How Alibaba Can Shake Off the 'Valuation Discount' Label Amid a Long-Awaited Rebound

07/13 2026

07/13 2026

342

342

Legend has it that King Gordias of Phrygia tied his chariot to an intricately knotted rope, with the ends hidden in layers of tangles. An oracle declared: He who unties this knot shall rule Asia.

For centuries, countless sages tried and failed. Then Alexander the Great arrived, drew his sword, and slashed through the millennium-old knot in one stroke.

In 2026, China’s internet giants face their own Gordian Knots. E-commerce, search, social, and local services—the core businesses built over two decades—have formed intertwined systems: each thread has logic, each carries baggage, and together they create deadlocks.

Take Alibaba as an example. Facing the AI-era transition, Alibaba holds unique advantages: a full-stack AI layout, Tongyi large models, cloud computing growth, and T-Head’s chip progress—a rare domestic asset.

Yet since this year, its stock price slid from around HK$180 to below HK$90; Tencent fared no better, retracing a third from its peak.

By mid-July, Alibaba’s stock finally staged a long-awaited strong rebound. This bullish candlestick after a yearlong plunge prompts investors to ask a deeper question: What does the market fear in this rollercoaster? Can Alibaba leverage this rebound to shatter its valuation discount?

In our view, the underlying logic of the sharp valuation pullback among Chinese internet stocks is shared: legacy businesses face downward industry valuations, mature growth businesses offer limited imagination, and AI has yet to build stable cash flow cycles.

Alibaba stands out as the most closely watched case. Using it as a lens, we dissect the crux of current valuation challenges for Chinese internet stocks and attempt to answer investors’ most pressing question: How to address the valuation discount.

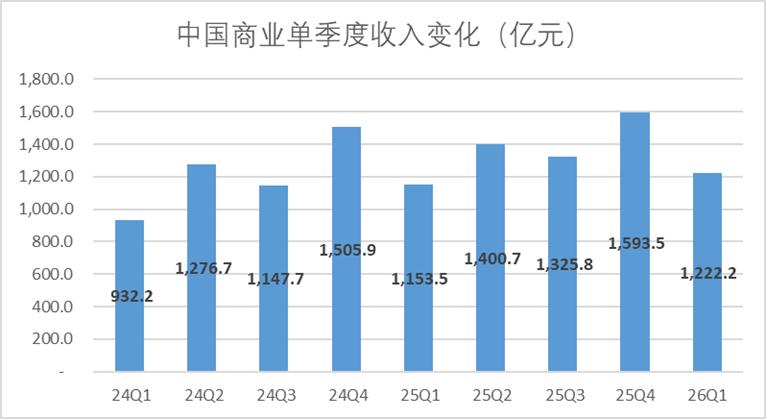

Before discussing valuations, we must examine fundamentals. By growth rate alone, Alibaba’s e-commerce has not performed poorly in the past two years.

In Q1 this year, Alibaba’s China commerce segment reported RMB 122.2 billion in revenue, with e-commerce contributing RMB 96.3 billion, down less than 1% YoY. Meanwhile, total retail sales of consumer goods grew 2.4% YoY, while online retail sales of goods and services rose 8.0%, with online goods retail up 7.5%. In this quarter, Alibaba’s e-commerce growth lagged the broader market.

However, one quarter of relative weakness proves little. From Q2 2024 through Q3 last year, driven by customer management revenue growth, Alibaba’s China commerce actual growth consistently outpaced quarterly online retail growth. Over the longer term, Alibaba’s e-commerce foundation remains solid. For a platform of such scale, these results did not come easily.

But two objective facts remain.

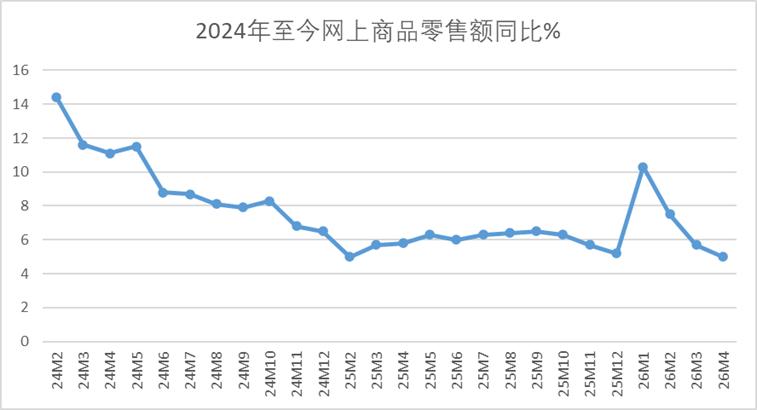

First, overall e-commerce growth is slowing, while head-to-head competition intensifies.

