real-world tasks. U2 achieved impressive results in domestic and international authoritative evaluations, with some media interpreting its release as Unisound's 'DeepSeek moment.'

However, this 'positive development' failed to offset the day's market decline; the company's share price fell nearly 11% and broke below its issue price of HK$205.

In the past, AI companies could attract attention based on model parameters and benchmark rankings. However, as large model competition intensifies, the market is increasingly focusing on the gap between technology and commercialization.

While U2's design philosophy indeed addresses commercialization concerns, a lengthy chain of productization, customer acquisition, and scalable deployment lies between philosophy and performance.

For Unisound, U2 demonstrates technological and product capabilities, but the market needs to see how these capabilities translate into tangible revenue and profits.

Currently, large model companies have generally followed two development paths. One emphasizes foundational model capabilities, expanding model invocation scale by enhancing intelligence limits. The other seeks to embed AI capabilities into specific industries, achieving commercial value by solving real-world business problems.

Zhipu emphasizes the platform value of foundational model capabilities, with its core logic centered on enhancing model capabilities and application coverage to unlock value through larger token usage scales. Its business logic can be summarized as: AGI commercial value = intelligence ceiling × token consumption scale. This represents an experiment in exchanging 'generality' for 'scale effects.'

Unisound, on the other hand, has chosen the latter path of 'industry deep dive,' attempting to extract value in specific scenarios such as healthcare and rail transit through 'strong foundational models + deep applications.'

This is also why Unisound proposes that 'an AI company's industry value = intelligence density × token value.' On the industrial side, clients not only demand industry-specific model expertise but are also constrained by local computational resources, generally being more sensitive to deployment costs and inference efficiency. Therefore, Unisound emphasizes 'intelligence density'—achieving sufficiently high intelligence levels with smaller parameters and lower costs to meet cost-effective demands in professional scenarios.

This logic is reflected in the U2 model. Rather than pursuing trillion-parameter scales, U2, with fewer than 300 billion parameters, attempts to achieve superior efficiency ratios in specific scenarios.

Theoretically, in this process, general-purpose foundational models continuously absorb vertical domain knowledge, becoming increasingly specialized, while vertical applications grow stronger due to enhancements in general-purpose foundational model capabilities, forming a virtuous cycle.

Taking healthcare as an example, medical AI must integrate into the workflows of doctors and hospitals. Truly implementable medical AI requires an understanding of professional medical knowledge, the ability to process private domain data, and compliance with the healthcare industry's safety, regulatory, and reliability requirements. This means that while general-purpose models provide foundational intelligence capabilities, industry applications still require scenario-specific experience and industry know-how.

In the past, Unisound has focused on technological accumulation in areas such as speech recognition, natural language processing, and human-computer interaction, while continuously deploying in vertical scenarios like healthcare and the Internet of Things. Compared to later entrants into the large model field, Unisound hopes to differentiate itself through long-standing industry experience.

Again, taking the healthcare sector as an example, Unisound has served over 400 tertiary hospitals and more than 500 enterprise clients, accumulating substantial real-world business data.

However, this 'deep accumulation' presents a different face at the commercialization level: project-based delivery. The business processes and system environments vary significantly across different hospitals, forcing AI companies to invest substantial manpower in customized development. More projects mean busier teams, but without scale effects.

Unisound hopes that large models can break this deadlock.

In the era of large models, companies can modularize and standardize certain capabilities through unified model foundations and intelligent agent frameworks, thereby reducing delivery costs and improving replication efficiency.

Huang Wei once cited an example: the company's insurance claim audit system previously required lengthy customized development, but with large model capabilities, clients could go live after simple configuration, reducing delivery cycles from three months to one week and cutting costs by approximately 80%.

If this model proves viable, Unisound aims to achieve not just growth in AI projects but a transformation in its business model: shifting from project delivery-based revenue to sustain creating value through standardized products and intelligent capabilities.

Ultimately, different AGI paths must all answer the same question: How can technological capabilities translate into commercial returns? The foundational model path needs to prove that model scale can generate sustained invocation value, while the industry intelligence path must demonstrate that industry accumulation can transform into replicable products and revenue.

This is also the issue the market truly cares about.

From its 2025 operating data, Unisound still has considerable ground to cover before achieving 'replicable products and revenue.'

In 2025, Unisound reported revenue of RMB 1.211 billion, a 29% year-over-year increase. Notably, its large model-related revenue surged more than tenfold in 2025.

However, Unisound's overall revenue primarily came from AI solution projects for government and enterprise clients (e.g., intelligent rail transit, full-stack voice solutions for smart cockpits, and healthcare informatization), mostly representing typical project-based system integration businesses.

For instance, in the smart living segment, 'solution revenue' accounted for approximately 69.8%. Such businesses generally recognize revenue based on contract fulfillment progress or acceptance timelines, exhibiting distinct phased or one-off characteristics.

Project-based work is characterized by 'one-time deals' or 'phased delivery,' making it difficult to accumulate into sustainable subscription revenue.

Customer retention rate data further supports this point. In its core smart healthcare business, the customer retention rate declined from 70.4% in 2022 to 53.3% in 2024. A 53.3% retention rate means that nearly half of clients did not convert into long-term users after project completion.

Furthermore, this old model introduces financial fragility.

