Exorbitant Computing Power Costs Drive Meta to Act

07/07 2026

07/07 2026

496

496

Last week, Bloomberg reported that Meta is venturing into the cloud infrastructure business, with plans to lease out computing power externally. This news sent ripples through the AI hardware sector and caused jitters in Neocloud, a company heavily reliant on Meta as its primary client. The market began to speculate about a potential glut in computing power, with pessimism spreading even to the storage sector, which had recently shown strong fundamentals.

Let's cut to the chase. Dolphin Research offers the following insights:

(1) Considering the magnitude of the market decline, investor sentiment may have overreacted. Yesterday's market reaction seemed to be more of a chain reaction, triggered by signs that short-sellers' expectations were materializing amidst a backdrop of crowded long positions.

(2) However, this doesn't imply an immediate market correction. With short-term highs in industrial logic sparking disagreements, a period of digestion and adjustment is necessary, or the emergence of new positive information to counteract pessimism and rebuild confidence. Consequently, speculative funds may choose to retreat, while external bullish funds may adopt a wait-and-see approach rather than blindly buying in.

(3) Whether Meta's foray into computing power leasing is a 'temporary business move' or a 'planned long-term strategy,' it is undoubtedly more beneficial than detrimental for Meta. In the short term, it may lead to a sentiment-driven recovery in valuation (P/E), but we believe the turning point for a sustained turnaround still hinges on the progress of Meta's internal large models and Meta AI.

We maintain that frequent changes in Meta's internal organizational structure and strategy make a complete fundamental turnaround unlikely in the short term (e.g., within this year).

(4) The extent to which Meta's computing power leasing can bolster its fundamentals depends entirely on the amount of 'idle computing power' Meta possesses, which is likely to fluctuate with changes in company strategy and the computing power environment. Dolphin Research has made calculations based on certain assumptions for reference only.

From Buyer to Scalper: Meta's Dilemma?