From 2024 to now, despite strong stimulus policies like local consumer vouchers and national subsidies, online retail growth has trended downward. CICC research estimates e-commerce platform growth will slow to ~8% in 2026, significantly below 2025’s 12%.

Moreover, the e-commerce market now shows a clear “hammer-shaped” concentration: in 2022, CR2 (top two players) held 60% market share, CR5 84%; by early this year, CR2 fell to 57% while CR5 surged to 93%. The tail has been cleared, leaving only capital-heavy players like ByteDance, Pinduoduo, and JD.com—horizontal competition drives little incremental growth.

Second, capital interest in e-commerce platforms is fading.

AI’s suction effect on capital markets is too strong; most funds shun predictable traditional internet businesses. Since last year, Goldman Sachs and Morgan Stanley have repeatedly cut target prices for traditional e-commerce platforms. From a forward earnings multiple perspective, JD.com’s 2027 forward P/E is just 6.9x—leaving little room for Alibaba’s e-commerce valuation.

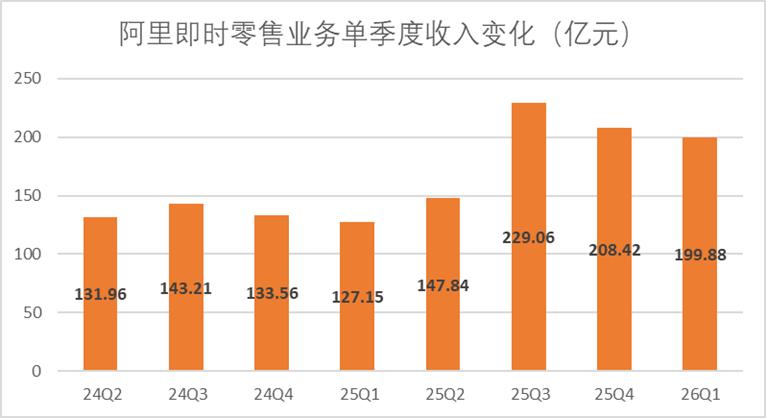

The core business remains, but more players are vying for shares. With e-commerce competition intensifying, valuations naturally stagnate. More critically, the new growth from instant retail looks far from compelling.

Starting in Q2 2025, Alibaba began disclosing quarterly instant retail data. As the latest entrant to the food delivery wars, Alibaba achieved Periodic achievements (phased results). In Q1 this year, its instant retail segment grew 57%, matching rival Meituan’s market share.

The issue is that instant retail’s allure cannot sustain a valuation narrative.

Alibaba’s cost control has struggled since the food delivery wars began. Despite clear anti-burnout rhetoric, subsidies have not meaningfully declined, nor has unit economics (UE) improved as expected. Everbright Securities forecasts instant retail’s average UE will remain negative at -RMB 1.8 in FY2027, -RMB 0.8 in FY2028, and break even in FY2029.

More critically, instant retail’s ability to drive Alibaba’s core e-commerce site has yet to materialize in valuation-relevant financials. As mentioned earlier, Alibaba’s e-commerce growth lagged the industry in Q1 this year—meaning instant retail’s synergy with e-commerce remains unrealized.

Excluding e-commerce synergies, even if instant retail builds a profitable model shortly, its profit contribution would be limited. JPMorgan reports that Uber Eats’ global profit margin is just 3.3%—food delivery remains a low-margin grind worldwide.

Instant retail has secured Alibaba a ticket to “near-field e-commerce,” and its market share gains prove execution. But markets never pay a premium for heavily loss-making businesses. For Alibaba, the growth narrative remains unsexy from a valuation standpoint.

