Tech Titans Embrace Spin-offs, Boosting Value with Each Divestiture

07/10 2026

07/10 2026

402

402

A friend lamented that Zhipu was sold off too prematurely.

As the inaugural global AI large-scale model stock, Zhipu's share price skyrocketed from HK$116.8 at its January 8th listing to a peak of HK$2,980, achieving a market capitalization of HK$1.33 trillion at its zenith.

Given that its 2025 revenue stood at a mere RMB 724 million, with losses amounting to a staggering RMB 4.718 billion.

He was equally hesitant to part with his Xiaomi shares.

In June 2025, Xiaomi's stock price peaked at HK$61.45, only to plummet over the following year.

On June 26th of the same year, it bottomed out at just HK$21.3, with its market capitalization shrinking by over HK$1 trillion in a single year.

Of course, Xiaomi is not alone; industry behemoths such as Alibaba and Tencent have also witnessed sluggish stock performances in recent months.

The stark reality is that major conglomerates, once shielded by multi-business moats, have suddenly fallen out of favor with investors. Meanwhile, companies focused on future-oriented sectors like AI, semiconductors, and robotics are now in hot pursuit.

Consequently, the tech giants have taken note and begun to divest non-core businesses.

Image Source: AI

Take Kuaishou, for instance. On July 2nd, it announced that its independently operated subsidiary, Beijing Kling, had secured external capital injections totaling up to US$3 billion, with a post-investment valuation expected to soar to US$18 billion.

On July 3rd, the market capitalization of parent company Kuaishou stood at HK$184.3 billion, implying that Kling's valuation had surpassed 65% of Kuaishou's total market value.

Baidu serves as another prime example.

Kunlunxin embarked on its STAR Market IPO journey on May 8th and had already confidentially submitted a listing application to the Hong Kong Stock Exchange in January, with rumors swirling about a target valuation as high as US$50 billion.

Baidu's U.S. market capitalization hovers at US$38.887 billion, meaning the spun-off Kunlunxin is nearly valued at RMB 100 billion more than Baidu itself.

A wave of revaluation is subtly reshaping the tech company landscape.

01 The Spin-off Surge

Despite Baidu often being criticized for being 'early but late to the game,' Kunlunxin's strategy appears astute.

In 2010, Baidu commenced developing its AI computing architecture, unveiling the first-generation Kunlunxin in 2018 and achieving mass production by 2020.

In 2021, Baidu officially spun off Kunlunxin, completing its first round of financing with a post-investment valuation of approximately RMB 13 billion, with Baidu retaining a 57.67% stake.

Subsequently, the second and third generations of chips were mass-produced in 2021 and 2024, respectively, riding the wave of domestic AI chip substitution.

According to IDC, by 2025, Kunlunxin had secured a 7% market share in China's cloud AI accelerator market, ranking third.

After several rounds of financing, its valuation has surged from RMB 13 billion to the rumored US$50 billion today.

While Kunlunxin has toiled for over a decade, Kuaishou's Kling AI is merely two years old.

In February 2024, shortly after OpenAI released its AI video generation model Sora, Kuaishou launched its self-developed Kling AI in June of the same year.

:

:

Image Source: Screenshot from Kling's official website

In April 2025, Kuaishou established the Kling AI Business Division, and by the first quarter of 2026, Kling AI's revenue had exceeded RMB 650 million, marking a year-over-year increase of over 300%, with an annualized revenue run rate (ARR) nearing US$500 million.

Today, Kling's valuation may reach US$18 billion. According to Southern Metropolis Daily, citing sources, Kling AI plans to initiate its Hong Kong listing process within the next 12 months.

These two companies are not isolated cases; everyone is actively divesting non-core businesses.

Dreame once expanded to over 200 independent business units (BUs). Even after consolidating into four major businesses, its spun-off Magic Atom, focused on AI embodied intelligence, remains a significant bet within the Dreame ecosystem.

Hikvision spun off EZVIZ Network for listing in 2021 and is now preparing to spin off Hikrobot for a STAR Market IPO.

Additionally, overseas media reported earlier this year that Alibaba's AI chip subsidiary, Pingtouge, is poised for an independent listing with a valuation of up to US$62 billion.

Tech giants have shifted their focus from pursuing scale to specializing in excellence.

02 Valuation Uplift

From recent capital market performance, the most immediate benefit of spin-offs is, undoubtedly, soaring valuations.

Over the past six months, stocks with concepts like AI, robotics, semiconductors, and commercial spaceflight have surged across global equity markets.

There's even a joke circulating: 'No matter what business a company is in, its prospectus must mention AI.'

Today, the tech sector is more fragmented, and future prospects hinge on the specific business.

Once spun off, with clearer business lines, valuations tend to ascend.

Secondly, spin-offs enhance financial management for both parent and subsidiary companies.

Whether it's AI, chips, or robotics, these businesses are future cash cows but also current money pits.

Integrating them can be cumbersome.

New businesses devour cash, and no matter how much they explode as a 'second curve' in financial reports, they still drag down overall revenue and profits.

