Relying on trucks to make money, Pony.ai awaits the spring of Robotaxi

10/21 2024

10/21 2024

745

745

Following WeRide, another L4 autonomous driving company is preparing to go public.

On October 18, Pony.ai, an autonomous driving service provider, submitted an IPO prospectus to the U.S. Securities and Exchange Commission (SEC). Following Baidu, Waymo, and Tesla, Pony.ai has become another player preparing to expand its Robotaxi operations in October this year, according to the prospectus's fund usage plan.

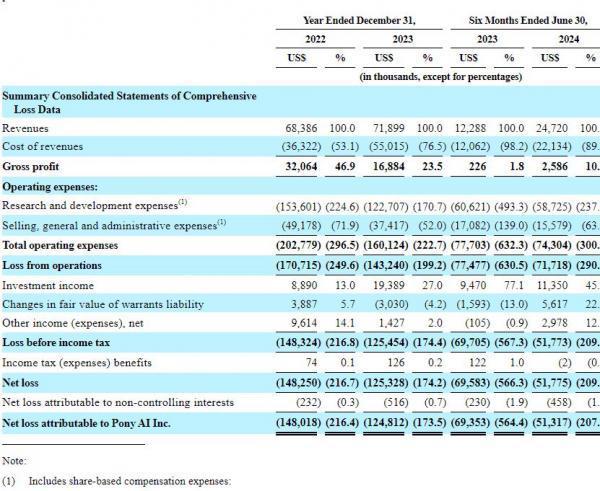

The prospectus shows that Pony.ai's revenues in 2022, 2023, and the first half of 2024 were US$68.39 million, US$71.9 million, and US$24.72 million, respectively, for a cumulative revenue of over US$165 million (approximately RMB 1.2 billion). However, the overall revenue scale is still relatively small.

Notably, Pony.ai's revenue in the first half of 2023 was only about one-seventh of its annual revenue, significantly different from the approximately half ratio of most companies. In the first half of 2024, revenue increased by nearly 100% year-on-year, a rapid growth rate, but it's difficult to predict full-year revenue.

Over the same period, Pony.ai's net losses were US$148 million, US$125 million, and US$51.78 million, respectively, with an overall narrowing trend in losses. The net loss in the first half of this year fell significantly by 25.6% year-on-year, indicating stricter cost control measures by the company.

Like many L4 autonomous driving companies, Pony.ai is still in the early stages of commercialization. The current primary source of revenue – the autonomous driving fleet – is still relatively small, with a total of fewer than 500 vehicles (250+ Robotaxis and 190+ self-driving trucks). The application in passenger and freight transportation is still in a phased pilot stage.

At a time when L4 autonomous driving companies are turning to L2 to seek faster profitability, Pony.ai is the only one that insists on pursuing L4 business.

Currently, although the L4 business is still in its early stages, Pony.ai is striving to get through the long period before the Robotaxi boom through trucking and technology licensing, supporting the company's long-term R&D investments.

Good news is that based on the operations of Pony.ai, Baidu, and Waymo, the Robotaxi industry has now largely transitioned from technology validation to seeking economies of scale.

"When Pony.ai was founded in 2017, I told the team that the industry might take another eight years to become profitable, which coincides with 2025," said Lou Tiancheng, CTO of Pony.ai, in an interview.

With the sudden boom in Robotaxi in 2024, Pony.ai has finally ushered in its own 'spring.'

Pony.ai has quietly transformed from a provider of autonomous driving technology services to an operator.

Behind this is a fundamental shift in Pony.ai's business model.

In terms of overall revenue, although Pony.ai has generally shown growth over the past two years, the quality of its revenue has continued to decline. The prospectus shows that Pony.ai's gross profit margin has fallen sharply from 46.9% in 2022 to 10.5% in the first half of 2024.

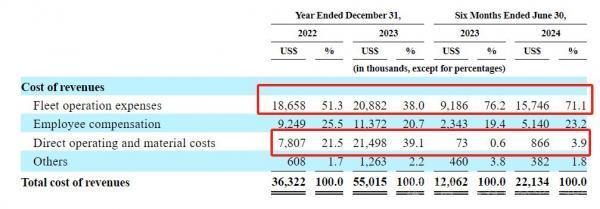

The decline in gross margin indicates that Pony.ai's revenue model is becoming increasingly challenging. Previously, Pony.ai relied primarily on 'selling software services,' but now, revenue mainly comes from operating autonomous truck fleets.