Beyond traditional businesses, Alibaba is among the few domestic firms with a full-stack AI layout—a clear rarity. Its “Tongyi large model + Alibaba Cloud + T-Head Semiconductor” stack positions it alongside global tech giants in infrastructure.

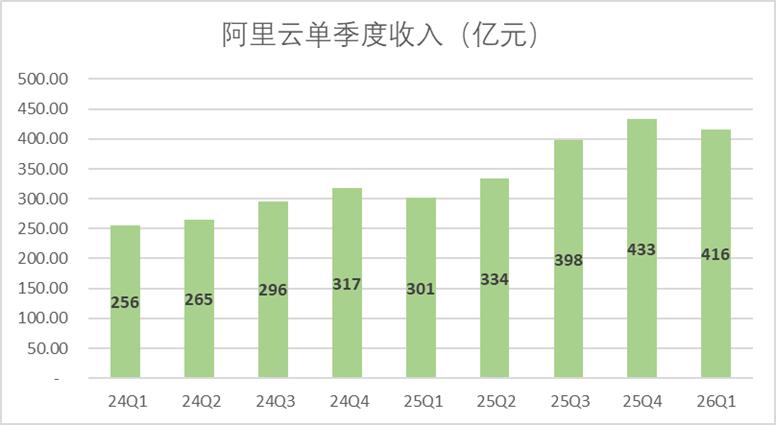

Yet valuations reflect no such premium. Take Alibaba Cloud:

· Compared to global cloud + hardware/software leaders, Microsoft Azure grew ~40% YoY in Q1 2026. Deutsche Bank estimates Azure’s true gross margin trajectory: ~60% in FY2024, 56% in FY2025, falling to 52% in FY2026. Azure now accounts for ~20% of Microsoft’s revenue, implying an overall forward P/E of ~34x.

· Compared to global cloud + e-commerce peers, CMB International values Amazon AWS at 28x P/E and 15x EV/EBITDA. CMBI uses 17.6x forward EV/EBITDA.

Using SOTP to value Alibaba: its e-commerce business (domestic + overseas) assumes a PE-TTM of ~6x (mainstream e-commerce valuation range). Over the past 12 months (excluding flash sales impact), profit was ~RMB 189 billion, implying a valuation of ~RMB 1.13 trillion. Instant retail, referencing Meituan and discounting for offline business (80% discount), is worth ~RMB 360 billion. Cainiao, valued at $20 billion three years ago pre-IPO, assumes a 50% discount, or ~RMB 70 billion in actual value.

Thus, the market values Alibaba Cloud at ~RMB 280 billion. While its growth matches Azure and AWS, its profit margin is low at just 9.1% in Q1 this year, implying an actual P/E of ~20x—still well below AWS and Azure.

What’s the crux? Alibaba’s AI narrative lacks closure.

First, investors doubt Alibaba’s cash flow capacity.

With legacy businesses suppressing profits, Alibaba has engaged deeply in both e-commerce and instant retail wars while ramping up AI capital spending to ~RMB 100 billion annually. Cash flow pressure is immense.

Second, Alibaba’s AI models have yet to build commercial moats around core capabilities.

From Anthropic, a leading AI large model firm, we see countless commercialization paths—but only those tied to productivity can sustain a trillion-dollar company. The viable routes are programming and office applications.

Coding capability is a critical gap all domestic foundation model firms must fill, including Alibaba’s QianWen. Additionally, DingTalk’s products have yet to drive meaningful office market innovation. While Alipay’s AI narrative spreads rapidly, it strays off course and cannot anchor the broader strategy.

Until coding and office applications prove viable, the AI investment cycle cannot close. Massive capital spending demands strong commercial feedback—until then, criticism will persist.

Returning to the opening question: the mid-July rebound lifted Alibaba’s stock from below HK$100 to above HK$110. But this rebound fixes sentiment, not valuations.

Alibaba faces three challenges: e-commerce profits are eroding amid competition, instant retail burns cash for market share, and AI capital spending swells without a closed commercial loop. On the same profit statement, cash flow tightens, expectations lengthen, and the valuation discount emerges.