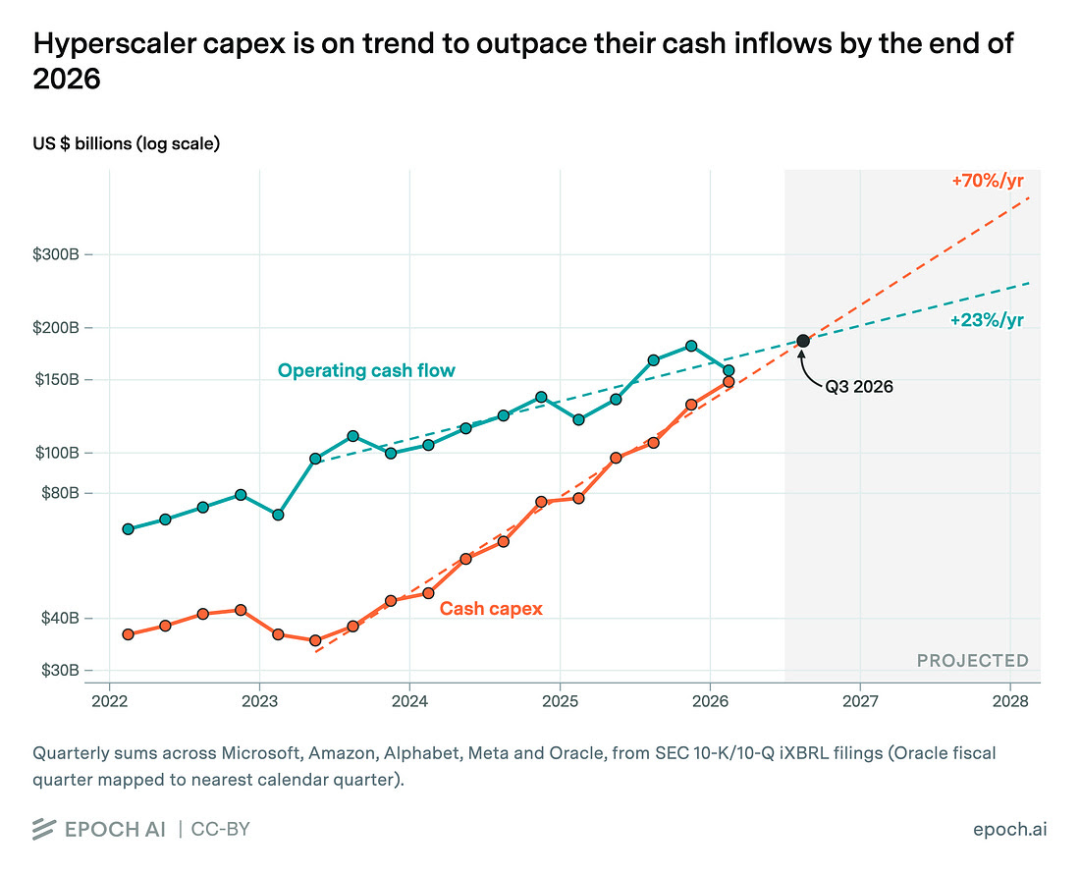

The capital expenditures (Capex) of end clients are the sole pillar supporting the entire computing power industry chain, and only a handful of major tech giants currently have the financial muscle to sustain this. Since the latter half of last year, Meta, Google, and Amazon have been raising funds through various channels, sparking market concerns about when these 'tech titans' will exhaust their resources. This logic has become a valuation curse for the current computing power industry chain, occasionally resurfacing to stir up speculation.

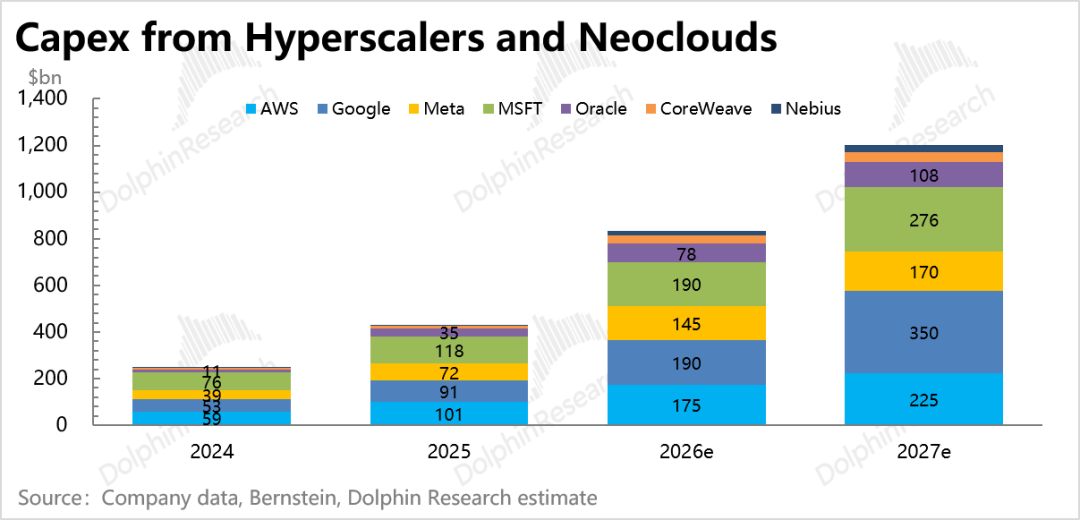

Meta is currently one of the world's top buyers of AI computing power, alongside Google, Microsoft, and Amazon, all of which own or lease multi-gigawatt-scale data centers. From a contribution perspective, Meta's 2026 Capex budget of $145 billion accounts for over 17% of the global total.