Pony.ai's primary revenue sources are Robotaxi (autonomous taxis), Robotruck (autonomous trucks), and technology licensing. Over two and a half years, Pony.ai's revenue structure has undergone significant changes.

Specifically, the revenue share of technology licensing (generally associated with higher gross margins) decreased from 54.2% in 2022 to 22.3% in the first half of 2024, while Robotruck operations increased correspondingly from 32.7% to 73.0%, becoming the absolute focus of revenue. As for Robotaxi, which holds the greatest industry expectations, it has yet to gain significant traction.

Changes in revenue and gross margin are related to the unique characteristics of these three businesses.

In trucking operations, Pony.ai officially entered the Robotruck market in 2021 and partnered with Sinotrans in 2022 to establish Qingzhi Logistics as a controlling shareholder. The establishment of the joint venture has allowed Pony.ai to record the deployment costs and revenues of over 160 of its 190+ Robotrucks on its books, leading to a sharp increase in business revenue share and costs.

Second, regarding technology licensing revenue, although Pony.ai only provided a two-year data comparison, it is evident that revenue from this business has been growing. The decline in gross margin in 2023 was primarily due to increased material demands for projects. The combination of these two factors has led to significant changes in Pony.ai's gross margin and revenue share.

Finally, there is Robotaxi, which is still in its infancy. With only 250+ Robotaxis, Pony.ai struggles to generate substantial revenue.

However, good news is that based on first-half 2024 data, assuming Pony.ai's Robotaxi fleet has 250 vehicles, the average daily revenue per vehicle is approximately US$26. Compared to Baidu's Apollo Go, Pony.ai's Robotaxi essentially ties with Apollo Go in terms of average daily orders (15 per day), but with an average fare that is more than double that of Apollo Go (considering subsidies, the average fare is around RMB 5).

In other words, Pony.ai's Robotaxi commercialization efforts have not only been successful but have also outperformed Apollo Go, which has already gained significant traction.

In summary, Pony.ai's current operating status is relatively smooth, contrary to the perception from a few years ago that L4 companies were struggling. The company has achieved high growth in its Robotruck business, with steady revenue growth in technology licensing, and promising commercial results in Robotaxi operations.

Moreover, while continuing to expand its business, Pony.ai has proactively reduced expenses.

Comparing 2023 and the first half of 2024, Pony.ai's total operating expenses decreased from US$78 million to US$74 million, reflecting a conservative overall investment strategy. Based on its 2023 cash reserves, the company has enough funds to ensure safe operations for approximately three years. In other words, if the Robotaxi boom does not materialize in 2024, Pony.ai is prepared for the long term.

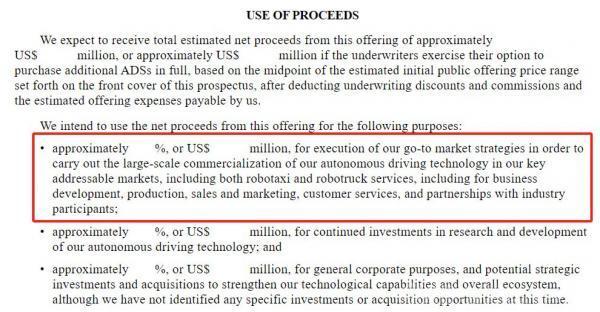

According to the prospectus's fund usage plan, Pony.ai's primary goal in this IPO, similar to Baidu and Waymo's actions in October this year, is to expand the commercial scale of autonomous vehicles.

Is Pony.ai ready for the Robotaxi boom?

As the largest independently operated L4 autonomous driving company in China, Pony.ai's every move has garnered significant attention.

The most crucial aspect is technology. Similar to Tesla's FSD, Pony.ai's autonomous driving employs an end-to-end architecture based on a single model. However, unlike FSD, which relies heavily on real-world data for training, Pony.ai focuses more on building world models through 'simulation.'

This approach stems from Pony.ai's experience in developing L4 technology from the ground up, which has led it to recognize that data is a double-edged sword for end-to-end intelligent driving models.

Indeed, in today's mainstream end-to-end intelligent driving development model, most vendors, including Baidu and Tesla, attach great importance to the value of data. After all, under the end-to-end development model (including 'staged' and One Model approaches), vendors can not only save costs by leveraging data-driven training instead of specialized development but also enhance the riding experience by mimicking the driving behavior of experienced drivers through their models.