The rebound offers a window. As market sentiment warms, investors re-examine asset quality. Alibaba holds rare full-stack AI assets, a leading domestic cloud business, and T-Head’s chip progress. Fear obscured these below HK$100; the rebound can illuminate them again.

But whether rebound turns to reversal depends on whether the market believes Alibaba can plug each profit hole. E-commerce profits must stabilize, instant retail losses must narrow, and AI investments must find the shortest path to commercialization. Failure in any area means the rebound stays a rebound.

Mount Hua is perilous—the only way is up, but Alibaba is weighed down. From e-commerce to instant retail to AI, its valuation story spans three chapters. Each chapter has logic, yet the market applies a blanket discount. Full-stack AI’s rarity is nearly unmatched domestically—a clear expectation gap exists, but closing it takes time.

Beyond waiting, Alibaba has a proactive option.

As we revealed in “How Xiaomi, Midea, and Other Chinese Industrial Giants Can Escape the ‘Bigger = Stronger’ Fallacy,” global industrial giants’ experiences over the past decade repeatedly prove: when a conglomerate’s business logic, growth curves, and capital attributes fully diverge, spin-offs are the most effective valuation repair tool.

General Electric split into three independent firms (healthcare, energy, aviation); Western Digital separated hard drives and flash storage for listing; Siemens divested healthcare and energy. Each move unlocked asset value suppressed by conglomerate discounts.

After Western Digital’s split, its combined market cap surged over 20x. General Electric rebounded from bottom, while Siemen’s three businesses now price independently by industry logic.

Alibaba’s dilemma mirrors these industrial giants’ past stages. E-commerce is a mature cash cow; instant retail is a growth business burning cash for market share; Alibaba Cloud and AI are full-stack tech platforms. These assets have entirely different risk appetites, valuation methods, and capital needs—crowded onto one profit statement, they drag each other down. E-commerce profits are consumed by instant retail and AI investments; the market cannot value each business clearly, so it discounts all.

Spinning off Alibaba Cloud and AI businesses would yield immediate results.

First, Alibaba Cloud could escape e-commerce’s valuation ceiling and directly benchmark against AWS and Azure’s valuation frameworks. The market currently implies a ~20x P/E for Alibaba Cloud, while AWS and Azure trade at significantly higher multiples. Second, e-commerce and instant retail would remain in the parent company, priced under a hybrid mature cash cow + growth business model, clarifying the valuation framework. Third, post-spin-off, each business unit could raise capital independently, ending mutual capital expenditure crowding and easing cash flow pressure.

The global industrial conglomerate spin-off trend conveys a clear logic: a company’s ballast is not merely revenue scale, but high-barrier, specialized core assets. When business logics diverge beyond a single narrative, unbundling and letting each asset price according to its industry rules is faster and more certain than waiting for a holistic market re-rating.

The wise appreciate mountains; the sagacious, water. Viewing mountains differently reveals distinct landscapes. Some see majesty, others peril; some glimpse the arduous climb from the back. But the mountain’s contours remain unchanged. Market sentiment discounts are fleeting; asset quality endures.

For investors, discerning the mountain’s true shape takes time. But the swiftest sword to shatter valuation discounts? Alexander demonstrated that 2,300 years ago.

This article is based on public information and serves for informational exchange only, not as investment advice.

-

![]()

Why Hasn’t AI-Driven Payment Flourished Despite Tech Giants’ Push?

-

![]()

Intensify Efforts in the High-End Optoelectronic Semiconductor Sector! Aipu Dingchun and Jiangsu Meidong Forge a New Joint Venture

-

![]()

From Endoscopes to Optical Interconnects for AI Computing Power: A Veteran Optical Company's Strategic Shift

-

![]()

Behind the Scenes of Token Factories' Rise as a Capital Market Sensation

-

![]()

What Does MaaS Ultimately Bring to Chinese Cloud Providers? | In-Depth Industry Analysis

-

![]()

China’s Auto Resale Value Report Unveiled: AITO M9 Electric and Hybrid Variants Dominate Rankings

-

![]()

Dialogue with Huang Yangming: On the Eve of the Physical AI Boom, the Value of Data Infrastructure Begins to Materialize

-

![]()

The Experience is a Bit Unusual! Logitech G Cloud Review: Great Feel, but Not Ideal for Cloud Gaming