Behind the Scenes of Token Factories' Rise as a Capital Market Sensation

07/13 2026

07/13 2026

329

329

The financing narrative in the large model industry is rapidly evolving. Six months ago, capital primarily chased foundational models themselves. Today, hot money is flowing to a more downstream segment: Token factories.

This Friday, the 2026 World Artificial Intelligence Conference (WAIC) will open in Shanghai, with the Token economy being one of the core topics of this year's event. Since late June, multiple capital events have occurred in the Token sector.

For instance, TrendHorizon Technology, which just announced the completion of its Series A funding, has raised over 1 billion yuan in total within six months. SiliconFlow previously submitted an application for listing on the Hong Kong Stock Exchange, with its platform achieving a peak daily Token throughput exceeding one trillion and registering over 10 million users. InfiniteCore AI disclosed that the Token call volume on its Agentic MaaS platform has surged over 20-fold since the end of last year, backed by nearly 50 investment institutions.

Capital and industry players alike believe that the next core bottleneck in the AI industry is deliverable, billable, and profitable services. The demand for inference services is no longer about how high the peak can be but whether they can be delivered stably, cost-effectively, and continuously. Whoever establishes efficiency barriers in this segment stands a chance to become an indispensable infrastructure layer in the AI industry chain.

However, as of now, there is no consensus on how this industry will ultimately succeed. SiliconFlow reported revenue of 55.33 million yuan in 2025, with a net loss of 345 million yuan and a gross margin of -24%. Many other companies have yet to continuously validate their business models. Bubbles and genuine value are churning in the same river.

I. The Business Model of Tokens: What It Is and What It Is Not

To understand the business logic of Token factories, it is essential first to clarify what Tokens are and what they are not.

From a technical perspective, Tokens are the basic units of measurement used by models when processing text, images, and speech. When a user asks a large model a question, the system converts both input and output into Tokens and bills accordingly. In this sense, Tokens are to AI services what kilowatt-hours are to electricity—they are units of settlement, cost accounting, and resource consumption.

However, the analogy should stop here. Tokens and electricity have a fundamental difference: electricity is a homogeneous commodity. What does that mean? One kilowatt-hour of electricity used for household lighting is physically indistinguishable from one kilowatt-hour used in a factory workshop.

Tokens are entirely different. One million Tokens generated by the same model could represent a lightweight generation of a casual conversation, a full-scale inference of a complex code refactoring, or even meaningless repetitive outputs. Their computational costs, requirements for precision and stability, and the ultimate commercial value generated can differ by orders of magnitude.

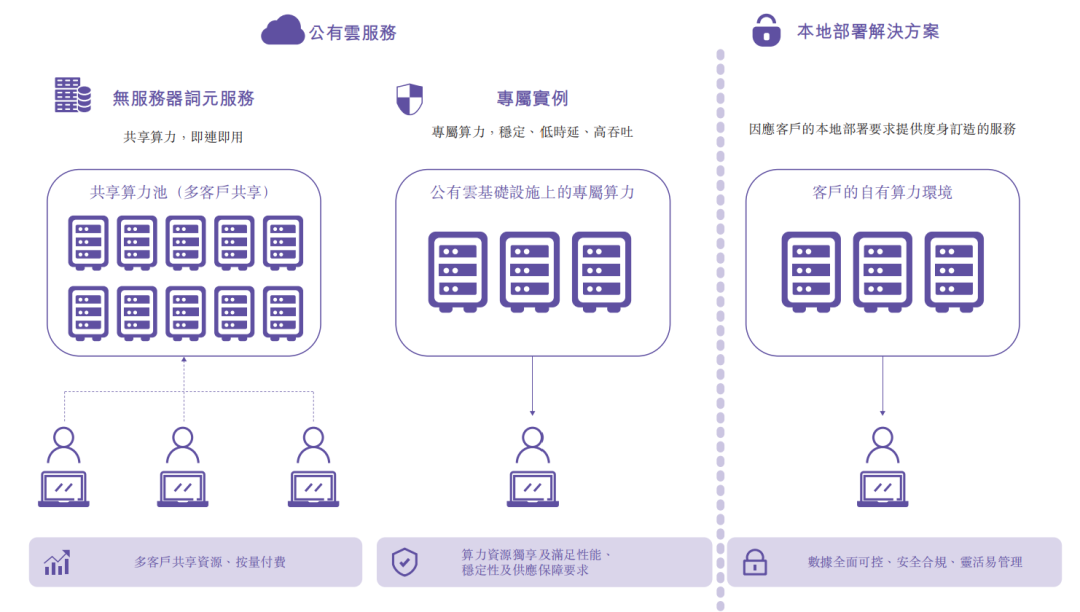

This difference directly determines the uniqueness of the Token factory business: it cannot sell merely the quantity of Tokens but must sell the quality of Tokens. Focusing solely on quantity would lead to an unfavorable situation similar to traditional CDN services—low barriers to entry, transparent pricing, and customers being able to switch providers at any time based on price comparisons. Only by focusing on quality can genuine barriers be established.