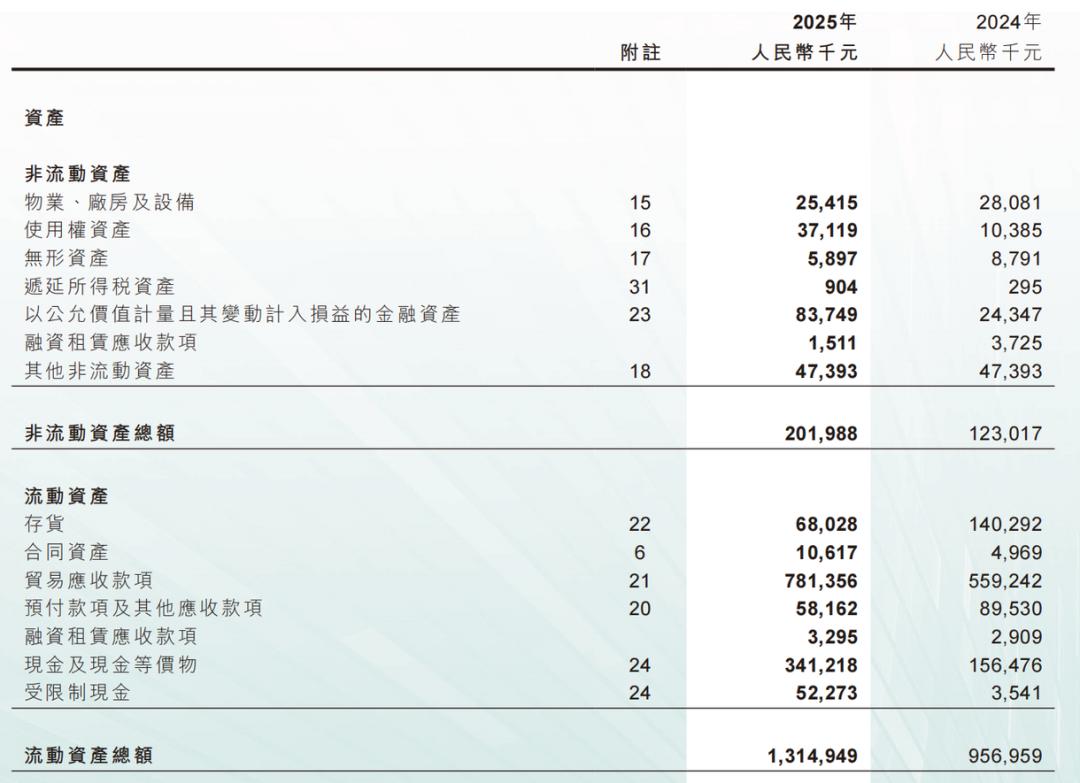

On one hand, payment collection cycles for government and enterprise projects are extremely long. By the end of 2025, Unisound's accounts receivable reached RMB 780 million, accounting for more than half of its total assets. From 2022 to 2024, accounts receivable turnover days ranged from 250 to 290. While turnover speed improved noticeably in 2025, payment collection still took nearly 200 days, meaning the company effectively financed clients for half a year.

On the other hand, the company has consistently operated at a loss, with deficits of RMB 370 million, RMB 380 million, RMB 450 million, and RMB 330 million in 2022, 2023, 2024, and 2025, respectively.

Whether viewed from a cash flow perspective (operating cash flow net amounts were -RMB 320 million and -RMB 210 million in 2024 and 2025, respectively) or a profitability perspective, Unisound lacks self-sustaining capabilities.

Unisound explicitly stated in its annual report that it is 'actively exploring the construction of a recurring revenue system through models such as API invocation and token-based billing,' indicating a transition from a heavy to a lighter operational model.

Models like API invocation and token-based billing are exemplified by 'Longxia,' a representative agent form.

One case study of seizing the 'Longxia' opportunity is Zhipu.

A significant portion of Zhipu's business also relies on project-based implementation with strong customization characteristics. However, benefiting from earlier platform-based Layout (layout) and the explosive popularity of Longxia, Zhipu's business has become lighter and more standardized, with commercialization no longer growing linearly. As of March 2026, Zhipu's MaaS platform had an ARR of approximately RMB 1.7 billion, representing about 60-fold growth over the previous year. Meanwhile, API business gross margins improved from 3.3% to 18.9%, with performance again acting as a catalyst for share price growth.

Longxia also triggered a recent sense of crisis for Huang Wei.

When Longxia became a sensation, Huang Wei felt anxious upon realizing the team's slow response. 'Later, I reflected that it wasn't that they didn't want to act; it's just that the existing organizational structure was designed for the original business model, leaving no extra personnel or bandwidth to address this,' he said.

Huang Wei's remarks reveal a deeper contradiction at Unisound: while technology has iterated to 2.0, the organizational structure supporting it remains stuck at 1.0.

Organizational structures must align with business models and profitability approaches. For Unisound, the anxiety sparked by 'Longxia' should not merely prompt an organizational review but serve as an opportunity to reshape its commercial DNA. After all, in the AGI marathon, technology determines starting speed, but the quality of the business model determines how far one can run.

-

![]()

Li Bin Claims, 'Denying the Pure EV Trend is Like Ostrichism.' What's Li Xiang's Take?

-

Lenovo: Liu Jun Turns Left, Yang Yuanqing Turns Right

-

Lenovo: Liu Jun Goes Left, Yang Yuanqing Goes Right

-

![]()

MiniMax Shares Unlock: Cornerstone Shareholders Show Long-Term Optimism, Yet Stock Plummets Nearly 30% in Two Days; Zhipu Also Sees Nearly 20% Drop Today

-

![]()

Single-Day Plunge of 40%: The 'First AGI Stock' Faces More Than Just Share Price Concerns

-

![]()

Ricoh and Fuji Hike Prices on Legacy Edge; Insta360 Poised to Disrupt Mirrorless Camera Market

-

![]()

Ricoh and Fujifilm Raise Prices in Tandem, Relying on Established Reputations; Insta360 Poised to Disrupt Mirrorless Camera Market

-

![]()

Strategic Shift in Photoelectric Sensing: Maxvision Secures Controlling Stake in CAS Optotech