What Does MaaS Ultimately Bring to Chinese Cloud Providers? | In-Depth Industry Analysis

07/13 2026

07/13 2026

506

506

What does AI ultimately bring to cloud providers? Has cloud computing finally entered a new phase of growth, or have cloud providers simply adopted a new vocabulary to describe growth? If growth is occurring, where is it truly coming from?

Author | Dou Dou

Editor | Pi Ye

Produced by | Industry Insight

As 2026 reaches its midpoint, the narrative logic of China's cloud computing industry begins to shift.

A close observation of the contexts in which major cloud providers discuss their businesses in various public settings reveals a tacit understanding (tacit) agreement to reduce the singular focus on traditional TOB computing power growth, replaced instead by the frequent introduction of new concepts.

Specifically, in the first quarter of 2026, Alibaba Cloud's AI-related products achieved double-digit growth for the 11th consecutive quarter, accounting for over 30% of external commercial revenue for the first time; Baidu's AI Cloud GPU cloud surged by 184%; Tencent's enterprise services revenue increased by 20%, with management explicitly attributing it to "AI demand driving GPU, CPU, and storage resources"; Volcano Engine's large model invocation volume on China's public cloud grew 16-fold year-on-year.

It is clear that in the first half of this year, whether it is Alibaba Cloud, Baidu Intelligent Cloud, or Volcano Engine, the focus of their external disclosures has shifted towards AI-related metrics, such as AI cloud revenue, MaaS, model invocations, GPU computing power, Token consumption, and Agent platforms.

AI has become the protagonist in press conferences and earnings calls.

While these changes may seem like mere adjustments in financial reporting, they raise a new question: What does AI ultimately bring to cloud providers? Has cloud computing finally entered a new phase of growth, or have cloud providers simply adopted a new vocabulary to describe growth? If growth is occurring, where is it truly coming from?

I. From GPUs to Tokens: Cloud Providers Shift Growth Metrics

Looking back at the golden age of China's cloud computing over the past decade, the industry's underlying logic was almost entirely built on CPU general-purpose computing. Traditional TOB businesses primarily billed based on vCPU core counts, memory capacity, and storage bandwidth, with resource consumption assessments relying on this metric system for an extended period.

This model resembles "real estate leasing." Cloud providers offer computing, storage, and network resources, with enterprises paying based on actual usage scale. The more virtual machines a customer activates and the larger the hard drive capacity they mount, the faster the cloud provider's revenue grows.

However, with leading providers like Volcano Engine and Alibaba Cloud frequently emphasizing "AI Cloud" and "MaaS" in their earnings reports and press conferences, the metrics for measuring cloud computing resources have begun to change. The focus has shifted from CPU core counts to GPU utilization rates, and further to Token invocation volumes at the application layer.