TrendHorizon Technology clearly understands this point. It explicitly positions itself as a high-quality AI Token production service provider and categorizes Tokens into layers: free chatbots correspond to low-speed, low-stability Tokens; developer packages correspond to medium-speed Tokens; and enterprise core production systems require high-speed, highly stable, long-context-supported high-quality Tokens. Different tiers of Tokens have entirely different requirements for Token latency, generation speed, concurrency, output stability, and structured call reliability.

This is not a new concept invented by TrendHorizon Technology. The evolution logic of the telecommunications industry from 2G to 5G is essentially the same—all generations can transmit information, but enterprise-level customers will not run their core businesses on high-latency, low-stability networks. AI services are undergoing a transition similar to that from 4G to 5G. As AI moves from casual chatting to coding, contract reviewing, and project management, Token quality becomes more critical than Token price.

SiliconFlow disclosed in its prospectus that its self-developed inference engine can reduce latency by up to 70%, increase throughput by three to five times, and dynamic quantization technology can reduce inference computational requirements by 60% to 80%. The significance lies in the fact that the same computational hardware can produce faster responses and lower costs after deep optimization.

Thus, most Token factory players emphasize deep optimization over broad access. For example, SiliconFlow does not compete with giants on the number of models but focuses on a few truly production-demanding top-tier models, pushing the effective Token output per unit of computational power to the extreme through model partitioning, memory management, and heterogeneous collaboration. This capability is fundamentally different from the intermediary model of being a model supermarket that repackages and resells hundreds of APIs.

II. The Window for Burning Money to Scale Is Still Open, but It's Narrowing

So, how should we view the current commercialization development of the Token industry? The answer is cautious optimism in the short term and long-term optimism.

Taking SiliconFlow's prospectus data as an example, its platform's registered users surged from 127,000 at the end of 2024 to 10.28 million in April 2026. During the same period, the average daily Token throughput climbed from 47.8 billion to 578.5 billion. Revenue jumped from 7.35 million yuan in 2024 to 55.33 million yuan in 2025, showing astonishing growth.

However, due to fixed costs, SiliconFlow still reported a net loss of 345 million yuan in 2025, with a gross margin of -24%, computational resource costs of 59.62 million yuan, and marketing expenses of 83.7 million yuan, indicating significant customer acquisition costs.

Considering the strong subsequent monetization value of Token subscribers, this is clearly a typical strategy of subsidizing to acquire users.

SiliconFlow also uses public cloud services as an entry point, attracting developers and enterprises to try its services at extremely low or even negative margins, hoping that some of these users will convert into high-margin dedicated instances or on-premises deployment customers. In 2025, its on-premises deployment revenue share dropped from 85.4% to 47.1%.

This bears similarity to the blitzscaling approach in the mobile internet era, but there is a fundamental difference between the AI infrastructure business and companies like Didi and Meituan back then: Token factories have extremely high fixed costs, but their network effects are significantly weaker. The reason is not complicated—computational power is often rented, technological optimization requires continuous investment in top talent, and customers do not necessarily experience better service just because more people are using a particular platform. The room for marginal cost reduction through scale expansion is far less steep than that of internet platforms.

Therefore, most companies are currently pursuing a genuinely healthy Token factory business model, which should be an efficiency flywheel rather than a financing flywheel.

What is an efficiency flywheel? Technological optimization reduces the unit cost of Tokens → lower prices attract more customers → more customers bring more real-world scenario feedback → real-world scenario feedback helps further optimize models and scheduling systems → optimized systems further reduce costs and enhance stability. The core lubricant of this flywheel requires engineering capabilities and scenario data. Therefore, Token factories must strive to explore downstream applications.

In contrast, if efficiency optimization takes effect, its impact will also be clearly reflected in the data. For example, some of the currently disclosed data from TrendHorizon Technology show that its unit computational power production efficiency has increased more than threefold since the Spring Festival, with total high-quality Token output increasing more than 30-fold. Some mature businesses have already broken even.

Next, Token companies only need to prove that when financing slows down and computational power procurement costs continue to rise, this efficiency engine can continue to operate independently. Only by navigating a complete stress cycle can we say that Token factories represent a sustainable business model.

III. Beyond Computational Power: Finding the Most Scarce Factor

Over the past three years, the dominant narrative in the AI industry has been one word: scarcity. There has been a shortage of GPUs, computational power, electricity, and data center space. This state of perpetual scarcity has fueled a massive investment boom in computational power infrastructure. Every construction of a smart computing center and every delivery of a 10,000-GPU cluster represents a forward bet on future AI demand.

However, in 2026, the market has begun to look for different influencing factors.

From a bottom-up supply perspective, with the continuous expansion of global computational power supply, accelerated localization of domestic chips, and continuous improvement in model inference efficiency, the availability of computational power itself is marginally improving.

It should be noted that this does not mean computational power is already surplus—high-end GPUs and access rights remain tight. However, pure computational power volume is transitioning from a scarce commodity to a bulk commodity. During this process, the weight of costs in areas such as electricity is beginning to rise. When a resource is no longer scarce, the competitive barriers built around it start to loosen.