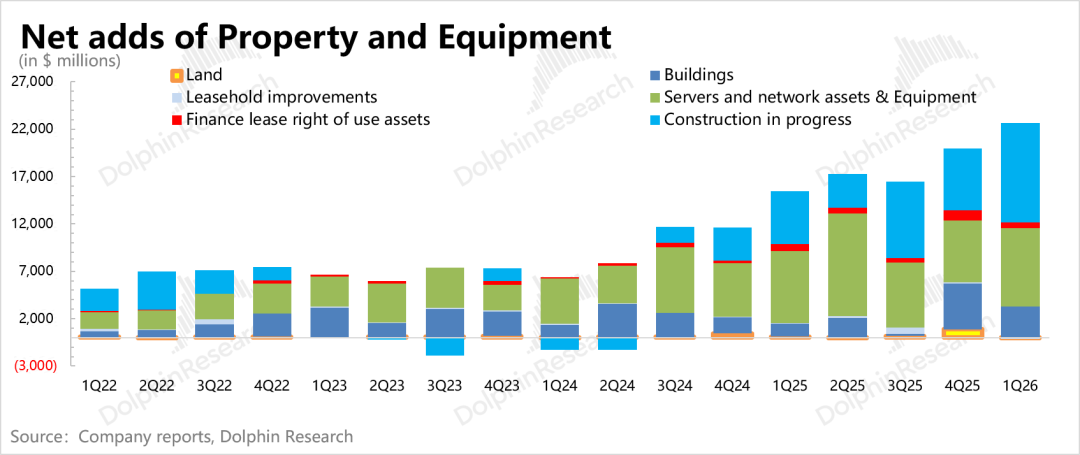

Over the past two years, Meta has accumulated a significant stash of H100/200 cards, along with some Blackwell and AMD MI300X models. By the end of 2025, its total equivalent computing power will reach 2.5 million H100 cards, roughly equivalent to 2 gigawatts. However, these H100/200 cards are primarily used for inference, offering relatively low economic utility for training large models with massive parameters, long contexts, and multimodal capabilities.

Therefore, from an optimal allocation standpoint, since the current leasing premium for older cards like H100/200 is exceptionally high, and Meta cannot leverage this computing power to enhance the training of its next-generation Muse Spark model, leasing it out to recoup some cash seems like a viable strategy.

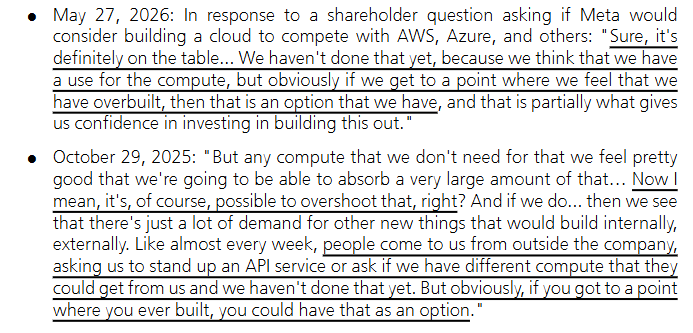

However, Meta's transformation from the most aggressive buyer of computing power to a seller, akin to a scalper, has been interpreted by the sensitive market as an industry-wide 'computing power glut.' At the shareholder meeting late last month, Zuckerberg mentioned that many clients were approaching Meta to lease computing power at high prices. If Meta indeed feels it has overbuilt and has idle capacity, it would consider leasing it out.

At the time, the market seemed to react indifferently, especially since Meta had just raised its 2026 Capex budget in its Q1 earnings report (increasing the median by $10 billion to $135 billion), indicating a strong demand for computing power that hardly suggested a strategic shift. Meanwhile, Google had just imposed restrictions on Meta's computing power supply, while Meta itself had secured a long-term computing power supply of 1.6 GW with Crosue in June.

In fact, Meta has faced a barrage of negative news in the past two months following its Q1 earnings report. Besides the demoralizing effect of falling behind in the technological race (the large model Muse Spark released in April initially seemed to narrow the gap with Tier 1 models but has since fallen behind again), the most critical issue lies in organizational culture—frequent adjustments in strategy and organizational structure have left the team confused and unfocused.

Therefore, the timing of this revelation is likely linked to the internal chaos of its self-developed system. Until Meta's large model catches up to Tier 1 standards, there will be no significant improvement in Meta AI's intelligent experience or large-scale applications of Meta Business Agents and Meta AI robots in the short term.

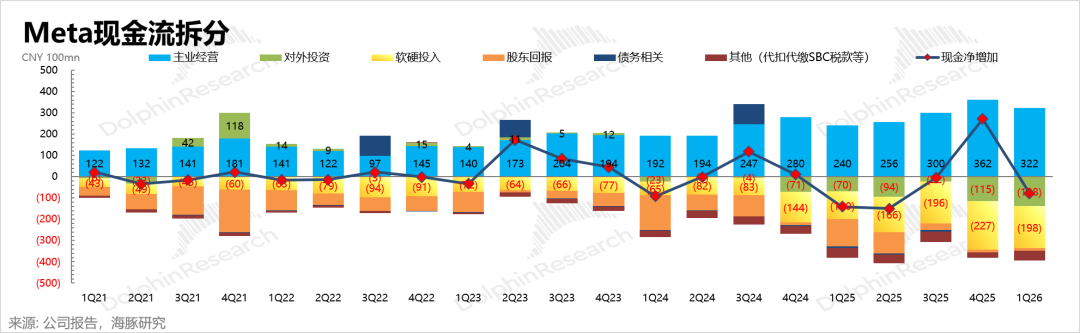

Leasing computing power can directly and effectively generate AI monetization revenue for Meta, alleviating market concerns about the ROI of its hefty Capex investments and worries about further deterioration in profits and cash flow in 2027.