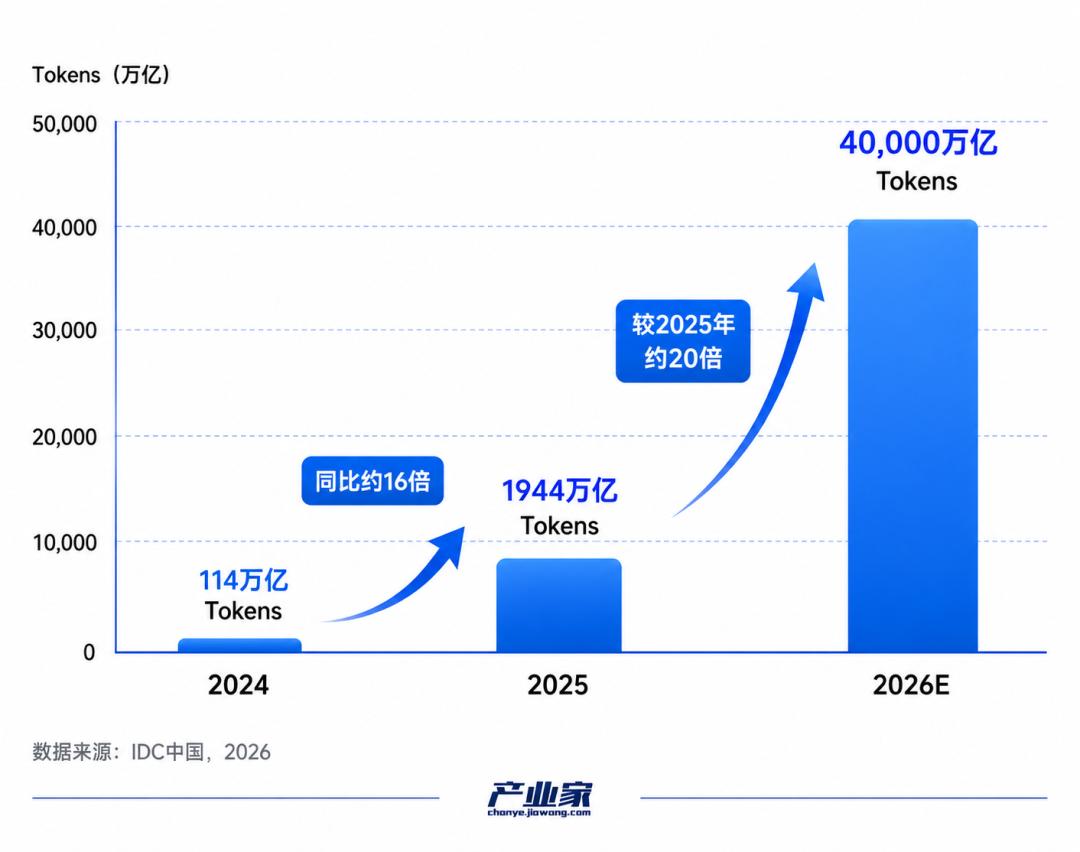

IDC's latest panoramic report shows that in 2025, China's public cloud large model invocation volume reached 1,944 trillion Tokens. IDC projects that by 2026, the annual Token consumption in China's MaaS market will rise to approximately 40,000 trillion times. Such growth rates would have been nearly unimaginable during the era when CPU core counts were the primary metric for resource consumption.

When examining specific enterprise examples, this "Token-driven" growth manifests more concretely and aggressively.