Therefore, after considering factors such as business models and output capabilities, what this industry ultimately tests is no longer who has how many GPUs but who can achieve higher effective output with the same GPUs. This metric goes by different names in the industry: Token production efficiency, computational power conversion rate, and cluster uptime ratio. Regardless of the name, they all point to the same thing—the competitive logic of AI infrastructure is shifting from resource possession to operational efficiency.

This is a stage that warrants caution but is also full of opportunities. The construction of smart computing centers has experienced a certain degree of overemphasis on construction and underemphasis on operation in the past few years. Data centers have been built, and equipment has been installed, but there has been an insufficient number of paying customers.

In the narrative of computational power being king, this contradiction was easily masked by the expectation that future demand would catch up with supply. However, the current Token factory boom may be giving rise to another form of resource misallocation—renaming computational power idling as Token idling.

Building a Token factory is not difficult. Buying computational power equipment, accessing a few open-source inference engines, and connecting several mainstream model APIs are enough to declare Token production capabilities. The challenge lies in making these Tokens genuinely purchasable, usable, and valuable.

Whether Token factories can avoid repeating the plight of some smart computing centers hinges on who is paying for these Tokens. If customers are primarily free users attracted by short-term subsidies and price arbitrageurs, they will quickly churn once subsidies are reduced or competitors offer lower prices. Only if customers are enterprises genuinely using Tokens in production can Token factories become part of the productivity toolkit.

From a industrial chain (industry chain) perspective, the essence of Token factories is to do something many industries have experienced before: organizing upstream dispersed, complex, and non-standardized resources into downstream standard services that are directly usable, measurable, and scalable. This is no different from petroleum refining transforming crude oil into gasoline, asphalt, and chemical feedstocks.

Crude oil cannot be used directly in oil fields; it must undergo a series of complex decomposition and recombination processes to become finished oils and industrial raw materials for different purposes. Token factories aim to transform crude oil into different grades of finished oils. Different models, chips, and scenarios require entirely different oil grades: some pursue ultra-low latency, some maximize throughput, and some require stable long-context outputs.

Overall, players in the industry currently fall into roughly two paths. One path emphasizes scale and breadth, accessing as many models and chip types as possible to achieve broad coverage and become a universal supply base at the Token level. The other path emphasizes depth and focus, optimizing around a few top-tier models to maximize unit computational power output efficiency and exchange technological barriers for profit margins.

Neither path is inherently superior, but the latter's competitive barriers are more sustainable from an industry logic perspective—because its value does not depend on what resources it has but on how effectively it can utilize those resources. The former relies on scale barriers, while the latter relies on technological barriers. Scale barriers can be easily caught up with when capital is abundant, while technological barriers require time and talent and cannot be achieved quickly.

Therefore, the current financing and listing boom in the Token sector is essentially a race to seize the window of opportunity before the industry chain solidifies.

Once giants complete internal integration of the inference segment—cloud vendors like Alibaba Cloud and Volcano Engine are already bundling their model services into their cloud infrastructure, forming a closed loop from chips to models to applications—the space for independent Token suppliers will be compressed.

However, independent Token factories possess a structural advantage: neutrality. SiliconFlow supports over 170 models from different model companies, and TrendHorizon Technology serves customers covering top model vendors and internet platforms. They do not develop general-purpose large models themselves, do not compete directly with any model company, and do not bind themselves to any single chip vendor. This position represents a hedging choice for customers during a stage when industry division of labor is not yet stable—no one can predict which model will ultimately prevail.

Industry division of labor is never completed through theoretical deduction but naturally settles after countless rounds of trial and error in market competition. Regardless of how much foam (bubble) is mixed in, the current heat of Token factories at least indicates that the AI industry chain is undergoing a critical shift in value focus downward. Making models genuinely serve production and life will be the main theme of the future industry. Standing at the starting point of this trend, the story of Token factories has just begun.

Source: Songguo Finance

-

![]()

Why Hasn’t AI-Driven Payment Flourished Despite Tech Giants’ Push?

-

![]()

Intensify Efforts in the High-End Optoelectronic Semiconductor Sector! Aipu Dingchun and Jiangsu Meidong Forge a New Joint Venture

-

![]()

From Endoscopes to Optical Interconnects for AI Computing Power: A Veteran Optical Company's Strategic Shift

-

![]()

Behind the Scenes of Token Factories' Rise as a Capital Market Sensation

-

![]()

What Does MaaS Ultimately Bring to Chinese Cloud Providers? | In-Depth Industry Analysis

-

![]()

China’s Auto Resale Value Report Unveiled: AITO M9 Electric and Hybrid Variants Dominate Rankings

-

![]()

Dialogue with Huang Yangming: On the Eve of the Physical AI Boom, the Value of Data Infrastructure Begins to Materialize

-

![]()

The Experience is a Bit Unusual! Logitech G Cloud Review: Great Feel, but Not Ideal for Cloud Gaming