However, Lou Tiancheng believes that this training method limits the intelligent driving system's ability to surpass human-level performance. "The essence of end-to-end or large language models is merely fitting existing data without providing any intelligent logic. Therefore, the model's capabilities are constrained by the performance of the data," he explained. In other words, human data can no longer guide AI advancements.

How can we break through the upper limit of end-to-end intelligent driving capabilities driven by real-world driving data?

Pony.ai has built a world model capable of accurately replicating and dynamically responding to real-world conditions. By allowing AI to 'freely explore' during the training process, Pony.ai's autonomous driving system can find optimal driving strategies that surpass human driving, thereby enhancing safety.

This technological philosophy has enabled Pony.ai to operate its Robotaxi fleet with minimal human intervention.

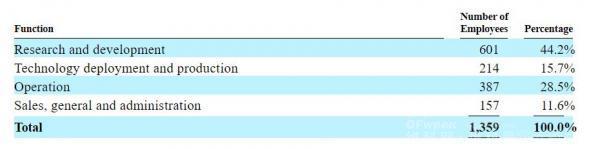

According to the prospectus, Pony.ai's pure R&D team currently comprises only 601 members. This team size and composition closely resemble Waymo's model from five years ago (totaling 950 people, with 350 in software engineering). In contrast, automakers like Xpeng Motors are significantly larger. In May this year, Xpeng's Chairman He Xiaopeng announced plans to expand the company's intelligent driving team by 4,000 employees.

Of course, this difference is also related to the number of vehicles supported by the technology. Automakers tend to have much larger engineering teams than L4 vendors, as they simultaneously develop both traditional and end-to-end autonomous driving systems. However, as end-to-end systems become more prevalent, automakers' intelligent driving teams are expected to become more streamlined.

Meanwhile, Pony.ai's autonomous driving technology advantages enable its AI algorithms to transcend vehicle and platform limitations. The same autonomous driving system (virtual driver) can be deployed across Robotaxi, Robotruck (and potentially future mass-produced passenger vehicles), regardless of sensor hardware, end-to-end training, intelligent driving deployment, or data processing.

This means that in the foreseeable 'land grab' competition within the Robotaxi industry, Pony.ai can leverage its universal autonomous driving capabilities across different vehicle models to continuously generate higher-margin software service fees (virtual driver). Driven by this software revenue model, Pony.ai can shed its identity as a mere operator of autonomous vehicle fleets and achieve higher profits and valuations.

As such, Pony.ai's primary focus now is to rapidly expand its fleet operations and validate the capabilities and profitability of its Robotaxi and Robotruck services on a larger scale as soon as possible.

Perhaps GAC Motor's 'emergency investment' in Pony.ai before its IPO filing and the unveiling of the Bozhi 4X Robotaxi model in collaboration with Toyota at this year's Beijing Auto Show signal that automakers are eagerly awaiting their entry into the Robotaxi industry.

Remember that in 2022, many autonomous driving companies collapsed during the 'capital winter' due to delays in meeting expectations for autonomous driving technology. Just two years later, Robotaxi is on the brink of widespread adoption, with only funding and policy as the remaining hurdles to achieving economies of scale.

-

![]()

The Surprisingly Significant Impact Difference Between Quiet and Noisy Cars!

-

![]()

Breaking Through Storage Cycle Barriers: How AI Large Models and Coding Technology Synergize to Drive Transformation in the Security Industry

-

Facilitating the Slimming of Camera Modules! O-film Obtains Utility Model Patent for Periscope-Type Reflective Component

-

![]()

Hikvision Raytine’s Millimeter-Wave Body Imaging Security Inspection Device Achieves ECAC SSc Category A Standard Level 2.1 Certification for European Civil Aviation

-

![]()

Global Market Share for Security Windows Hits 26%! This Optical 'Little Giant' Makes Its Debut on NEEQ

-

![]()

The Evolutionary Path of Agent Engineering: From Prompt to Harness by Zhang Yutao, Co-founder of Moonshot AI

-

![]()

Profits and stock prices are both declining, so why are executives from these auto companies increasing their purchases?

-

![]()

Burning Tens of Billions of Dollars, Yet No Unified Definition for World Models