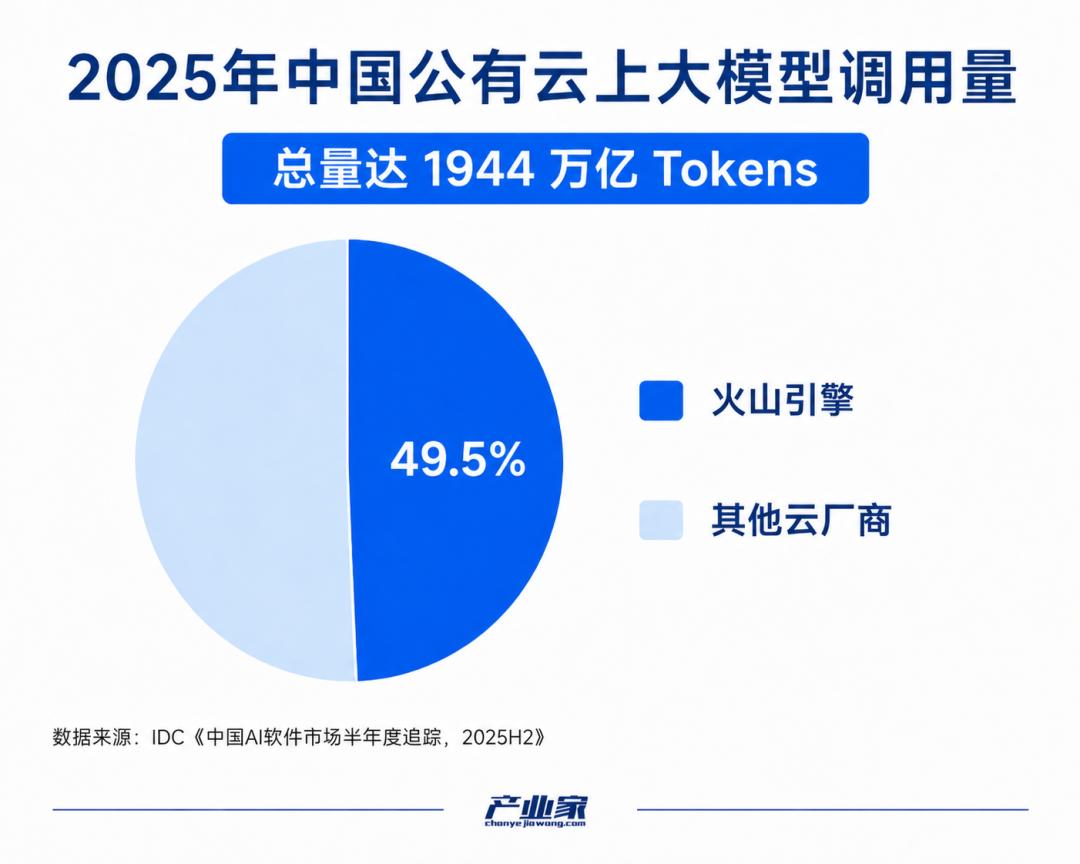

At Volcano Engine's Summer Force Conference in June 2026, the company proudly disclosed that its Doubao large model's daily Token invocation volume had surged past 180 trillion, achieving over a 10-fold explosive growth in just one year. Leveraging this massive and high-frequency consumption, Volcano Engine claimed a 49.5% market share in China's public cloud MaaS market.

Alibaba's Q1 2026 earnings report showed that Alibaba Cloud Intelligence Group's quarterly revenue reached RMB 41.626 billion, with AI-related product revenue accounting for over 30% for the first time, contributing RMB 8.971 billion in a single quarter. Supporting this core driver was an 8-fold year-on-year explosive growth in customer numbers on its MaaS platform, "Bailian."

From these publicly disclosed data and actions, it is evident that the growth momentum of AI businesses is not only real but also growing wildly within cloud providers' systems at a nearly frenetic pace.

However, when shifting focus away from these multi-fold or even thousand-fold "Token explosions" to examine the overall financial performance of cloud providers, reality casts a cold light.

According to the latest data from the China Academy of Information and Communications Technology (CAICT) and third-party research firms, from 2025 to the first half of 2026, the year-on-year growth rate of China's overall public cloud market has normalization (normalized) to the 8%-11% range. This pales in comparison to the golden era of general-purpose computing, when growth rates often exceeded 30% or even doubled.

In summary, behind this localized surge fueled by Tokens and GPUs, the true state of the broader cloud computing market is far from a full recovery. While the increment (increments) are fierce, China's cloud computing market has not witnessed an overall, high-spirited recovery, presenting an anomaly of "localized explosive growth while the broader market remains stagnant."

II. Beyond "Traffic Anxiety": The Truth Behind AI Cloud Growth

What is the truth behind AI cloud growth?

On the surface, the cloud computing market in the first half of 2026 appears extremely vibrant. An intense "traffic Entrance anxiety (entry point anxiety)" pervades all major cloud providers. To avoid falling behind in this AI marathon that will decide the next decade's fate, providers are striving to build their defenses at the application and ecosystem levels.

For example, Alibaba promotes collaboration between its Tongyi Qianwen App, DingTalk, and Tongyi Labs, hoping to establish AICoding tools like CodeWork as entry points for B-end programmers; ByteDance leverages its traffic advantage to keep Doubao at the forefront of C-end AI applications; Baidu relies on the DoMate and Wenxin Yiyan ecosystems, hoping to replicate its search business experience in smart cockpits and intelligent hardware.

However, from a longer-term perspective, traffic entry points and AI assistants are still in their nascent stages, with their commercial value and profitability yet to be fully validated. At this stage, they primarily serve strategic defensive functions. Cloud providers must secure these entry points but cannot immediately derive stable profits from them. Thus, their high hopes for new AI-driven revenue and profits remain focused on "selling computing power and Tokens."

But this business is no easy feat.

AI cloud and MaaS still involve high capital expenditures, relying on heavy asset depreciation and long-term recovery models. Cloud providers need to build high-standard green data centers, lay high-bandwidth fiber optics, procure expensive servers, and secure power supply indicators for GPU's high power consumption.