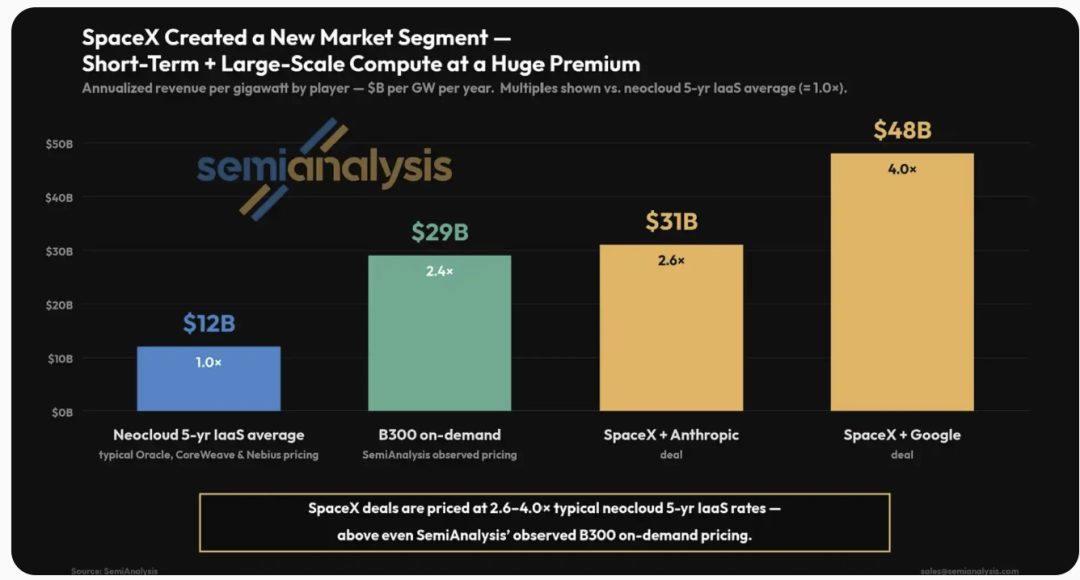

Coupled with xAI's recent signing of several multi-billion-dollar contracts, which have resulted in short-term premium rates skyrocketing due to immediate demand fulfillment (according to Dolphin Research's calculations, the annualized revenue per GW exceeds $30 billion, 2-3 times the industry's normal price), and considering the B300 system deployment cost of $40-50 billion per GW, the cost can be recovered in just one and a half years. Such a lucrative ROI from selling computing power at a premium is hard for Meta to ignore.

Meta Will Not Willingly Exit the Battlefield

However, Dolphin Research believes that Meta, like xAI, is not entirely withdrawing from the large model competition. Selling idle computing power and focusing on cutting-edge computing power do not equate to reducing overall computing power investments.

As mentioned in our previous in-depth report on SpaceX, xAI's two computing clusters—the H100-based Colossus 1 and the GB-series Colossus 2—have Colossus 1 currently fully leased to Anthropic, while Colossus 2 will continue to handle the training of Grok 5 and subsequent advanced models, with only a portion available for external leasing.

Similarly, Meta's computing power slated for external leasing is reportedly primarily from its frenetic stockpiling of H100/H200 cards in previous years, while advanced computing power like the GB and Rubin series will still be used for the continuous training of core large models like Muse Spark.