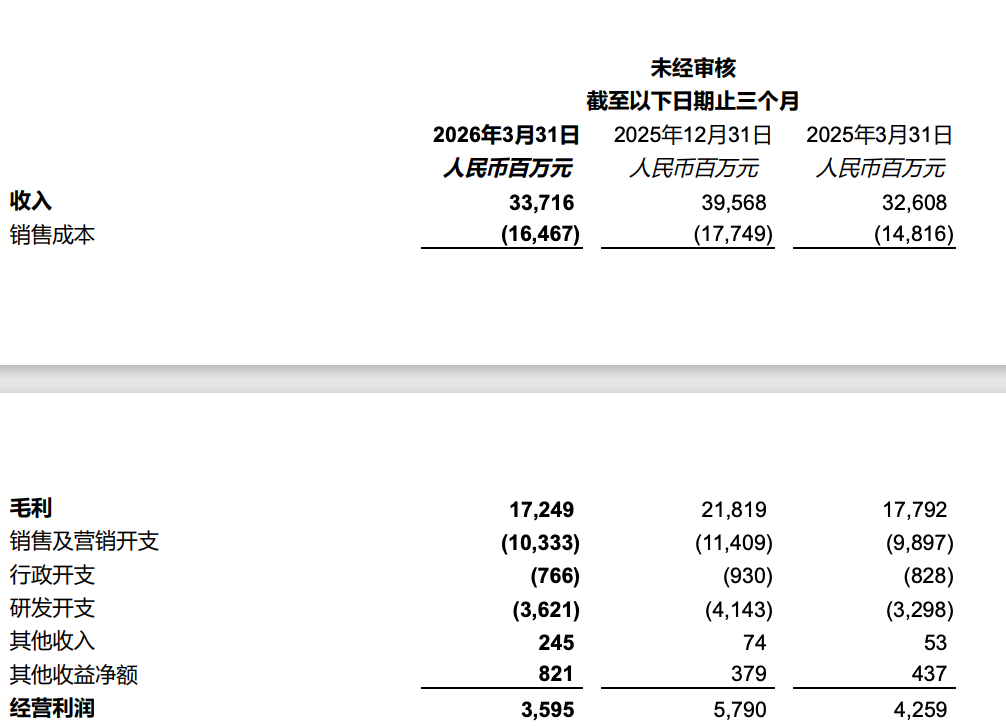

For instance, in the first quarter, Kuaishou's revenue was RMB 33.716 billion, a slight year-over-year increase of 3.4%; adjusted net profit was only RMB 3.374 billion, a significant year-over-year decline of 26.3%.

Research and development expenses were RMB 3.6 billion, a 9.8% year-over-year increase, while bandwidth and server hosting costs, depreciation, and amortization all witnessed double-digit growth.

Image Source: Kuaishou financial report

The massive short-term investment in new businesses, which are unlikely to turn a profit anytime soon, affects the capital market performance of tech giants.

But once spun off, the subsidiary burns cash to secure its future, while the parent company steadily earns profits—the logic is sound.

Another advantage is the streamlining and acceleration of new businesses.

Everyone is familiar with the common issues plaguing large companies, such as the popular essays about being 'trapped inside X.'

Large companies are bogged down by numerous levels and lengthy processes, making them slow to adapt.

Especially in sectors like AI and robotics, where technology iterates rapidly, being a step behind can mean being left behind.

After spinning off into independent companies, new businesses boast leaner teams, shorter hierarchies, and faster focus. They can also leverage stock options to attract technical talent, breaking the parent company's salary balance and starting with a light load.

Innovative companies fit seamlessly into the startup ecosystem.

03 Securing a Seat on the Next Wave

Both hardware and the internet are ushering in a new era of transformation.

This is driven by the impact of AI and internal factors.

A few years ago, many believed consumer electronics technology had reached its zenith.

Smartphones, the barometer of the mobile internet era, saw stagnant sales a decade ago, while new products like smartwatches, VR, and AR glasses have failed to become the next iPhone.

Major manufacturers are making fewer software and hardware updates, instead engaging in mergers and acquisitions to secure their positions in the existing market. Apps are growing in size and functionality, aspiring to meet all consumer needs within a single ecosystem.

Image Source: AI

Microsoft, Google, Alibaba, and Tencent—many major firms have taken this path.

The explosive growth of AI and robotics seems to have reignited the sense of anticipation reminiscent of the eve of the internet boom.

Where is the ticket for the next wave? This is the concern for all.

The essence of giants spinning off businesses is to proactively humble themselves and compete using startup tactics.

The key is to liberate new businesses from the vast parent system.

But spin-offs are not a panacea; every action has its trade-offs.

The most direct risk is the hollowing out of the parent company.

Spinning off the most promising businesses leaves the parent with mostly mature businesses experiencing slowing growth, potentially weakening its appeal to investors and talent.

Secondly, coordination costs may rise.

Previously, high-quality resources within the company could be shared, and financial and legal structures were mature.

After spin-offs, communication and resource-sharing efficiency between the two may decline, increasing the likelihood of redundant efforts.

Not to mention valuation bubbles.

The future visions painted by spun-off new businesses may seem enticing, but most are still in the stage of burning cash to acquire technology and market share.

With more and more new companies entering the market, competition will only intensify, and the investment period for many sectors seems endless for now.

-

Lenovo: Liu Jun Goes Left, Yang Yuanqing Goes Right

-

![]()

MiniMax Shares Unlock: Cornerstone Shareholders Show Long-Term Optimism, Yet Stock Plummets Nearly 30% in Two Days; Zhipu Also Sees Nearly 20% Drop Today

-

![]()

Single-Day Plunge of 40%: The 'First AGI Stock' Faces More Than Just Share Price Concerns

-

![]()

Ricoh and Fuji Hike Prices on Legacy Edge; Insta360 Poised to Disrupt Mirrorless Camera Market

-

![]()

Ricoh and Fujifilm Raise Prices in Tandem, Relying on Established Reputations; Insta360 Poised to Disrupt Mirrorless Camera Market

-

![]()

Strategic Shift in Photoelectric Sensing: Maxvision Secures Controlling Stake in CAS Optotech

-

![]()

Optical Communication and Robot Vision: OFILM’s Bold Transformation Amid a 460 Million Yuan Loss

-

![]()

From 100,000-GPU Computing Might to Industrial Efficiency: The Logic Behind AI4S-Driven Intelligence