Data shows that Alibaba's property and equipment expenditures reached RMB 122.021 billion in FY2026, up about 45% from RMB 84.278 billion in FY2025. While not entirely attributable to AI cloud investments, this reflects the financial pressure from AI infrastructure expansion. Tencent's data points to a similar trend, with Q2 2025 capital expenditures reaching RMB 19.1 billion, up 119% year-on-year. Tencent management explicitly stated that some GPU and AI project investments have longer cycles, with natural time lags between investment and significant incremental returns. ByteDance is even evaluating raising its 2026 capital expenditures to as high as USD 70 billion, primarily for AI chips, data centers, and related infrastructure.

Meanwhile, traditional enterprises prioritize system stability and data security. Large model hallucinations remain unresolved, and enterprise AI project ROIs are not fully validated. This has led to extreme caution among a large number of traditional manufacturing, offline retail, and large financial institution TOB clients regarding connecting their core databases and operating systems to AI clouds. Except for internet, gaming, autonomous driving, and large model startups—industries naturally resonant with AI—most traditional enterprises remain on the sidelines.

If traditional enterprises, which support the broader market, are largely inactive, where do Alibaba Cloud's 40% external commercial growth rate and Volcano Engine's exponentially surging Token invocation volumes come from?

Specifically, the first factor is a complete overhaul of the core customer base.

During the CPU era, cloud providers' major clients included pan-internet apps, gaming firms, and government and enterprise clients in digital transformation. Today, AI newcomers like Yuezhi's Dark Face, Zhipu AI, and MiniMax, along with autonomous driving firms continuously investing in end-to-end large model R&D, have become the primary consumers of AI cloud resources. Lacking the capability to build their own large-scale data centers, much of the funding raised by large model startups ultimately flows into purchasing AI public cloud computing power from major providers. This represents a typical stage-specific net increment driven by "capital circulating within the ecosystem."

Second is the high average selling price (ASP) premium of computing power resources. While ASPs and profit margins for general-purpose CPU cloud resources were relatively fixed in the past, cloud providers now sell highly scarce, premium GPU computing clusters optimized through in-house R&D to these AI newcomers and automotive firms. For example, Alibaba Cloud's Pingtouge self-developed AI chips and GPU acceleration technologies achieved large-scale mass production in H1 2026, with over 60% of this computing power directly serving external commercial clients. The cost advantages from this self-developed hardware provide significant pricing flexibility when selling computing power, squeezing higher profit increments from existing revenue.

Finally, there is the internal settlement dividend from upgrades within internet giants' own business lines. Giants like Volcano Engine, Tencent, and Alibaba are comprehensively upgrading their search, e-commerce recommendation ad systems, and short-video distribution algorithms to deep learning and multimodal large models. This "old computing power to new computing power" replacement within conglomerates, while internally offset in consolidated financial statements, provides stable demand for cloud businesses, keeping AI computing power pool utilization rates consistently above safety thresholds and reducing large-scale infrastructure idleness risks.

Thus, the current AI cloud revenue explosion primarily comes from concentrated procurement of computing power by large model startups and GPU-driven core tech stack restructuring in pioneering industries. This increment features high concentration and high ASPs, aptly filling the gap left by traditional government and enterprise clients tightening their cloud budgets due to macroeconomic cycles. Through this structural replacement, the overall revenue curve of the cloud computing market has steeply ascended.

III. What Does MaaS Ultimately Bring to Cloud Service Providers?

What is worth exploring is when AI cloud can shed the Stage anxiety (stage-specific anxiety) and high energy consumption investments brought by technological disruptions and enter a healthy, steady growth phase.

In fact, during this AI transformation, cloud providers are gradually showing such trends.

For example, Volcano Engine's consecutive revenue target upgrades directly reflect changing industry winds. In early June 2026, reports emerged that Volcano Engine had raised its MaaS business's 2026 annual revenue target to RMB 15 billion. This rare move indicates that MaaS is transitioning from strategic investment to a scalable revenue source. Supporting this target is a continuously expanding model invocation scale. IDC data shows that Volcano Engine held a 49.5% share in China's 2025 public cloud large model invocation volume market, ranking first in the industry.