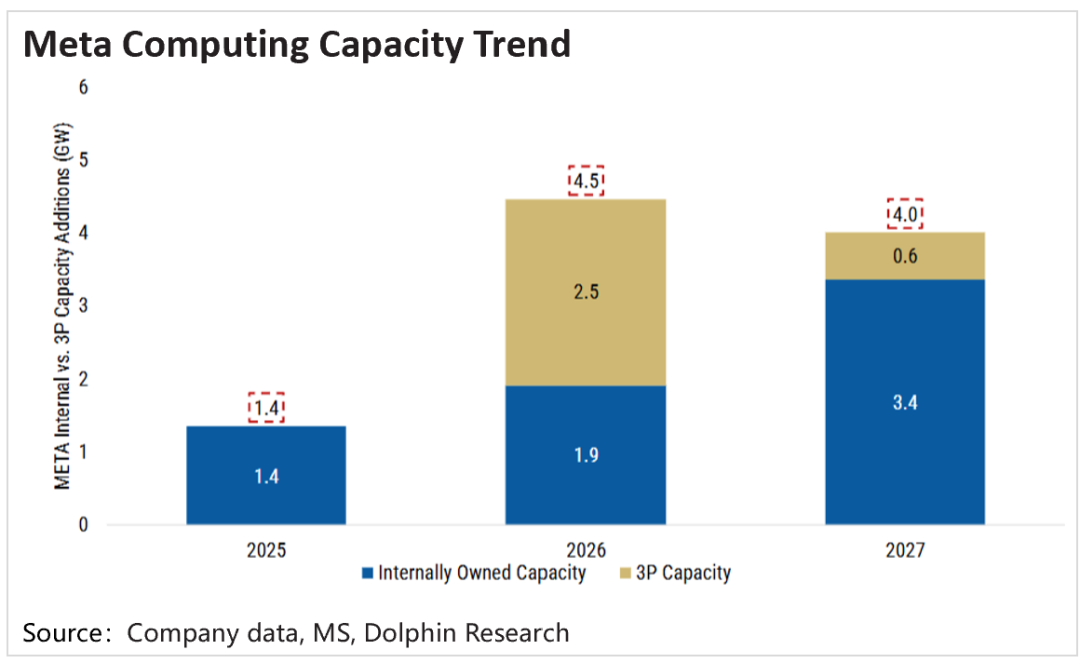

According to public information and industry forecasts, Meta possesses the world's largest 'AI-related' data center computing capacity. By the end of 2027, Meta is projected to have a total computing capacity of 10 GW, combining self-built and externally procured resources.

(1) Self-owned capacity: By the end of 2025, Meta will have 2 GW (equivalent to 2.5 million H100 cards). With the progress of the Hyperion project, an additional 2 GW and 4 GW are expected to be added in 2026 and 2027, respectively. By the end of 2027, Meta's self-owned computing capacity is projected to reach 8 GW.

(2) Leased capacity: Since early 2024, Meta has signed cumulative computing power contracts totaling 10 GW with third-party cloud providers, with CoreWeave, Nebius, and Google being the main suppliers. According to SemiAnalysis estimates, Meta signed over 5 GW of new third-party cloud-hosted computing power contracts in the first half of 2026 (multi-year locked-in contracts).

Although CoreWeave has stringent signing rules to ensure short-term contract fulfillment, Neocloud will inevitably face competition from former major buyers turned computing power lessors in the long run.

Therefore, while the market may still harbor doubts and controversies about whether Meta will halt Capex increases due to external computing power leasing, the intensified competition in computing power leasing is bound to impact Neocloud's logic and valuation expectations.

How Much Can Meta Gain from This Move?

Returning to Meta, based on the above analysis, we believe that whether Meta is leasing computing power short-term or preparing for long-term sales, it can at least dispel some market uncertainties, leading to a bidirectional recovery in EPS and valuation.

According to Bloomberg, Meta's computing power leasing operations likely fall into two categories:

One is similar to Amazon AWS's Bedrock product, offering computing power + models as a bundled service; the other is directly leasing raw computing power like Neocloud (given Meta's lack of advantage in large models).

In the current seller's market, Meta's computing power leasing revenue largely depends on how much 'idle computing power' it is willing to release. Given the current situation, if Meta adopts an aggressive approach and starts leasing computing power in the second half of this year, Dolphin Research believes that, in such a short timeframe, it will likely focus on leasing raw computing power (as bundling large model APIs would require improving sales and after-sales support teams).

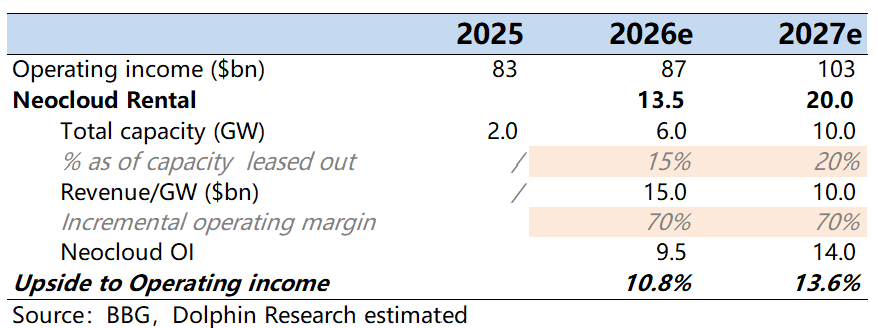

Currently, Meta operates 2-3 GW of AI computing power, with an additional 10 GW of self-built capacity expected to come online by 2027. Without adding new capacity, the total computing power reserve (self-built + leased) is projected to reach 10 GW. Considering Meta's self-developed large models and AI Agent plans in the next two years, Dolphin Research assumes that 15% and 20% of its total operational computing power will be leased out in 2026 and 2027, respectively.

Since market consensus expectations already factor in data center-related costs (depreciation, electricity, etc.), even at the current Neocloud's five-year average contract price (significantly lower than immediate demand prices), with annualized leasing revenue of $10-15 billion per GW, the additional net profit increase for Meta's existing terminal profit expectations is relatively high (after deducting some sales expenses, electricity costs, platform support, etc., and assuming a marginal profit rate of 70%, compared to the normal profit rate of 20-40%).

Based on these not overly aggressive assumptions, Dolphin Research estimates that Meta's cloud computing power leasing could yield a 10-15% net profit increase. Following the news of Meta's computing power leasing, its stock price rose 9% on the day but quickly fell back nearly 5% the next day, reflecting some correction in short-term computing power panic sentiment among investors.

Meanwhile, a complete fundamental turnaround still awaits further progress in Meta's internal self-development, especially in large model iterations to narrow the gap with Tier 1 models. This suggests that Meta's valuation pressure relative to other Mag 7 companies may persist for some time.

- END -

// Reprint Authorization

This article is an original work by Dolphin Research. Reproduction requires authorization.

// Disclaimer and General Disclosure

This report is for general comprehensive data purposes only, intended for users of Dolphin Research and its affiliated institutions for general reading and data reference. It does not consider the specific investment objectives, investment product preferences, risk tolerance, financial situation, or special needs of any individual receiving this report. Investors must consult with independent professional advisors before making investment decisions based on this report. Any investment decisions made using or referring to the content or information in this report are at the investor's own risk. Dolphin Research shall not be liable for any direct or indirect responsibilities or losses arising from the use of the data contained in this report. The information and data in this report are based on publicly available sources and are for reference purposes only. Dolphin Research strives to ensure but does not guarantee the reliability, accuracy, and completeness of the information and data.

The information cited or the viewpoints articulated in this report should not be interpreted as an offer to sell, nor as a solicitation of an offer to purchase, securities within any jurisdiction. Furthermore, they do not constitute advice, inquiries, or recommendations concerning relevant securities or associated financial instruments. The information, tools, and materials presented in this report are not intended for distribution to, or utilization by, any individual or entity in any jurisdiction or country where such distribution, publication, availability, or use would contravene legal or regulatory provisions, or would impose any registration or licensing obligations on Dolphin Research and/or its subsidiaries or affiliates within that jurisdiction.

This report exclusively mirrors the personal perspectives, insights, and analytical approaches of the respective authors and does not represent the official position of Dolphin Research and/or its affiliated entities.

This report is compiled by Dolphin Research, which holds exclusive copyright ownership. Without the prior written consent of Dolphin Research, no institution or individual is permitted to (i) produce, copy, reproduce, duplicate, forward, or create any form of copies or reproductions in any manner, and/or (ii) directly or indirectly redistribute or transfer to other unauthorized individuals. Dolphin Research reserves all associated rights.

-

![]()

The Surprisingly Significant Impact Difference Between Quiet and Noisy Cars!

-

![]()

Breaking Through Storage Cycle Barriers: How AI Large Models and Coding Technology Synergize to Drive Transformation in the Security Industry

-

Facilitating the Slimming of Camera Modules! O-film Obtains Utility Model Patent for Periscope-Type Reflective Component

-

![]()

Hikvision Raytine’s Millimeter-Wave Body Imaging Security Inspection Device Achieves ECAC SSc Category A Standard Level 2.1 Certification for European Civil Aviation

-

![]()

Global Market Share for Security Windows Hits 26%! This Optical 'Little Giant' Makes Its Debut on NEEQ

-

![]()

The Evolutionary Path of Agent Engineering: From Prompt to Harness by Zhang Yutao, Co-founder of Moonshot AI

-

![]()

Profits and stock prices are both declining, so why are executives from these auto companies increasing their purchases?

-

![]()

Burning Tens of Billions of Dollars, Yet No Unified Definition for World Models