So, through what pathways does MaaS break the traditional cloud computing cycle of relying on "selling bare resources and price wars" to create new increments for cloud providers?

In the traditional cloud computing era, when enterprises migrated their businesses from Alibaba Cloud to Tencent Cloud, the process primarily involved data and system relocation, such as handling bandwidth, databases, and code migration. As long as competitors offered low enough prices, enterprises might switch platforms.

With the advent of MaaS, the situation changes.

Once enterprises connect their core business data to Alibaba Cloud's Bailian or Volcano Engine's Fangzhou platforms and spend months fine-tuning to develop business scenario-specific models and Agent systems, they form deep bonds with the platforms. Model parameters, contextual understanding capabilities, and the long-established invocation relationships between models and vector databases are difficult to replicate and migrate to other platforms through code alone.

This "ecosystem and algorithm stickiness" brings extremely high customer retention rates, locking in long-term, stable renewal increments for cloud providers.

Simultaneously, MaaS shatters the past ASP barriers in cloud computing, achieving geometric growth in customer base through "infinitely lowering entry standards."

In the past, SMEs and independent developers using GPU computing power often needed to rent multiple nodes, incurring monthly expenses of tens of thousands or even hundreds of thousands of yuan, leaving many long-tail customers unable to enter the market. MaaS transforms heavy asset investments into lightweight API invocations, with developers paying based on Token counts. Model interactions can be completed for a few cents or even fractions of a cent.

Alibaba Cloud's Bailian platform achieving an 8-fold year-on-year customer growth rate is inseparable from this low-barrier billing model. SMEs, individual developers, and campus startup teams, which rarely contributed to cloud computing revenue in the past, have now entered cloud providers' billing systems. The overall increment stacked by this long-tail effect is becoming the most cannot be ignored (non-negligible) capillary revenue stream in cloud providers' overall picture.

More importantly, as a traffic magnet, MaaS is efficiently driving Composite cross consumption (composite cross-consumption) of high-margin, foundational cloud resources around cloud providers.

In real-world industrial practice, when a company frequently invokes large models on an MaaS platform for business reasoning, it must synchronously procure the cloud provider's vector databases, high-throughput object storage, and security cloud products to ensure real-time data updates and precise retrieval, as well as compliance for the model's output content. In other words, while MaaS charges ahead with what may appear to be low-price or even free API strategies, it silently drives "full-stack sales" of high-margin foundational software products under the cloud provider's umbrella.

This composite consumption of second- and third-order peripheral resources triggered by first-order large model invocations represents the most imaginative extended increment that MaaS brings to cloud providers.

While MaaS in 2026 remains a typical "capital expenditure first, profit release later" uphill battle, and while the underlying commercial laws of cloud providers' heavy asset operations remain unchanged in this vigorous and dynamic (vigorous) computing restructuring, cloud computing has completed its most essential value evolution in advancing AI technology's industrial adoption and transforming AI into a truly universal productivity tool.

Nowadays, the criterion for measuring the excellence of a cloud provider is no longer how many acres of data centers it has built in the physical world or how many CPU cores it has sold, but how many Tokens it efficiently, inclusively, and securely processes every day for the real economy across various industries in the digital world.

-

![]()

Why Hasn’t AI-Driven Payment Flourished Despite Tech Giants’ Push?

-

![]()

Intensify Efforts in the High-End Optoelectronic Semiconductor Sector! Aipu Dingchun and Jiangsu Meidong Forge a New Joint Venture

-

![]()

From Endoscopes to Optical Interconnects for AI Computing Power: A Veteran Optical Company's Strategic Shift

-

![]()

Behind the Scenes of Token Factories' Rise as a Capital Market Sensation

-

![]()

What Does MaaS Ultimately Bring to Chinese Cloud Providers? | In-Depth Industry Analysis

-

![]()

China’s Auto Resale Value Report Unveiled: AITO M9 Electric and Hybrid Variants Dominate Rankings

-

![]()

Dialogue with Huang Yangming: On the Eve of the Physical AI Boom, the Value of Data Infrastructure Begins to Materialize

-

![]()

The Experience is a Bit Unusual! Logitech G Cloud Review: Great Feel, but Not Ideal for Cloud Gaming